Forecast-Eversource

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Calculating SMART Incentives for New Residential Solar Photovoltaic Arrays

FACT SHEET Calculating SMART Incentives for New Residential Solar Photovoltaic Arrays This is one of a series of fact sheets designed to help Massachusetts residents incorporate energy efficiency and renewable energy into their day-to-day lives. For more information, visit the UMass Clean Energy Extension (CEE) website, https://ag.umass.edu/clean-energy. Solar photovoltaic (PV) panels can generate renewable electricity for your home, while providing you with significant energy cost savings. This fact sheet provides a guide to calculating incentives available for residential solar PV systems through the Solar Massachusetts Renewable Target (SMART) program. For general information on purchasing a residential-scale solar PV array for your property, see Considering a Solar Photovoltaic Array for Your Home on our website. SMART Program Incentives for Small Systems The Solar Massachusetts Renewable Target (SMART) program is a new program which will regulate incentives associated with production of electricity from new solar PV facilities in Massachusetts. The program is expected to begin in late 2018, once the Department of Public Utilities (DPU) has reviewed and approved the regulation, which has already been finalized by the Massachusetts Department of Energy Resources (MA DOER). Under the SMART program, residents and businesses can qualify to receive incentives for solar PV installations in the form of what are known as “tariffs,” which are credits that appear on the electricity bill of the system owner. For small residential PV systems (≤ 25 kW in capacity), the program provides a fixed credit for every kilowatt-hour (kWh) of electricity that is generated by the system for a period of 10 years. -

Electricity Delivery Superseding Nhpuc No

NHPUC NO. 10 – ELECTRICITY DELIVERY SUPERSEDING NHPUC NO. 9 – ELECTRICITY DELIVERY NHPUC NO. 10 – ELECTRICITY DELIVERY PUBLIC SERVICE COMPANY OF NEW HAMPSHIRE DBA EVERSOURCE ENERGY TARIFF FOR ELECTRIC DELIVERY SERVICE in Various towns and cities in New Hampshire, served in whole or in part. (For detailed description, see Service Area) Issued: December 23, 2020 Issued by: /s/ Joseph A. Purington Joseph A. Purington Effective: January 1, 2021 Title: President, NH Electric Operations NHPUC NO. 10 - ELECTRICITY DELIVERY Original Page 1 PUBLIC SERVICE COMPANY OF NEW HAMPSHIRE DBA EVERSOURCE ENERGY TABLE OF CONTENTS Page TERMS AND CONDITIONS FOR DELIVERY SERVICE 1. Service Area .............................................................................................................. 5 2. Definitions.................................................................................................................. 7 3. General ....................................................................................................................... 9 4. Availability ................................................................................................................ 10 5. Application, Contract and Commencement of Service.............................................. 10 6. Selection of Supplier or Self-Supply Service by a Customer .................................... 11 7. Termination of Supplier Service or Self-Supply Service .......................................... 12 8. Unauthorized Switching of Suppliers ....................................................................... -

Welcome to Eversource

Welcome to Eversource Dear Customer, Three years ago Northeast Utilities and its operating companies, Connecticut Light & Power, Public Service of New Hampshire, Western Massachusetts Electric, and Yankee Gas merged with NSTAR Electric & Gas to better serve New England. We’ve spent every day working to build one company united around a mission of delivering reliable energy and superior customer service. Today, we’ve reached an important milestone in this three-year journey as we come together as Eversource. Our more than 8,000 employees are very proud of our history and our future as New England’s energy provider. It’s more than a new name on our vehicles, website, and facilities. It’s about the value we place on always improving on our commitment to bringing you reliable energy and superior customer service. Over the next few months you’ll be hearing more about our commitment to our customers and New England, and how energy brings us together. Sincerely, Thomas J. May Chairman, President & Chief Executive Officer Eversource Energy Handy Facts for Your Reference Eversource.com is our newly designed website that’s easy to navigate and replaces our former websites. You’ll be able to continue to: • Pay your bill with your existing login information. • Get information about your account. • Report outages and receive outage information. • Learn about ways to save energy and money, and get financial assistance. You’ll notice at Eversource.com you’ll be asked for your ZIP code to provide you with the best possible information related to your account. If you have bookmarked or visited one of our former • If you pay your bill by check, you can make it websites, visiting the link will take you to Eversource.com. -

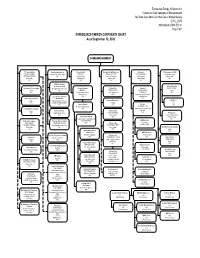

Eversource Corporate Chart As of 2020.06.02 Eversource Gas-MA.Opx

Eversource Energy, NiSource Inc. Eversource Gas Company of Massachusetts Bay State Gas d/b/a Columbia Gas of Massachusetts D.P.U. 20-59 Attachment LIUNA-ES-1-1 Page 1 of 1 EVERSOURCE ENERGY CORPORATE CHART As of September 12, 2020 EVERSOURCE ENERGY The Connecticut Light Yankee Energy System, Inc. Eversource Water Eversource Energy Transmission Eversource NU Enterprises, Inc. (NUEI) and Power Company Gas Businesses Holding Company Ventures, Inc. Ventures, Inc. (EE-TV) Holdco Corporation Unregulated Businesses (dba Eversource Energy) 100% Water Businesses Transmission Businesses Wind Businesses Holding Company Electric Utility Holding Company Holding Company Holding Company 100% 100% 100% 100% 100% NSTAR Gas Company (dba Eversource Energy) Northeast Generation The Connecticut Steam Company Retail Distribution of Natural Gas Eversource Aquarion Northern Pass Eversource Services Company Inactive 100% Holdings, Inc. Transmission LLC Investment Service Inactive 100% Aquarion Water Businesses Electric Transmission Company LLC 100% Holding Company 100% Construction of Onshore Facilities Eversource Gas Company of 100% for Bay State Wind Electric Power Incorporated Massachusetts 100% Inactive Acquisition Subsidiary for Assets of Renewable Properties, Inc. NGS Sub, Inc. 100% Columbia Gas of Massachusetts Real Estate Inactive 100% Aquarion Company 100% Eversource 100% Intermediate Holding Company Investment LLC (EI) The Nutmeg Power Company 100% Holds Eversource Investment in Bay State Wind Inactive Hopkinton LNG Corp. Eversource LNG 100% 100% Liquid -

EDITED TRANSCRIPT ES.N - Q1 2021 Eversource Energy Earnings Call

REFINITIV STREETEVENTS EDITED TRANSCRIPT ES.N - Q1 2021 Eversource Energy Earnings Call EVENT DATE/TIME: MAY 10, 2021 / 1:00PM GMT OVERVIEW: Co. reported 1Q21 EPS of $1.06. Expects 2021 EPS towards lower end of $3.81-3.93 range, including $0.07 per share impacts of credits. REFINITIV STREETEVENTS | www.refinitiv.com | Contact Us ©2021 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. 'Refinitiv' and the Refinitiv logo are registered trademarks of Refinitiv and its affiliated companies. MAY 10, 2021 / 1:00PM, ES.N - Q1 2021 Eversource Energy Earnings Call CORPORATE PARTICIPANTS Jeffrey R. Kotkin Eversource Energy - VP of IR Joseph R. Nolan Eversource Energy - President, CEO & Trustee Philip J. Lembo Eversource Energy - Executive VP & CFO CONFERENCE CALL PARTICIPANTS Angie Storozynski Seaport Global Securities LLC, Research Division - Research Analyst David Arcaro Morgan Stanley, Research Division - Research Associate Durgesh Chopra Evercore ISI Institutional Equities, Research Division - Associate Insoo Kim Goldman Sachs Group, Inc., Research Division - Equity Analyst Jeremy Tonet JP Morgan Chase & Co, Research Division - Senior Analyst Julien Dumoulin-Smith BofA Securities, Research Division - Director and Head of the US Power, Utilities & Alternative Energy Equity Research Michael Weinstein Crédit Suisse AG, Research Division - United States Utilities Analyst Paul Patterson Glenrock Associates LLC - Analyst Sophie Karp KeyBanc Capital Markets Inc., Research Division - Director and Senior Analyst of Electric Utilities & Power Steven Fleishman Wolfe Research, LLC - MD & Senior Analyst Travis Miller Morningstar Inc., Research Division - Director of Utilities Research and Strategist PRESENTATION Operator Good morning, and welcome to the Eversource Energy First Quarter 2021 Results Conference Call. -

Program Materials for Connected Solutions for Commercial / Industrial Customers

Program Materials for Connected Solutions for Commercial / Industrial Customers Contents Summary ........................................................................................................................................................................................... 2 Enrollment through a CSP and Direct Participation .......................................................................................................................... 2 Shared Savings .................................................................................................................................................................................. 3 Annual Payment Process .................................................................................................................................................................. 3 Number of Events ............................................................................................................................................................................. 3 Targeted Dispatch ........................................................................................................................................................................ 3 Daily Dispatch Demonstration ..................................................................................................................................................... 4 Winter Dispatch .......................................................................................................................................................................... -

Christopher Paul Soderman, P.E.*

NSTAR Electric Company d/b/a Eversource Energy EFSB 14-04AID.P.U. 14-153A/14-154A 1110112018 EV-CS-1 Page 1 of 3 Work (860) 728-6 172 Email: christopher.soderman@cvc•·source.com Christopher Paul Soderman, P.E.* Education: Rensselaer Polytechnic Institute (Troy, NY) Bachelor of Science in Mechanical Engineering Worcester Polytechnic Institute (Worcester, MA) Master of Science in Electrical Engineering University of Hartford (West Hartford, CT) Master of Engineering (Civil Engineering) University of Hartford (West Hartford, CT) Master of Business Administration Special Skills: Team Leader-ship: I can lead and develop technical teams including development of indoctrination into new processes and technical capabilities. This includes aJmual performance reviews, special coaching, classroom style lectures and more. Cr-itical Ana lytical T hinking: I am constantly on the hunt fo r new ways of doing things, trying to challenge how things are done and drive more efficiencies and better accuracy. This includes development of new standards that allow for quick and easy design work that is understandable and production savvy. Exper-t Testimony: I can and have provided expert testimony on behalf of Eversource. This includes expertise in Transmission Line Engineering, Construction and Electric and Magnetic Fields. Relevant Work Experience: 2/2018-Present Eversource Ene r·gy Service Company Manager - Transmission Line & Civil Engineel'ing CT & WMA: Manage a department of engineers and designers providing engineering support for the design of new transmi -

Advancing Smart Energy Homes and Buildings in the Northeast

SMART ENERGY HOMES AND BUILDINGS Evolving Homes and Buildings to Keep Up with the Evolving Grid August 27, 2020 Building Decarbonization 3 Key Elements Advanced Electric Deep Energy Grid Technologies Efficiency Integration Space/Water Thermal Flexible use of Heating – Heat Pumps Improvements Low-Carbon Electricity Northeast Strategic Electrification Action Plan – NEEP 2018 1 Allies Network State Partners Connecticut New York State Partners: CT DEEP, CT Energy Efficiency Board, Eversource State Partners: NYSERDA Energy, United Illuminating Company, Southern Connecticut Gas and Connecticut Natural Gas Partners in 2017/2018/2019/2020 Partners in 2017/2018/2019/2020 Rhode Island State Partners: RI Office of Energy Resources, National Grid RI, RI District of Columbia Department and Education and RI Energy Efficiency & Resource State Partners: Department of Energy and Environment and DC Management Council Sustainable Energy Utility Partners in 2017/2018/2019/2020 Partners in 2017/2019/2020 Vermont Massachusetts State Partners: Efficiency Vermont State Partners: Massachusetts Department of Energy Resources Partners in 2017/2018/2019/2020 Partners in 2019 West Virginia New Hampshire State Partners: West Virginia Office of Energy State Partners: NH Office of Strategic Initiatives, NH Public Utilities Commission, Eversource Energy, NH Electric Coop, Unitil and Partners in 2020 Liberty Utilities Partners in 2017/2018/2019/2020 3 Agenda at a Glance 4 SESSION 1 The Current State of Smart Energy Homes and Buildings 5 Integrating Smart Energy Homes and Buildings with a Modernized Grid: Grid-interactive Efficient Buildings Overview Monica Neukomm, US DOE Building Technologies Office August 2020 U.S. DEPARTMENT OF ENERGY OFFICE OF ENERGY EFFICIENCY & RENEWABLE ENERGY 6 Smart Building…Smart Energy Management…GEB © Navigant Consulting Inc. -

Settlement Agreement

KEEGAN WERLIN LLP ATTORNEYS AT LAW 99 HIGH STREET, Suite 2900 BOSTON, MASSACHUSETTS 02110 TELECOPIER: ——— (617) 951- 1354 (617) 951-1400 July 2, 2020 Mark D. Marini, Secretary Department of Public Utilities One South Station, 5th Floor Boston, MA 02110 Re: Joint Petition of Eversource Energy, NiSource Inc., Eversource Gas of Massachusetts, and Bay State Gas Company d/b/a Columbia Gas of Massachusetts for Approval of Purchase and Sale of Assets Pursuant to General Laws Chapter 164, §§ 94 and 96 - D.P.U. 20-59 Dear Mr. Marini: Enclosed for filing with the Department of Public Utilities in the above-referenced proceeding is a Joint Motion for Approval of Settlement and the related Settlement Agreement,1 entered into by and among Bay State Gas Company d/b/a Columbia Gas of Massachusetts (“Bay State Gas”), and its holding company parent, NiSource Inc. (“NiSource”), Eversource Gas Company of Massachusetts and its holding company parent, Eversource Energy (“Eversource”), the Massachusetts Attorney General’s Office, the Massachusetts Department of Energy Resources, and the Low-Income Weatherization and Fuel Assistance Program Network (“Network”) (collectively, the “Settling Parties”) with regard to the proposed sale by NiSource and Bay State Gas, and acquisition by Eversource, of the business of Bay State Gas. Thank you for your attention to this matter. Sincerely, Cheryl M. Kimball, Esq. Enclosures cc: Hon. Matthew Nelson, Chair (cover letter only) Hon. Robert Hayden, Commissioner (cover letter only) 1 Also enclosed with this filing is a Settlement Explanatory Statement prepared by NiSource and Eversource, consistent with the Department’s requirements the Settlement Proposal Filing Requirements Memorandum (“Memorandum”) issued by the Department of Public Utilities (“Department”) on July 17, 2015, in Bay State Gas Company d/b/a Columbia Gas of Massachusetts, D.P.U. -

Net Benefits Filing for Eversource Acquisition of Columbia Gas Of

KEEGAN WERLIN LLP ATTORNEYS AT LAW 99 HIGH STREET, Suite 2900 BOSTON, MASSACHUSETTS 02110 TELECOPIER: ——— (617) 951- 1354 (617) 951-1400 July 2, 2020 Mark D. Marini, Secretary Department of Public Utilities One South Station, 5th Floor Boston, MA 02110 Re: Joint Petition of Eversource Energy, NiSource Inc., Eversource Gas Company of Massachusetts and Bay State Gas Company d/b/a Columbia Gas of Massachusetts for Approval of Purchase and Sale of Assets Pursuant to General Laws Chapter 164, §§ 94 and 96 - D.P.U. 20-59 Dear Mr. Marini: On July 2, 2020, pursuant to G.L. c. 164, §§ 94 and 96, Eversource Energy (“Eversource”), NiSource Inc. (“NiSource”), Eversource Gas Company of Massachusetts, and Bay State Gas Company d/b/a Columbia Gas of Massachusetts (“Bay State Gas”) (together the “Joint Petitioners”) submitted a petition to the Department of Public Utilities (the “Department”) for approval of NiSource’s sale of the operating assets of Bay State Gas to Eversource (the “Initial Filing”). A Joint Motion for Approval of Settlement and the related Settlement Agreement, entered into by and among Bay State Gas, and its holding company parent, NiSource, Eversource Gas Company of Massachusetts and its holding company parent, Eversource, the Massachusetts Attorney General’s Office, the Massachusetts Department of Energy Resources and the Low- Income Weatherization and Fuel Assistance Program Network (“Network”) was also filed on July 2nd (the “Settlement Agreement Filing”). Enclosed for filing with the Department is Exhibit JP-DPH-4 Supp., which supplements Exhibit JP-DPH-4 of the Joint Petitioner’s Initial Filing to incorporate the impact of the Settlement Agreement. -

The Honorable Charlie Baker Office of the Governor State House Boston, MA 02133 October 8, 2020 RE: Employer Support for Region

The Honorable Charlie Baker Office of the Governor State House Boston, MA 02133 October 8, 2020 RE: Employer Support for Regional Proposal for Clean Transportation Dear Governor Baker: We are a diverse group of organizations and businesses united by the extraordinary opportunity to modernize and decarbonize our region’s transportation system. We are writing to express our strong support for the draft Memorandum of Understanding on the Transportation and Climate Initiative (TCI). We believe that the policy created through TCI will achieve several of our shared goals focused on responding to the impacts of COVID-19: deploying necessary clean transportation technologies; mitigating greenhouse gas emissions from transportation; investing in much- needed public transit, alternative transportation and road infrastructure; and more. Why TCI is Not a Gas Tax TCI is a carbon pricing system focused on an essential outcome: reducing pollution from the transportation sector. A gas tax, by contrast, allows states to raise and spend revenues however they like. TCI’s carbon pricing system focuses on reducing pollution from the transportation sector by placing a cap on carbon emissions while auctioning emissions allowances; proceeds of which would only go towards low-GHG transportation improvements. Investment in Transportation Infrastructure and EVs We are heartened by the opportunity to invest TCI proceeds in new and improved transit solutions that will make transit, alternative transportation modes, and electrification of transportation more affordable, reliable, safe, and accessible. Public transit remains the most low-congestion, carbon-efficient, affordable and equitable way to move people. TCI proceeds could improve public transit, offer more choices for individuals, and encourage the purchase of electric and low-carbon-emitting vehicles (fleets, buses, passenger vehicles, trucks and rail). -

COMMONWEALTH of MASSACHUSETTS DEPARTMENT of PUBLIC UTILITIES ) Petition of NSTAR Elec

COMMONWEALTH OF MASSACHUSETTS DEPARTMENT OF PUBLIC UTILITIES __________________________________________ ) Petition of NSTAR Electric Company d/b/a ) Eversource Energy for Approval of Proposed ) D.P.U. 18-64 Long-Term Contracts for Clean Energy Projects ) Pursuant to Section 83D of An Act Relative to ) Green Communities, St. 2008, c. 169, as amended ) by St. 2016, c. 188, § 12 ) __________________________________________) __________________________________________ ) Petition of Massachusetts Electric Company and ) Nantucket Electric Company d/b/a National Grid ) for Approval of Proposed Long-Term ) D.P.U. 18-65 Contracts for Clean Energy Projects Pursuant to ) Section 83D of An Act Relative to Green ) Communities, St. 2008, c. 169, as amended by ) St. 2016, c. 188, § 12 ) __________________________________________) __________________________________________ ) Petition of Fitchburg Gas and Electric Light ) Company d/b/a Unitil for Approval of Proposed ) D.P.U. 18-66 Long-Term Contracts for Clean Energy Projects ) Pursuant to Section 83D of An Act Relative to ) Green Communities, St. 2008, c. 169, as amended ) by St. 2016, c. 188, § 12 ) __________________________________________) INITIAL BRIEF OF CONSERVATION LAW FOUNDATION Conservation Law Foundation (“CLF”) hereby submits its Initial Brief in support of the Petitions and the Contracts. RELEVANT FACTUAL AND PROCEDURAL BACKGROUND On July 23, 2018, NSTAR Electric Company d/b/a Eversource Energy (“Eversource”), Massachusetts Electric Company and Nantucket Electric Company d/b/a National Grid (“National Grid”), and Fitchburg Gas and Electric Light Company d/b/a Unitil (“Unitil”) (collectively, the electric “Distribution Companies”) each filed petitions with the Department of Public Utilities (“Department”) pursuant to Section 83D of An Act Relative to Green Communities, St.