On Better Footing 12M Price Target PHP 247.00 (+18%) Previous Price Target PHP 247.00

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mall Guide 60X60 JULY 19 FINAL SF&U2

ANCHOR STORES SPECIALTY CONCEPT STORES HOMEWEAR / HOME FURNISHING 311 BURGER KING 327 / E377 AL WAHDA CINEMA E220 THE CUSTOM SHOPS / / DÉCOR / LINEN 312 BEIRUT REST. & GRILL E206 GOLD'S GYM BUCKLE UP E201 LIFESTYLE 313 DELIZIOZA PIZZERIA 301 WANASA LAND SFK20 ART ATTACK CALLIGRAPHER FS01 IL FORNO FS02-03 WENDY'S 314-315 MAX FASHION SEK15 KINGDOM OF HONEY & SECOND FLOOR FASHION - SPORTSWEAR & FS04 LONDON FISH & CHIPS HERBALS SPORTS GOODS FS05 SUBWAY 309 SF SEK21 KNIGHT SHOT E207B REEBOK FCK01 CHARLEY'S GRILLED SUB 310 ART & PHOTOGRAPHY / PICTURE FRAMING POPEYES E258-259/264 VIRGIN MEGASTORE SFK05 MOBILE OUTFITTERS E209-211 ADIDAS PERFORMANCE SFK14A SOFT CAFÉ 311 MAROOSH SFK15A SHOKUDO EXPRESS Soon to open FCK01 SK02 PHOTO MAGIC E233 ATHLETE'S CO. BURGER CAFETERIA 312 KING CHARLEY’S SFK02 ART ATTACK CALLIGRAPHER RESTAURANTS E234 SKECHERS GRILL 308 SFK07 SIOMAI HOUSE 313 BEIRUT KFC E203-204 FAMOUS DAVE’S DILIZIOSA E254-255 MING'S CHAMBER PIZZRIA 307 EXTENSION UPPER SECOND FLOOR ATM SERVICES & EXCHANGE E256-257 PEPPERMILL PHARMACY/FITNESS/ WELLNESS & SPA HARDEES SF01 SHARJAH ISLAMIC BANK SK02A DOCIB NUTRITION 402-403 AL IBRAHIMI RESTAURANT 306 E277 RUSSO'S NEW YORK PIZZA 404 CHOWKING SF5 DUBAI ISLAMIC BANK E207C/207D BIG & FIT SPORTS PIZZA HUT E278-279 GALITO’S 405 JUMANAH REST. 305 SF6 RAK BANK NUTRITION / JUICE BAR 408 FUDDRUKERS FS01 ADCB - ATM FS04 MC DONALD’S E252 AL AHALIA EXCHANGE E232 DR. NUTRITION SF2 RAK BANK - ATM LONDON FISH IL FORNO COFFEE SHOPS E208B VINTAGE SALON & CHIPS SF6 303B PAPPAROTI E236 NAIL STYLE BEAUTY CENTER FS02-03 -

1289130, 140 & 180 Southsan Jose, Californiapark Victoria Drive Milpitas, California

FOR SALELEASE 1289130, 140 & 180 SOUTHSAN JOSE, CALIFORNIAPARK VICTORIA DRIVE MILPITAS, CALIFORNIA 1289 S Park Victoria Dr PROPERTY HIGHLIGHTS + ±9,094 SF + Corner Location at Signalized Location + Anchored by Comerica Bank (NYSE: CMA) + Walking Distance to Nearby Retail with Enclosed Walk Up ATM Amenities + Great Investor or User (SBA) Opportunity + Great Access to Highway 680 + Ground Floor: 4,450 SF (49%) + Building Signage Available – Leased to Comerica Bank + Parking Ratio: 4/1,000 SF (LED: 12/31/24) (35 On-Site Parking Spaces) + 2nd Floor: 4,644 SF (51%) + Parcel Size 22,521 SF – To be Delivered Vacant + APN: 088-36-035 CONTACT US VINCE MACHADO ANTHONY PODESTA Senior Vice President Associate Lic. 01317553 Lic. 01467260 +1 408 453 7411 +1 408 453 7479 [email protected] [email protected] www.cbre.us/siliconvalley 1289 S PARK VICTORIA DR FOR SALE Milpitas, California FLOOR PLAN 1st FLOOR ±4,450 SF Leased to Comerica Suite 100 ±4,450 SF VACANT VACANT Suite 200 Suite 205 ±1,662 SF ±751 SF 2nd FLOOR ±4,644 SF Suite 201 ±2,231 SF VACANT © 2018 CBRE, Inc. This information has been obtained from sources believed reliable. We have not verified it and make no guarantee, warranty or representation about it. Any projections, opinions, assump- tions or estimates used are for example only and do not represent the current or future performance of the property. You and your advisors should conduct a careful, independent investigation of the property to determine to your satisfaction the suitability of the property for your needs. N:\Team-Marketing\1289 S Park Victoria Drive\1289_S_ParkVictoria_Flyer_V04.indd Photos herein are the property of their respective owners and use of these images without the express written consent of the owner is prohibited. -

Restaurant Trends App

RESTAURANT TRENDS APP For any restaurant, Understanding the competitive landscape of your trade are is key when making location-based real estate and marketing decision. eSite has partnered with Restaurant Trends to develop a quick and easy to use tool, that allows restaurants to analyze how other restaurants in a study trade area of performing. The tool provides users with sales data and other performance indicators. The tool uses Restaurant Trends data which is the only continuous store-level research effort, tracking all major QSR (Quick Service) and FSR (Full Service) restaurant chains. Restaurant Trends has intelligence on over 190,000 stores in over 500 brands in every market in the United States. APP SPECIFICS: • Input: Select a point on the map or input an address, define the trade area in minute or miles (cannot exceed 3 miles or 6 minutes), and the restaurant • Output: List of chains within that category and trade area. List includes chain name, address, annual sales, market index, and national index. Additionally, a map is provided which displays the trade area and location of the chains within the category and trade area PRICE: • Option 1 – Transaction: $300/Report • Option 2 – Subscription: $15,000/License per year with unlimited reporting SAMPLE OUTPUT: CATEGORIES & BRANDS AVAILABLE: Asian Flame Broiler Chicken Wing Zone Asian honeygrow Chicken Wings To Go Asian Pei Wei Chicken Wingstop Asian Teriyaki Madness Chicken Zaxby's Asian Waba Grill Donuts/Bakery Dunkin' Donuts Chicken Big Chic Donuts/Bakery Tim Horton's Chicken -

Annual Report Permittee Name: City of Daly City

FY 2017-2018 Annual Report Permittee Name: City of Daly City Table of Contents Section Page Section 1 – Permittee Information ................................................................................................................................. 1-1 Section 2 – Provision C.2 Municipal Operations ......................................................................................................... 2-1 Section 3 – Provision C.3 New Development and Redevelopment ....................................................................... 3-1 Section 4 – Provision C.4 Industrial and Commercial Site Controls ......................................................................... 4-1 Section 5 – Provision C.5 Illicit Discharge Detection and Elimination ..................................................................... 5-1 Section 6 – Provision C.6 Construction Site Controls .................................................................................................. 6-1 Section 7 – Provision C.7 Public Information and Outreach .................................................................................... 7-1 Section 9 – Provision C.9 Pesticides Toxicity Controls ................................................................................................ 9-1 Section 10 – Provision C.10 Trash Load Reduction ................................................................................................... 10-1 Section 11 – Provision C.11 Mercury Controls .......................................................................................................... -

Wendy's Final

FAST CASUAL FINAL RFP JHENI GIBSON EXECUTIVE SUMMARY What do we want to do? How will we do it? What’s the timeline? • Wendy’s would like to reposition its • We will address Wendy’s • This campaign plan will run for brand as “Fast Casual” offering higher quality foods and lite service millennial target audience by the full 2018 Fiscal Year. coupled with the convenience of exploring their habits, budget, • All testing will be completed quick output. lifestyle and priorities. within the first 2 months of • Competitors such as • We’ll test and launch campaigns the FY. Chipotle, Shake Shack, and that highlight Wendy’s fresher • Progress will be measured Smashburger have adopted ingredients, sourcing, nutrition, monthly to incrementally the fast casual business analyze success and optimize model and continue to and our new Fast Casual dining attract millennials taking experience. Channels used will towards goals through the market share from “fast be Advertising, PR, Sponsorships year. food” restaurants like and Promotions. • Final success metrics McDonalds, Wendy’s and • Creative and copy will will be gathered at the Burger King. feature fresh and end of the fiscal to • The Fast Casual dining observe if goals and experience provides a progressive images of modern, comfortable and new menu options and objectives have been inviting aesthetic where millennials enjoying a met. customers can enjoy a more quick and nutritious meal. upscale dining experience. • Food is locally sourced, honest and made to order. • . "Everybody in the world is talking about fast casual… It just has a broad appeal.” BONNIE RIGGS – INDUSTRY ANALYST WITH NPD GROUP (The Washington Post) BUSINESS SITUATION • With the success of fast casual restaurants, its evident that customers prefer an in- store, upmarket experience. -

Downloadable Menu Updated As of May 8

DOWNLOADABLE MENU UPDATED AS OF MAY 8 TABLE OF CONTENTS RESTAURANT MENU Blackscoop 3-4 Bonchon Chicken 5-8 Chowking 9-10 Classic Savory 11-12 Dairy Queen 13-15 French Baker 16-17 Gringo 18-19 Infinitea 20-23 Jollibee 24-27 KFC 28 Krispy Kreme 29 Mary Grace Café 30 Max’s Restaurant 31 Original Cake 32 Pancake House 33 Ramen Kuroda 34 Red Ribbon 35 S&R New York Style Pizza 36 Samgyeopmasarap 37 Tokyo Tokyo 38-39 TAKE-OUT AND DELIVERY GUIDE 40-41 BLACK SCOOP Available for take-out or order via Shop For Me by , , for delivery. Page 3 BLACK SCOOP Available for take-out or order via Shop For Me by , , for delivery. Page 4 BONCHON CHICKEN CHICKEN SEAFOOD 1pc Chicken Boxed Meal Php 109.00 Crispy Shrimp Boxed Meal Php 175.00 2pc Chicken Boxed Meal Php 172.00 Crispy Squid Boxed Meal Php 175.00 2pc Chops Boxed Meal Php 172.00 Crispy Fish Boxed Meal Php 175.00 Wings Boxed Meal Php 172.00 Fish and Chips Boxed Meal Php 175.00 Double Loaded Sandwhich Boxed Meal Php 179.00 Seafood Chapchae: 2pc Crispy Fish, Half Php 175.00 3pcs Glazed Chicken Fries Boxed Meal Php 172.00 Chapchae, Drink Seafood K-Style: 2pc Crispy Fish, Half 5pcs Glazed Chicken Fries Boxed Meal Php 195.00 Php 198.00 Chapchae, Milk Kreme, Drink Chicken Chapchae Meal Php 172.00 BEEF K-Style Feast A: 1pc Chicken with Rice, Half Php 198.00 Beef Bulgogi Meal Php 175.00 Chapchae, Milky Kreme and Regular Drink Korean Beef Stew Meal Php 185.00 K-Style Feast B: 1pc Chicken with Rice, Fish Php 198.00 Poppers, Milky Kreme and Regular Drink Spicy Korean Beef Stew Php 189.00 Available for take-out or order via Shop For Me by , , for delivery. -

Dine and Win Mall & Restaurant List 23March.Indd

AL GHURAIR CENTRE TIM HORTONS CAFÉ AND BAKE SHOP ALL THE PERKS ESPRESSO CAFÉ UMAMI BASKIN ROBBINS WENDY’S BESTOON SAMAD WING.STOP BIKANERVALA STAR RESTAURANT YAKITATE BUBEE DRINKS CAFFE NERO AL KHAIL GATE COMMUNITY CENTRE CHARLEY’S GRILLED SUBS ARABIAN GRILL RESTAURANT CO. CHIC BOY RESTAURANT CAFETERIA AL KHAIL EXPRESS CHINESE PALACE CHENNAI CURRY PALACE RESTAURANT CHOWKING ORIENT RESTAURANT KFC CINNABON & SEATTLE’S BEST COFFEE LIMS CAFE DENNY’S MADRAS KITCHEN RESTAURANT DIN TAI FUNG RESTAURANT NEW ALBAYAN RESTAURANT - CHICKING DQ GRILL & CHILL QASR ANTAR CAFETERIA FARSI RESTAURANT HAPPY LEMON IL FORNO UNO ARABIAN CENTRE IRVINS BASKIN ROBINS JOLLIBEE BOMBAY CHOWPATHY KFC CHINESE PALACE KRISPY KREME COSTA COFFEE LEMON BAR GLORIA JEAN’S COFFEES MANOUSHE STREET HARDEES MARU UDON HATAM RESTAURANT MCDONALD’S JUNGLE JUICE MCDONALD’S KFC MUKALLA HADHRAMI HONEY MADFOON AL SADDA PAPA JOHNS (JAWAD RESTAURANT) MCDONALD’S PAPPAROTI NEW YORK FRIES PAUL BOULANGERIE PATTISSERIE PIZZA HUT PIZZA HUT SECOND CUP RETRO 7 CAFÉ STARBUCKS COFFEE SHOP STARBUCKS SULTAN BABA EXPRESS TONY ROMAS TAPA KING VANELLIS TERIYAKI BOY / SIZZLIN’ STEAK VIVEL THE CHOCO MONARCH COFFEE SHOP YALLA SAJ BAY AVENUE NJOY CHOCOLATIER & CAFÉ ATTIBASSI OAKBERRY BASKIN ROBBINS PAUL CAFÉ BIKANERVALA PIZZA HUT BURGER KING SARAVANAA BHAVAN CAFÉ FUNKIE TOWN STARBUCKS 25 MAR - 17 APR CARIBOU SUBWAY COSTA UNCLE DEEK ENSO RESTAURANT WHEEL 35 FARSI RESTAURANT YELLOW CHILLI FILLI CAFÉ GAZEBO SHOROOQ COMMUNITY HOT & SPICY CENTRE KABABJI CIRCLE RESTAURANT KAMAT KABABJI KCAL MISTER BAKER KFC PROJECT KUNAFA CAFE KULFILICIOUS STARBUCKS LA BRIOCHE LA FRAGOLA THE MALL MALAK AL TWOOK ARABIAN TEA HOUSE METRO FALCON BURGER KING MOSAIC GOURMET COSTA COFFEE MOTI MAHAL NOODLE EXPRESS RESTAURANT UPTOWN MIRDIFF PAPA JOHNS AL HAKAWATI PIZZA HUT AL ARAB RESTAURANT RAJU OMLET AL SAYER RETAIL EST. -

Former Restaurant Pad Site 11965 S

BUILDING LEASE, GROUND LEASE OR BTS FORMER RESTAURANT PAD SITE 11965 S. STRANG LINE RD., OLATHE, KANSAS New Courtyard Marriott 1.1 Acres CAN BE SPLIT SITE Future Mixed-use Tenant LINE ROAD 33,600 CPD STRANG PROPERTY HIGHLIGHTS > 6,810 s.f. building available on 1.41 acres > Existing building can be split for 2 tenants > Existing Building can be demolished, and parcel redeveloped into two lots (Ground Lease or BTS) > One of the Kansas City Metro’s strongest retail intersections > Anchored by SuperTarget and highest volume AMC Theatre in the market > Strong Visibility and easy access at signalized intersection > 90,000 CPD on I-35 > 33,600 CPD on 119th Street > 23,000 CPD on Strang Line Road FOR INFORMATION: JEFF BERG COLEBY HENZLIK PARTNER PARTNER 913-914-7065 913-914-7146 [email protected] [email protected] FORMER RESTAURANT PAD SITE OLATHE, KS PROPERTY AERIAL NORTHRIDGE SC S. BLACK BOB RD. RD. BOB BOB BLACK BLACK S. S. 64,499 CPD 33,600 CPD WEST 119TH STREET OLATHE POINTE . RD STR INE ANG L PD 0 C ,00 23 OLATHE STATION 56,499 CPD 3 ELEVATE PROPERTY ADVISORS FORMER RESTAURANT PAD SITE OLATHE, KS PROPERTY FEATURES 6,10 SF 1.1 Acres BUILDING OR LOT SITE CAN BE SPLIT S . S TR ANG LINE RD . UTURE MIED-USE TET S. STRANG LINE CT. spacious outdoor patio 5 ELEVATE PROPERTY ADVISORS NEIGHBORHOOD FORMER RESTAURANT PAD SITE OLATHE, KS DYNAMICS RESTAURANTS The fast-casual and full-service restaurant scene at this regional node hosts an unbeatable mix of local and regional hometown heroes like Joe’s Kansas City Bar-B-Que, Doc Greens, Mr. -

Equity Research Report Jollibee Foods Corp. 24Th April 2019

Equity Research Report Jollibee Foods Corp. 24th April 2019 Murtaza Salman Abedin Anirudh Ganeriwala Harsharan Singh Muhammad Salik Raymond Widjaja Tang Man Chung Tommy Fang Yucheng Published By CityU Student Research & Investment Club THE FINAL PAGE OF THIS REPORT CONTAINS A DETAILED DISCLAIMER The content and opinions in this report are written by university students from the CityU Student Research & Investment Club, and thus are for reference only. Investors are fully responsible for their investment decisions. CityU Student Research & Investment Club is not responsible for any direct or indirect loss resulting from investments referenced to this report. The opinions in this report constitute the opinion of the CityU Student Research & Investment Club and do not constitute the opinion of the City University of Hong Kong nor any governing or student body or department under the University. 24 April 2019 Asia Pacific/Philippines Equity Research Restaurants Rating OUTPERFORM Price (22 April 19, PHP) 304.00 Target price (PHP) % up from Price on April, 22: 18.58% 360.49 Market cap. (PHP, m) 333,621 Enterprise Value (PHP m) 337,271.4 Jollibee Foods Corporation (JFC:PM) Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. Target price is for 12 months. Research Analysts: Jollibee Foods Corporation (JFC) is an Asian food service multinational company which owns and operates a large number of Quick Service Murtaza Salman Abedin +852 59858568 Restaurants (QSRs). The company is listed on the Philippines Stock [email protected] Exchange and has a market capitalization of PHP347.57 Billion (USD Anirudh Ganeriwala 6.72 Billion) and a revenue of PHP126.2 Billion (USD 2.43 Billion) as [email protected] of 2017. -

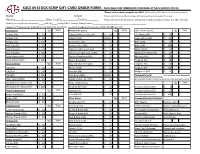

Sacs in Stock Scrip Gift Card Order Form

SACS IN STOCK SCRIP GIFT CARD ORDER FORM - AVAILABLE FOR IMMEDIATE PURCHASE AT SACS SCHOOL OFFICE ~Please make checks payable to: SACS (There will be a $25 fee for any returned payments.) Name:___________________________________________ Scrip #___________ ~Please note that the profit percentages offered by merchants are subject to change. Phone:(_____)________________ Order Total $____________Check #________ ~Please note that SCRIP gift cards can only be used to purchase goods or services, NOT other gift cards. Pickup/Delivery (Please select one):_____Pick-Up_____Send w/Child - Student Name/Teacher________________________________________________ Questions? Please contact Diane Mulcrone, SACS Scrip Coordinator, at [email protected] or (952)445-3387 ext. 140 Gas Stations Qty Total Restaurants (cont.) Qty Total Other Stores (cont.) Qty Total Holiday (4%) $ 25 $ Chipotle Mexican Grill (10%) $ 10 $ J.C. Penney (5%) $ 25 $ Holiday (4%) $ 50 $ Culver's (10%) $10/$25 $ JoAnn Fabrics (6%) $ 25 $ Holiday (4%) $ 100 $ Dairy Queen (3%) $ 10 $ Kohl's (5%) $ 25 $ Kwik Trip (5%) $ 25 $ Domino's Pizza (8%) $ 10 $ Kohl's (5%) $ 100 $ Kwik Trip (5%) $ 50 $ O'Brien's Public House (5%) $ 25 $ Macy's (10%) $ 25 $ Kwik Trip (5%) $ 100 $ Olive Garden/Red Lobster (9%) $ 25 $ Marshalls/TJ Maxx (7%) $ 25 $ Super America (4%) $ 25 $ Outback Steakhouse (8%) $ 25 $ Michael's (4%) $ 25 $ Super America (4%) $ 100 $ Panera Bread (9%) $ 10 $ Target (2.5%) $ 10 $ Grocery Stores Qty Total Papa Murphy's Pizza (8%) $ 10 $ Target (2.5%) $ 25 $ Cub (5%) $ 25 $ Perkin's (10%) $ 25 $ Target (2.5%) $ 100 $ Cub (5%) $ 50 $ Pizza Hut (8%) $ 10 $ Walgreen's (6%) $ 25 $ Cub (5%) $ 100 $ Pizza Ranch (10%) $10/$25 $ Community Scrip* This certificate is not designated Von Hanson's (10%) $ 25 $ Qdoba Mexican Grill (7%) $ 25 $ for a specific retailer. -

Greenwich Jollibee Bonchon Kfc Classic Savory Mang

GREENWICH JOLLIBEE BONCHON Ground Level Ground Level Ground Level (042) 373 77-11 (042) 710-0002 (042) 717-4911 KFC BUDDY’S RESTAURANT CLASSIC SAVORY Ground Level Second Level Ground Level (042) 323-2189 (042) 710-48-22 (042) 373-4606 MANG INASAL CHOWKING RED RIBBON Ground Level Ground Level Ground Level (042) 795-3800 (042) 717-3416 (042) 717-2943 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP BURGER KING DUNKIN DONUTS INFINITEA Ground Level Ground Level Third Level (042) 717-9532 CHATIME GERRY’S RESTARANT KOFFEE KLATCH Ground Level Ground Level Second Level 0906-483-1459 (042) 717-9515 (042) 713-0214 CLYDES GONG CHA MAX’S RESTAURANT Ground Level Second Level Second Level 0923-957-5922 09753097279 (042) 717-9032 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP PAN DE MANILA POTATO CORNER STARBUCKS Ground Level Third Level Ground Level 0977-797-0973 0925-889-3600 0917-851-5292 PEPPER LUNCH SHAWARMA SHACK TOKYO TOKYO Ground Level Ground Level Second Level (042) 717-0094 0917-793-0263 POP AND MIX SIOMAI HOUSE TURKS Third Level Second Level Third Level 0917-639-0902 0999-887-0919 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP WINGED POTATO ZARK’S BURGER Third Level Ground Level 0927-759-3789 (042) 717-0094 OPPA BUFFALO WINGS SAMGYEOPSAL AND THINGS Second Level Ground Level 0966-985-4089 (042) 322-9483 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM -

West Saint Paul West St. Paul Complex June 7-9, 2013 13A Black

Directions Between W St Paul Sports Complex and Hampton Inn West Saint Paul West St. Paul Complex June 7-9, 2013 13A Black This tournament is a State Qualifier. This souvenir program is brought to you by Becky Cromwell. If you take photos of the ball games, I would appreciate if you would email me a few for our MAYBA.com Royals 13A page. [email protected] or [email protected] Thank you. Enjoy the game! Royals 13A Roster 3 Danny Johnson 7 Mitchell Barnes 9 Zach Zellmer 14 Matthew Murray 17 Sam Murray 21 Brendan McCullom 22 Ford Johnson 23 Logan Stevenson – Injured Reserve 24 Tyler Cromwell 27 Noah Weimert 31 Reese Melvin 32 Ethan Crouch 43 Reid Gruenes They are going to be hungry later… So, what is near the field you ask? All along 52/S Robert Street are - KFC, Taco Bell, Burger King, Noodles & Company, Culvers, Arby’s, Applebees, Fireside Lounge, Perkins, Buffalo Wild Wings, McDonalds, Jimmy Johns, Chuck E Cheese, Bakers Square, Chipotle, Old Country Buffet So, what is near the hotel you ask? Many near the intersection of Pilot Knob Rd and Yankee Doodle Rd includes - Lone Oak Grill, Granite City Food & Brewery, Houlihans, Jake’s City Grille, Red’s Savoy Pizza, Buffalo Wild Wings & Bar, Jimmy Johns, Chipotle, Potbelly Sandwich Shop, Team Hotel (Block) Information Panera, Genghis Grill, Smashburger, Dairy Queen, Old Chicago, “Mankato Royals 13 Black” Applebees, Perkins, McDonalds, Wildcats Bar and Grill, Al Hampton Inn of Eagan Baker’s, The Italian Pie Shop, El Loro, Dragon Palace 3000 Eagandale Place (651) 688-3343 .