2014 Annual REPORT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Geology Map of Newfoundland

LEGEND POST-ORDOVICIAN OVERLAP SEQUENCES POST-ORDOVICIAN INTRUSIVE ROCKS Carboniferous (Viséan to Westphalian) Mesozoic Fluviatile and lacustrine, siliciclastic and minor carbonate rocks; intercalated marine, Gabbro and diabase siliciclastic, carbonate and evaporitic rocks; minor coal beds and mafic volcanic flows Devonian and Carboniferous Devonian and Carboniferous (Tournaisian) Granite and high silica granite (sensu stricto), and other granitoid intrusions Fluviatile and lacustrine sandstone, shale, conglomerate and minor carbonate rocks that are posttectonic relative to mid-Paleozoic orogenies Fluviatile and lacustrine, siliciclastic and carbonate rocks; subaerial, bimodal Silurian and Devonian volcanic rocks; may include some Late Silurian rocks Gabbro and diorite intrusions, including minor ultramafic phases Silurian and Devonian Posttectonic gabbro-syenite-granite-peralkaline granite suites and minor PRINCIPAL Shallow marine sandstone, conglomerate, limey shale and thin-bedded limestone unseparated volcanic rocks (northwest of Red Indian Line); granitoid suites, varying from pretectonic to syntectonic, relative to mid-Paleozoic orogenies (southeast of TECTONIC DIVISIONS Silurian Red Indian Line) TACONIAN Bimodal to mainly felsic subaerial volcanic rocks; includes unseparated ALLOCHTHON sedimentary rocks of mainly fluviatile and lacustrine facies GANDER ZONE Stratified rocks Shallow marine and non-marine siliciclastic sedimentary rocks, including Cambrian(?) and Ordovician 0 150 sandstone, shale and conglomerate Quartzite, psammite, -

(PL-557) for NPA 879 to Overlay NPA

Number: PL- 557 Date: 20 January 2021 From: Canadian Numbering Administrator (CNA) Subject: NPA 879 to Overlay NPA 709 (Newfoundland & Labrador, Canada) Related Previous Planning Letters: PL-503, PL-514, PL-521 _____________________________________________________________________ This Planning Letter supersedes all previous Planning Letters related to NPA Relief Planning for NPA 709 (Newfoundland and Labrador, Canada). In Telecom Decision CRTC 2021-13, dated 18 January 2021, Indefinite deferral of relief for area code 709 in Newfoundland and Labrador, the Canadian Radio-television and Telecommunications Commission (CRTC) approved an NPA 709 Relief Planning Committee’s report which recommended the indefinite deferral of implementation of overlay area code 879 to provide relief to area code 709 until it re-enters the relief planning window. Accordingly, the relief date of 20 May 2022, which was identified in Planning Letter 521, has been postponed indefinitely. The relief method (Distributed Overlay) and new area code 879 will be implemented when relief is required. Background Information: In Telecom Decision CRTC 2017-35, dated 2 February 2017, the Canadian Radio-television and Telecommunications Commission (CRTC) directed that relief for Newfoundland and Labrador area code 709 be provided through a Distributed Overlay using new area code 879. The new area code 879 has been assigned by the North American Numbering Plan Administrator (NANPA) and will be implemented as a Distributed Overlay over the geographic area of the province of Newfoundland and Labrador currently served by the 709 area code. The area code 709 consists of 211 Exchange Areas serving the province of Newfoundland and Labrador which includes the major communities of Corner Brook, Gander, Grand Falls, Happy Valley – Goose Bay, Labrador City – Wabush, Marystown and St. -

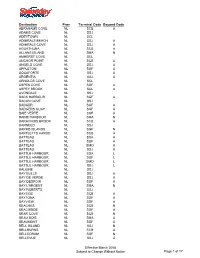

ROUTING GUIDE - Less Than Truckload

ROUTING GUIDE - Less Than Truckload Updated December 17, 2019 Serviced Out Of City Prov Routing City Carrier Name ABRAHAMS COVE NL TORONTO, ON Interline Point ADAMS COVE NL TORONTO, ON Interline Point ADEYTON NL TORONTO, ON Interline Point ADMIRALS BEACH NL TORONTO, ON Interline Point ADMIRALS COVE NL TORONTO, ON Interline Point ALLANS ISLAND NL TORONTO, ON Interline Point AMHERST COVE NL TORONTO, ON Interline Point ANCHOR POINT NL TORONTO, ON Interline Point ANGELS COVE NL TORONTO, ON Interline Point APPLETON NL TORONTO, ON Interline Point AQUAFORTE NL TORONTO, ON Interline Point ARGENTIA NL TORONTO, ON Interline Point ARNOLDS COVE NL TORONTO, ON Interline Point ASPEN COVE NL TORONTO, ON Interline Point ASPEY BROOK NL TORONTO, ON Interline Point AVONDALE NL TORONTO, ON Interline Point BACK COVE NL TORONTO, ON Interline Point BACK HARBOUR NL TORONTO, ON Interline Point BACON COVE NL TORONTO, ON Interline Point BADGER NL TORONTO, ON Interline Point BADGERS QUAY NL TORONTO, ON Interline Point BAIE VERTE NL TORONTO, ON Interline Point BAINE HARBOUR NL TORONTO, ON Interline Point BAKERS BROOK NL TORONTO, ON Interline Point BARACHOIS BROOK NL TORONTO, ON Interline Point BARENEED NL TORONTO, ON Interline Point BARR'D HARBOUR NL TORONTO, ON Interline Point BARR'D ISLANDS NL TORONTO, ON Interline Point BARTLETTS HARBOUR NL TORONTO, ON Interline Point BAULINE NL TORONTO, ON Interline Point BAULINE EAST NL TORONTO, ON Interline Point BAY BULLS NL TORONTO, ON Interline Point BAY DE VERDE NL TORONTO, ON Interline Point BAY L'ARGENT NL TORONTO, ON -

HYDROGEOLOGY 50°0' Central Newfoundland

55°15' 55°0' 54°45' 54°30' 54°15' 54°0' 53°45' 53°30' 53°15' 50°15' Department of Environment and Conservation Department of Natural Resources Map No. 3b HYDROGEOLOGY 50°0' Central Newfoundland Well Yield Well Depth 50°0' Characteristics Characteristics (m) Number (L/min) Hydrostratigraphic Unit Lithology of Wells Average Median Average Median Unit 1 schist, gneiss, Low to Moderate Yield 73 20 6 51 48 quartzite, slate Metamorphic Strata siltstone, Unit 2 conglomerate, argillite, Low to Moderate Yield 1403 20 7 51 46 greywacke, with Sedimentary Strata minor volcanic 49°45' flows and tuff Unit 3 basic pillow Low to Moderate Yield lava, flows, 723 22 9 50 46 Barr'D Islands Volcanic Strata breccia and tuff 49°45' Fogo Joe Batt's Arm Tilting Unit 4 mafic and ultramafic Shoal Bay Pike's Arm Low Yield intrusions of ophiolite 13 9 7 58 61 Herring Neck Change Islands complexes FogoC oIsolkasn Pdond Ophiolite Complexes Durrell Deep Bay Fogo Island Region Unit 5 granite, granodiorite, Salt Harbour N o r t h Twillingate Island Harbour diabase, and diorite 688 22 9 44 37 Little Harbour Cobbs Arm A t l a n t i c Low to Moderate Yield Too Good Arm Seldom intrusions Notre Dame Bay O c e a n Plutonic Strata Gilliards Cove F Jenkins Cove rid Keattyle Cove Black Duck Cove Little Seldom Tizzard's Harbour B Rogers Cove ay Indian Cove Surficial deposits - Unconsolidated sediments Stag Harbour Newville Valley Pond Moreton's Harbour Surficial Hydrostratigraphic Units Fairbanks-Hillgrade Unit A - Till Deposits Hillgrade Port Albert Well yields range from 2 litres per minute (L/min) to 136 L/min and averaged 29 L/min Bridgeport 49°30' Virgin Arm-Carter's Cove with a median value of 18 L/min. -

Surficial Sediments and Post-Glacial Relative Sea-Level History, Hamilton Sound, Newfoundland

An.ANTIC GEOLOGY 97 Surficial sediments and post-glacial relative sea-level history, Hamilton Sound, Newfoundland J. Shaw and K.A. Edwardson Geological Survey of Canada, Atlantic Geoscience Centre, Bedford Institute of Oceanography, PO. Box 1006, Dartmouth, Nova Scotia B2Y 4A2, Canada Date Received September 28, 1993 Date Accepted April 4, 1994 Hamilton Sound is a shallow, wave-exposed cmbaymcnt on the northeast coast of Newfoundland. Four scismostratigraphic units are recognised: (1) bedrock (acoustic basement); (2) a unit with incoherent reflections, interpreted as Late Wisconsinan glacial diamicton or till, which in places forms small drumlins; (3) a thin, acoustically stratified, draped unit found in the deepest parts of the eastern sound, interpreted as glacimarinc gravelly mud; and (4) an uppermost unit with an acoustically stratified, ponded facies, and a facies which can be acoustically incoherent. Unit 4 consists of sandy mud, muddy sand, sand and gravel, and results from reworking of units 2 and 3. Three types of seabed occur: (1) bedrock; (2) bouldery gravel or gravel, sub-angular to rounded, which overlies, and is derived from, glacial diamicton of acoustic unit 2. The coralline alga Lithothamnion sp. coats some clasts on their upper surfaces and some clasts completely. This, together with the occurrence of gravel ripples in several areas, is evidence of intermittent sediment mobility; and (3) gravelly sand, sand, muddy sand, or sandy mud, located in basins. Seabed features in this zone include dunes, iceberg furrows and pits. The regional relative sca level curve is constrained by two types of morphological evidence: rounded drumlin crests at depths below 19 m which would have been truncated if sea level had fallen below -18.5 m, and (wave-cut) terraces at depths of 17 to 21 m. -

22 Enrolment Information Education Statistics - Elementary-Secondary, 2002-03 Table 13

Table 13. Enrolment by Grade1 and School by School District, 2002-03 District 6 - Lewisporte/Gander 4th School Name Comm unity K 1 2 3 4 5 6 7 8 9 10 11 12 Total Yr 2 Greenwood Academy Campbellton 14 19 19 30 27 16 35 32 28 28 0 0 0 0 248 Carmanville School Complex Carmanville 9 13 15 24 24 22 16 30 27 25 26 18 18 6 273 Centreville Academy Centreville-Wareham 7 12 8 12 16 15 18 22 22 0 0 0 0 0 132 A. R. Scammell Academy Change Islands 2 4 1 2 4 2 6 5 3 1 4 8 4 0 46 Charlottetown Elem entary Charlottetown, B.B. 3 6 1 5 1 3 0 0 0 0 0 0 0 0 19 William Mercer Academy Dover 23 15 16 21 15 22 28 25 23 0 0 0 0 0 188 Holy Cross School Complex Eastport 5 3 10 9 16 9 19 20 18 13 29 13 17 1 182 Fogo Island Central Academy Fogo Island 26 22 17 36 31 21 33 39 37 45 49 47 53 15 471 Smallwood Academy Gambo 23 27 25 21 33 33 33 30 30 30 30 30 31 6 382 Gander Academy Gander 108 120 102 113 108 120 132 0 0 0 0 0 0 0 803 Gander Collegiate Gander 0 0 0 0 0 0 0 0 0 0 109 121 127 29 386 St. Paul's Intermediate School Gander 0 0 0 0 0 0 0 146 131 135 0 0 0 0 412 Lakewood Academy Glenwood 11 16 15 14 13 18 15 20 12 20 24 13 24 0 215 Glovertown Academy Glovertown 22 28 28 23 32 33 34 41 37 34 54 44 42 7 459 Heritage Academy Greenspond 4 5 4 5 8 3 5 0 0 0 0 0 0 0 34 Jane Collins Academy Hare Bay 0 0 0 0 0 0 0 0 0 55 52 57 38 2 204 Sandstone Academy Ladle Cove 4 4 2 6 2 5 4 0 0 0 0 0 0 0 27 Lewisporte Academy Lew isporte 44 53 53 46 49 0 0 0 0 0 0 0 0 0 245 Lew isporte Collegiate Lew isporte 0 0 0 0 0 0 0 0 0 0 143 134 103 13 393 Lewisporte Middle School Lew isporte 0 0 0 0 0 59 53 67 63 58 0 0 0 0 300 Lumsden School Complex Lumsden 8 9 11 9 13 6 12 14 24 12 14 16 16 1 165 Gill Memorial Academy Musgrave Harbour 18 6 9 8 16 11 17 16 19 11 15 19 14 0 179 Newville Elem entary Newville 8 13 12 12 8 7 7 17 19 0 0 0 0 0 103 Hillview Academy Norris Arm 9 14 6 9 12 15 11 10 20 16 0 0 0 0 122 St. -

Community Files in the Centre for Newfoundland Studies

Community Files in the Centre for Newfoundland Studies A | B | C | D | E | F | G | H | I | J | K | L | M | N | 0 | P | Q-R | S | T | U-V | W | X-Y-Z A Abraham's Cove Adams Cove, Conception Bay Adeytown, Trinity Bay Admiral's Beach Admiral's Cove see Port Kirwan Aguathuna Alexander Bay Allan’s Island Amherst Cove Anchor Point Anderson’s Cove Angel's Cove Antelope Tickle, Labrador Appleton Aquaforte Argentia Arnold's Cove Aspen, Random Island Aspen Cove, Notre Dame Bay Aspey Brook, Random Island Atlantic Provinces Avalon Peninsula Avalon Wilderness Reserve see Wilderness Areas - Avalon Wilderness Reserve Avondale B (top) Baccalieu see V.F. Wilderness Areas - Baccalieu Island Bacon Cove Badger Badger's Quay Baie Verte Baie Verte Peninsula Baine Harbour Bar Haven Barachois Brook Bareneed Barr'd Harbour, Northern Peninsula Barr'd Islands Barrow Harbour Bartlett's Harbour Barton, Trinity Bay Battle Harbour Bauline Bauline East (Southern Shore) Bay Bulls Bay d'Espoir Bay de Verde Bay de Verde Peninsula Bay du Nord see V.F. Wilderness Areas Bay L'Argent Bay of Exploits Bay of Islands Bay Roberts Bay St. George Bayside see Twillingate Baytona The Beaches Beachside Beau Bois Beaumont, Long Island Beaumont Hamel, France Beaver Cove, Gander Bay Beckford, St. Mary's Bay Beer Cove, Great Northern Peninsula Bell Island (to end of 1989) (1990-1995) (1996-1999) (2000-2009) (2010- ) Bellburn's Belle Isle Belleoram Bellevue Benoit's Cove Benoit’s Siding Benton Bett’s Cove, Notre Dame Bay Bide Arm Big Barasway (Cape Shore) Big Barasway (near Burgeo) see -

Department of Health and Community Services Ambulance Listing

Department of Health and Community Services Ambulance Listing There are three categories of ambulance services in the province: Hospital Based Ambulance Services - 12 Public Utilities Board Licenses Private Ambulance Services – 27 Public Utilities Board Licenses Community Ambulance Services – 22 Public Utilities Board Licenses Hospital Bases Ambulance Services Funded through the RHAs budgets Paramedics are RHA staff The RHA ambulances services are positioned as follows: St. John’s Metro – Minimum of 5 ambulances staffed to a maximum of 10 ambulances staffed during peak periods. Carbonear – One ambulance Gander – Two ambulances – One 24/7 and one call in Twillingate – One ambulance Grand Falls –Winsor - Two ambulances - One 24/7 and one call in Buchans – One ambulance Springdale – One ambulance Baie Verte – One ambulance Corner Brook – One ambulance (Note – Shared Emergency response with a private operator) Port Saunders – Two ambulances Flower’s Cove – One ambulance Roddickton – One ambulance St. Anthony – Two ambulances North West River – One ambulance Labrador City – One ambulance Private Ambulance Services Funded through Service Agreements signed with HCS and the appropriate RHA (tri- partite) For profit service delivery Two associations and four independent operators: o NL Association of Ambulance Services o NL Ambulance Operator Association o Moore’s, Delaney, MacKenzie and Tryco Ambulance Services Refer to the attached tables for position Community Ambulance Services Funded through Service Agreements signed with HCS and the appropriate RHA (tri- partite) For not for profit service delivery Types of Funded Ambulances (Refer to the tables starting on the next page) Primary ambulances (P1 and P2) – 24/7 emergency response. 4.5 FTEs per ambulances. -

ARCHIVES and SPECIAL COLLECTIONS QUEEN ELIZABETH II LIBRARY MEMORIAL UNIVERSITY, ST

ARCHIVES and SPECIAL COLLECTIONS QUEEN ELIZABETH II LIBRARY MEMORIAL UNIVERSITY, ST. JOHN'S, NL Graham Snow collection COLL-088 Website: Archives and Special Collections Author: Roberta Thomas Date: 1987 Scope and Content: In October 1985, Graham Snow arranged to have his papers donated to the Archives and Special Collections, and they were received in June of 1987. The collection consists mainly of research data for an authoritative work on the history of organized sport in Newfoundland, which he had been working on for a number of years. The material is in the form of photocopies from newspaper articles and histories, original news clippings and official reports.The preliminary manuscript and handwritten notes for the history are also included. The data covers all facets of sports development in the province, both in St. John's and outlying areas.The arrangement of the papers follows the chapter outline of the proposed history fairly closely and would be of some value to Newfoundland sports historians. Custodial History: Graham S. Snow, St. John's, Nfld., 1985. Gift. Restrictions: There are no restrictions on access. Copyright laws and regulations may apply to all or to parts of this collection. All patrons should be aware that copyright regulations state that any copy of archival material is to be used solely for the purpose of research or private study. Any use of the copy for any other purpose may require the authorization of the copyright owner. It is the patron's responsibility to obtain such authorization. Biography or History: Graham Snow was born in Carmanville in 1928. -

Convention Bulletin 2019 from the NL Teachers' Association

NEWFOUNDLAND AND LABRADOR TEACHERS’ ASSOCIATION Convention 2019 Derrick Baker Maureen Derek Drover Kyran Dwyer Doyle-Gillingham Craig Hicks Jamie Jenkins Kelly Loch Tracey Payne Gabriel Ryan Joseph Santos Colin Short Sean Weir Chesley West CONVENTION NOTES Biennial General Meeting 2019 he major decision-making forum of the Newfoundland and communities and populations – including working with; Congolese TLabrador Teachers’ Association, Convention 2019, will take and Burundian refugees, young Tanzanians living with HIV/AIDS, to place April 23-26 at the Sheraton Hotel Newfoundland in St. John’s. Indigenous Inuit living in the Canadian Arctic. She brings a community Approximately 93 delegates from Branches and Special Interest development approach to her teaching styles and cares deeply about Councils will attend the meeting to consider resolutions put forth removing gendered barriers in the class, to exploring how education by Branches and Councils, resolutions from the floor of Convention, can be used to “de-colonize”. She loves movement and using physical the 2019-21 budget, by-law changes, and other important business activity as a tool to engage with youth. Ms. MacDonnell is currently an which must be carried out by the Association throughout the year. Education Consultant with the School Board of Nunavik. One of the highlights of the Biennial General Meeting will be the elections for the Provincial Executive of the Association. Candidates Editor’s Note: Candidates’ biographies and position statements are printed as sub- for Provincial Executive are indicated throughout this issue of The mitted and have been edited for length/word count only. Bulletin. Other highlights of the BGM include presentation of the Special Recognition Award, the Bancroft and Barnes Awards, the Patricia Cowan Award, the President’s Award, and the conferring of Honorary Membership in the Association. -

Destination Prov Terminal Code Beyond Code ABRAHAMS COVE

Destination Prov Terminal Code Beyond Code ABRAHAMS COVE NL SCB A ADAMS COVE NL SSJ ADEYTOWN NL SCL ADMIRALS BEACH NL SSJ A ADMIRALS COVE NL SSJ A AGUATHUNA NL SCB A ALLANS ISLAND NL SMA N AMHERST COVE NL SCL ANCHOR POINT NL SCB A ANGELS COVE NL SSJ A APPLETON NL SGF A AQUAFORTE NL SSJ A ARGENTIA NL SSJ A ARNOLDS COVE NL SCL ASPEN COVE NL SGF A ASPEY BROOK NL SCL A AVONDALE NL SSJ BACK HARBOUR NL SGF A BACON COVE NL SSJ BADGER NL SGF A BADGERS QUAY NL SGF A BAIE VERTE NL SGF A BAINE HARBOUR NL SMA N BARACHOIS BROOK NL SCB A BARNEED NL SSJ BARRD ISLANDS NL SGF N BARTLETTS HARBO NL SCB A BATTEAU NL SDA A BATTEAU NL SGF A BATTEAU NL SMO A BATTEAU NL SSJ A BATTLE HARBOUR NL SDA L BATTLE HARBOUR NL SGF L BATTLE HARBOUR NL SMO L BATTLE HARBOUR NL SSJ L BAULINE NL SSJ BAY BULLS NL SSJ A BAY DE VERDE NL SSJ A BAY DESPOIR NL SGF A BAY L'ARGENT NL SMA N BAY ROBERTS NL SSJ BAYSIDE NL SCB A BAYTONA NL SGF A BAYVIEW NL SGF A BEACHES NL SCB N BEACHSIDE NL SGF A BEAR COVE NL SCB N BEAU BOIS NL SMA A BEAUMONT NL SGF A BELL ISLAND NL SSJ N BELLBURNS NL SCB A BELLEORAM NL SGF N BELLEVUE NL SSJ A Effective March 2008 Subject to Change Without Notice Page 1 of 17 Destination Prov Terminal Code Beyond Code BELLMANS COVE NL SCB A BENOITS COVE NL SCB A BENTON NL SGF A BIDE ARM NL SCB N BIG BROOK NL SAN N BIRCHY BAY NL SGF A BIRCHY COVE BB NL SCL BIRCHY HEAD NL SCB N BIRD COVE NL SCB A BISCAY BAY NL SSJ BISHOPS COVE NL SSJ BISHOPS FALLS NL SGF BLACK DUCK NL SCB A BLACK DUCK COVE NL SCB A BLACK DUCK SIDI NL SCB A BLACK TICKLE NL SDA L BLACK TICKLE NL SGF L BLACK -

CLPNNL By-Laws

COLLEGE BY-LAWS Table of Contents PART I: TITLE AND DEFINITIONS . 2 PART II: COLLEGE ADMINISTRATION . 3 PART III: COLLEGE BOARD AND STAFF. 5 PART IV: ELECTION(S). 8 PART V: MEETINGS . 11 PART VI: BOARD COMMITTEES . 14 PART VII: FEES/LICENSING. 15 PART VIII: GENERAL. 16 Appendix A: Electoral Zones. 17 Appendix B: Nomination Form . 29 1 PART I: TITLE AND DEFINITIONS By-laws Relating to the Activities of the College of Licensed Practical Nurses of Newfoundland and Labrador References in this document to the Act , Regulations and By-laws refer to the Licensed Practical Nurses Act (2005) ; the Licensed Practical Nurses Regulations (2011) and the By-laws incorporated herein, made under the Licensed Practical Nurses Act, 2005 . 1. Title These By-laws may be cited as the C ollege of Licensed Practical Nurses of Newfoundland and Labrador By-laws . 2. Defi nitions In these Bylaws , “act” means the Licensed Practical Nurses Act, 2005 ; “appointed Board member” means a member of the Board appointed under section 4 of the Act ; “Board” means the Board of the College of Licensed Practical Nurses of Newfoundland and Labrador as referred to in section 3 of the Act ; “Chairperson” means the chairperson of the Board elected under Section 3(8) of the Act ; “College” means the College of Licensed Practical Nurses of Newfoundland and Labrador as established by section 3 of the Act ; “elected Board member” means a member of the Board elected under section 3 of the Act ; “committee member” means a member of a committee appointed by the Board; “Registrar” means the Registrar of the College of Licensed Practical Nurses of Newfoundland and Labrador; “Licensee” means a member of the College who is licensed under section 12 of the Act ; “Licensed Practical Nurse (LPN)” means a practical nurse licensed under the Act ; and “Regulation” means a Regulation passed pursuant to the Act , as amended.