Traffic Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Redalyc.International Vs. Intra-National Convergence in Europe

Investigaciones Regionales ISSN: 1695-7253 [email protected] Asociación Española de Ciencia Regional España Cornett, Andreas P.; Sørensen, Nils Karl International vs. Intra-national Convergence in Europe - an Assessment of Causes and Evidence Investigaciones Regionales, núm. 13, 2008, pp. 35-56 Asociación Española de Ciencia Regional Madrid, España Available in: http://www.redalyc.org/articulo.oa?id=28901302 How to cite Complete issue Scientific Information System More information about this article Network of Scientific Journals from Latin America, the Caribbean, Spain and Portugal Journal's homepage in redalyc.org Non-profit academic project, developed under the open access initiative 02 CORNETT 11/11/08 15:32 Página 35 © Investigaciones Regionales. 13 – Páginas 35 a 56 Sección ARTÍCULOS International vs. Intra-national Convergence in Europe – an Assessment of Causes and Evidence Andreas P. Cornett* and Nils Karl Sørensen** ABSTRACT: The article aims to explain the different patterns of economic deve- lopment in Europe based on an assessment of regional and national performance with regard to innovation, entrepreneurship and difference in the industrial struc- ture. The central hypothesis of the paper is that large intra-regional disparities do not necessarily lead to lower economic growth on the national level than smaller disparities do. On the contrary, the polarization of economic activities can lead to excess growth in some cases, and contribute to a process of convergence between nations. To address the mechanisms behind this process, the long run patterns of convergence and disparities in regional economic performance with regard to GDP and the distri- bution of employment are analyzed on the regional and the national level for selected European countries. -

Department of Regional Health Research Faculty of Health Sciences - University of Southern Denmark

Department of Regional Health Research Faculty of Health Sciences - University of Southern Denmark The focus of Department of Regional Health Research, Region of Southern Denmark, and Region Zealand is on cooperating to create the best possible conditions for research and education. 1 Successful research environments with open doors With just 11 years of history, Department of Regional Health Research (IRS) is a relatively “The research in IRS is aimed at the treatment new yet, already unconditional success of the person as a whole and at the more experiencing growth in number of employees, publications and co-operations across hospitals, common diseases” professional groups, institutions and national borders. University partner for regional innovations. IRS is based on accomplished hospitals professionals all working towards improving The research in IRS is directed towards the man’s health and creating value for patients, person as a whole and towards the more citizens and the community by means of synergy common diseases. IRS reaches out beyond the and high professional and ethical standards. traditional approach to research and focusses on We largely focus on the good working the interdisciplinary and intersectoral approach. environment, equal rights and job satisfaction IRS makes up the university partner and among our employees. We make sure constantly organisational frame for clinical research and to support the delicate balance between clinical education at hospitals in Region of Southern work, research and teaching. Denmark* and Region Zealand**. Supports research and education Many land registers – great IRS continues working towards strengthening geographical spread research and education and towards bringing the There is a great geographical spread between the department and the researchers closer together hospitals, but research environments and in the future. -

Growth and Ineqaulity in Danish Municipalities

Income Growth and Income Inequality in Danish Municipalities BACHELOR THESIS WITHIN: Economics BACHELOR THESIS NUMBER OF CREDITS: 15 ECTS THESIS WITHIN: Economics PROGRAMME OF STUDY: International Economics and Policy NUMBER OF CREDITS: 15hp AUTHOR: Mattias Lindell PROGRAMME OF STUDY: International Economics and Policy JÖNKÖPING December 2017 AUTHOR: Mattias Lindell SUPERVISOR: Michael Olsson 0 JÖNKÖPING December, 2017 I Bachelor Thesis in Economics Title: Income Growth and Inequality in Danish Municipalities Authors: Mattias Lindell Tutor: Michael Olsson Date: 2018-01-01 Income inequality, Gini coefficient, income growth, regional economics, Denmark Abstract Income growth and income inequality is an important theme in Economic research. It has been debated for decades whether income inequality hinders or enhances income growth. One of the classic models of this relationship was the Kuzenets curve which shows inequality against income per capita can be defined by an inverted U-shaped curve, over a period of time. The purpose of the paper is to see to see the relationship between income growth and inequality on a municipality level. To do this, four econometric panel data models were constructed with data gathered from Statbank Denmark. Log of income was used as the dependent variable and different measures of inequality were used as independent variables among other variables (public expenditure, education, population density, demographic composition, taxation). Results from these models show how income growth is positively related to income inequality, with vastly higher growth at the top end of the income distribution in Denmark. The implications of these findings can show that a trade-off between income inequality and income growth is not true, and it is possible that both variables work in tandem. -

Planning for the German Rail Access Route to the Fehmarn Belt Fixed Link

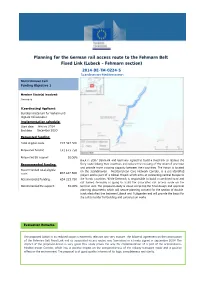

Planning for the German rail access route to the Fehmarn Belt Fixed Link (Lubeck - Fehmarn section) 2014-DE-TM-0224-S Scandinavian-Mediterranean Multi-Annual Call Funding Objective 1 Member State(s) involved: Germany C:\Temp\fichemaps\20150630AfterCorrs\2014-DE-TM-022 (Coordinating) Applicant: Bundesministerium fur Verkehr und digitale Infrastruktur Implementation schedule: Image found and displayed. Start date: January 2014 End date: December 2020 Requested funding: Total eligible costs: €83 347 500 Requested funding: €41 673 750 Requested EU support: 50.00% Back in 2007 Denmark and Germany agreed to build a fixed link to replace the Recommended funding: ferry route linking their countries and reduce the crossing of the strait of one hour and provide more crossing capacity between their countries. The Action is located Recommended total eligible on the Scandinavian - Mediterranean Core Network Corridor, is a pre-identified €68 447 500 costs: project and is part of a Global Project which aims at connecting central Europe to Recommended funding: €34 223 750 the Nordic countries. While Denmark is responsible to build a combined road and rail tunnel, Germany is going to build the associated rail access route on the Recommended EU support: 50.00% German side. The proposed study is about compiling the final design and approval planning documents which will secure planning consent for the section of double- track electrified line between Lübeck and Puttgarden and will provide the basis for the call to tender for building and construction works. Evaluation Remarks The proposed Action in its reduced scope is extremely relevant and very mature. The bilateral agreement on the construction of the Fehmarn Belt Fixed Link and its associated access routes was formalised in a treaty signed in September 2008. -

The Committee of the Regions and the Danish Presidency of the Council of the European Union 01 Editorial by the President of the Committee of the Regions 3

EUROPEAN UNION Committee of the Regions The Committee of the Regions and the Danish Presidency of the Council of the European Union 01 Editorial by the President of the Committee of the Regions 3 02 Editorial by the Danish Minister for European Aff airs 4 03 Why a Committee of the Regions? 6 Building bridges between the local, the regional and 04 the global - Danish Members at work 9 05 Danish Delegation to the Committee of the Regions 12 06 The decentralised Danish authority model 17 EU policy is also domestic policy 07 - Chairmen of Local Government Denmark and Danish Regions 20 08 EU-funded projects in Denmark 22 09 The 5th European Summit of Regions and Cities 26 10 Calendar of events 28 11 Contacts 30 EUROPEAN UNION Committee of the Regions Editorial by the President of 01 the Committee of the Regions Meeting the challenges together We have already had a taste of Danish culture via NOMA, recognised as the best restaurant in the world for two years running by the UK’s Restaurants magazine for putting Nordic cuisine back on the map. Though merely whetting our appetites, this taster has confi rmed Denmark’s infl uential contribution to our continent’s cultural wealth. Happily, Denmark’s contribution to the European Union is far more extensive and will, undoubtedly, be in the spotlight throughout the fi rst half of 2012! A modern state, where European and international sea routes converge, Denmark has frequently drawn on its talents and fl ourishing economy to make its own, distinctive mark. It is in tune with the priorities for 2020: competitiveness, social inclusion and the need for ecologically sustainable change. -

Alternatives for Upgrading the Nykøbing Falster - Puttgarden Railway Line

ALTERNATIVES FOR UPGRADING THE NYKØBING FALSTER - PUTTGARDEN RAILWAY LINE JOANNA PAULINA LAZEWSKA, S150897 Danmarks Tekniske Universitet MASTER THESIS AUGUST 2017 ALTERNATIVES FOR UPGRADING THE NYKØBING FALSTER - PUTTGARDEN RAILWAY LINE MAIN REPORT AUTHOR JOANNA PAULINA LAZEWSKA, S150897 MASTER THESIS 30 ETCS POINTS SUPERVISORS STEVEN HARROD, DTU MANAGEMENT ENGINEERING HENRIK SYLVAN, DTU MANAGEMENT ENGINEERING RUSSEL DA SILVA, ATKINS Alternatives for upgrading the Nykøbing F — Puttgarden railway line Joanna Paulina Lazewska, s150897, August 14th 2017 Preface This project constitutes the Master’s Thesis of Joanna Lazewska, s150897. The project is conducted at the Department of Management Engineering of the Technical University of Denmark in the spring semester 2017. The project accounts for 30 ECTS points. The official supervisors for the project have been Head of Center of DTU Management Engineering Henrik Sylvan, Senior Adviser at Atkins Russel da Silva, and Associate Professor at DTU Steven Harrod. I would like to extend my gratitude to Russel da Silva for providing skillful guidance through the completion of project. Furthermore, I would like to thank Henrik Silvan and Steven Harrod for, in addition to guidance, also providing the project with their broad knowledge about economic and operational aspects of railway. In addition, I would like to thank every one who has contributed with material, consultations and guidance in the completion of this project, especially Rail Net Denmark that provided materials and plans, as well as guidance at the technical aspects of the project. A special thank is given to Atkins, which has provided office facilities, computer software, and railway specialists’ help throughout the project. It would not be possible to realize project without their help. -

Danish Kriegers Flak Update

Danish Kriegers Flak Update The Danish Energy Agency issued the Construction Licence for Danish Kriegers Flak on the 3rd February 2020 Photo: Global Marine Group/Osbit. Construction work to start at the bottom in 2020 First up in 2020 is preparing the Kriegers Flak seabed to accept the cables. Global Marine Group is using the newly developed Subsea Pre-Lay Plough, which enables boulder clearance and pre- trenching up to 1,7m in a single run and backfilling of the trenches. The plough has been developed in collaboration with technology company Osbit. Kriegers Flak is well under way Photo: Nordhagen Kommunikation. Kriegers Flak Project Director Ian Bremner. By Ian Bremner Construction works on the DKF project are currently scheduled to begin in February 2020. A key part of the preparations for this phase is the manufacture of the main component parts which is in full swing. To be more specific, by November 2019 the project had completed the manufacture of the monopiles at EEW in Rostock, which are part of the foundation structure, pending coating works. The second component part of the foundation structure, the transition piece, is being manufactured in Aalborg by Bladt Industries. Completion of the first transition piece is scheduled for February 2020, with all works scheduled for completion next summer. The cables required to connect the turbines have just begun to be manufactured by JDR Cable Systems, and they are also scheduled for completion in the summer of 2020. Of course, these component parts must be installed, and this leads to our installation schedule. First up will be Global Marine, mobilising in February 2020 to prepare the seabed to accept the cables. -

555 the Regime of Passage Through the Danish Straits Alex G. Oude

The Regime of Passage Through the Danish Straits Alex G. Oude Elferink* Netherlands Institute for the Law of the Sea, Utrecht University, The Netherlands ABSTRACT The Danish Straits are the main connection between the Baltic Sea and the world oceans. The regime of passage through these straits has been the subject of extensiveregulation, raising the question how different applicable instruments interact. Apart from applicable bilateral and multilateral treaties, it is necessaryto take into account the practice of Denmark and Swedenand other interested states, and regulatory activities within the framework of the IMO. The Case ConcerningPassage Through the Great Belt before the ICJ provides insights into the views of Denmark and Finland. The article concludesthat an 1857treaty excludesthe applicabilityof Part III of the LOS Convention to the straits, and that there are a number of difficultiesin assessingthe contents of the regimeof the straits. At the same time, these uncertaintiesdo not seem to have been a complicatingfactor for the adoption of measuresto regulate shipping traffic. Introduction The Danish Straits are the main connection between the Baltic Sea and the world oceans. The straits are of vital importance for the maritime communication of the Baltic states and squarely fall within the legal category of straits used for international navigation For a number of these states the Baltic Sea is the only outlet to the oceans (Estonia, Finland, Latvia, Lithuania and Poland). Although * An earlier version of this article was presented at the international conference, The Passage of Ships Through Straits, sponsored by the Defense Analyses Institute, Athens, 23 October 1999. The author wishes to thank the speakers and participants at that conference for the stimulating discussions, which assisted in preparing the final version of the article. -

Die Küste, Heft 74, 2008

Die Küste, 74 ICCE (2008), 379-389 379 The Ports of Schleswig-Holstein Hubs of maritime economy between North and Baltic Sea and Continental Europe By GESAMTVERBAND SCHLESWIG-HOLSTEINISCHER HÄFEN C o n t e n t s 1. Introduction . 379 2. Selected Ports as Examples for the Current Situation and Development . 380 2.1 Lübeck – Germany’s largest Baltic Port . 380 2.2 Port Operating Company Brunsbüttel/Harbour Group Brunsbüttel and Glückstadt . 382 2.3 Rendsburg District Harbour . 383 2.4 Flensburg . 384 2.5 Seaport Kiel – Logistics Hub and Germany’s most important Cruise Terminal . 385 2.6 Puttgarden . 387 3. References . 389 1. I n t r o d u c t i o n The range of Schleswig-Holstein ports is manifold: High performance installations for handling large numbers of passengers, bulk and mixed cargo, as well as of Ro-Ro freight are available in the major sea ports. A consolidated network of regular ferry and freight lines provide continuous service to the Northern European States, as well as to Russia and the Baltic States. Destination and source areas of the products handled in these ports extend from the German industrial centres far into mid-, western- and southern European Sates. Nu- merous regionally important harbours open the waterways for Schleswig-Holstein’s trades and industry, afford unobstructed traffic to the islands and create an essential basis for local fisheries. Schleswig-Holstein’s ports along the Lower Elbe between Hamburg and the North Sea are partly located on junctions of the Elbe and the Kiel Canal. Due to their location, the ports of Brunsbüttel, Glückstadt and Wedel, are ideal partners for Metropolitan Hamburg in managing its streams of goods and traffic by water, rail and road. -

352 INDE X 000 Map Pages 000 Photograph Pages

© Lonely Planet Publications 352 Index Andersen, Martin 190 Bellevue beach 113 DANISH ALPHABET Anemonen 178 Charlottenlund 88 Note that the Danish letters Æ, animals 59, see also individual animals Dueodde 189 Ø and Å fall in this order at the Græsholm 197 Ebeltoft 272 end of the alphabet. Skandinavisk Dyrepark 274 Gilleleje beaches 128 Staffordshire china spaniels 226 Grenaa 273 animal parks, see zoos & animal parks Hornbæk Beach 126 A Anne Hvides Gård 216-17 Jutland’s best 309 Aa Kirke 187 Ant chair 231 Karrebæksminde 152 Aalborg 294-300, 296 Apostelhuset 151 Klintholm Havn 172 Aalborg Carnival 297 Aqua 276 Køge 140 Aalborg history museums 295 aquariums Marielyst 176 Aalborg Zoo 297 Aqua 276 Melsted 192 Aalholm Automobil Museum 180 Danmarks Akvarium 113 Moesgård Strand 260 Aalholm Slot 180 Fiskeri- og Søfartsmuseet 234 Ristinge 222 accommodation 314-17 Fjord & Bælt 210 Tisvildeleje beach 129 language 338 Kattegatcentret 273 Tornby Strand 309 activities 8-9, 62-8, 317, see also Nordsømuseet 309 Ulvshale Strand 169 individual activities Aquasyd Dykker & Vandsportscenter 176 bed & breakfasts 316 adventure-holiday spots 278 architecture 158-9 beer 49-50, 245 air pollution 61 Aalborg houses 295 Carlsberg Visitors Center 88 air travel 326-8 Anne Hvides Gård 216-17 microbreweries 7 INDEX airports 326 Kommandørgården 244 Ølfestival 22 tickets 326 Kubeflex 231 Bellevue beach 113 to/from Denmark 326 Nordjyllands Kunstmuseum 297 Besættelsesmuseet 262 within Denmark 331 Rudkøbing 220-1 bicycling, see cycling Allinge 195-6 Arken Museum Of Modern -

OHDSI in Denmark

A journey unfolded by Iannis Drakos, PhD Chief consultant in precision medicine Operations, Research & Innovation (PFI) Region of Zealand, Denmark OHDSI in Denmark from Ithaca to bedside OHDSI in Denmark: from Ithaca to bedside Iannis Drakos – [email protected] OHDSI in Denmark: from Ithaca to bedside 2 Iannis Drakos, PhD*1, Piotr J. Chmura, MSc*3,4, Rasmus C. Jørgensen, MSc1,6, Nicolas Derian, PhD1, Rune B. Hasselager MD2, Rasmus Peuliche Vogelsang MD2, Tina Fransgård, MD2, Sara K. Watt, MD2, Christina Ellervik, MD, PhD1,4,9, Palle L. Pedersen, PhD6, Stig E. Andersen, MD, PhD4,5, Benjamin S. Kaas- Hansen, MD, MSc3,4, Kirstine G. Belling, PhD3,4, Erling Samdahl, MSc1, Anders Rasmussen, MSc1, Karen Søeby, MD, PhD7, Anna Ostropolets, MD10, Maria Pozhidaeva10, Pavel Grafkin10, Peter R. Rijnbeek, PhD8, Anne Bernth, MSc1, Søren Brunak, MD, PhD3,4, Jesper Grarup, DVM**1, Ismail Gögenur MD,PhD**2,4 1. Operations, Research and Innovation, Region Zealand, Denmark 2. Center for Surgical Science, Zealand University Hospital, Denmark 3. Novo Nordisk Foundation Center for Protein Research, Copenhagen, Denmark 4. University of Copenhagen, Copenhagen, Denmark 5. Clinical Pharmacology, Zealand University Hospital, Denmark 6. Region Zealand Biobank, Zealand, Denmark 7. Biochemistry, Zealand University Hospital, Denmark 8. Erasmus University Medical Center, Rotterdam, Netherlands 9. Harvard Medical School, Boston, USA 10. Odysseus Data Services, Cambridge, Massachusetts, USA OHDSI in Denmark: from Ithaca to bedside Iannis Drakos – [email protected] The Danish health data scene 3 Personal Identification Number Nationwide since 1968 (used to be regional) National Electronic Health Record Health data produced at any healthcare level and source is digitally stored and available both to the citizen and the treating MD. -

NY DK Og UK Grants 2016.Xlsx

VILLUM FONDEN Technical and Scientific Research Project title Organisation Department Applicant Amount Breaking Barriers in Scattering Amplitudes: Understanding via Computation (and vice versa) University of Copenhagen Niels Bohr Institute Jacob Bourjaily kr. 7.390.515 Search for heavy Higgs particles in diboson decays at LHC run II University of Copenhagen Niels Bohr Institute Troels Christian Petersen kr. 2.075.000 The Villum Kann Rasmussen Annual Award 2017 University of Copenhagen Niels Bohr Institute Jens Hjorth kr. 4.500.000 The Villum Kann Rasmussen Annual Award 2017 - personal stake University of Copenhagen Niels Bohr Institute Jens Hjorth kr. 500.000 Crossroads for inflation theory: Uncovering the origins of the Universe University of Southern Denmark Department of Physics, Chemistry and Pharmacy Martin S. Sloth kr. 2.901.780 Analyses of sub-mesoscale frontiers as essential barriers of dispersion for phytoplancton University of Copenhagen Natural History Museum of Denmark Katherine Richardson Christensen kr. 3.432.727 miGENEPI: Evaluation of effects of new selected pressurizers on GENomers EPIgenomes an MIkrobiota University of Copenhagen Natural History Museum of Denmark Ludovic Orlando kr. 5.995.927 Dispersal, differentiation and speciation across barriers and along elevational gradients in island bird communities University of Copenhagen Natural History Museum of Denmark Knud Jønsson kr. 9.999.971 HiddenRisk - Understanding the impact of human activities on subterranean biodiversity University of Copenhagen Natural History Museum of Denmark Ana Sofia Reboleira kr. 7.075.471 Molecular mechanisms behind recognition of extraneous RNa in plants - and connected effects on antiviral immunity University of Copenhagen Department of Biology Peter Brodersen kr. 5.878.520 Novel Molecular Targets for Beetle Pest Control - From Genome to Phenome University of Copenhagen Department of Biology Kenneth Halberg kr.