Depositors Disciplining Banks: the Impact of Scandals 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Randall S. Kroszner, Elizabeth A. Duke, and Larry A

S. HRG. 110–928 NOMINATIONS OF: RANDALL S. KROSZNER, ELIZABETH A. DUKE, AND LARRY A. KLANE HEARING BEFORE THE COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS UNITED STATES SENATE ONE HUNDRED TENTH CONGRESS FIRST SESSION ON NOMINATIONS OF: RANDALL S. KROSZNER, OF NEW JERSEY, TO BE A MEMBER OF THE BOARD OF GOVERNORS, FEDERAL RESERVE SYSTEM ELIZABETH A. DUKE, OF VIRGINIA, TO BE A MEMBER OF THE BOARD OF GOVERNORS, FEDERAL RESERVE SYSTEM LARRY A. KLANE, OF THE DISTRICT OF COLUMBIA, TO BE A MEMBER OF THE BOARD OF GOVERNORS, FEDERAL RESERVE SYSTEM THURSDAY, AUGUST 2, 2007 Printed for the use of the Committee on Banking, Housing, and Urban Affairs ( Available at: http://www.access.gpo.gov/congress/senate/senate05sh.html U.S. GOVERNMENT PRINTING OFFICE 50–354 WASHINGTON : 2009 For sale by the Superintendent of Documents, U.S. Government Printing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Nov 24 2008 08:23 Jan 12, 2010 Jkt 050354 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 E:\HR\OC\D354.XXX D354 WReier-Aviles on DSKGBLS3C1PROD with HEARING COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS CHRISTOPHER J. DODD, Connecticut, Chairman TIM JOHNSON, South Dakota RICHARD C. SHELBY, Alabama JACK REED, Rhode Island ROBERT F. BENNETT, Utah CHARLES E. SCHUMER, New York WAYNE ALLARD, Colorado EVAN BAYH, Indiana MICHAEL B. ENZI, Wyoming THOMAS R. CARPER, Delaware CHUCK HAGEL, Nebraska ROBERT MENENDEZ, New Jersey JIM BUNNING, Kentucky DANIEL K. AKAKA, Hawaii MIKE CRAPO, Idaho SHERROD BROWN, Ohio JOHN E. -

Resolution Plan 2018 Public Section

RESOLUTION PLAN 2018 PUBLIC SECTION TABLE OF CONTENTS Page INTRODUCTION ......................................................................................................................... 1 1. Names of Material Entities .................................................................................... 3 2. Description of Core Business Lines ....................................................................... 3 3. Summary Financial Information Regarding Assets, Liabilities, Capital, and Major Funding Sources. .................................................................................. 4 4. Description of Derivatives and Hedging Activities ............................................... 7 5. Memberships in Material Payment, Clearing, and Settlement Systems ................ 7 6. Description of Foreign Operations......................................................................... 8 7. Identities of Material Supervisory Authorities ...................................................... 8 8. Identities of Principal Officers ............................................................................... 9 9. Corporate Governance Structure and Processes Related to Resolution Planning ............................................................................................................... 10 10. Material Management Information Systems ........................................................ 11 11. High Level Description of Resolution Strategy ................................................... 12 -i- INTRODUCTION Section -

Wells Fargo International Equity Fund

QUARTERLY MUTUAL FUND COMMENTARY Q4 2020 | All information is as of 12/31/2020 unless otherwise indicated. Wells Fargo International Equity Fund Quarterly review GENERAL FUND INFORMATION ● The International Equity Fund underperformed the MSCI ACWI ex USA Index (Net) Ticker: WFENX and the MSCI ACWI ex USA Value Index (Net) for the quarter that ended December 31, 2020. Portfolio managers: Dale A. Winner, ● Performance was driven largely by stock selection, with positive contributions coming CFA®; and Venk Lal from investments in the industrials and materials sectors as well as in China/Hong Subadvisor: Wells Capital Kong and Canada. Management Inc. ● Positions in information technology (IT) and health care as well as in France and Japan Category: Foreign large value detracted from performance. Market review FUND STRATEGY ● Maintains a core equity style that International equity markets initially declined in October before advancing 19.6% in the emphasizes bottom-up stock final two months of the year as multiple COVID-19 vaccines reached 90%+ efficacy and selection based on rigorous, uncertainty surrounding the U.S. presidential election receded, resulting in a 17.0% in-depth, fundamental company return for the MSCI All Country World ex USA Index (Net) in the fourth quarter, the research highest quarterly return since the third quarter of 2009. In this environment, the Global ● Uses a bottom-up research process Purchasing Managers’ Index (PMI) reached 53.3 in October, the highest level since that targets companies with August 2018, but fell back to 52.7 in December, still in expansionary territory. Emerging underestimated earnings growth markets outperformed developed markets and sovereign yields saw mixed fluctuations potential or those trading at during the period, including the U.S. -

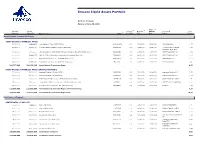

Invesco Liquid Assets Portfolio

Invesco Liquid Assets Portfolio Portfolio Holdings Data as of June 30, 2021 4 2 3 Final Principal Market 1 Coupon/ Maturity Maturity Associated % of Amount Value ($) Name of Issue CUSIP Yield (%) Date Date Issuer Portfolio Asset Backed Commercial Paper ASSET-BACKED COMMERCIAL PAPER 25,000,000 24,998,958 Ionic Capital III Trust (CEP-UBS AG) 46220WUG9 0.13 07/16/2021 07/16/2021 UBS GROUP AG 1.27 37,777,000 37,774,140 Lexington Parker Capital Company (Multi-CEP) 52953AUV5 0.15 07/29/2021 07/29/2021 Lexington Parker Capital 1.93 Company (Multi-CEP) 10,500,000 10,500,000 LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QXR6 0.05 10/25/2021 10/25/2021 CREDIT AGRICOLE SA 0.54 40,000,000 39,992,272 LMA SA (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QW30 0.24 09/03/2021 09/03/2021 CREDIT AGRICOLE SA 2.04 20,000,000 20,000,000 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JW26 0.14 09/02/2021 09/02/2021 BNP PARIBAS SA 1.02 55,000,000 54,964,250 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JY81 0.14 11/08/2021 11/08/2021 BNP PARIBAS SA 2.80 188,277,000 188,229,620 Asset-Backed Commercial Paper 9.60 ASSET-BACKED COMMERCIAL PAPER (INTEREST BEARING) 50,000,000 50,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VG1 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 2.55 25,000,000 25,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VL0 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 1.27 10,000,000 10,000,000 Bedford Row Funding Corp. -

Uncorrected Transcript

1 CEA-2016/02/11 THE BROOKINGS INSTITUTION FALK AUDITORIUM THE COUNCIL OF ECONOMIC ADVISERS: 70 YEARS OF ADVISING THE PRESIDENT Washington, D.C. Thursday, February 11, 2016 PARTICIPANTS: Welcome: DAVID WESSEL Director, The Hutchins Center on Monetary and Fiscal Policy; Senior Fellow, Economic Studies The Brookings Institution JASON FURMAN Chairman The White House Council of Economic Advisers Opening Remarks: ROGER PORTER IBM Professor of Business and Government, Mossavar-Rahmani Center for Business and Government, The John F. Kennedy School of Government at Harvard University Panel 1: The CEA in Moments of Crisis: DAVID WESSEL, Moderator Director, The Hutchins Center on Monetary and Fiscal Policy; Senior Fellow, Economic Studies The Brookings Institution ALAN GREENSPAN President, Greenspan Associates, LLC, Former CEA Chairman (Ford: 1974-77) AUSTAN GOOLSBEE Robert P. Gwinn Professor of Economics, The Booth School of Business at the University of Chicago, Former CEA Chairman (Obama: 2010-11) PARTICIPANTS (CONT’D): GLENN HUBBARD Dean & Russell L. Carson Professor of Finance and Economics, Columbia Business School Former CEA Chairman (GWB: 2001-03) ALAN KRUEGER Bendheim Professor of Economics and Public Affairs, Princeton University, Former CEA Chairman (Obama: 2011-13) ANDERSON COURT REPORTING 706 Duke Street, Suite 100 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 2 CEA-2016/02/11 Panel 2: The CEA and Policymaking: RUTH MARCUS, Moderator Columnist, The Washington Post KATHARINE ABRAHAM Director, Maryland Center for Economics and Policy, Professor, Survey Methodology & Economics, The University of Maryland; Former CEA Member (Obama: 2011-13) MARTIN BAILY Senior Fellow and Bernard L. Schwartz Chair in Economic Policy Development, The Brookings Institution; Former CEA Chairman (Clinton: 1999-2001) MARTIN FELDSTEIN George F. -

The Evolution of the Financial Services Industry and Its Impact on U.S

THOUGHT LEADERSHIP SERIES THE EVOLUTION OF THE FINANCIAL SERVICES INDUSTRY AND ITS IMPACT ON U.S. OFFICE SPACE June 2017 TABLE OF CONTENTS OVERVIEW OF U.S. FINANCIAL SERVICES INDUSTRY I PAGE: 4 OVERVIEW OF OFFICE MARKET CONDITIONS IN 11 MAJOR FINANCIAL CENTERS PAGE: 8 A. ATLANTA, GA PAGE: 8 B. BOSTON, MA PAGE: 10 C. CHARLOTTE, NC PAGE: 12 D. CHICAGO, IL PAGE: 14 E. DALLAS-FORT WORTH, TX II PAGE: 16 F. DENVER, CO PAGE: 18 G. MANHATTAN, NY PAGE: 20 H. ORANGE COUNTY, CA PAGE: 22 I. SAN FRANCISCO, CA PAGE: 24 J. WASHINGTON, DC PAGE: 26 K. WILMINGTON, DE PAGE: 28 MARKET SUMMARY AND ACTION STEPS III PAGE: 30 KEY FINDINGS The financial services sector has adapted its office-space usage in ways that are consistent with many office-using industries. However, its relationship to real estate has changed as a result of its role within the broader economy. In particular, four major causes have spurred a reduction in gross leasing activity by financial services firms: increased government regulation following the Great Recession of 2007-2009, cost reduction, efficient space utilization, and the emergence of the financial technology (fintech) sector. While demand for office space among financial services tenants has edged down recently overall, industry demand is inconsistent among major metros. For example, leasing increased for financial services tenants in San Francisco from 10% of all leasing activity in 2015 to 20% in 2016, while leasing among tenants in New York City declined from 32% to 20% over the same time period. Leasing trends within the financial services industry correlate with: the types of institutions involved, environments with policies and incentives that are conducive to doing business, the scale of operations and access to a highly-skilled talent pool, a shift from some urban to suburban locations, and a desire for new construction. -

Quarterly Report DNB Bank ASA 3Q19

DNB Bank A company in the DNB Group Third quarter report 2019 (Unaudited) Q3 Financial highlights Income statement DNB Bank Group 3rd quarter 3rd quarter January-September Full year Amounts in NOK million 2019 2018 2019 2018 2018 Net interest income 10 150 9 299 29 367 27 634 37 388 Net commissions and fees 1 536 1 431 4 799 4 721 6 605 Net gains on financial instruments at fair value 1 523 611 3 622 905 1 351 Other operating income 612 581 1 839 1 939 2 522 Net other operating income 3 672 2 623 10 260 7 564 10 478 Total income 13 822 11 922 39 627 35 198 47 866 Operating expenses (5 318) (5 114) (16 108) (15 189) (20 681) Restructuring costs and non-recurring effects (134) (26) (177) (106) (565) Pre-tax operating profit before impairment 8 370 6 782 23 343 19 902 26 620 Net gains on fixed and intangible assets (40) (3) (43) 480 529 Impairment of financial instruments (1 247) (11) (2 014) 374 139 Pre-tax operating profit 7 083 6 769 21 286 20 756 27 288 Tax expense (1 417) (1 354) (4 257) (4 151) (4 976) Profit from operations held for sale, after taxes (36) (42) (117) (63) (204) Profit for the period 5 631 5 373 16 912 16 542 22 109 Balance sheet 30 Sept. 31 Dec. 30 Sept. Amounts in NOK million 2019 2018 2018 Total assets 2 576 850 2 307 710 2 387 216 Loans to customers 1 673 924 1 598 017 1 561 867 Deposits from customers 983 472 940 087 995 154 Total equity 215 989 207 933 200 665 Average total assets 2 543 839 2 434 354 2 454 510 Key figures and alternative performance measures 3rd quarter 3rd quarter January-September Full year 2019 -

Randall Kroszner

Randall S Kroszner | The University of Chicago Booth School of Business NEWS CAMPUSES INTRANET GIVE APPLY NOW FACULTYABOUT US PROGRAMS FACULTY& RESEARCH & RESEARCH ALUMNI RECRUITERS & COMPANIES Search Print Bio ADDITIONAL Faculty Directory » INFORMATION Faculty Photo Curriculum Vitae » Directory » RANDALL S. Unrestricted Teaching Materials » Emeriti Faculty KROSZNER Directory » Norman R. Bobins Professor of Economics Capital Ideas SELECTED Research and Learning Phone : 1-773-702-8779 ARTICLES Centers » IS IT BETTER TO FORGIVE THAN Capital Ideas » Email : [email protected] RECEIVE? History Lessons Guide Policy Choices Selected Papers Personal Website Series » Address : 5807 South Woodlawn Avenue Chicago, IL 60637 CHECKS AND BALANCES The Economics of Corporate Journals » Governance Reform Research Workshops » TO HAVE AND TO HOLD Faculty Openings » The Big Question Randall S. Kroszner served as a Governor of the Federal Reserve System from 2006 until 2009. WATCH VIDEO He chaired the committee on Supervision and Regulation of Banking Institutions and the committee on Consumer and Community Affairs. In these capacities, he took a leading role in developing responses to the financial crisis and in undertaking new initiatives to improve SHARE THIS PAGE consumer protection and disclosure, including rules related to home mortgages and credit cards. HOW CAN He represented the Federal Reserve Board on the Financial Stability Forum (now called the THE US CUT Financial Stability Board), the Basel Committee on Banking Supervision, and the Central Bank ITS DEFICIT? Governors of the American Continent and was a director of NeighborWorks America. Dr. Kroszner chaired the working party of the Organization for Economic Cooperation and Development (OECD), composed of deputy central bank governors and finance ministers, on Policies for the Promotion of Better International Payments Equilibrium. -

The Judges 2017 FT & Mckinsey Business Book of the Year Award

By continuing to use this site you consent to the use of cookies on your device as described in our cookie policy unless you have disabled them. You can change your cookie settings at any time but parts of our site will not function correctly without them. Business books The judges 2017 Lionel Barber, FT editor, chairs our panel of experts FT & McKinsey Business Book of the Year Award YESTERDAY LIONEL BARBER Editor, Financial Times Lionel Barber is the editor of the Financial Times. Since his appointment in 2005, Barber has helped solidify the FT’s position as one of the first publishers to successfully transform itself into a multichannel news organisation. During Barber’s tenure, the FT has won numerous global prizes for its journalism, including Newspaper of the Year, Overseas Press Club, Gerald Loeb and Society of Publishers in Asia awards. Barber has co-written several books and has lectured widely on foreign policy, transatlantic relations, European security and monetary union in the US and Europe and appears regularly on TV and radio around the world. As editor, he has interviewed many of the world’s leaders in business and politics, including: US President Barack Obama, Chancellor Angela Merkel of Germany and President of Iran Hassan Rouhani. Barber has received several distinguished awards, including the St George Society medal of honour for his contribution to journalism in the transatlantic community. He serves on the Board of Trustees at the Tate and the Carnegie Corporation of New York. MITCHELL BAKER Executive chairwoman, Mozilla Mitchell Baker co-founded the Mozilla Project to support the open, innovative web and ensure it continues offering opportunities for everyone. -

Davis Global Fund

DGF ANNUAL REVIEW 2021 Davis Global Fund Update from Portfolio Manager Danton Goei The Equity Specialists DGF | ANNUAL REVIEW [ 1 ] Davis Global Fund Annual Review 2021 Please provide an update on the long-term We also learned that while the novel virus was performance and more recent results for Davis highly transmissible, exacerbated by asymptomatic Global Fund. Discuss the current positioning: carriers, the mortality rate was lower than initially feared. As overwhelmed hospitals recovered, record For the year 2020, Davis Global Fund returned high unemployment levels fell, and the Federal 23.06%, compared with a 16.25% return for Reserve further eased monetary policy, equity the MSCI ACWI (All Country World Index), an markets recovered, looking ahead to the end of outperformance of 6.81%. In the first half of 2020, Davis Global Fund returned −4.87%, though it still the pandemic. outperformed the index by 1.38%. This weak market The beginning of the end was on November 9, environment in the first half was followed by a very when Pfizer and its partner, German biotech firm strong rebound in the second half, when the Fund returned 29.36% for the six months, compared to BioNTech, announced the results of their Phase 3 the market return of 24.01%. interim analysis, showing vaccine efficacy of over 90%. This stunning level of efficacy, achieved in less In the first half of 2020, the rapid spread of than 10 months after the genetic sequence of the the COVID-19 pandemic led to a wide range of novel virus was first shared globally on January 11, reasonable disaster scenario forecasts, given the was astounding. -

Wells Fargo VT International Equity Fund

Annual Report December 31, 2020 Wells Fargo VT International Equity Fund Contents Letter to shareholders............................................................................2 Performance highlights..........................................................................6 Fund expenses .......................................................................................10 Portfolio of investments ........................................................................11 Financial statements Statement of assets and liabilities............................................................ 14 Statement of operations.........................................................................15 Reduce clutter. Statement of changes in net assets .........................................................16 Financial highlights ................................................................................. 17 Save trees. Sign up for Notes to financial statements.................................................................19 electronic delivery Report of independent registered public accounting firm.........................26 of prospectuses and shareholder Other information..................................................................................27 reports at wellsfargo.com/ advantagedelivery The views expressed and any forward-looking statements are as of December 31, 2020, unless otherwise noted, and are those of the Fund's portfolio managers and/or Wells Fargo Asset Management. Discussions of individual securities or the markets -

The EEA the Norwegian Banking Sector, The

Case No: 77452 Document No: 1046871 Decision No: 022119/COL EFTA SURVEILLANCE AUTHORITY DECISION of 2 April2019 closing proceedings initiated against Finans Norge, Bits, BankID Norge, DNB and Nordea pursuant to Article 53 of the EEA Agreement (Case No 77452 - e-Payment services in Norway) THE EFTA SURVEILLANCE AUTHORITY, HAVING REGARD to the Agreement on the European Economic Area ("the EEA Agreement"), and in particular Article 55 thereof, HAVING REGARD to the EFTA Surveillance Authority's ("the Authority'') Decision No l95ll6lCOL of 25 October 2016 to initiate proceedings against Finans Norge, Bits AS, BankID Norge AS, DNB Bank ASA, DNB ASA, NordeaBank AB (publ) and Nordea Bank Norge ASA, WHEREAS: l. In October 2075, the Authority received a complaint from the Trustly Group AB ("Trustly''), a provider of electronic payment ("e-payment") services established in Sweden, regarding an alleged coordinated blocking of its ability to provide its e- payment services in Norway by several members of the Norwegian banking sector.l 2. Following a preliminary review of documents collected from the relevant members of the Norwegian banking sector, the Authority decided that there was sufficient information to initiate proceedings,2 pursuant to Article 2(1) of Chapter III of Protocol 4 to the Agreement between the EFTA States on the Establishment of a Surveillance Authority and a Court of Justice ("SCA"), and require an in-depth investigation in respect ofl Finans Norge and its related organisation Bits AS; I The complaint was initially addressed to the Norwegian Competition Authority in April 2015. Pursuant to the rules governing cooperation between the EFTA Surveillance Authority and the national competition authorities of the EFTA States, the case was allocated to the Authority in October 2015: see Chapter III of Protocol 4 to the SCA and the EFTA Surveillance Authority Notice on cooperation within the EFTA Network ofCompetitionAuthorities (OJC 227,21.9.2006,p.