Smaller Companies) Portfolio Update | 31 May 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Code Security Description ARI Arrium Ltd AWC Alumina Ltd AWE AWE

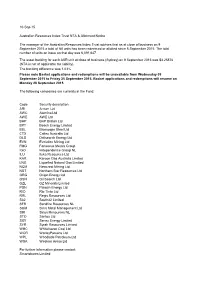

10-Sep-15 Australian Resources Index Trust NTA & Allotment Notice The manager of the Australian Resources Index Trust advises that as at close of business on 9 September 2015 a total of Nil units has been redeemed or allotted since 8 September 2015. The total number of units on issue on that day was 6,091,647. The asset backing for each ASR unit at close of business (Sydney) on 9 September 2015 was $3.25876 (NTA is net of applicable tax liability). The tracking difference was 1.03% Please note Basket applications and redemptions will be unavailable from Wednesday 09 September 2015 to Friday 25 September 2015. Basket applications and redemptions will resume on Monday 28 September 2015. The following companies are currently in the Fund: Code Security description ARI Arrium Ltd AWC Alumina Ltd AWE AWE Ltd BHP BHP Billiton Ltd BPT Beach Energy Limited BSL Bluescope Steel Ltd CTX Caltex Australia Ltd DLS Drillsearch Energy Ltd EVN Evolution Mining Ltd FMG Fortescue Metals Group IGO Independence Group NL ILU Iluka Resources Ltd KAR Karoon Gas Australia Limited LNG Liquefied Natural Gas Limited NCM Newcrest Mining Ltd NST Northern Star Resources Ltd ORG Origin Energy Ltd OSH Oil Search Ltd OZL OZ Minerals Limited PDN Paladin Energy Ltd. RIO Rio Tinto Ltd RRL Regis Resources Ltd S32 South32 Limited SFR Sandfire Resources NL SGM Sims Metal Management Ltd SIR Sirius Resources NL STO Santos Ltd SXY Senex Energy Limited SYR Syrah Resources Limited WHC Whitehaven Coal Ltd WOR WorleyParsons Ltd WPL Woodside Petroleum Ltd WSA Western Areas Ltd For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

Monthly NTA and Performance Update

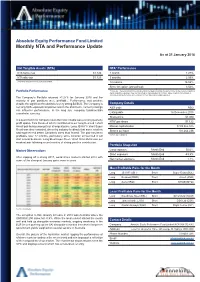

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

FTSE World Asia Pacific

2 FTSE Russell Publications 19 August 2021 FTSE World Asia Pacific Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.04 NEW Asustek Computer Inc 0.1 TAIWAN Cheil Worldwide 0.02 KOREA ZEALAND ASX 0.12 AUSTRALIA Cheng Shin Rubber Industry 0.03 TAIWAN AAC Technologies Holdings 0.05 HONG KONG Atlas Arteria 0.05 AUSTRALIA Chiba Bank 0.04 JAPAN ABC-Mart 0.02 JAPAN AU Optronics 0.08 TAIWAN Chicony Electronics 0.02 TAIWAN Accton Technology 0.07 TAIWAN Auckland International Airport 0.06 NEW China Airlines 0.02 TAIWAN Acer 0.03 TAIWAN ZEALAND China Development Financial Holdings 0.07 TAIWAN Acom 0.02 JAPAN Aurizon Holdings 0.05 AUSTRALIA China Life Insurance 0.02 TAIWAN Activia Properties 0.03 JAPAN Ausnet Services 0.03 AUSTRALIA China Motor 0.01 TAIWAN ADBRI 0.01 AUSTRALIA Australia & New Zealand Banking Group 0.64 AUSTRALIA China Steel 0.19 TAIWAN Advance Residence Investment 0.05 JAPAN Axiata Group Bhd 0.04 MALAYSIA China Travel International Investment <0.005 HONG KONG ADVANCED INFO SERVICE 0.06 THAILAND Azbil Corp. 0.06 JAPAN Hong Kong Advantech 0.05 TAIWAN B.Grimm Power 0.01 THAILAND Chow Tai Fook Jewellery Group 0.04 HONG KONG Advantest Corp 0.19 JAPAN Bandai Namco Holdings 0.14 JAPAN Chubu Elec Power 0.09 JAPAN Aeon 0.2 JAPAN Bangkok Bank (F) 0.02 THAILAND Chugai Seiyaku 0.27 JAPAN AEON Financial Service 0.01 JAPAN Bangkok Bank PCL (NVDR) 0.01 THAILAND Chugoku Bank 0.01 JAPAN Aeon Mall 0.02 JAPAN Bangkok Dusit Medical Services PCL 0.07 THAILAND Chugoku Electric Power 0.03 JAPAN Afterpay Touch Group 0.21 AUSTRALIA Bangkok Expressway and Metro 0.02 THAILAND Chunghwa Telecom 0.17 TAIWAN AGC 0.08 JAPAN Bangkok Life Assurance PCL 0.01 THAILAND CIMB Group Holdings 0.08 MALAYSIA AGL Energy 0.04 AUSTRALIA Bank of East Asia 0.03 HONG KONG CIMIC Group 0.01 AUSTRALIA AIA Group Ltd. -

Hybrids: Monthly Update - August 2020

Hybrids: Monthly Update - August 2020 Month: Aug-20 Trading days: 21 Period ending: Monday, 31 August 2020 Snapshot by Category Trades Value Australian Segment Bond Segment Number listed Market Cap $b Total (#) Trades per day (#) Volume (#) $m Convertible Preference Shares and Capital Notes 41 38.9 21,947 1,045 4,812,627 488.2 Convertible Bonds 4 0.3 327 16 791,325 5.3 Hybrid Securities 5 3.4 1,594 76 306,338 28.5 Total 50 42.59 23,868 1,137 5,910,290 521.9 Recent Listings Interest Rate / Distribution Entity ASX Code Size ($m) Type Listing Date Issue Price Maturity / Conv / Reset Dividend Frequency Last Price Macquarie Bank Limited MBLPC 641.0 Convertible Preference Shares and Capital03-Jun-2020 Notes $100.00 N/A 4.80% Qtrly $107.00 AMP Limited AMPPB 275.0 Convertible Preference Shares and 24-Dec-2019Capital Notes $100.00 16-Dec-2025 4.60% Qtrly $97.99 Suncorp Group Limited SUNPH 389.0 Convertible Preference Shares and 18-Dec-2019Capital Notes $100.00 17-Jun-2026 3.10% Qtrly $98.80 Clean Seas Seafood Limited CSSG 12.3 Convertible Bonds 18-Nov-2019 $1.00 18-Nov-2022 8.00% S/A $1.04 Commonwealth Bank of Australia CBAPI 1,650.0 Convertible Preference Shares and 15-Nov-2019Capital Notes $100.00 20-Apr-2027 3.10% Qtrly $99.21 Macquarie Group Limited MQGPD 905.5 Convertible Preference Shares and 28-Mar-2019Capital Notes $100.00 10-Sep-2026 4.25% Qtrly $104.85 National Australia Bank Limited NABPF 1,874.1 Convertible Preference Shares and 21-Mar-2019Capital Notes $100.00 17-Jun-2026 4.10% Qtrly $104.43 Westpac Banking Corporation WBCPI 1,423.1 -

Weekly Ratings, Targets, Forecast Changes - 28-05-21

Weekly Ratings, Targets, Forecast Changes - 28-05-21 May 31, 2021 Weekly update on stockbroker recommendation, target price, and earnings forecast changes. By Mark Woodruff Guide: The FNArena database tabulates the views of seven major Australian and international stock brokers: Citi, Credit Suisse, Macquarie, Morgan Stanley, Morgans, Ord Minnett and UBS. For the purpose of broker rating correlation, Outperform and Overweight ratings are grouped as Buy, Neutral is grouped with Hold and Underperform and Underweight are grouped as Sell to provide a Buy/Hold/Sell (B/H/S) ratio. Ratings, consensus target price and forecast earnings tables are published at the bottom of this report. Summary Period: Monday May 24 to Friday May 28, 2021 Total Upgrades: 9 Total Downgrades: 8 Net Ratings Breakdown: Buy 54.81%; Hold 38.67%; Sell 6.52% For the week ending Friday 28 May, there were nine upgrades and eight downgrades to ASX-listed companies by brokers in the FNArena database. After ALS Ltd posted an underlying FY21 profit 4.5% ahead of consensus last week, two brokers in the FNArena database downgraded the company rating due to a strong recent share price. Morgans attributed the result to astute management of costs and capacity, while Morgan Stanley was impressed by momentum in the Commodities segment, but notes the risk with cost inflation. The final dividend of 14.6 cents was well ahead of expectations, underpinned by strong cash conversionFNArena and debt reduction. ALS also achieved the weekly double by appearing atop the tables for the largest positive percentage change to broker’s forecast target prices and earnings. -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Business Leadership: the Catalyst for Accelerating Change

BUSINESS LEADERSHIP: THE CATALYST FOR ACCELERATING CHANGE Follow us on twitter @30pctAustralia OUR OBJECTIVE is to achieve 30% of ASX 200 seats held by women by end 2018. Gender balance on boards does achieve better outcomes. GREATER DIVERSITY ON BOARDS IS VITAL TO THE GOOD GOVERNANCE OF AUSTRALIAN BUSINESSES. FROM THE PERSPECTIVE OF PERFORMANCE AS WELL AS EQUITY THE CASE IS CLEAR. AUSTRALIA HAS MORE THAN ENOUGH CAPABLE WOMEN TO EXCEED THE 30% TARGET. IF YOUR BOARD IS NOT INVESTING IN THE CAPABILITY THAT DIVERSITY BRINGS, IT’S NOW A MARKED DEPARTURE FROM THE WHAT THE INVESTOR AND BROADER COMMUNITY EXPECT. Angus Armour FAICD, Managing Director & Chief Executive Officer, Australian Institute of Company Directors BY BRINGING TOGETHER INFLUENTIAL COMPANY CHAIRS, DIRECTORS, INVESTORS, HEAD HUNTERS AND CEOs, WE WANT TO DRIVE A BUSINESS-LED APPROACH TO INCREASING GENDER BALANCE THAT CHANGES THE WAY “COMPANIES APPROACH DIVERSITY ISSUES. Patricia Cross, Australian Chair 30% Club WHO WE ARE LEADERS LEADING BY EXAMPLE We are a group of chairs, directors and business leaders taking action to increase gender diversity on Australian boards. The Australian chapter launched in May 2015 with a goal of achieving 30% women on ASX 200 boards by the end of 2018. AUSTRALIAN 30% CLUB MEMBERS Andrew Forrest Fortescue Metals Douglas McTaggart Spark Group Ltd Infrastructure Trust Samuel Weiss Altium Ltd Kenneth MacKenzie BHP Billiton Ltd John Mulcahy Mirvac Ltd Stephen Johns Brambles Ltd Mark Johnson G8 Education Ltd John Shine CSL Ltd Paul Brasher Incitec Pivot -

Deliver Sustainable Value

Annual Report 2020 DELIVER ABN 34 008 675 018 SUSTAINABLE VALUE ABOUT ILUKA RESOURCES lluka Resources Limited (Iluka) is an international mineral With over 3,000 direct employees, the company has sands company with expertise in exploration, project operations and projects in Australia and Sierra Leone; development, mining, processing, marketing and and a globally integrated marketing network. rehabilitation. Iluka conducts international exploration activities and The company’s objective is to deliver sustainable value. is actively engaged in the rehabilitation of previous operations in the United States, Australia and Sierra With over 60 years’ industry experience, Iluka is a Leone. leading global producer of zircon and the high grade titanium dioxide feedstocks rutile and synthetic rutile. In Listed on the Australian Securities Exchange (ASX) addition, the company has an emerging position in rare and headquartered in Perth. Iluka holds a 20% stake in earth elements (rare earths). Iluka’s products are used Deterra Royalties Limited (Deterra), the largest ASX-listed in an increasing array of applications including home, resources focussed royalty company. workplace, medical, lifestyle and industrial uses. PRODUCTS TITANIUM DIOXIDE ZIRCON TiO2 Zr Iluka is the largest producer of natural Iluka is a leading global producer of rutile and a major producer of synthetic zircon. Zircon is opaque; and heat, water, rutile, which is an upgraded, value added chemical and abrasion resistant. Primary form of ilmenite. Collectively, these uses include ceramics; refractory and products are referred to as high-grade foundry applications; and zirconium titanium dioxide feedstocks, owing to chemicals. their high titanium content. Primary uses include pigment (paints), titanium metal and welding.