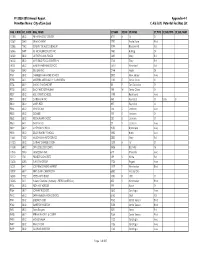

Foodservice Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mall Guide 60X60 JULY 19 FINAL SF&U2

ANCHOR STORES SPECIALTY CONCEPT STORES HOMEWEAR / HOME FURNISHING 311 BURGER KING 327 / E377 AL WAHDA CINEMA E220 THE CUSTOM SHOPS / / DÉCOR / LINEN 312 BEIRUT REST. & GRILL E206 GOLD'S GYM BUCKLE UP E201 LIFESTYLE 313 DELIZIOZA PIZZERIA 301 WANASA LAND SFK20 ART ATTACK CALLIGRAPHER FS01 IL FORNO FS02-03 WENDY'S 314-315 MAX FASHION SEK15 KINGDOM OF HONEY & SECOND FLOOR FASHION - SPORTSWEAR & FS04 LONDON FISH & CHIPS HERBALS SPORTS GOODS FS05 SUBWAY 309 SF SEK21 KNIGHT SHOT E207B REEBOK FCK01 CHARLEY'S GRILLED SUB 310 ART & PHOTOGRAPHY / PICTURE FRAMING POPEYES E258-259/264 VIRGIN MEGASTORE SFK05 MOBILE OUTFITTERS E209-211 ADIDAS PERFORMANCE SFK14A SOFT CAFÉ 311 MAROOSH SFK15A SHOKUDO EXPRESS Soon to open FCK01 SK02 PHOTO MAGIC E233 ATHLETE'S CO. BURGER CAFETERIA 312 KING CHARLEY’S SFK02 ART ATTACK CALLIGRAPHER RESTAURANTS E234 SKECHERS GRILL 308 SFK07 SIOMAI HOUSE 313 BEIRUT KFC E203-204 FAMOUS DAVE’S DILIZIOSA E254-255 MING'S CHAMBER PIZZRIA 307 EXTENSION UPPER SECOND FLOOR ATM SERVICES & EXCHANGE E256-257 PEPPERMILL PHARMACY/FITNESS/ WELLNESS & SPA HARDEES SF01 SHARJAH ISLAMIC BANK SK02A DOCIB NUTRITION 402-403 AL IBRAHIMI RESTAURANT 306 E277 RUSSO'S NEW YORK PIZZA 404 CHOWKING SF5 DUBAI ISLAMIC BANK E207C/207D BIG & FIT SPORTS PIZZA HUT E278-279 GALITO’S 405 JUMANAH REST. 305 SF6 RAK BANK NUTRITION / JUICE BAR 408 FUDDRUKERS FS01 ADCB - ATM FS04 MC DONALD’S E252 AL AHALIA EXCHANGE E232 DR. NUTRITION SF2 RAK BANK - ATM LONDON FISH IL FORNO COFFEE SHOPS E208B VINTAGE SALON & CHIPS SF6 303B PAPPAROTI E236 NAIL STYLE BEAUTY CENTER FS02-03 -

1289130, 140 & 180 Southsan Jose, Californiapark Victoria Drive Milpitas, California

FOR SALELEASE 1289130, 140 & 180 SOUTHSAN JOSE, CALIFORNIAPARK VICTORIA DRIVE MILPITAS, CALIFORNIA 1289 S Park Victoria Dr PROPERTY HIGHLIGHTS + ±9,094 SF + Corner Location at Signalized Location + Anchored by Comerica Bank (NYSE: CMA) + Walking Distance to Nearby Retail with Enclosed Walk Up ATM Amenities + Great Investor or User (SBA) Opportunity + Great Access to Highway 680 + Ground Floor: 4,450 SF (49%) + Building Signage Available – Leased to Comerica Bank + Parking Ratio: 4/1,000 SF (LED: 12/31/24) (35 On-Site Parking Spaces) + 2nd Floor: 4,644 SF (51%) + Parcel Size 22,521 SF – To be Delivered Vacant + APN: 088-36-035 CONTACT US VINCE MACHADO ANTHONY PODESTA Senior Vice President Associate Lic. 01317553 Lic. 01467260 +1 408 453 7411 +1 408 453 7479 [email protected] [email protected] www.cbre.us/siliconvalley 1289 S PARK VICTORIA DR FOR SALE Milpitas, California FLOOR PLAN 1st FLOOR ±4,450 SF Leased to Comerica Suite 100 ±4,450 SF VACANT VACANT Suite 200 Suite 205 ±1,662 SF ±751 SF 2nd FLOOR ±4,644 SF Suite 201 ±2,231 SF VACANT © 2018 CBRE, Inc. This information has been obtained from sources believed reliable. We have not verified it and make no guarantee, warranty or representation about it. Any projections, opinions, assump- tions or estimates used are for example only and do not represent the current or future performance of the property. You and your advisors should conduct a careful, independent investigation of the property to determine to your satisfaction the suitability of the property for your needs. N:\Team-Marketing\1289 S Park Victoria Drive\1289_S_ParkVictoria_Flyer_V04.indd Photos herein are the property of their respective owners and use of these images without the express written consent of the owner is prohibited. -

On Better Footing 12M Price Target PHP 247.00 (+18%) Previous Price Target PHP 247.00

209. 40 January 21, 2020 Jollibee Foods (JFC PM) BUY Share Price PHP 209.40 On better footing 12m Price Target PHP 247.00 (+18%) Previous Price Target PHP 247.00 Company Description Showing signs of recovery; Reiterate BUY Engaged in the development, operation, and We are encouraged on JFC’s current state of operations as we recently franchising of quick-service restaurants in the met the company. Although not yet out of the woods, across-the-board Philippines and worldwide improvement in both domestic and international operations in 4Q19 raised our confidence in JFC’s 2020 outlook. With 2019 behind us, we think that our PHP5.5b (+23.5% YoY) core income forecast for 2020E is Statistics achievable. Reiterate our non-consensus BUY as current price level 52w high/low (PHP) 325.00/184.10 remains attractive. Our earnings forecasts and DCF-based TP (WACC: 3m avg turnover (USDm) 2.7 7.3%; LTG: 3.0%) are unchanged. Free float (%) 42.6 Issued shares (m) 1,097 Baby steps for Smashburger Market capitalisation PHP229.7B USD4.5B Consumer Staples In 9M19, Smashburger generated roughly PHP1.3b in losses as SSSG Major shareholders: reached double-digit negative figures. By Dec 2019, Smashburger’s SSSG Hyper Dynamic Corp. 25.6% was negative low single-digit (4Q19: mid- to high- negative), a stark Honeysea Corp. 12.0% Winall Holding Corp 5.1% improvement. However, we expect the magnitude of losses to sustain in the near-term as store closures were back-loaded in 4Q19. JFC Price Performance accelerated store closures in 4Q19 (35 stores closed) from 15 stores 340 150 closed as of 9M19. -

Annual Report Permittee Name: City of Daly City

FY 2017-2018 Annual Report Permittee Name: City of Daly City Table of Contents Section Page Section 1 – Permittee Information ................................................................................................................................. 1-1 Section 2 – Provision C.2 Municipal Operations ......................................................................................................... 2-1 Section 3 – Provision C.3 New Development and Redevelopment ....................................................................... 3-1 Section 4 – Provision C.4 Industrial and Commercial Site Controls ......................................................................... 4-1 Section 5 – Provision C.5 Illicit Discharge Detection and Elimination ..................................................................... 5-1 Section 6 – Provision C.6 Construction Site Controls .................................................................................................. 6-1 Section 7 – Provision C.7 Public Information and Outreach .................................................................................... 7-1 Section 9 – Provision C.9 Pesticides Toxicity Controls ................................................................................................ 9-1 Section 10 – Provision C.10 Trash Load Reduction ................................................................................................... 10-1 Section 11 – Provision C.11 Mercury Controls .......................................................................................................... -

Downloadable Menu Updated As of May 8

DOWNLOADABLE MENU UPDATED AS OF MAY 8 TABLE OF CONTENTS RESTAURANT MENU Blackscoop 3-4 Bonchon Chicken 5-8 Chowking 9-10 Classic Savory 11-12 Dairy Queen 13-15 French Baker 16-17 Gringo 18-19 Infinitea 20-23 Jollibee 24-27 KFC 28 Krispy Kreme 29 Mary Grace Café 30 Max’s Restaurant 31 Original Cake 32 Pancake House 33 Ramen Kuroda 34 Red Ribbon 35 S&R New York Style Pizza 36 Samgyeopmasarap 37 Tokyo Tokyo 38-39 TAKE-OUT AND DELIVERY GUIDE 40-41 BLACK SCOOP Available for take-out or order via Shop For Me by , , for delivery. Page 3 BLACK SCOOP Available for take-out or order via Shop For Me by , , for delivery. Page 4 BONCHON CHICKEN CHICKEN SEAFOOD 1pc Chicken Boxed Meal Php 109.00 Crispy Shrimp Boxed Meal Php 175.00 2pc Chicken Boxed Meal Php 172.00 Crispy Squid Boxed Meal Php 175.00 2pc Chops Boxed Meal Php 172.00 Crispy Fish Boxed Meal Php 175.00 Wings Boxed Meal Php 172.00 Fish and Chips Boxed Meal Php 175.00 Double Loaded Sandwhich Boxed Meal Php 179.00 Seafood Chapchae: 2pc Crispy Fish, Half Php 175.00 3pcs Glazed Chicken Fries Boxed Meal Php 172.00 Chapchae, Drink Seafood K-Style: 2pc Crispy Fish, Half 5pcs Glazed Chicken Fries Boxed Meal Php 195.00 Php 198.00 Chapchae, Milk Kreme, Drink Chicken Chapchae Meal Php 172.00 BEEF K-Style Feast A: 1pc Chicken with Rice, Half Php 198.00 Beef Bulgogi Meal Php 175.00 Chapchae, Milky Kreme and Regular Drink Korean Beef Stew Meal Php 185.00 K-Style Feast B: 1pc Chicken with Rice, Fish Php 198.00 Poppers, Milky Kreme and Regular Drink Spicy Korean Beef Stew Php 189.00 Available for take-out or order via Shop For Me by , , for delivery. -

Dine and Win Mall & Restaurant List 23March.Indd

AL GHURAIR CENTRE TIM HORTONS CAFÉ AND BAKE SHOP ALL THE PERKS ESPRESSO CAFÉ UMAMI BASKIN ROBBINS WENDY’S BESTOON SAMAD WING.STOP BIKANERVALA STAR RESTAURANT YAKITATE BUBEE DRINKS CAFFE NERO AL KHAIL GATE COMMUNITY CENTRE CHARLEY’S GRILLED SUBS ARABIAN GRILL RESTAURANT CO. CHIC BOY RESTAURANT CAFETERIA AL KHAIL EXPRESS CHINESE PALACE CHENNAI CURRY PALACE RESTAURANT CHOWKING ORIENT RESTAURANT KFC CINNABON & SEATTLE’S BEST COFFEE LIMS CAFE DENNY’S MADRAS KITCHEN RESTAURANT DIN TAI FUNG RESTAURANT NEW ALBAYAN RESTAURANT - CHICKING DQ GRILL & CHILL QASR ANTAR CAFETERIA FARSI RESTAURANT HAPPY LEMON IL FORNO UNO ARABIAN CENTRE IRVINS BASKIN ROBINS JOLLIBEE BOMBAY CHOWPATHY KFC CHINESE PALACE KRISPY KREME COSTA COFFEE LEMON BAR GLORIA JEAN’S COFFEES MANOUSHE STREET HARDEES MARU UDON HATAM RESTAURANT MCDONALD’S JUNGLE JUICE MCDONALD’S KFC MUKALLA HADHRAMI HONEY MADFOON AL SADDA PAPA JOHNS (JAWAD RESTAURANT) MCDONALD’S PAPPAROTI NEW YORK FRIES PAUL BOULANGERIE PATTISSERIE PIZZA HUT PIZZA HUT SECOND CUP RETRO 7 CAFÉ STARBUCKS COFFEE SHOP STARBUCKS SULTAN BABA EXPRESS TONY ROMAS TAPA KING VANELLIS TERIYAKI BOY / SIZZLIN’ STEAK VIVEL THE CHOCO MONARCH COFFEE SHOP YALLA SAJ BAY AVENUE NJOY CHOCOLATIER & CAFÉ ATTIBASSI OAKBERRY BASKIN ROBBINS PAUL CAFÉ BIKANERVALA PIZZA HUT BURGER KING SARAVANAA BHAVAN CAFÉ FUNKIE TOWN STARBUCKS 25 MAR - 17 APR CARIBOU SUBWAY COSTA UNCLE DEEK ENSO RESTAURANT WHEEL 35 FARSI RESTAURANT YELLOW CHILLI FILLI CAFÉ GAZEBO SHOROOQ COMMUNITY HOT & SPICY CENTRE KABABJI CIRCLE RESTAURANT KAMAT KABABJI KCAL MISTER BAKER KFC PROJECT KUNAFA CAFE KULFILICIOUS STARBUCKS LA BRIOCHE LA FRAGOLA THE MALL MALAK AL TWOOK ARABIAN TEA HOUSE METRO FALCON BURGER KING MOSAIC GOURMET COSTA COFFEE MOTI MAHAL NOODLE EXPRESS RESTAURANT UPTOWN MIRDIFF PAPA JOHNS AL HAKAWATI PIZZA HUT AL ARAB RESTAURANT RAJU OMLET AL SAYER RETAIL EST. -

Equity Research Report Jollibee Foods Corp. 24Th April 2019

Equity Research Report Jollibee Foods Corp. 24th April 2019 Murtaza Salman Abedin Anirudh Ganeriwala Harsharan Singh Muhammad Salik Raymond Widjaja Tang Man Chung Tommy Fang Yucheng Published By CityU Student Research & Investment Club THE FINAL PAGE OF THIS REPORT CONTAINS A DETAILED DISCLAIMER The content and opinions in this report are written by university students from the CityU Student Research & Investment Club, and thus are for reference only. Investors are fully responsible for their investment decisions. CityU Student Research & Investment Club is not responsible for any direct or indirect loss resulting from investments referenced to this report. The opinions in this report constitute the opinion of the CityU Student Research & Investment Club and do not constitute the opinion of the City University of Hong Kong nor any governing or student body or department under the University. 24 April 2019 Asia Pacific/Philippines Equity Research Restaurants Rating OUTPERFORM Price (22 April 19, PHP) 304.00 Target price (PHP) % up from Price on April, 22: 18.58% 360.49 Market cap. (PHP, m) 333,621 Enterprise Value (PHP m) 337,271.4 Jollibee Foods Corporation (JFC:PM) Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. Target price is for 12 months. Research Analysts: Jollibee Foods Corporation (JFC) is an Asian food service multinational company which owns and operates a large number of Quick Service Murtaza Salman Abedin +852 59858568 Restaurants (QSRs). The company is listed on the Philippines Stock [email protected] Exchange and has a market capitalization of PHP347.57 Billion (USD Anirudh Ganeriwala 6.72 Billion) and a revenue of PHP126.2 Billion (USD 2.43 Billion) as [email protected] of 2017. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < 07 March 2019 > Registered national marks as of February 2019 Registration / No. Registration Date Mark Applicant Nice class(es) Application No. DEPARTMENT OF SCIENCE AND TECHNOLOGY - PHILIPPINE 1 4/1718/00002270 7 October 2018 35 TEXTILE RESEARCH INSTITUTE (DOST-PTRI) [PH] 2 4/2013/00004631 13 March 2014 HAVAIANAS FLAT ALPARGATAS S.A. [BR] 25 3 4/2013/00007787 22 September 2013 CRAFT COFFEE Abegail N. Fuentes [PH] 30 and 43 4 4/2013/00503747 11 April 2016 JAGABEE CALBEE, INC. [JP] 29 QLA`S 50 BILLION DOLLAR 5 4/2014/00004109 12 April 2018 DANIEL STEVEN PEÑA SR. [PH] 16 and 41 MAN NOUVAC TECHNOLOGIES AND 6 4/2015/00011548 3 January 2019 ALEXANDER C. YAO [PH] 35 SERVICES, INC. 7 4/2015/00012808 16 August 2018 AQUA METALS AQUA METALS, INC. [US] 40 8 4/2015/00012809 16 August 2018 AQUAREFINERY AQUA METALS, INC. [US] 40 9 4/2015/00505481 25 October 2018 KINGONE YIN, HONGSHENG [CN] 9 10 4/2015/00505977 3 January 2019 PETALIER BOXED BLOOMS YAP, DIANA GRACE V [PH] 31 TENACITY AUTO PARTS CO., 11 4/2015/00506208 7 October 2018 TENACITY 12 LTD. [TW] Grains Innovation and Solutions 12 4/2016/00000185 6 January 2019 TOUGHROLLS 7 Co., Inc. [PH] 13 4/2016/00002582 4 November 2018 GELATTTO DAVID FU [HK] 25 14 4/2016/00010262 3 January 2019 STA. -

Greenwich Jollibee Bonchon Kfc Classic Savory Mang

GREENWICH JOLLIBEE BONCHON Ground Level Ground Level Ground Level (042) 373 77-11 (042) 710-0002 (042) 717-4911 KFC BUDDY’S RESTAURANT CLASSIC SAVORY Ground Level Second Level Ground Level (042) 323-2189 (042) 710-48-22 (042) 373-4606 MANG INASAL CHOWKING RED RIBBON Ground Level Ground Level Ground Level (042) 795-3800 (042) 717-3416 (042) 717-2943 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP BURGER KING DUNKIN DONUTS INFINITEA Ground Level Ground Level Third Level (042) 717-9532 CHATIME GERRY’S RESTARANT KOFFEE KLATCH Ground Level Ground Level Second Level 0906-483-1459 (042) 717-9515 (042) 713-0214 CLYDES GONG CHA MAX’S RESTAURANT Ground Level Second Level Second Level 0923-957-5922 09753097279 (042) 717-9032 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP PAN DE MANILA POTATO CORNER STARBUCKS Ground Level Third Level Ground Level 0977-797-0973 0925-889-3600 0917-851-5292 PEPPER LUNCH SHAWARMA SHACK TOKYO TOKYO Ground Level Ground Level Second Level (042) 717-0094 0917-793-0263 POP AND MIX SIOMAI HOUSE TURKS Third Level Second Level Third Level 0917-639-0902 0999-887-0919 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM PICK-UP & TAKE-OUT RIDER DELIVERY PICK-UP WINGED POTATO ZARK’S BURGER Third Level Ground Level 0927-759-3789 (042) 717-0094 OPPA BUFFALO WINGS SAMGYEOPSAL AND THINGS Second Level Ground Level 0966-985-4089 (042) 322-9483 COMMUNITY CURBSIDE SM CITY LUCENA SM CITY LUCENA SMSUPERMALLS.COM -

FY 2009-2010 Annual Report Permittee Name: City of San José Appendix 4-1 C.4.B.Iii.(1) Potential Facilities List

FY 2009-2010 Annual Report Appendix 4-1 Permittee Name: City of San José C.4.b.iii.(1) Potential Facilities List ORG_CODE SIC_CODE ORG_NAME ST_NUM ST_DIR ST_NAME ST_TYPE ST_SUB_TYPE ST_SUB_NUM 11385 5812 PIN HIGH GOLF CENTER 4701 N 1st St 13062 3540 3B MACHINING 2292 Trade Zone Blvd 13086 7542 SEVENTY SIX AUTO DETAILING 1099 Blossom Hill Rd 16046 3499 KC METAL PRODUCTS INC 1960 Hartog Dr 16322 5812 LA TROPICANA FOODS 1630 Story Rd 16330 5812 MI PUEBLO FOOD CENTER #4 1745 Story Rd 16331 5812 MARTIN FARNHAM SCHOOL 15711 Woodard Rd 15664 3540 K&H LAB INC 2744 Aiello Dr 9761 5812 CHARLES FANMATRE SCHOOL 2800 New Jersey Ave 9788 5411 MI TIERRA MERCADO Y CARNICERIA 1130 E Santa Clara St 9726 5812 DAKAO SANDWICHES 98 E San Salvador St 9730 5812 DAC-PHUC RESTAURANT 198 W Santa Clara St 9807 5812 HOLY SPIRIT SCHOOL 1198 Redmond Ave 9811 5812 CATERMAN INC 448 Reynolds Cir Suite B 9812 5812 MIKE'S PIZZA 497 Reynolds Cir 9846 5812 TRINE'S CAFE 146 S Jackson Ave 9853 5812 GOMBEI 193 E Jackson St 9862 5812 RESTAURANT KAZOO 250 E Jackson St 9863 5411 SHOP N GO 29 S Jackson Ave 9822 5812 MATHSON SCHOOL 2050 Kammerer Ave 9833 5812 DELOS BAGBY SCHOOL 1850 Harris Ave 11661 7530 MILLENNIUM AUTO SERVICE 2520 Story Rd 11523 5812 CATHAY CHINESE CUISINE 1339 N 1st St 11538 5812 SAN JOSE JOB CORPS 3485 East Hills Dr 11816 3540 TAGDESIGN INC. 619 University Ave 12112 1741 PIONEER CONCRETE 139 S White Rd 13600 5093 TUNG TAI GROUP 1726 Rogers Ave 16257 5411 LOS PRIMOS MEAT MARKET 1539 S Winchester Blvd 15939 5812 KIM'S CAFE-CANDESCENT 6580 Via del Oro 16248 7532 -

Non-Participating Airport Outlets

Non-participating airport outlets Category Departments Baskin & Robbins Bombay Chowpatty Bricco Café Brioche Doree Burger King Butlers Café CAFÉ Chocolat Café Nero Camden Foods Camden Foods Carluccios Caviar House Charley's Grill and Sub Cho Gao Chowking Cinnabon Cold Stone Cosi Dining / Costa restaurants Delizie Draft House Giraffe Haagen Daaz Heineken Bar JACK'S Bar & Grill KFC Krispy Kreme Le Pain Qoutidien Mary Brown Masale McDonalds Mezzanine Restaurant Mezze Express O' Briens Ocean Basket Paul Café PICNIC Gourmet Market Pink Berry Pint 19 Pret A Manger Pulp Bar Juice Red Carpet Rosso Vivo Rupee Room Safar Seafood Bar Seafood Restaurant Shake Shack Shawarmanji Starbucks Subway Sweet Factory Taqado Taste of India Texas Chicken Thai Express The HUB The Kitchen/Wolfgang The Noodle House Wafi Gourmet (WG) Yo! Sushi Al Ansari Al Noor Bank Currency Commercial Bank of Dubai Dubai Express Exchange Emirates NBD Services Sharaf Exchange Travelex Exchange UAE Exchange BE Relax Spa Dubai International Hotel Massage and O2 Spa Fitness Spa Express** Timeless Spa Boots Pharmacy BinSina Dallmayr Vending Machines Masafi Vending Machine Red Bull Vending Machine Retailer Le Clos Self Service Kiosk Sweet Factory Al Wefaq Car Rental Alpha Destinations Management Arabian Tours Atlantis The Palm Dubai AVIS Diamond Lease Car Rental Dollar rent a car Dollar Car Rental Europe Car Europe rent a car Fast Rent-A-Car Golden Sands Hotel Apartments Hotels/Rent a Habtoor Hotel Car Hertz Intercontinental Hotel Group Jumeirah Stay Different Lotus Hotel Marriot The Ritz Carlton Movenpick National rent a car Payless Car Rental Sixt Car Rental The Address Hotel Thrifty Car Rental Thrifty rent a car Airport Business Center Aramex Baggage Wrapping Services DU Telecommunication Others Du Business Center Etisalat Telecommunication Etisalat Business Center CNN Traveller . -

FOR SUBLEASE: CENTRE POINT PLAZA: 39355 California St., Suite 307 – Fremont, CA

FOR SUBLEASE: CENTRE POINT PLAZA: 39355 California St., Suite 307 – Fremont, CA Available Now: ±2,285 SF Office Space As exclusive agents, we are pleased to offer the following space: LOCATION INFO: • ±2,285 SF –3rd Floor Office Space • Sublease or Longer Term Direct w/ Landlord • LED: 12/31/2022 • Asking Rate: $2.70 Modified Full Service LOCATION HIGHLIGHTS: • Corner Location at California Street & Walnut Avenue • Walking Distance to Downtown Fremont BART • Covered Parking Structure • Medical uses Permitted • Walking Distance to the Fremont Hub Shopping Center • Contact Broker for Tour Instructors Curtis Stahle 510.300.0222 [email protected] CA RE Lic. #01955258 1111 Broadway, Suite 100, Oakland, CA 94607 www.ngkf.com The distributor of this communication is performing acts for which a real estate license is required. The information contained herein has been obtained from sources deemed reliable but has not been verified and no guarantee, warranty or representation, either express or implied, is made with respect to such information. Terms of sale or lease and availability are subject to change or withdrawal without notice. FOR SUBLEASE: CENTRE POINT PLAZA: 39355 California St., Suite 307 – Fremont, CA Suite 307 Available Now Curtis Stahle 510.300.0222 [email protected] CA RE Lic. #01955258 1111 Broadway, Suite 100, Oakland, CA 94607 www.ngkf.com The distributor of this communication is performing acts for which a real estate license is required. The information contained herein has been obtained from sources deemed reliable but has not been verified and no guarantee, warranty or representation, either express or implied, is made with respect to such information.