Vornado 2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

No. 13-3148 in the UNITED STATES COURT of APPEALS for THE

Case: 13-3148 Document: 20-2 Filed: 01/10/2014 Pages: 43 No. 13-3148 IN THE UNITED STATES COURT OF APPEALS FOR THE SEVENTH CIRCUIT INTERCON SOLUTIONS, INC., Plaintiff-Appellee, v. BASEL ACTION NETWORK AND JAMES PUCKETT, Defendants-Appellants. ON APPEAL FROM THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS Case No. 12-CV-6814 (Hon. Virginia M. Kendall) _____________________________________________________________________________________________________________________ BRIEF OF AMICI CURIAE ADVANCE PUBLICATIONS, INC., ALLIED DAILY NEWSPAPERS OF WASHINGTON, AMERICAN SOCIETY OF NEWS EDITORS, ASSOCIATION OF ALTERNATIVE NEWSMEDIA, THE ASSOCIATION OF AMERICAN PUBLISHERS, INC., BLOOMBERG L.P., CABLE NEWS NETWORK, INC., DOW JONES & COMPANY, INC., THE E.W. SCRIPPS COMPANY, HEARST CORPORATION, THE MCCLATCHY COMPANY, MEDIA LAW RESOURCE CENTER, THE NATIONAL PRESS CLUB, NATIONAL PRESS PHOTOGRAPHERS ASSOCIATION, NATIONAL PUBLIC RADIO, INC., NEWS CORPORATION, NEWSPAPER ASSOCIATION OF AMERICA, ONLINE NEWS ASSOCIATION, PRO PUBLICA, INC., RADIO TELEVISION DIGITAL NEWS ASSOCIATION, REPORTERS COMMITTEE FOR FREEDOM OF THE PRESS, SEATTLE TIMES COMPANY, SOCIETY OF PROFESSIONAL JOURNALISTS, TIME INC., TRIBUNE COMPANY, THE WASHINGTON NEWSPAPER PUBLISHERS ASSOCIATION, AND THE WASHINGTON POST IN SUPPORT OF DEFENDANTS-APPELLANTS AND REVERSAL _____________________________________________________________________________________________ Bruce E. H. Johnson Laura R. Handman Ambika K. Doran Alison Schary DAVIS WRIGHT TREMAINE LLP DAVIS WRIGHT TREMAINE LLP 1201 Third Avenue, Suite 2200 1919 Pennsylvania Avenue, NW Seattle, WA 98101 Suite 800 (206) 622-3150 Washington, DC 20006 (202) 973-4200 Thomas R. Burke DAVIS WRIGHT TREMAINE LLP Counsel for Amici Curiae 505 Montgomery Street, Suite 800 San Francisco, CA 94111 (*Of counsel listed on inside cover) (415) 276-6500 Case: 13-3148 Document: 20-2 Filed: 01/10/2014 Pages: 43 OF COUNSEL Richard A. -

New York Fourth Quarter 2001 Analyzes: CBD Office Retail Apartments Suburban Office Industrial Local Economy Real a Publication of the Global New York Vol

NATIONAL REAL ESTATE INDEX M M ETRO New York ETRO Vol. 32 Fourth Quarter 2001 M M ARKET ARKET Analyzes: Reports: CBD Office Property Prices Retail Property Rents Apartments Sector Forecasts Suburban Office Demographic Highlights Industrial Job Formation Trends Local Economy Economic Base Profile Educational Achievement Tax Structure F F Quality of Life Factors ACTS ACTS A publication of the National Real Estate Index Global Real Analytics New York Vol. 32 ✯ The National Real Estate Index extends its deepest sympathies and condolences to the victims of the World Trade Center, Pentagon and Pennsylvania tragedies and their families and friends. We would also like to extend our gratitude to the rescue workers, medical personnel and other professionals and citizens who have come to the aid of those affected. Report Format This report is organized as follows. Section I costs and availability are detailed in Section VI. provides a snapshot that highlights the key eco- A series of other important factors, including nomic, demographic and real estate-related retail sales trends and international trade, are findings of the study. Sections II through IX reported in Section VII. Local and state fiscal provide an in-depth look (generally in a tabular policies, including taxes and federal spending, format) at the key economic, demographic, pub- are highlighted in Section VIII. Several key lic policy, and quality of life factors that can quality-of-life considerations are summarized in affect the demand for real estate. Section IX. In Section II, recent population trends are In Section X, local market price, rent and capi- reported. Section III analyzes the local eco- talization rate trends for the preceding 12 months nomic base and current labor force and job for- are reported. -

I I I Case 13-13086-KG Doc 1 Filed 11/22/13 Page 1 of 4

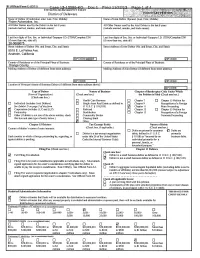

B! (Official Form 11 (12/11) Case 13-13086-KG Doc 1 Filed 11/22/13 Page 1 of 4 UNITED STATES BANKRUPTCY COURT District of Delaware YOLIJ1"4T4RYPET1TION - Name of Debtor (if individual, enter Last, First, Middle): Name of Joint Debtor (Spouse) (Last, First, Middle): Fisker_ Automotive, _Inc. All Other Names used by the Debtor in the last 8 years All Other Names used by the Joint Debtor in the last 8 years (include married, maiden, and trade names): (include married, maiden, and trade names): Last four digits of Soc. Sec. or Individual-Taxpayer I.D. (ITIN)/Complete Eli') Last four digits of Soc. Sec. or individual-Taxpayer I.D. (ITIN)/Complete EIN (if more than one, state all): (if more than one, state all): 26-0689075 Street Address of Debtor (No. and Street, City, and State): Street Address of Joint Debtor (No. and Street, City, and State): 5515 E. La Palma Ave. Anaheim, California IZIP CODE 92807 I VIP CODE I County of Residence or of the Principal Place of Business: County of Residence or of the Principal Place of Business: Orange County Mailing Address of Debtor (if different from street address): Mailing Address of Joint Debtor (if different from street address): IZIP CODE I IZIP CODE I Location of Principal Assets of Business Debtor (if different from street address above): IZIP CODE I Type of Debtor Nature of Business Chapter of Bankruptcy Code Under Which (Form of Organization) (Check one box.) the Petition is Filed (Check one box.) (Check one box.) El Health Care Business D Chapter 7 0 Chapter 15 Petition for 0 Individual (includes Joint Debtors) 0 Single Asset Real Estate as defined in 0 Chapter 9 Recognition of a Foreign See Exhibit Don page 2 of thisform. -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

Emergency Response Incidents

Emergency Response Incidents Incident Type Location Borough Utility-Water Main 136-17 72 Avenue Queens Structural-Sidewalk Collapse 927 Broadway Manhattan Utility-Other Manhattan Administration-Other Seagirt Blvd & Beach 9 Street Queens Law Enforcement-Other Brooklyn Utility-Water Main 2-17 54 Avenue Queens Fire-2nd Alarm 238 East 24 Street Manhattan Utility-Water Main 7th Avenue & West 27 Street Manhattan Fire-10-76 (Commercial High Rise Fire) 130 East 57 Street Manhattan Structural-Crane Brooklyn Fire-2nd Alarm 24 Charles Street Manhattan Fire-3rd Alarm 581 3 ave new york Structural-Collapse 55 Thompson St Manhattan Utility-Other Hylan Blvd & Arbutus Avenue Staten Island Fire-2nd Alarm 53-09 Beach Channel Drive Far Rockaway Fire-1st Alarm 151 West 100 Street Manhattan Fire-2nd Alarm 1747 West 6 Street Brooklyn Structural-Crane Brooklyn Structural-Crane 225 Park Avenue South Manhattan Utility-Gas Low Pressure Noble Avenue & Watson Avenue Bronx Page 1 of 478 09/30/2021 Emergency Response Incidents Creation Date Closed Date Latitude Longitude 01/16/2017 01:13:38 PM 40.71400364095638 -73.82998933154158 10/29/2016 12:13:31 PM 40.71442154062271 -74.00607638041981 11/22/2016 08:53:17 AM 11/14/2016 03:53:54 PM 40.71400364095638 -73.82998933154158 10/29/2016 05:35:28 PM 12/02/2016 04:40:13 PM 40.71400364095638 -73.82998933154158 11/25/2016 04:06:09 AM 40.71442154062271 -74.00607638041981 12/03/2016 04:17:30 AM 40.71442154062271 -74.00607638041981 11/26/2016 05:45:43 AM 11/18/2016 01:12:51 PM 12/14/2016 10:26:17 PM 40.71442154062271 -74.00607638041981 -

FORM 10-K Vornado Realty Trust Vornado Realty L.P

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended: December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 001-11954 (Vornado Realty Trust) Commission File Number: 001-34482 (Vornado Realty L.P.) Vornado Realty Trust Vornado Realty L.P. (Exact name of registrants as specified in its charter) Vornado Realty Trust Maryland 22-1657560 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number) Vornado Realty L.P. Delaware 13-3925979 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number) 888 Seventh Avenue, New York, New York 10019 (Address of principal executive offices) (Zip Code) (212) 894-7000 (Registrants’ telephone number, including area code) N/A (Former name, former address and former fiscal year, if changed since last report) Securities registered pursuant to Section 12(b) of the Act: Name of Exchange on Which Registrant Title of Each Class Trading Symbol(s) Registered Vornado Realty Trust Common Shares of beneficial interest, $.04 par value per share VNO New York Stock Exchange Cumulative Redeemable Preferred Shares of beneficial interest, liquidation preference $25.00 per share: Vornado Realty Trust 5.70% Series K VNO/PK New York Stock Exchange Vornado Realty Trust 5.40% Series L VNO/PL New York Stock Exchange Vornado Realty Trust 5.25% Series M VNO/PM New York Stock Exchange Vornado Realty Trust 5.25% Series N VNO/PN New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: Registrant Title of Each Class Vornado Realty Trust Series A Convertible Preferred Shares of beneficial interest, liquidation preference $50.00 per share Vornado Realty L.P. -

March 2015 Manhattan Office Leasing

Office Outlook Manhattan | March 2015 Leasing market wrap up Manhattan Class A vacancy rates Feb-13 Feb-14 Feb-15 20.0% Midtown Manhattan After a lull in large block leasing activity in Midtown in January, deal flow 15.0% accelerated in February with three transactions over 100,000 square feet completed, causing the Midtown Class A vacancy to decrease to 11.2 percent from 11.4 percent during the month. Overall vacancy remained 10.0% unchanged at 10.2 percent. In the largest lease of the month, advertising firm Publicis Groupe 5.0% renewed and expanded its commitment at 1675 Broadway, bringing its total footprint in the building to 506,009 square feet. Advertising has been 0.0% one of Midtown’s strongest sectors, especially on the West Side, since Manhattan Midtown Midtown South Downtown the recovery. As a result of the Publicis expansion, Class A vacancy in the Columbus Circle submarket decreased to 11.2 percent from 11.8 percent in January. Investment management firm Fortress Investment Group Manhattan Class A asking rates renewed and expanded its space at 1345 Avenue of the Americas for Feb-13 Feb-14 Feb-15 a total of 200,030 square feet. The lease included a 68,000-square-foot $100.00 sublease from Allianz and a 44,000-square-foot expansion. Bloomberg LP signed a lease for 150,000 square feet at 919 Third Avenue, just a $80.00 couple of blocks south of its headquarters at 731 Lexington Avenue. In a relocation from 395 Hudson Street in Midtown South, Kaplan Test Prep $60.00 will sublease 80,000 square feet at 750 Third Avenue from Condé Nast. -

“It's Not What You Know, It's Who You Know.”

ADVERTISING SUPPLEMENT TO CRAIN’S NEW YORK BUSINESS Restaurants, Conference Centers Venues and Catering New York Area Hotels Florists Results Address: 583 Park Ave, New York, NY 10065 “It’s not what Past success is often a good indicator of future success, but Phone: (212) 583-7200 keep in mind, success comes in many forms such as rave Email: [email protected] reviews, savings on budget, flawless execution, or a myriad Website: www.583parkave.com you know, it’s of other key performance indicators. Pick the ones that are most important to you and asses their success ratio. AMA New York Executive Conference Center Affordable meeting packages. Meeting rooms can who you know.” Remember, for long-term resources it’s always a good accommodate over 200 attendees. Executive chairs. High- idea to refresh and reassess every two years! speed Internet access. Complimentary Wi-Fi in lounges. Complimentary continuous beverage service. Optional catering. owhere is the phrase truer than in corporate No service charges and no guest room commitment required. event planning. The success of your event is Free projector and PC use. Noften the direct result of a carefully orchestrated CONFERENCE CENTERS Address: 1601 Broadway at 48th Street, dance among a handful of select providers. However, New York, NY 10019 assembling a team of reliable event vendors does not 92nd Street Y Contact: Valerie Mazzilli-Brown happen overnight. Your dream team should be curated Give your special event the extraordinary and versatile venue Phone: (212) 903-8277 over many years. A good rule of thumb to use when it deserves at 92nd Street Y. -

Sheraton New York Times Square

Sher aton New Y ork Tim es Square Sheraton New York Times Square 811 7th Avenue New York, NY 10019 University Faculty and Staff Preferred Booking Method: GEMS online booking tool For Telephone Reservations, Call: 877-843-8869 Phone: 212-581-1000 Fax: 212-262-4410 Sales Contact: Sharon Kelley-Tuck at 212-841-6553 Guest room rates vary by season and are subject to availability. Ask for the University of Chicago rate. Offer is available to all faculty, staff, students, guests, visitors, alumni, affiliates, contractors, consultants, retirees and Big Ten University guests. For groups of ten or more, contact Sharon Kelley-Tuck at 212-841-6553. 2015 Blackout Periods Nov 30 Dec 1-11, 31 Cancellation Policy By 4PM ET, Twenty-four (24) hours prior to day of arrival A $160 million renovation has reinvigorated the Sheraton New York Times Square Hotel, between Central Park and Times Square in the Midtown business and entertainment district. Go from a crucial meeting to a famous uptown eatery without missing a beat. Be a part of the NYC spirit at the Sheraton New York Times Square Hotel, located on 7th Avenue between 52nd and 53rd Streets in midtown Manhattan. Just steps from the excitement of Broadway theatres, prestige of Carnegie Hall and world-class shopping of Fifth Avenue - our location is the perfect way to immerse yourself in the best that New York has to offer. 20% discount on all food and beverage, including room service, excluding alcohol Complimentary wireless internet and fitness center 50 floors, 1750 rooms Restaurant - lounge - business services Reimbursement Policy Faculty and staff business travel expenses are to be processed through the GEMS System located at https://gems.uchicago.edu/login/auth.php. -

9 West 57Th Street

Space Report of Select Relocation Alternatives February 13, 2013 Looking for office space in New York City? Click here to contact us for a free customized report. Table of Contents 1. 250 WEST 55TH STREET 2. 9 WEST 57TH STREET 3. 681 FIFTH AVENUE 4. 712 FIFTH AVENUE 5. 717 FIFTH AVENUE 6. 745 FIFTH AVENUE 7. 540 MADISON AVENUE 8. 660 MADISON AVENUE 9. 1370 AVENUE OF THE AMERICAS 10. 888 SEVENTH AVENUE th 250 West 55 Street Location: BETWEEN BROADWAY AND EIGHTH AVENUE AVAILABLE SPACE Floor Rentable Area Asking Rental (in square feet) (per square foot) Multiple floors available in Roughly 24,000 rsf each $80’s - $90’s the base and tower of the building. COMMENTS: • Brand new LEED Gold construction. All floors feature oversized windows, 10’ finished ceilings, column free floorplates and minimal core penetrations. • Tower floors have incredible Southern, Western and Northern Views. ELECTRICITY: Submetered LANDLORD’S WORK: Build-to-suit POSSESSION: June 1, 2013 TERM: 10 years minimum BUILDING PROFILE OWNERSHIP: Boston Properties, Inc. YEAR BUILT: 2013 BUILDING AREA: 1,052,150 square feet NUMBER OF FLOORS: 38 250 West 55th Street Actual Photos and Renderings 250 West 55th Street Actual Photos and Renderings 250 West 55th Street Typical Core and Shell Plan – Tower Floors th 9 West 57 Street Solow Building Location: BETWEEN FIFTH & SIXTH AVENUES AVAILABLE SPACE Floor Rentable Area Asking Rental (in square feet) (per square foot) th th Entire 30 – 49 Approximately $165 - $200 31,000 rsf Each (divisible) COMMENTS: • Partial 30th – 49th Floors: Pricing reflects units to be built on the north side of the building with unobstructed views of Central Park. -

Off* for Visitors

Welcome to The best brands, the biggest selection, plus 1O% off* for visitors. Stop by Macy’s Herald Square and ask for your Macy’s Visitor Savings Pass*, good for 10% off* thousands of items throughout the store! Plus, we now ship to over 100 countries around the world, so you can enjoy international shipping online. For details, log on to macys.com/international Macy’s Herald Square Visitor Center, Lower Level (212) 494-3827 *Restrictions apply. Valid I.D. required. Details in store. NYC Official Visitor Guide A Letter from the Mayor Dear Friends: As temperatures dip, autumn turns the City’s abundant foliage to brilliant colors, providing a beautiful backdrop to the five boroughs. Neighborhoods like Fort Greene in Brooklyn, Snug Harbor on Staten Island, Long Island City in Queens and Arthur Avenue in the Bronx are rich in the cultural diversity for which the City is famous. Enjoy strolling through these communities as well as among the more than 700 acres of new parkland added in the past decade. Fall also means it is time for favorite holidays. Every October, NYC streets come alive with ghosts, goblins and revelry along Sixth Avenue during Manhattan’s Village Halloween Parade. The pomp and pageantry of Macy’s Thanksgiving Day Parade in November make for a high-energy holiday spectacle. And in early December, Rockefeller Center’s signature tree lights up and beckons to the area’s shoppers and ice-skaters. The season also offers plenty of relaxing options for anyone seeking a break from the holiday hustle and bustle. -

Board Liaison

BOARD OF DIRECTORS LIAISON ASSIGNMENTS 2021/22 BUSINESS CLUSTER CHILDREN & FAMILY CLUSTER CRIMINAL JUSTICE CLUSTER Antitrust & Trade Regulation Children & the Law Capital Punishment Banking Law Children, Council on Corrections and Community Reentry Bankruptcy & Corporate Reorganization Domestic Violence Criminal Advocacy Commercial Law & Uniform State Laws Education & the Law Criminal Courts Consumer Affairs Family Court & Family Law Criminal Justice Operations Employee Benefits & Executive Juvenile Justice Criminal Law Compensation Matrimonial Law Mass Incarceration Task Force Hospitality Law White Collar Crime Judith Whiting David Levine Community Service Society of NY Sarah J. Berger Bloomberg LP 633 Third Avenue, Fl 10 Phone: (646) 386-3992 731 Lexington Avenue New York, NY 10017 [email protected] Legal Dept. FL 14 Phone: (212)614-5323 New York, NY 10022 [email protected] Phone: (212) 318-2000 [email protected] DIVERSITY CLUSTER GOVERNMENT/ FINANCIAL CLUSTER Diversity, Equity and Inclusion ENVIRONMENT/TRANSPORTATION Compliance Diversity Pipeline Initiatives CLUSTER Corporation Law Lesbian, Gay, Bisexual, Transgender & Administrative Law Emerging Companies and Venture Capital Queer Rights Aeronautics Financial Reporting Minorities in the Profession Election Law Futures & Derivatives Regulation Recruitment & Retention of Lawyers Energy Investment Management Regulation Women in the Legal Profession Environmental Law Mergers Acquisitions & Corporate Control Government Ethics and State Affairs Contests Anna M. Pohl International