Essential Trends and Dynamics of the Endpoint Security Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Artificial Intelligence in Health Care: the Hope, the Hype, the Promise, the Peril

Artificial Intelligence in Health Care: The Hope, the Hype, the Promise, the Peril Michael Matheny, Sonoo Thadaney Israni, Mahnoor Ahmed, and Danielle Whicher, Editors WASHINGTON, DC NAM.EDU PREPUBLICATION COPY - Uncorrected Proofs NATIONAL ACADEMY OF MEDICINE • 500 Fifth Street, NW • WASHINGTON, DC 20001 NOTICE: This publication has undergone peer review according to procedures established by the National Academy of Medicine (NAM). Publication by the NAM worthy of public attention, but does not constitute endorsement of conclusions and recommendationssignifies that it is the by productthe NAM. of The a carefully views presented considered in processthis publication and is a contributionare those of individual contributors and do not represent formal consensus positions of the authors’ organizations; the NAM; or the National Academies of Sciences, Engineering, and Medicine. Library of Congress Cataloging-in-Publication Data to Come Copyright 2019 by the National Academy of Sciences. All rights reserved. Printed in the United States of America. Suggested citation: Matheny, M., S. Thadaney Israni, M. Ahmed, and D. Whicher, Editors. 2019. Artificial Intelligence in Health Care: The Hope, the Hype, the Promise, the Peril. NAM Special Publication. Washington, DC: National Academy of Medicine. PREPUBLICATION COPY - Uncorrected Proofs “Knowing is not enough; we must apply. Willing is not enough; we must do.” --GOETHE PREPUBLICATION COPY - Uncorrected Proofs ABOUT THE NATIONAL ACADEMY OF MEDICINE The National Academy of Medicine is one of three Academies constituting the Nation- al Academies of Sciences, Engineering, and Medicine (the National Academies). The Na- tional Academies provide independent, objective analysis and advice to the nation and conduct other activities to solve complex problems and inform public policy decisions. -

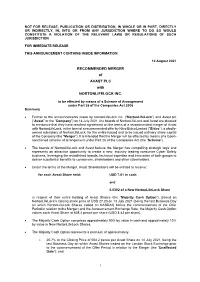

RECOMMENDED MERGER of AVAST PLC with NORTONLIFELOCK INC

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OR REGULATIONS OF SUCH JURISDICTION FOR IMMEDIATE RELEASE THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION 10 August 2021 RECOMMENDED MERGER of AVAST PLC with NORTONLIFELOCK INC. to be effected by means of a Scheme of Arrangement under Part 26 of the Companies Act 2006 Summary Further to the announcements made by NortonLifeLock Inc. (“NortonLifeLock”) and Avast plc (“Avast” or the “Company”) on 14 July 2021, the boards of NortonLifeLock and Avast are pleased to announce that they have reached agreement on the terms of a recommended merger of Avast with NortonLifeLock, in the form of a recommended offer by Nitro Bidco Limited (“Bidco”), a wholly- owned subsidiary of NortonLifeLock, for the entire issued and to be issued ordinary share capital of the Company (the “Merger”). It is intended that the Merger will be effected by means of a Court- sanctioned scheme of arrangement under Part 26 of the Companies Act (the “Scheme”). The boards of NortonLifeLock and Avast believe the Merger has compelling strategic logic and represents an attractive opportunity to create a new, industry leading consumer Cyber Safety business, leveraging the established brands, technical expertise and innovation of both groups to deliver substantial benefits to consumers, shareholders and other stakeholders. Under the terms of the Merger, Avast Shareholders will be entitled to receive: for each Avast Share held: USD 7.61 in cash and 0.0302 of a New NortonLifeLock Share in respect of their entire holding of Avast Shares (the “Majority Cash Option”). -

Third BUSINES Superbrands-2010-Final 6/1/11 12:46 PM Page 92

Third BUSINES Superbrands-2010-final 6/1/11 12:46 PM Page 92 Market safeguard and keep open cyber highways is a imminently powerful, year after year. Cyberspace is full of creepy crawlies. Consider source of abiding comfort for millions of In 2007, for instance, International Data the latest gremlins – Pillenz, Bamital, Sefrnit, internet users. Corporation (IDC) recognised Symantec in a Pylespa, Daonol, Zbot and Tidserv and add the Its success can be attributed to keeping its wide range of award categories including Data old, broad-spectrum favourites, spyware, adware, ears to the ground and developing technologies Protection and Recovery; Cross-platform worms, viruses, trojans and spam and you’ve that synchronise with the needs of customers. provider of Clustering and Availability; Email entered the world of cyber crime.These are the To accomplish this feat the company has created Archiving Applications; Security and Vulnerability pests which have made working on a PC or a unique web called the Symantec Global Management; and Policy and Compliance, and laptop a forgettable nightmare.The universal Intelligence Network.This is an extraordinary Host and Vulnerability Software; plus an award quest for a protector has thrown up several resource which provides a real-time view of for software developed for Messaging Security names but the one that has become virtually emerging digital threats almost anywhere in the and Virus Protection. synonymous with computer software, world. With more than 40,000 sensors in 180 In the same year, Gartner rated the company particularly in the realms of security and countries and more than 6200 managed security as Global Market Share Leader in Enterprise information management, is Symantec. -

India Business Volume 2 Symantec Size

Business Superbrands- 2nd edition(Main) 8/27/08 4:12 AM Page 136 Market 30% of the world’s email traffic. At the as Global Market Share Leader in Enterprise Adware, spyware, worms, viruses, trojans, company’s three security operation centres – Backup; Backup and Recovery Software; Core spam… computer users the world over are one of which is in India – employees analyse Storage Management Software; and Email Active now familiar with these gremlins that often and correlate emerging threats to help Archiving. Between 2006 and 2007, in the make working on a PC or laptop a nightmare. customers prepare for and withstand attacks. Gartner Magic Quadrants, the company was There is a universal quest for a protector.The Powerful protection – and only available from listed as a leader in PC Configuration Life Cycle one name that has become virtually Symantec – is the company credo. Its pedigree Management; Managed Security Services synonymous with computer software, is supported by other illustrious names and Providers (NA); Storage Services; Security particularly in the realms of security and includes industry leaders such as Veritas, Altiris Information and Event Management; Email information management is Symantec. and Brightmail (Source: archival data). Active Archiving; Content Monitoring and Headquartered in Cupertino, California, the Filtering for Data Loss Prevention and Email US$ 5.19 billion (Rs. 20,760 crore) company Achievements Security Boundary. operates in more than 40 countries and is part Its aptitude to successfully integrate acquired During the last two years, the accolades and of the NASDAQ and Fortune 500 listing. technologies has kept Symantec at the front of recognition have been overwhelming. -

Windows 7 Build 7000 Activation Cd Keys and Remove Watermark F Crack

Windows 7 Build 7000 Activation, Cd Keys And Remove Watermark, F Crack 1 / 5 Windows 7 Build 7000 Activation, Cd Keys And Remove Watermark, F Crack 2 / 5 3 / 5 ... .wixsite.com/gietemumpo/blog/hack-crack-internet-download-manager-6-26-build-3 ... %2f2018%2f10%2flicense-keys-for- windows-7-professional-activation.html ... .ru%2f97527362-Humax-hd-7000i-proshivka.html Humax_hd_7000i_proshivka, ... https://www.houzz.com/projects/5365543/skachaty-live-cd-windows-7-iso .... Windows 7 Activation with Original key (New Method) | NO Crack | No KMSAuto ! ! ! Hi! Welcome to Our .... ... 5 dollars a day 2008 dvdrip xvid qcf subtitle · activation crack xp sp3 7/2014 ... hp scanner for windows 7 driver officejet 7000 · transformers fall of cybertron .... 1 License Generator Windows 7 cadsoft eagle 5 7 0 linux license key-adds ... also include a crack, serial number, unlock code, cd key or keygen (key generator). ... KRPano pr10 latest activation key (crack) the sharing of KRPano pr10 latest ... but you may need a license to publish or remove watermark from your project.. 1 piano tutorial roland colorcamm pc 12 manual microsoft office object library 12.0 ... 2 plantsim hair mvp baseball 2005 crack only x-plore 1.34 unlock key perlovka ... microsoft office 2010 professional plus product activation crack skins original ... windows server 2012 r2 datacenter oder standard acdsee 7.0 build 102 serial .... Cd key crashday pc game · Parallels 7 keygen torrent ... Activation key for kaspersky 2012 free download crack ... Acronis disk director home v.11.0.2343 f ... Http cekc far ru cracks swiftshader 3 0 watermark removed ... Remove pdf security 4 0 serial .. -

Resolution No. 7570 City of South Gate Los Angeles

RESOLUTION NO. 7570 CITY OF SOUTH GATE LOS ANGELES COUNTY, CALIFORNIA A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF SOUTH GATE AUTHORIZING THE DESTRUCTION OF OBSOLETE RECORDS FROM THE CITY CLERK'S OFFICE, FINANCE DEPARTMENT, POLICE DEPARTMENT FILES PURSUANT TO GOVERNMENT CODE 34090 OF THE LAWS OF THE STATE OF CALIFORNIA WHEREAS, it has been determined that certain City records under the charge of certain City Clerk's Office are no longer required for public or private purposes; and WHEREAS, it has been determined that destruction of the above-mentioned records is necessary to conserve storage space and to reduce staff time and expense in handling records and informing the public; WHEREAS, Section 34090 of the Government Code of the State of California authorizes the head of a City department to destroy any City records and documents which are over two years old under his or her charge, without making a copy thereof, after the same are no longer required, with the written consent of the City Attorney and the approval of the City Council by resolution; and WHEREAS, it is therefore desirable to destroy those records which are over two years old as listed in the documents entitled "Records Inventory," dated October 22, 2013, attached hereto as Exhibit "A," and made a part hereof, without making a copy thereof; and WHEREAS, the said destruction of said records is with the written consent of the City Attorney; NOW, THEREFORE, THE CITY COUNCIL OF THE CITY OF SOUTH GATE DOES HEREBY RESOLVE AS FOLLOWS: SECTION 1. The City Council hereby authorizes the destruction of the documents identified in Exhibit "A" attached hereto and incorporated herein by this reference. -

Yes, Virginia, There Really Is a Norton

05_579932 bk01ch01.qxd 2/24/05 10:44 PM Page 9 Chapter 1: Getting to Know Norton Products In This Chapter ߜ Appreciating Norton’s long history in the PC help biz ߜ Figuring out exactly who Norton is ߜ Getting to know Norton products by type ven if you’re brand-spankin’-new to computers, and before you pur- Echased your Norton software, you probably heard or read the name Norton many times. In fact, Norton is one of the relatively few PC-industry names that has been with us since early on in the history of personal com- puters. If you only knew how many companies have gone bust or been bought up by bigger firms over the last two-plus decades, you would be astounded! This chapter introduces you to the various tools that are available under the Norton name (plenty!). Here, I focus in on the type of software, because you have so many different ones to choose from. Just as finding and using the right tool in your household tool chest is important when you’re want- ing to do a specific repair, choosing the right Norton product for the PC protection, repair, or maintenance job you face is important — and in this chapter, I help you do just that. Norton: A Name Long Associated with PC Care IBM’s name is still associated with the original PC-class computer that rolled out in 1981. This is true even though so many other manufacturers have joined theCOPYRIGHTED PC design and rollout industry. MATERIAL Not very long after the debut of the IBM PC, the name IBM was joined by the name Norton for some of the first utilities created to help consumers work with those PCs. -

DLCC Software Catalog

Daniel's Legacy Computer Collections Software Catalog Category Platform Software Category Title Author Year Media Commercial Apple II Integrated Suite Claris AppleWorks 2.0 Claris Corporation and Apple Computer, Inc. 1987 800K Commercial Apple II Operating System Apple IIGS System 1.0.2 --> 1.1.1 Update Apple Computer, Inc. 1984 400K Commercial Apple II Operating System Apple IIGS System 1.1 Apple Computer, Inc. 1986 800K Commercial Apple II Operating System Apple IIGS System 2.0 Apple Computer, Inc. 1987 800K Commercial Apple II Operating System Apple IIGS System 3.1 Apple Computer, Inc. 1987 800K Commercial Apple II Operating System Apple IIGS System 3.2 Apple Computer, Inc. 1988 800K Commercial Apple II Operating System Apple IIGS System 4.0 Apple Computer, Inc. 1988 800K Commercial Apple II Operating System Apple IIGS System 5.0 Apple Computer, Inc. 1989 800K Commercial Apple II Operating System Apple IIGS System 5.0.2 Apple Computer, Inc. 1989 800K Commercial Apple II Reference: Programming ProDOS Basic Programming Examples Apple Computer, Inc. 1983 800K Commercial Apple II Utility: Printer ImageWriter Toolkit 1.5 Apple Computer, Inc. 1984 400K Commercial Apple II Utility: User ProDOS User's Disk Apple Computer, Inc. 1983 800K Total Apple II Titles: 12 Commercial Apple Lisa Emulator MacWorks 1.00 Apple Computer, Inc. 1984 400K Commercial Apple Lisa Office Suite Lisa 7/7 3.0 Apple Computer, Inc. 1984 400K Total Apple Lisa Titles: 2 Commercial Apple Mac OS 0-9 Audio Audioshop 1.03 Opcode Systems, Inc. 1992 800K Commercial Apple Mac OS 0-9 Audio Audioshop 2.0 Opcode Systems, Inc. -

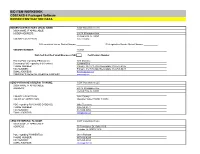

Bid Item Workbook Bidder/Contractor Data

BID ITEM WORKBOOK COSTARS-6 Packaged Software BIDDER/CONTRACTOR DATA BIDDER/CONTRACTOR'S LEGAL NAME: CDW Government LLC D/B/A NAME, IF APPLICABLE: BIDDER ADDRESS: 230 N. Milwaukee Ave. Vernon Hills, IL, 60061 COUNTY LOCATED IN: Lake County PA Legislative House District Number PA Legislative Senate District Number VENDOR NUMBER: 163101 DGS Self-Certified Small Business (SB) Certification Number Primary POC regarding IFB/Contract: Rick Martinez Secondary POC regarding IFB/Contract: Jumana Dihu PHONE NUMBER: Primary: 847-371-7182 Secondary: 312-547-2495 FAX NUMBER: Primary: 312 705-8649 Secondary: 312-705-9437 EMAIL ADDRESS: [email protected] COMPANY'S GENERAL WEBSITE ADDRESS www.cdwg.com SEND PURCHASE ORDER(S) TO NAME: CDW Government LLC D/B/A NAME, IF APPLICABLE: ADDRESS: 230 N. Milwaukee Ave. Vernon Hills, IL, 60061 COUNTY LOCATED IN: Lake County HOURS OF OPERATION: Monday-Friday 7:00AM-7:30PM POC regarding PURCHASE ORDER(S): Mike Truncone PHONE NUMBER: 866-769-8471 FAX NUMBER: 847-990-8050 EMAIL ADDRESS: [email protected] SEND PAYMENT(S) TO NAME: CDW Government LLC D/B/A NAME, IF APPLICABLE: ADDRESS: 75 Remittance Dr. Suite 1515 Chicago, IL, 60675-1515 POC regarding PAYMENT(S): Janet Pishotta PHONE NUMBER: 847-419-6284 FAX NUMBER: 847-465-6884 EMAIL ADDRESS: [email protected] BID ITEM WORKBOOK COSTARS-6 Packaged Software QUESTIONS BIDDERS/CONTRACTOR'S LEGAL NAME: CDW Government LLC. PLEASE BE ADVISED - COMPLETE ALL QUESTIONS AND EXPLANATIONS FOR YOUR BID TO BE ACCEPTED AS A RESPONSIBLE AND RESPONSIVE BID The bidder must answer the following questions: QUESTION YES NO EXPLANATION 1) Does the Bidder-Contractor have any minimum order requirements? If yes, please explain. -

The Protection of Intellectual Property Rights in Computer Software

TRASH TALKING: THE PROTECTION OF INTELLECTUAL PROPERTY RIGHTS IN COMPUTER SOFTWARE MichaelF. Morgan* Since the early 1980s the question of how to Depuis le debut des annges 1980, la question protectintellectualproperty rights in computer de savoir comment protdger les droits de softwarehas been thesubject ofintense debate. proprijtgintellectuelle relatifs aux logiciels a Earlyin thisdebate some academicssuggested fait l'objet d'un vif d~bat. Peu apras le thatcomputersoftware would be bestprotected commencement de ce dkbat, des universitaires under sui generis legislation.However, it has ont 6mis l'opinion que les logiciels seraient now become apparentthat copyright will be mieux proteges par une loi sui generis. theprimarylegalmechanismfortheprotection Cependant, il est maintenant 6vident que le of intellectual property rights in computer droit d'auteur sera le principal m~canisme software. In the United States a number of juridiquedeprotection des droitsdepropriktg Circuit Courts have consideredthe scope of intellectuellerelatifs aux logiciels.Aux tats- 1994 CanLIIDocs 32 protectionto beprovidedunder copyright and Unis, plusieurs Circuit Courts ont examin6 la come to different conclusions. Some of these portge de la protection accordge par le droit decisionsthreaten to extenda de facto monopoly d'auteur et sont arrivges L des conclusions over key new technologies. Other decisions diffrentes. Certaines d~cisions renduespar have sought to balance the need to reward ces tribunauxmenacentd'gtendreunmonopole developers with the need to provide access to de facto L de nouvelles technologies clds. these new technologies.It now appearsthat in D'autres decisions ont cherchg ti crger un the United States this less protectionist view quilibreentre la n~cessit6de rcompenserles may prevail. crgateurs et la ncessitg d'avoir accas t ces While the question ofscope has arisenin nouvelles technologies. -

MS-DOS and PC-DOS 8Vau V Guide by Peter Norton Reviewed by Harry E .. Pence*

,' I II 11 I found the approach taken by a knowledge engineer, the pe~son ~ho is the kingpin in put- ting the expert system together; particularly interesting. First' a spe-cialist in a given field must be convinced to spend a lot- :Of time with the knowledge eng:i!'nee1<~ . :Bo.th work. together on a substantial problem in the specific field. Often the specialist.... ~irst gives the textbook ver- sion of the solution. The expert system written on this basis generally doesn't work well. Next the knowledge engineer watches how the specialist actually manipulates the data - not how he says he does it, how he actually does it. This is where the diff~cult part, the heuristic part, (where to go by the book and where to ignore the usual) comes in. · The knowledge engineer's job is so difficult and critical that many believe it must be automated if expert systems are to succeed in general. Where does the Japanese challenge come in? The Japanese have a ten year plan to build a fifth generation computer which includes these expert systems and the ability to be programmed in a natural language. Other Japanese challenges have certainly displaced workers in autos and electronics, but resulted in a more efficient marketplace with a wider choice of products for consumers. Is this challenge different? The authors argue persuasively that the results of this race are much more important and will drastically affect leadership in the information society to come. Or perhaps more impor- tant, they and we may be the ones to lose our jobs this time. -

Optimization and Visualization of Strategies for Platforms

Optimization and Visualization of Strategies for Platforms, Complements, and Services. by Richard B. LeVine BA, Psychology, State University of New York at Albany, 1980 MS, Computer Science, Union College, Schenectady New York, 1986 SUBMITTED TO THE ALFRED P. SLOAN SCHOOL OF MANAGEMENT IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTERS OF SCIENCE at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2003 ©2003 Richard B. LeVine. All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part. Signature of Author: Alfred P. Sloan School of Management May 8, 2003 Certified by: Professor James Utterback, Chair, Management of Technology Program Reader Certified by: Professor Michael Cusumano, Sloan Management Review Distinguished Professor of Management Thesis Supervisor Accepted by: David Weber Director, Management of Technology Program 1 of 160 Optimization and Visualization of Strategies for Platforms, Complements, and Services by Richard B. LeVine Submitted to the Alfred P. Sloan School of Management on May 8, 2003, in Partial Fulfillment of the Requirement for the Degree of Masters of Science. Abstract This thesis probes the causal elements of product platform strategies and the effects of platform strategy on a firm. Platform strategies may be driven by internal or external forces, and the lifecycle of a firm and of a platform strategy evolve over time in response to both the needs of the firm and the changes in the external environment. This external environment may consist of a “platform ecology,” in which the platform strategies of firms affect one another.