Xerox-Analysis.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

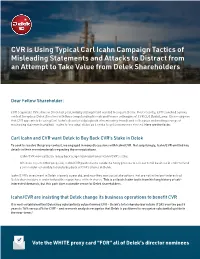

CVR Is Using Typical Carl Icahn Campaign Tactics of Misleading Statements and Attacks to Distract from an Attempt to Take Value from Delek Shareholders

CVR is Using Typical Carl Icahn Campaign Tactics of Misleading Statements and Attacks to Distract from an Attempt to Take Value from Delek Shareholders Dear Fellow Shareholder: CVR acquired a 15% stake in Delek last year, initially stating that it wanted to acquire Delek. Most recently, CVR launched a proxy contest to replace Delek Directors with three longstanding friends and former colleagues of CVR CEO David Lamp. It is no surprise that CVR appears to be using Carl Icahn’s decades old playbook of nominating friends and colleagues and making a range of misleading statements and half-truths to ‘see what sticks’ as it seeks to get its nominees elected. Here are the facts: Carl Icahn and CVR want Delek to Buy Back CVR’s Stake in Delek To seek to resolve this proxy contest, we engaged in many discussions with Icahn/CVR. Not surprisingly, Icahn/CVR omitted key details in their recent materials regarding these negotiations. · Icahn/CVR wanted Delek to buy back a significant portion of Icahn/CVR’s stake. · When we rejected that proposal, Icahn/CVR pushed us to conduct a hasty process to sell our retail business in order to fund a self-tender ostensibly to fund a buyback of CVR’s shares in Delek. Icahn/CVR’s investment in Delek is barely a year old, and now they want us to take actions that are not in the best interests of Delek shareholders in order to fund the repurchase of their shares. This is a classic Icahn tactic from his long history of self- interested demands, but this path does not make sense for Delek shareholders. -

![Filed by the Registrant [ ]](https://docslib.b-cdn.net/cover/4544/filed-by-the-registrant-184544.webp)

Filed by the Registrant [ ]

SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. __) Filed by the Registrant [ ] Filed by a Party other than the Registrant [x] Check the appropriate box: [ ] Preliminary Consent Solicitation Statement [ ] Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) [ ] Definitive Proxy Statement [ ] Definitive Additional Materials [X] Soliciting Material Pursuant to § 240.14a-12 Xerox Corporation (Name of Registrant as Specified In Its Charter) CARL C. ICAHN ICAHN PARTNERS LP ICAHN PARTNERS MASTER FUND LP ICAHN ENTERPRISES G.P. INC. ICAHN ENTERPRISES HOLDINGS L.P. IPH GP LLC ICAHN CAPITAL L.P. ICAHN ONSHORE LP ICAHN OFFSHORE LP BECKTON CORP. HIGH RIVER LIMITED PARTNERSHIP HOPPER INVESTMENTS LLC BARBERRY CORP. JONATHAN CHRISTODORO KEITH COZZA JAFFREY (JAY) A. FIRESTONE RANDOLPH C. READ (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (check the appropriate box): [X] No fee required. [ ] Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. 1) Title of each class of securities to which transaction applies: 2) Aggregate number of securities to which transaction applies: 3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): 4) Proposed maximum aggregate value of transaction: 5) Total fee paid: [ ] Fee paid previously with preliminary materials. [ ] Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. -

Mylan Responds to Carl Icahn's 13D Filing

Mylan Responds to Carl Icahn's 13D Filing PITTSBURGH, Sept. 8 /PRNewswire-FirstCall/ -- Mylan Laboratories Inc. (NYSE: MYL) today stated that Carl Icahn's current opposition to the proposed acquisition of King Pharmaceuticals, Inc. by Mylan does not affect Mylan's commitment to complete the transaction in a timely manner under the agreed terms. In response to Icahn's 13D filing and other public statements, Robert J. Coury, Mylan's Vice Chairman and Chief Executive Officer, stated, "It is unfathomable that Mr. Icahn, a Mylan shareholder for little more than one month, could reasonably conclude what is in the best long-term interest for all Mylan shareholders. Mr. Icahn, to our knowledge, has never owned Mylan shares prior to our announcement to acquire King, nor has he ever met with management to discuss its business, the generics industry, or more recently, the benefits of the King transaction." Mr. Coury added, "Mr. Icahn had already purchased the vast majority of his holdings prior to attempting to contact me by telephone at the end of last week. It was at my suggestion that a face-to-face meeting was arranged for this week." Mr. Coury further stated, "This conduct leads me to believe that Mr. Icahn has an agenda designed to maximize his gains without regard for the long-term interests of all shareholders." Mr. Coury continued, "Over the last few weeks, we've held over 100 institutional investor and major shareholder meetings. Feedback from these meetings has been positive which is reflective, we believe, of a growing appreciation of the compelling logic of the King transaction. -

Who Trump Is Putting in Power by Jessica Huseman, Ian Macdougall and Rob Weychert Updated January 19, 2018

THE CHOSEN H H H Who Trump Is Putting in Power by Jessica Huseman, Ian MacDougall and Rob Weychert Updated January 19, 2018 We’ve created an easy-to-print version of our cards showing President Trump’s key picks. Use them however you like: as con- versation-starting stocking stuffers, with students, or just to test your knowledge of the unfolding administration. Enjoy — and let us know what you do with them! PROPUB.LI/CABINET-CARDS REX TILLERSON SECRETARY OF STATE H Confirmed by the Senate (56–43) REX TILLERSON SECRETARY OF STATE YOUR READING GUIDE H Tillerson is the former CEO of Exxon Mobil. At the State Department, he has overseen a massive downsizing, which resulted in what the New Yorker called “the near-dismantling of America’s diplomatic corps.” He originally supported Jeb Bush for president, and he has had a tumultuous relationship with Trump. He reportedly called the president a “moron” after a July 2017 meeting with other senior officials. For his part, Trump has repeatedly undermined Tillerson, and rumors of Tillerson’s impending departure from Foggy Bottom have dogged him for much of his tenure. PROPUB.LI/CABINET-CARDS STEVE MNUCHIN SECRETARY OF THE TREASURY H Confirmed by the Senate (53–47) STEVE MNUCHIN SECRETARY OF THE TREASURY YOUR READING GUIDE H The former Goldman Sachs banker served as Trump’s campaign finance chairman. Mnuchin was a key booster for the recent tax cut. Reports that he and his wife, Louise Linton (who also generated controversy for comments viewed as tone-deaf), used a government plane to fly to Kentucky to see an eclipse triggered an investigation by Treasury’s Inspector General. -

Ebay Response to Carl Icahn

February 24, 2014 eBay Inc. Responds to Carl Icahn's Feb. 24 Open Letter to Stockholders SAN JOSE, Calif.--(BUSINESS WIRE)-- New eBay shareholder Carl Icahn has cherry-picked old news clips and anecdotes out of context to attack the integrity of two of the most respected, accomplished and value-driven technology leaders in Silicon Valley. Marc Andreessen and Scott Cook bring extraordinary insight, expertise and leadership to eBay's board, which is scrupulous in its governance practices and fully transparent with regard to its directors' other affiliations and businesses. And eBay Inc. President and CEO John Donahoe is widely respected for his turnaround of eBay and leadership of the company over the past six years. As we are sure our other shareholders would agree, we prefer to engage in more constructive and substantive discussions of why, in our view, PayPal and eBay are better together. Instead, Mr. Icahn unfortunately has resorted to mudslinging attacks against two impeccably qualified directors. Mr. Icahn has nominated two of his employees to eBay's board. As we have said, the board's nominating committee will review the nominations of his employees in due course. Even if our board does not support the nominations, ultimately shareholders will decide whether they believe Mr. Icahn's employees are better qualified than directors such as Mr. Cook (Mr. Andreessen is not up for re-election this year) to sit on the board of a leading technology company. The board has been clear in its view that shareholders are best served by keeping PayPal part of eBay. The board regularly assesses all strategic options for the company; should circumstances change the board is entirely capable of evaluating alternatives for optimizing shareholder value. -

FOIA) Document Clearinghouse in the World

This document is made available through the declassification efforts and research of John Greenewald, Jr., creator of: The Black Vault The Black Vault is the largest online Freedom of Information Act (FOIA) document clearinghouse in the world. The research efforts here are responsible for the declassification of hundreds of thousands of pages released by the U.S. Government & Military. Discover the Truth at: http://www.theblackvault.com Received Received Request ID Requester Name Organization Closed Date Final Disposition Request Description Mode Date 17-F-0001 Greenewald, John The Black Vault PAL 10/3/2016 11/4/2016 Granted/Denied in Part I respectfully request a copy of records, electronic or otherwise, of all contracts past and present, that the DOD / OSD / JS has had with the British PR firm Bell Pottinger. Bell Pottinger Private (legally BPP Communications Ltd.; informally Bell Pottinger) is a British multinational public relations and marketing company headquartered in London, United Kingdom. 17-F-0002 Palma, Bethania - PAL 10/3/2016 11/4/2016 Other Reasons - No Records Contracts with Bell Pottinger for information operations and psychological operations. (Date Range for Record Search: From 01/01/2007 To 12/31/2011) 17-F-0003 Greenewald, John The Black Vault Mail 10/3/2016 1/13/2017 Other Reasons - Not a proper FOIA I respectfully request a copy of the Intellipedia category index page for the following category: request for some other reason Nuclear Weapons Glossary 17-F-0004 Jackson, Brian - Mail 10/3/2016 - - I request a copy of any available documents related to Army Intelligence's participation in an FBI counterintelligence source operation beginning in about 1959, per David Wise book, "Cassidy's Run," under the following code names: ZYRKSEEZ SHOCKER I am also interested in obtaining Army Intelligence documents authorizing, as well as policy documents guiding, the use of an Army source in an FBI operation. -

PUBLIC SUBMISSION Posted: November 20, 2020 Tracking No

Page 1 of 2 As of: 11/23/20 10:03 AM Received: November 18, 2020 Status: Posted PUBLIC SUBMISSION Posted: November 20, 2020 Tracking No. 1k4-9k60-8cjw Comments Due: December 03, 2020 Submission Type: Web Docket: PTO-C-2020-0055 Request for Comments on Discretion to Institute Trials Before the Patent Trial and Appeal Board Comment On: PTO-C-2020-0055-0001 Discretion to Institute Trials Before the Patent Trial and Appeal Board Document: PTO-C-2020-0055-0452 Comment from Japan Business Machine and Information System Industries Association Submitter Information Name: Hideaki Chishima Address: Lila Hijirizaka 7FL 3-4-10, Mita Minato-ku, Tokyo, Japan, 1080073 Email: [email protected] Phone: +81-3-6809-5495 Fax: +81-3-3451-1770 Submitter's Representative: Hideki Sanatake Organization: Japan Business Machine and Information System Industries Association General Comment Dear Sir, This post is for Japan Business Machine and Information System Industries Association (JBMIA) to submit its comments in response to solicitation of public comments by USPTO as announced in Federal Register / Docket No. PTO-C-2020-0055. The comments are attached hereto. JBMIA is a Japanese incorporated association which was renamed in 2002 from Japan Business Machine Makers Association established originally in 1960. JBMIA consists of 40 member companies engaged in business machine and information system and 5 supporting companies. Almost all of the member companies have actively filed patent applications in the USA. https://www.fdms.gov/fdms/getcontent?objectId=0900006484967b2a&format=xml&sho... 11/23/2020 Page 2 of 2 Sincerely, Hideaki Chishima (Mr) Intellectual Property Committee Secretariat Attachments JBMIA Comment (finnal) https://www.fdms.gov/fdms/getcontent?objectId=0900006484967b2a&format=xml&sho.. -

Quick Print Station (ASK-300)

Tentative The Best All-in-one System! You can start a photo business easily with this affordable, all-in-one solution. Small Initial Investment Compact Size Variety of Photo Finishing Formats Small Initial Investment Variety of Photo Finishing Formats All-in-one solution at an affordable price. Standard, ID and template The kiosk includes: ready photo formats available. Printer Photo formatting selection is Order terminal easy for everyone, using the Fujifilm software on-screen step-by-step guide. Compact Size & Easy Maintenance High Quality Prints Increase Shop’s Efficiency Outstanding image quality is realized by matching our This compact system is suitable for any retail environment. Image IntelligenceTM processing technology* with Easy loading of paper and replacing of ink ribbons in less than FUJIFILM Quality Thermal Photo Paper. 3 minutes. Adjustable display angle FUJIFILM Dye-sublimation Compact Kiosk System "Quick Print Station" Specifications Display 10.4 inch Touch Panel Display (800 x 600 pixel) OS: Windows XP Embedded (English) PC Unit CPU: Intel Atom N455 (1.6GHz) Memory: DDR3 SO-DIMM (1GB) HDD: 160GB (SATA) 275 mm Wireless LAN: Option Wireless BlueTooth (IEEE 802.15.1) : Option 445 mm Device (LAN port) Option Optical External Device (CD/DVD) Option (USB Connection) 170 mm PC Dimensions (W x D x H) 275 x 295 x 70-275 mm/10.8 x 11.6 x 2.8-10.8 inch (DPC Portable) Weight (approx.) 3.5 kg/7.7 lb Input media SD Memory Card, MicroSD Card, Memory Stick, 275 mm 446 mm Memory Stick Micro, xD-Picture Card, CompactFlash, USB Flash Memory Power Consumption 100-240V AC50/60 Hz Consumables Lineup Interface USB 2.0 x 4 ports (Type A) Print size Description Number of prints per Box Printing speed (approx) Standard Print 3.5 x 5 inch T RL-CF900 900 prints 11.2 seconds/print ID Photo 4 x 6 inch T RK-CF800 800 prints 12.3 seconds/print Frame photo 5 x 7 inch T R2L-CF460 460 prints 19.0 seconds/print Service & Function Edit (Crop, Rotate) 6 x 8 inch T R68-CF400 400 prints · Not include data transfering time. -

Owner's Manual

Owner’s Manual BL00004970-200 EN Introduction Thank you for your purchase of this product. Be sure that you have read this manual and understood its contents be- fore using the camera. Keep the manual where it will be read by all who use the product. For the Latest Information The latest versions of the manuals are available from: http://fujifilm-dsc.com/en/manual/ The site can be accessed not only from your computer but also from smartphones and tablets. It also contains information on the software license. For information on fi rmware updates, visit: http://www.fujifilm.com/support/digital_cameras/software/ ii P Chapter Index Menu List iv 1 Before You Begin 1 2 First Steps 27 3 Basic Photography and Playback 45 4 Movie Recording and Playback 51 5 Taking Photographs 57 6 The Shooting Menus 101 7 Playback and the Playback Menu 159 8 The Setup Menus 185 9 Shortcuts 221 10 Peripherals and Optional Accessories 233 11 Connections 251 12 Technical Notes 265 iii Menu List Camera menu options are listed below. Shooting Menus Menu List Adjust settings when shooting photos or movies. N See page 101 for details. H IMAGE QUALITY SETTING P G AF/MF SETTING P IMAGE SIZE 102 FOCUS AREA 114 IMAGE QUALITY 103 AF MODE 115 RAW RECORDING 103 AF-C CUSTOM SETTINGS 116 FILM SIMULATION 104 STORE AF MODE BY ORIENTATION 119 1⁄3 1⁄3 B & W ADJ. ab(Warm/Cool) 105 AF POINT DISPLAYyz 119 GRAIN EFFECT 105 NUMBER OF FOCUS POINTS 120 COLOR CHROME EFFECT 105 PRE-AF 120 WHITE BALANCE 106 AF ILLUMINATOR 120 DYNAMIC RANGE 108 FACE/EYE DETECTION SETTING 121 D RANGE PRIORITY -

Service Schedule for BT Web Conferencing Service Powered by Microsoft Live Meeting

Service Schedule for BT Web Conferencing Service powered by Microsoft Live Meeting 1. INTERPRETATION “Account” means an identifier that BT gives to the Customer. This identifier is used on all records. “BT Conferencing” means the business unit of BT that provides conferencing services. “Live Meeting” means the web conferencing service provided under this Contract and is the BT Web Conferencing Service powered by Microsoft Office Live Meeting service. “Microsoft” means PlaceWare Inc a wholly owned subsidiary of Microsoft Corporation. “Organiser” means the person whose account the meeting is booked under. “Presenter” means the person presenting the visual information to the audience. “Participant” means a person or persons connected to the Service. “BT Conference Coordinator” means the individual who will assist during the conference. “Minimum Period” means the initial term as stated in the order form. “Third Party Information” means data, information, video, graphics, sound, music, photographs, software and any other materials (in whatever form) not owned or generated by or on behalf of the Customer, published or otherwise made available by the Customer using Live Meeting 2007. Reference in this Contract to a month shall be deemed to mean a calendar month unless the context requires otherwise. Version 1.1 Page 1 of 6 August 2008 BT1006ee 2. SERVICE DESCRIPTION 2.1 Live Meeting Office Live Meeting provides the ability to share a PC desktop with a group of individuals for the purposes of collaborative working and presentations. Live Meeting uses advanced secure sockets layer encryption as standard. Table of included service features Service Features Number of participants Total number of participants that can join 1250* each meeting. -

NOTICE of FISCAL YEAR 2018 (The 55Th FY) ANNUAL GENERAL MEETING of SHAREHOLDERS

㻝㻌 World Headquarters 3-1 Akasaka 5-chome, Minato-ku Tokyo 107-6325, Japan ISIN JP3571400005 Tel:+81-3-5561-7000 SEDOL 6895675 TSE 8035 May 28, 2018 NOTICE OF FISCAL YEAR 2018 (the 55th FY) ANNUAL GENERAL MEETING OF SHAREHOLDERS To Our Shareholders: We are pleased to announce that the 55th Annual General Meeting of Shareholders (the “AGM”) of Tokyo Electron Ltd. (“TEL”) will be held on Tuesday, June 19, 2018, at 10:00 a.m. Japan standard time, at PALACE HOTEL TOKYO, located at 1-1 Marunouchi 1-chome, Chiyoda-ku, Tokyo. Shareholders will also be asked to vote upon the following Agenda: 1: Election of Twelve Corporate Directors 2: Payment of Bonuses to Corporate Directors for the 55th Fiscal Year 3: Issuance of Share Subscription Rights as Stock-Based Compensation to Corporate Directors 4: Issuance of Share Subscription Rights as Stock-Based Compensation to Executives of the Company and its Subsidiaries 5: Introduction of a Stock Compensation System as Medium-term Performance-linked Compensation for Corporate Directors of the Company As part of our ongoing effort to improve the quality of communications with our foreign investors and to increase the participation of those investors and to exercise your voting rights at the AGM, Tokyo Electron Ltd. has appointed IR Japan, Inc. as our Global Information Agent in connection with the shareholder meeting. We realize that many shareholders do not vote at Japanese Shareholders Meeting due to the volume of meetings and timing concerns. Therefore, we attach special importance to your vote, and hope that you will continue to distinguish yourselves from many institutions, who, unfortunately, do not participate. -

PDF Download [1

Annual Report 2002 TOKYO ELECTRON Profile Established in 1963, Tokyo Electron (TEL) is a world-leading supplier of semiconductor production equipment (SPE) and related services for the semiconductor industry. The Company develops, manufactures and markets a broad lineup of products, including oxidation/diffusion/LP-CVD systems, single wafer CVD and PVD systems, coater/developers, spin-on dielectric (SOD) coaters, etch systems, cleaning systems, wafer probers, and others. Tokyo Electron also uses its accumulated expertise in SPE to develop, manufacture and market coater/developers and etch/ash systems for the manufacture of Flat Panel Display (FPD). Most of the Company’s semiconductor and FPD production systems hold the leading share in their respective markets. Tokyo Electron also maintains a strong presence as a distributor, providing a wide array of semiconductor production systems, storage Disclaimer regarding area network and Internet related products for broadband solutions, and Forward-looking Statements electronic components in Japan from other leading suppliers. With a Matters discussed in this annual report, including network spanning 16 countries on three continents, Tokyo Electron forecasts of future business performance of Tokyo Electron, management strategies, beliefs provides superior products and services to its customers, and superior and other statements are based on the returns to its shareholders. Company’s assumption in light of information that is currently available. These forward-looking statements involve known