English GWL 2020 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Management's Discussion and Analysis

Management’s Discussion and Analysis Table of Contents 4 At a Glance The following Management’s Discussion and Analysis (“MD&A”) for George Weston 5 Our Business Limited (“GWL” or the “Company”) should be read in conjunction with the audited annual consolidated financial statements and the accompanying notes on pages 89 8 Key Performance Indicators to 171 of this Annual Report. The Company’s audited annual consolidated financial Operating Segments statements and the accompanying notes for the year ended December 31, 2019 have 12 Loblaw been prepared in accordance with International Financial Reporting Standards (“IFRS” or “GAAP”) as issued by the International Accounting Standards Board (“IASB”). 14 Choice Properties The audited annual consolidated financial statements include the accounts of 16 Weston Foods the Company and other entities that the Company controls and are reported in 19 Financial Results Canadian dollars, except where otherwise noted. 76 Outlook Under GAAP, certain expenses and income must be recognized that are not necessarily reflective of the Company’s underlying operating performance. Non-GAAP financial 77 Non-GAAP Financial Measures measures exclude the impact of certain items and are used internally when analyzing 87 Forward-Looking Statements consolidated and segment underlying operating performance. These non-GAAP 88 Additional Information financial measures are also helpful in assessing underlying operating performance on a consistent basis. See Section 14, “Non-GAAP Financial Measures”, of this MD&A for more information on the Company’s non-GAAP financial measures. The Company operates through its three reportable operating segments, Loblaw Companies Limited (“Loblaw”), Choice Properties Real Estate Investment Trust (“Choice Properties”) and Weston Foods. -

BMO Low Volatility Canadian Equity ETF (ZLB) Summary of Investment Portfolio • As at September 30, 2016

Quarterly portfolio disclosure BMO Low Volatility Canadian Equity ETF (ZLB) summary of investment portfolio • as at september 30, 2016 % of Net Asset % of Net Asset Portfolio Allocation Value Top 25 Holdings Value Financials ......................................................................25.4 Fairfax Financial Holdings Limited ............................................ 5.0 Consumer Staples .............................................................15.4 Dollarama Inc. ................................................................. 4.1 Real Estate ....................................................................12.0 Waste Connection, Inc. ........................................................ 3.7 Utilities ........................................................................11.7 Intact Financial Corporation ................................................... 3.6 Consumer Discretionary ......................................................10.3 Canadian REIT .................................................................. 3.6 Telecommunication Services .................................................. 8.1 BCE Inc. ......................................................................... 3.0 Information Technology ....................................................... 6.9 RioCan REIT ..................................................................... 2.9 Industrials ...................................................................... 3.7 Empire Company Limited, Class A ........................................... -

Growth Potential of Stocks: Security of a GIC

BMO Financial Group BMO Growth GIC Growth potential of Stocks: Security of a GIC This medium term GIC allows you to participate in the growth of Canadian stocks with no risk to your principal investment. It offers the potential to generate returns based on the performance of a basket of 15 large Canadian companies. Is this GIC right for you? Product Features This GIC may be right for you if you: Term • are looking to diversify your portfolio with a medium term investment Minimum Investment • would like principal protection Maximum Rate of Return • are willing to forego a guaranteed return for the potential for the Term to earn higher market linked returns • can keep your money invested until the end of the term 100 % Principal protected Reference Portfolio Key Benefits This GIC is an excellent way for you to gain access to the Company (equally weighted) returns on a portfolio of 15 large Canadian companies with • Toronto-Dominion Bank (The) (TD) • Royal Bank of Canada (RY) the security of principal protection. • Canadian Imperial Bank of • George Weston Limited (WN) Commerce (CM) • Principal protection 100% of your original investment is • Nutrien Ltd. (NTR) returned to you at maturity • Bank of Nova Scotia (The) (BNS) • Canadian Tire Corp Ltd (CTC.A) • BCE Inc. (BCE) • Higher return potential based on the performance of a • Suncor Energy Inc. (SU) portfolio of Canadian stocks • Saputo Inc. (SAP) • Enbridge Inc. (ENB) • Designed in partnership with BMO Capital Markets®, a • National Bank of Canada (NA) • TransCanada Corporation (TRP) market -

Blg.Com Mergers & Acquisitions Mining United States United Kingdom Agribusiness

Steve Suarez Partner T 416.367.6702 Business Tax F 416.367.6749 International Tax Toronto Tax Disputes & Litigation [email protected] Mergers & Acquisitions Mining United States United Kingdom Agribusiness Steve works exclusively on income tax matters, focusing on mergers and acquisitions, inbound and outbound investment, corporate restructurings and audit management, and tax dispute resolution. He is the founder of Mining Tax Canada website, a website devoted to mining-related taxation issues. Experience Sterling Capital Brokers in its merger with Luedey Consultants Inc. to become one of the largest independent employee-owned benefit consulting firms in Canada. Epiroc Canada Holding Inc., a subsidiary of Epiroc Rock Drills AB, in its acquisition of 100% of MineRP Holdings Inc. from Dundee Precious Metals Inc. (TSX: DPM). BNY Mellon Wealth Management, Advisory Services, Inc. in its sale to Guardian Capital Group (TSX: GCG). SterlingCapitalBrokers Ltd. acquired all of the issued and outstanding shares of Riverview Insurance Solutions Inc. Virtu Financial (NASDAQ: VIRT), a leading provider of financial services and products that leverages cutting-edge technology, in its sale of MATCHNow marketplace to Cboe Global Markets. Canadian Premier Life Insurance Company in its acquisition of Gerber Life Insurance Company's Canadian insurance business from U.S.-based Western & Southern Financial Group. Berkshire Hathaway Energy Company ("BHE"), in its indirect share purchase acquisition of the Montana Alberta Tie-Line from Enbridge Inc. for an approximate purchase price of $200M. Atlas Copco AB on its divisive reorganization and spin-out of Epiroc AB. HollyFrontier Corporation in connection with its acquisition of Petro-Canada Lubricants Inc. from Suncor Energy. -

2018 Annual Report

2018 Annual Report George Weston Limited Footnote Legend (1) See Section 18, “Non-GAAP Financial Measures”, of the Company’s 2018 Management’s Discussion and Analysis. (2) For financial definitions and ratios refer to the Glossary beginning on page 174. (3) To be read in conjunction with “Forward-Looking Statements” beginning on page 4. (4) Certain current and comparative figures have been restated to present Continuing Operations at Loblaw as a result of Loblaw’s spin-out of Choice Properties. See note 5 in the Company’s 2018 annual consolidated financial statements. (5) Certain figures have been restated as a result of IFRS 15, “Revenue from Contracts with Customers” and a change in accounting policy. See note 2 in the Company’s 2018 annual consolidated financial statements. Financial Highlights 1 / Report to Shareholders 2 / Management’s Discussion and Analysis 3 / Financial Results 79 / Three Year Summary 172 / Glossary 174 / Corporate Directory 176 / Shareholder and Corporate Information 177 Financial Highlights(2) As at or for the years ended December 31 ($ millions except where otherwise indicated) 2018 2017(5) Consolidated Operating Results Sales $ 48,568 $ 48,289 Operating income 2,585 2,561 Adjusted EBITDA(i) 4,528 4,337 Depreciation and amortization(ii) 1,746 1,685 Net interest expense and other financing charges 948 523 Adjusted net interest expense and other financing charges(i) 762 555 Income taxes 639 449 Adjusted income taxes(i) 680 712 Net earnings 998 1,589 Net earnings attributable to shareholders of the Company(iii) -

Odgers Berndtson CFO Talent Report 2021

CFO Talent Report 2021 WHAT’S NEXT FOR FINANCE LEADERSHIP ODGERS BERNDTSON CFO PRACTICE THE CFO REPORT Over the past 16 years, Odgers Berndtson tracked CFO TALENT movements in CFO leadership and analyzed trends in demographics, tenure, education and other aspects of professional development to better understand how the REPORT 2021 composition of top CFOs is evolving. We also interviewed leaders from Canada’s top organizations, including WHAT’S NEXT Shopify, Celestica and George Weston Limited, in order to gain insight into how public companies are recruiting, FOR FINANCE managing succession planning and developing their LEADERSHIP finance talent for the future. What we continue to see is that the growing demand The CFO role has never been more critical or more in for strategic acumen, transformational capabilities and demand — and yet the gap continues to grow between balanced oversight of an ever-expanding portfolio has what companies want in their CFOs and their ability to made the CFO role one of the most demanding and critical recruit and develop these top finance leaders. roles in the C-suite, and also increasingly harder to fill. Canada is in the midst of a CFO talent crunch and our new Chief Financial Officers have been thrust into the spotlight report explores what organizations can do about it. to help their companies adjust to market conditions, reinvent outdated business models or simply ensure enough liquidity to survive. To be successful, today’s finance leaders must quickly move beyond the numbers Succession planning is and understand the key levers to creating value across the more important than ever business and driving growth. -

2020 Annual Report

Rapport de gestion Le présent rapport de gestion (le « rapport de gestion ») de George Weston Limitée (« GWL » Table des matières ou la « société ») doit être lu en parallèle avec les états financiers consolidés annuels audités et les notes y afférentes figurant aux pages 100 à 182 du présent rapport annuel. Les états 4 Aperçu financiers consolidés annuels audités de la société et les notes y afférentes de l’exercice clos le 31 décembre 2020 ont été établis selon les Normes internationales d’information 5 Notre entreprise financière (les « IFRS » ou les « PCGR ») publiées par l’International Accounting Standards 8 Indicateurs de performance clés Board (l’« IASB »). Les états financiers consolidés annuels audités comprennent les comptes Secteurs d’exploitation de la société et ceux des autres entités que la société contrôle et sont présentés en dollars canadiens, sauf indication contraire. 12 Loblaw Certaines charges et certains produits qui ne sont pas nécessairement représentatifs de 14 Propriétés de Choix la performance sous-jacente de la société sur le plan de l’exploitation doivent être comptabilisés en vertu des PCGR. Les mesures financières non conformes aux PCGR ne 16 Weston Foods tiennent pas compte de l’incidence de certains éléments et sont utilisées à l’interne aux 19 Résultats financiers fins d’analyse de la performance sous-jacente consolidée et sectorielle sur le plan de 82 Perspectives l’exploitation. Ces mesures financières non conformes aux PCGR permettent également d’évaluer la performance sous-jacente sur le plan de l’exploitation de façon uniforme. 83 Mesures financières non Voir la rubrique 14, « Mesures financières non conformes aux PCGR », du présent rapport conformes aux PCGR de gestion pour plus de précisions sur les mesures financières non conformes aux PCGR 98 Énoncés prospectifs de la société. -

ANNUAL INFORMATION FORM (For the Year Ended December 31, 2020)

ANNUAL INFORMATION FORM (for the year ended December 31, 2020) March 1, 2021 GEORGE WESTON LIMITED ANNUAL INFORMATION FORM TABLE OF CONTENTS I. FORWARD-LOOKING STATEMENTS 1 II. CORPORATE STRUCTURE 2 Incorporation 2 Intercorporate Relationships 2 III. GENERAL DEVELOPMENT OF THE BUSINESS 3 Overview 3 COVID-19 3 Loblaw 3 Retail Segment 3 Financial Services Segment 5 Choice Properties 5 Acquisition of Canadian Real Estate Investment Trust 5 Reorganization of Choice Properties 6 Acquisition, Disposition and Development Activity 6 Weston Foods 10 Acquisitions 10 Dispositions 10 Capital Investment 10 Restructuring Activities 10 Financial Performance 10 IV. DESCRIPTION OF THE BUSINESS 11 Loblaw 11 Retail Segment 11 Financial Services Segment 15 Labour and Employment Matters 15 Intellectual Property 15 Environmental, Social and Governance 15 Choice Properties 16 Retail Portfolio 16 Industrial Portfolio 16 Office Portfolio 16 Residential Portfolio 16 Acquisitions 17 Development 17 Competition 18 Employment 18 Environmental, Social and Governance 18 Weston Foods 18 Principal Products 18 Production Facilities 19 Distribution to Consumers 19 Competitive Conditions 19 Brands 19 Raw Materials 20 Intellectual Property 20 Seasonality 20 Labour and Employment Matters 20 Environmental, Social and Governance 20 Food Safety and Public Health 20 Research and Development and New Products 21 Foreign Operations 21 V. PRIVACY AND ETHICS 21 VI. OPERATING AND FINANCIAL RISKS AND RISK MANAGEMENT 22 Enterprise Risks and Risk Management 22 COVID-19 Risks and Risk Management 22 Operating Risks and Risk Management 23 Financial Risks and Risk Management 33 VII. CAPITAL STRUCTURE AND MARKET FOR SECURITIES 35 Share Capital 35 Trading Price and Volume 36 Medium-Term Notes and Debt Securities 37 Credit Ratings 37 Dominion Bond Rating Service 38 Standard & Poor’s 39 VIII. -

English GWL 2020 Annual Report

Financial Results Management’s Statement of Responsibility for Financial Reporting 90 Independent Auditors’ Report 91 Consolidated Financial Statements 94 Consolidated Statements of Earnings 94 Consolidated Statements of Comprehensive Income 94 Consolidated Balance Sheets 95 Consolidated Statements of Changes in Equity 96 Consolidated Statements of Cash Flows 97 Notes to the Consolidated Financial Statements 98 Note 1. Nature and Description of the Reporting Entity 98 Note 2. Significant Accounting Policies 98 Note 3. Critical Accounting Estimates and Judgments 111 Note 4. Future Accounting Standard 113 Note 5. Subsidiaries 113 Note 6. Business Acquisitions 114 Note 7. Net Interest Expense and Other Financing Charges 114 Note 8. Income Taxes 115 Note 9. Basic and Diluted Net Earnings per Common Share 116 Note 10. Cash and Cash Equivalents, Short-Term Investments and Security Deposits 117 Note 11. Accounts Receivable 118 Note 12. Credit Card Receivables 118 Note 13. Inventories 120 Note 14. Assets Held for Sale 120 Note 15. Fixed Assets 121 Note 16. Investment Properties 123 Note 17. Equity Accounted Joint Ventures 124 Note 18. Intangible Assets 125 Note 19. Goodwill 127 Note 20. Other Assets 128 Note 21. Customer Loyalty Awards Program Liability 128 Note 22. Provisions 129 Note 23. Short-Term Debt 130 Note 24. Long-Term Debt 131 Note 25. Other Liabilities 134 Note 26. Share Capital 135 Note 27. Loblaw Capital Transactions 138 Note 28. Capital Management 139 Note 29. Post-Employment and Other Long-Term Employee Benefits 140 Note 30. Equity-Based Compensation 146 Note 31. Employee Costs 151 Note 32. Leases 152 Note 33. Financial Instruments 155 Note 34. -

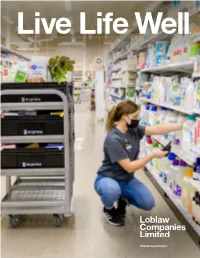

2020 Annual Report $2.8 Billion

2020 Annual Report $2.8 billion REVENUE FROM ONLINE SOURCES, AS WE SCALED E-COMMERCE, PROVIDING CUSTOMERS MORE FLEXIBILITY AND CHOICE THAN EVER BEFORE 25,026 TEMPORARY WORKERS HIRED AT THE PEAK OF THE PANDEMIC TO SUPPORT OUR STORES, COLLEAGUES AND CUSTOMERS 7,250 TEMPORARY WORKERS OFFERED PERMANENT EMPLOYMENT ONCE THE FIRST WAVE SUBSIDED 4,000 NUMBER OF PRODUCTS AVAILABLE AT SHOPPERSDRUGMART.CA, INCLUDING BEST SELLERS IN ELECTRONICS, BABY AND CHILD, HOME GOODS, OVER-THE-COUNTER AND EVERYDAY ESSENTIALS $445 million 2020 INVESTMENTS IN COVID- RELATED ADJUSTMENTS AND SAFETY MEASURES 2 million + FLU SHOTS ADMINISTERED IN OUR PHARMACIES IN 2020 285,000 NUMBER OF HOURS OUR STORES OPENED EXCLUSIVELY FOR SENIORS AND HEALTHCARE WORKERS A passion for customers fully ignited As a nation, and as an organization, 2020 was among the most stressful and anxious years in our history. Throughout this uncertainty, you – our colleagues – were there. As the country learned to deal with change, you brought comfort. As your friends and neighbours sought to meet their most fundamental of needs – for good food and good health – you opened your stores and your hearts to them. You truly helped Canadians Live Life Well®, and you can hold your heads high knowing that you helped a nation move forward. From the bottom of our hearts: thank you. Table of Contents 2 Our Stores, Our Colleagues, Our Strategy 4 Financial Highlights 5 Chairman’s Message 8 Our Divisions 10 Strategic Enablers 12 Corporate Social Responsibility 14 Corporate Governance Practices 16 Board of Directors 16 Leadership 17 Financial Review 2020 ANNUAL REPORT 1 LOBLAW COMPANIES LIMITED Our Stores Our Colleagues Our Strategy From the ground up, we exist to help Canadians Live Life Well.® This commitment factors into how we operate our stores and pharmacies day-to-day, and how we deliver on our long-term organizational strategy – known internally as the Strategic Compass. -

Final Transcript

FINAL TRANSCRIPT Loblaw Companies Limited Special Meeting of Shareholders Event Date/Time: October 18, 2018 — 11:00 a.m. E.T. Length: 28 minutes "Though CNW Group has used commercially reasonable efforts to produce this transcript, it does not represent or warrant that this transcript is error-free. CNW Group will not be responsible for any direct, indirect, incidental, special, consequential, loss of profits or other damages or liabilities which may arise out of or result from any use made of this transcript or any error contained therein." « Bien que CNW Telbec ait fait tous les efforts possibles pour produire cet audioscript, la société ne peut affirmer ou garantir qu’il ne contient aucune erreur. CNW Telbec ne peut être tenue responsable de pertes ou profits, responsabilités ou dommages causés par ou 1 découlant directement, indirectement, accidentellement ou corrélativement à l’utilisation de ce texte ou toute erreur qu’il contiendrait. » FINAL TRANSCRIPT October 18, 2018 — 11:00 a.m. E.T. Loblaw Companies Limited Special Meeting of Shareholders CORPORATE PARTICIPANTS Galen Weston Loblaw Companies Limited — Chairman and Chief Executive Officer CONFERENCE CALL PARTICIPANTS Leslie Dobus Shareholder Frank Sarosella Shareholder "Though CNW Group has used commercially reasonable efforts to produce this transcript, it does not represent or warrant that this transcript is error-free. CNW Group will not be responsible for any direct, indirect, incidental, special, consequential, loss of profits or other damages or liabilities which may arise out of or result from any use made of this transcript or any error contained therein." « Bien que CNW Telbec ait fait tous les efforts possibles pour produire cet audioscript, la société ne peut affirmer ou garantir qu’il ne contient aucune erreur. -

2020 Third Quarter Report

2020 Third Quarter Report West Block | Toronto ON 175 Bloor St East | Toronto ON Letter to Unitholders Fellow Unitholders, The COVID-19 pandemic continues to evolve, impacting quality of our portfolio. This focus was evident in the past our communities and our day-to-day lives. In response, quarter as we completed $32.3 million of dispositions and we are taking thoughtful actions to mitigate the effects of $248.0 million of acquisitions, including the acquisition the pandemic on our business operations and focusing of the Weston Centre, a multi-tenant office and retail on the best interests of our employees, tenants and other site that includes a Loblaw grocery store located in mid- stakeholders. While we are encouraged by signs of the town Toronto, and the remaining ownership interest in economy reopening in some areas and the positive impact West Block, a mixed-use site that combines retail shops that is having on most of our tenants, we acknowledge anchored by a Loblaw grocery store and office space that uncertainty persists. With that backdrop in mind, we located in downtown Toronto. are pleased with our financial results this past quarter, demonstrating that our business model, stable tenant Subsequent to the quarter end we completed or entered base and disciplined approach to financial management into agreements to complete additional dispositions of continue to position us well. $309.0 million and acquisitions of $85.9 million of highly sought-after industrial assets. This transaction activity Our diversified portfolio of office, retail and industrial demonstrates our ability to generate stable and growing properties is well occupied at 97.0% and leased to high- net operating income through strategic acquisitions and quality tenants across Canada.