We See the Future in STEEL

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Securities and Exchange Commission Washington, D.C. 20549 Form 8‑K Current Report

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8‑K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 DATE OF REPORT - December 16, 2013 (Date of Earliest Event Reported) AK STEEL HOLDING CORPORATION (Exact name of registrant as specified in its charter) Commission File No. 1-13696 Delaware 31-1401455 (State of Incorporation) (I.R.S. Employer Identification No.) 9227 Centre Pointe Drive West Chester, OH 45069 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (513) 425-5000 Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below): q Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) q Solicitation material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) q Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) q Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Item 5.02 Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers. On December 16, 2013, John F. Kaloski, Executive Vice President and Operating Officer, gave notice of his retirement from AK Steel Holding Corporation (the “Company”), effective January 31, 2014. The Company issued a press release with respect to Mr. Kaloski’s retirement, a copy of which is attached hereto as Exhibit 99.1 and is incorporated by reference herein. -

EMERGE As a Stronger Company in 2014

EMERGE as a stronger company in 2014 ANNUAL REPORT AND FORM 10-K 2014 9853c1.indd 1 4/1/15 8:04 AM EMERGE AS A STRONGER COMPANY IN 2014: At AK Steel, we were determined to “EMERGE as a stronger company” in 2014 by striving to Execute our plans, Maintain our focus on our key values, Enhance our earnings and cash flow as we continued to seek the full benefits of our Raw materials strategic initiatives, Grow profitable sales and enhance margins because we are Energized for our future. single OSHA recordable injury. And, our Works, and Coshocton Works each James L. Wainscott Zanesville plant continued its record-setting also setting records for retreats. Chairman, President and performance for OSHA lost workday Both our carbon and specialty steel Chief Executive Officer cases, finishing the year with 4,270 customers ranked AK Steel “Number days without an OSHA lost workday. One” in quality compared to our peers, Our Butler Works tied its best ever according to independent surveys by record for OSHA recordables and Jacobson and Associates for 2014. newly-acquired Dearborn Works and At AK Steel, serving customers better Overall, 2014 was a year of Mountain State Carbon, LLC set their than any other steelmaker with some of the progress for AK Steel. Despite battling best annual records for both OSHA finest carbon, stainless and electrical steel unprecedented extreme winter weather recordables and lost workday cases. products produced anywhere in the world conditions, energy price spikes, a shortage In addition, our Middletown Works is at the heart of who we are. -

2020 Annual Report Cleveland-Cliffs Share Performance Vs

2020 Annual Report Cleveland-Cliffs Share Performance vs. Peers One Year Three Year Five Year (percent change over 2020) (percent change over three years) (percent change over five years) CLF +73% CLF +84% CLF +822% X +47% STLD +47% MT +137% MT +31% NUE +31% X +110% STLD +8% MT +8% STLD +106% NUE – 5% X – 5% NUE +32% Jan Apr Jun Sept Dec Jan-18 Jul Dec Jun-19 Dec Jun-20 Dec Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Message from the CEO Dear Fellow Shareholders: steel. Moreover, with the current scarcity of domestic prime scrap in the marketplace, our timing to bring In the 173 years of our existence this product to market in 2021 could not be better. as a company, 2020 proved Very importantly, our Toledo plant is the first Direct to be the most seminal year in Reduction plant that was built with the capability to our history. In a year that will be utilize hydrogen as reductant, partially replacing natural forever known for the COVID-19 gas when hydrogen becomes commercially available. pandemic, Cleveland-Cliffs transformed itself from a mining company supplying With our leadership position in the steel industry, it is iron ore pellets to North American steel companies very important to acknowledge that climate change into the largest flat-rolled steel producer in North is one of the most important issues impacting our America. This transformation was accomplished industry and our planet, and to take action to mitigate through the acquisitions of AK Steel and ArcelorMittal it. -

Cleveland-Cliffs Annual Report 2021

Cleveland-Cliffs Annual Report 2021 Form 10-K (NYSE:CLF) Published: February 26th, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE ☐ SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 1-8944 clf-20201231_g1.jpg CLEVELAND-CLIFFS INC. (Exact name of registrant as specified in its charter) Ohio 34-1464672 (State or Other Jurisdiction of (I.R.S. Employer Incorporation or Organization) Identification No.) 200 Public Square, Cleveland, Ohio 44114-2315 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (216) 694-5700 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Shares, par value $0.125 per share CLF New York Stock Exchange Securities registered pursuant to section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ NO ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Bernard Fidel, Et Al. V. AK Steel Holding Corporation, Et Al. 00-CV

FILED AUG 2 8 2000 W AUG 3 0 2000 KENNETH J. MURPHY, Clerk CINCINNATIL OHIO UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF OHIO WESTERN DIVISION BERNARD FIDEL and IRONWOOD Lead Case No. C-1-00-320 CAPITAL MANAGEMENT, On Behalf of (Consolidated with No. C-1-00-349) Themselves and All Others Similarly Situated, Plaintiffs, Judge Herman J. Weber CLASS ACTION AK STEEL HOLDING CORPORATION, CONSOLIDATED AMENDED ARMCO INC., RICHARD M. WARDROP, COMPLAINT FOR VIOLATION JR., JAMES F. WILL, JAMES L. WAREHAM, OF THE FEDERAL SECURITIES JAMES L. WAINSCOTT, JOHN G. HRITZ, LAWS ALLEN BORN, BONNIE G. HILL, ROBERT H. JENKINS, LAWRENCE A. LESER, (Jury Trial Demanded) ROBERT E. NORTHAM, CYRUS TANG and JAMES A. THOMSON, Defendants INTRODUCTION AND OVERVIEW 1. This is an action on behalf of those who purchased or otherwise acquired AK Steel Holding Corporation ("AK Steel" or the "Company") publicly traded securities between July 15, 1999 through January 25, 2000 (the "Class Period"). This action also is brought on behalf of a sub- class of those who held Armco Inc. ("Armco") shares as of August 25, 1999 and were thereby entitled to vote to approve the merger with AK Steel (the "sub-class"). 2. AK Steel is a fully integrated producer of flat-rolled carbon, stainless and electrical steels. AK Steel's steel operations consist of eight steelmaking and finishing plants in Indiana, Kentucky, Ohio and Pennsylvania. AK Steel's other operations include steel pipe and tubing products, snow plows and ice control products for light trucks and the operation of the Greens Port Industrial Park in Texas. -

Word Template for Creating Internal Use Only Pdfs in Portrait Mode

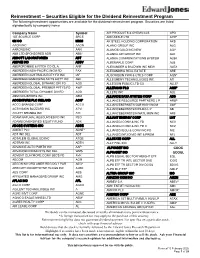

Reinvestment – Securities Eligible for the Dividend Reinvestment Program The following investment opportunities are available for the dividend reinvestment program. Securities are listed alphabetically by company name Company Name Symbol AIR PRODUCTS & CHEMICALS APD 1ST SOURCE CORP SRCE AIRCASTLE LTD AYR* 3M CO MMM AK STEEL HOLDING CORPORATION AKS AAON INC AAON ALAMO GROUP INC ALG AARONS INC AAN ALAMOS GOLD INC NEW AGI* ABB LTD SPONSORED ADR ABB* ALASKA AIR GROUP INC ALK ABBOTT LABORATORIES ABT ALASKA COMMUNICATIONS SYSTEM ALSK ABBVIE INC ABBV ALBEMARLE CORP ALB ABERCROMBIE & FITCH CO CL A ANF ALEXANDER & BALDWIN INC NEW ALEX ABERDEEN ASIA-PACIFIC INCM FD FAX ALEXANDRIA REAL ESTATE ARE ABERDEEN AUSTRALIA EQTY FD INC IAF ALGONQUIN PWR & UTILS CORP AQN* ABERDEEN EMERGING MKTS EQTY INC AEF ALLEGHENY TECHNOLOGIES INC ATI ABERDEEN GLOBAL DYNAMIC DIV FD AGD ALLEGION PUBLIC LTD CO ALLE* ABERDEEN GLOBAL PREMIER PPTYS FD AWP ALLERGAN PLC AGN* ABERDEEN TOTAL DYNAMIC DIV FD AOD ALLETE INC ALE ABM INDUSTRIES INC ABM ALLIANCE DATA SYSTEM CORP ADS ACCENTURE PLC IRELAND ACN* ALLIANCE RESOURCE PARTNERS L P ARLP ACCO BRANDS CORP ACCO ALLIANCEBERNSTN GLB HIGH INCM AWF ACTIVISION BLIZZARD INC ATVI ALLIANCEBERNSTEIN HLDG L P AB ACUITY BRANDS INC AYI ALLIANCEBERNSTEIN NATL MUN INC AFB ADAM NATURAL RESOURCES FD INC PEO ALLIANT ENERGY CORP LNT ADAMS DIVERSIFIED EQUITY FUND ADX ALLIANZGI CONV & INC FD NCV ADOBE SYSTEMS INC ADBE ALLIANZGI CONV & INC FD II NCZ ADIENT PLC ADNT* ALLIANZGI EQU & CONV INC FD NIE ADT INC DEL ADT ALLIANZGI NFJ DIVID INT & PREM NFJ ADTALEM -

AK STEEL HOLDING CORPORATION (Exact Name of Registrant As Specified in Its Charter)

Table of Contents SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2004 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. 1-13696 AK STEEL HOLDING CORPORATION (Exact name of registrant as specified in its charter) Delaware 31-1401455 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 703 Curtis Street, Middletown, Ohio 45043 (Address of principal executive offices) (Zip Code) (513) 425-5000 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to filing requirements for the past 90 days. Yes x No ¨ Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Exchange Act). Yes x No ¨ Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. 108,704,401 shares of common stock (as of April 30, 2004) Table of Contents AK STEEL HOLDING CORPORATION INDEX Page PART I. FINANCIAL INFORMATION Item 1. Financial Statements Consolidated Statements of Operations - Three-Month Periods Ended March 31, 2003 and 2004 1 Consolidated Balance Sheets - As of December 31, 2003 and March 31, 2004 2 Condensed Consolidated Statements of Cash Flows - Three-Month Periods Ended March 31, 2003 and 2004 3 Notes to Consolidated Financial Statements 4 Item 2. -

January 5, 2017 U.S. Securities and Exchange Commission 100 F Street

January 5, 2017 U.S. Securities and Exchange Commission 100 F Street NE Washington D.C. 20549 Office of Congressional Ethics U.S. House of Representatives 425 3rd Street SW Washington D.C. 20024 RE: Request for investigation of Reps. Tom Price (R-Ga.) and Chris Collins (R-NY) Dear Commissioners: On behalf of Public Citizen, we request an investigation into the stock market trading activities of Reps. Tom Price (R-Ga.) and Chris Collins (R-NY) for possible violations of insider trading and conflicts of interest laws and regulations. A letter of inquiry is below. Sincerely, Lisa Gilbert Craig Holman, Ph.D. Director Government affairs lobbyist Public Citizen’s Congress Watch division Public Citizen’s Congress Watch division 215 Pennsylvania Avenue SE 215 Pennsylvania Avenue SE Washington, D.C. 20003 Washington, D.C. 20003 (551) 404-5200 (202) 454-5182 January 4, 2017 U.S. Securities and Exchange Commission 100 F Street NE Washington D.C. 20549 Office of Congressional Ethics U.S. House of Representatives 425 3rd Street SW Washington D.C. 20024 Dear Commissioners: Since passage of the STOCK Act in 2012 – which (i) explicitly applied the laws against insider trading to members of Congress and (ii) mandated real-time disclosure of stock trading activity by members of Congress (as well as the President and cabinet officials) – most members of Congress have become more cautious about trading activity that may pose questions of conflicts of interest. There is a greater reluctance by members of Congress to trade in the stock market generally, and in stocks that are directly related to the members’ official duties specifically. -

Ohio Iron and Steel Industry March 2020 TABLE of CONTENTS Page

Advanced Manufacturing: The Ohio Iron and Steel Industry March 2020 TABLE OF CONTENTS Page Executive Summary 1 Description of Ohio’s Iron and Steel Industry - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 3 Notable Iron and Steel Industry Manufacturers 5 Globalization and Foreign Investment in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 8 Recent Expansion and Attraction Announcements 11 Iron and Steel Industry Concentration in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 13 The Composition of Ohio’s Iron and Steel Industry: Employment 15 Industry Pay- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 17 The Distribution of Industry Establishments in Ohio 19 The Distribution of Industry Employment in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 21 Trends 23 Raw Steel Production - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 25 Production as Measured by Value-Added 29 Capital Expenditures- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 31 Establishments 33 Employment- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Of the Securities Exchange Act of 1934

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report(Date of earliest event reported) March 25, 1997 ----------------- AK STEEL HOLDING CORPORATION - ------------------------------------------------------------------ (Exact name of registrant as specified in its charter) DELAWARE File No. 1-13696 31-1401455 - --------------- ----------------------- ------------- (State or other (Commission file number) (IRS employer jurisdiction of identification incorporation) number) 703 Curtis Street, Middletown, Ohio 45043 - ---------------------------------------- --------- (Address of principal executive offices) (Zip code) Registrant's telephone number, including area code: (513) 425-5000 ------------- Not Applicable - ------------------------------------------------------------------ (Former name or former address, if changed since last report) Item 5. Other Events. ------------ Filed herewith are copies of two Press Releases, dated March 19 and March 20, 1997, respectively, issued by AK Steel Holding Corporation (the "Company") to announce they had reached an agreement which resolves the expiration date of the labor agreement covering the company's Ashland, Kentucky USW-represented employees and the Board of Directors announced the election of James L. Wareham as President of the Company, effective March 20, 1997. Item 7. Exhibits. --------- (a) Financial Statements of business acquired: Not applicable. (b) Pro Forma financial information: Not -

SECURITIES and EXCHANGE COMMISSION Washington, D.C

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K Pursuant to Section 13 or 15 (d) of The Securities and Exchange Act or 1934 Date of Report (Date of earliest event reported) July 29, 2002 -------------------------------- AK STEEL HOLDING CORPORATION -------------------------------------------------------------------------------- (Exact name of registrant as specified in its charter) Delaware File No. 1-13696 31-1401455 ------------------ -------------------------- ------------------------- (State or other (Commission file number) (IRS employer jurisdiction of identification incorporation) number) 703 Curtis Street, Middletown, Ohio 45043 ---------------------------------------------- -------------------------- (Address of principal executive offices) (Zip code) Registrant's telephone number, including area code: 513-425-5000 ---------------------------- Not Applicable -------------------------------------------------------------------------------- (Former name or former address, if changed since last report) Item 5. Other Events. ------------ On July 29, 2002, AK Steel Corporation ("AK Steel") announced that Eugene A. Renna has been elected to its board of directors, effective July 22, 2002. Item 7. Exhibit. ------- (a) Financial Statements of business acquired: Not applicable. (b) Pro Forma financial information: Not applicable. (c) Exhibit: 99 Press Release dated July 29, 2002 Signatures Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its -

Creating Innovative Steel Solutions

CREATING INNOVATIVE STEEL SOLUTIONS AKAK Steteel’elel ssn neww ResRReeeseareaara chch andannd InInnovnovvatiationn CenCeC terteter ANNUAL REPORT AND FORM 10-K 2017 2017 AK STEEL ANNUAL REPORT AND FORM 10-K steel solutions provider. productpp capabilitiesp for the manufacturing These solutions leverage our of our stainless products.p All of these broadening portfolio of stainless, projects were completed safely, on electrical, and carbon steels, as budget, and on time. Roger K. Newport well as tubular carbon and stainless Chief Executive Officer steel products.p We also took a Progress in Trade Support transformational step to expand our Duringgg 2017, we continued our fight products and services with the to ensure fair trade in the steel industry strategic acquisition of Precision Partners, in the United States. I joined other steel with their advanced capabilities in industry leaders at the White House as A Message From Roger K. Newport tooling and complex hot- and cold- President Trumpp initiated the Section 232 I am pleased with the great progress stamped components. Investigation, and I testified about the we made in 2017 to strengtheng the Over the pastpy two years, we have unfair globalg trade issues that the steel overall foundation of our company and meaningfullygy enhanced our portfolio p industry faces related to the dumping of drive a longg term, sustainable increase of products,pp production capabilities, p steel into the U.S. in shareholder value. Our performancep and facilities, while at the same time We supported President Trump’s bold was veryyp solid in terms of operational strengthening our capital structure. action in early 2018 to impose global, execution, employee safety, product broad based trade actions, includingg quality, and environmental compliance.