Office of the Auditor General

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

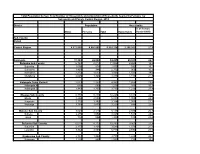

Vote:781 Kira Municipal Council Quarter1

Local Government Quarterly Performance Report FY 2017/18 Vote:781 Kira Municipal Council Quarter1 Terms and Conditions I hereby submit Quarter 1 performance progress report. This is in accordance with Paragraph 8 of the letter appointing me as an Accounting Officer for Vote:781 Kira Municipal Council for FY 2017/18. I confirm that the information provided in this report represents the actual performance achieved by the Local Government for the period under review. Name and Signature: Accounting Officer, Kira Municipal Council Date: 27/08/2019 cc. The LCV Chairperson (District) / The Mayor (Municipality) 1 Local Government Quarterly Performance Report FY 2017/18 Vote:781 Kira Municipal Council Quarter1 Summary: Overview of Revenues and Expenditures Overall Revenue Performance Ushs Thousands Approved Budget Cumulative Receipts % of Budget Received Locally Raised Revenues 7,511,400 1,237,037 16% Discretionary Government Transfers 2,214,269 570,758 26% Conditional Government Transfers 4,546,144 1,390,439 31% Other Government Transfers 0 308,889 0% Donor Funding 0 0 0% Total Revenues shares 14,271,813 3,507,123 25% Overall Expenditure Performance by Workplan Ushs Thousands Approved Cumulative Cumulative % Budget % Budget % Releases Budget Releases Expenditure Released Spent Spent Planning 298,531 40,580 12,950 14% 4% 32% Internal Audit 110,435 15,608 10,074 14% 9% 65% Administration 1,423,810 356,949 150,213 25% 11% 42% Finance 1,737,355 147,433 58,738 8% 3% 40% Statutory Bodies 1,105,035 225,198 222,244 20% 20% 99% Production and Marketing -

UGANDA: PLANNING MAP (Details)

IMU, UNOCHA Uganda http://www.ugandaclusters.ug http://ochaonline.un.org UGANDA: PLANNING MAP (Details) SUDAN NARENGEPAK KARENGA KATHILE KIDEPO NP !( NGACINO !( LOPULINGI KATHILE AGORO AGU FR PABAR AGORO !( !( KAMION !( Apoka TULIA PAMUJO !( KAWALAKOL RANGELAND ! KEI FR DIBOLYEC !( KERWA !( RUDI LOKWAKARAMOE !( POTIKA !( !( PAWACH METU LELAPWOT LAWIYE West PAWOR KALAPATA MIDIGO NYAPEA FR LOKORI KAABONG Moyo KAPALATA LODIKO ELENDEREA PAJAKIRI (! KAPEDO Dodoth !( PAMERI LAMWO FR LOTIM MOYO TC LICWAR KAPEDO (! WANDI EBWEA VUURA !( CHAKULYA KEI ! !( !( !( !( PARACELE !( KAMACHARIKOL INGILE Moyo AYUU POBURA NARIAMAOI !( !( LOKUNG Madi RANGELAND LEFORI ALALI OKUTI LOYORO AYIPE ORAA PAWAJA Opei MADI NAPORE MORUKORI GWERE MOYO PAMOYI PARAPONO ! MOROTO Nimule OPEI PALAJA !( ALURU ! !( LOKERUI PAMODO MIGO PAKALABULE KULUBA YUMBE PANGIRA LOKOLIA !( !( PANYANGA ELEGU PADWAT PALUGA !( !( KARENGA !( KOCHI LAMA KAL LOKIAL KAABONG TEUSO Laropi !( !( LIMIDIA POBEL LOPEDO DUFILE !( !( PALOGA LOMERIS/KABONG KOBOKO MASALOA LAROPI ! OLEBE MOCHA KATUM LOSONGOLO AWOBA !( !( !( DUFILE !( ORABA LIRI PALABEK KITENY SANGAR MONODU LUDARA OMBACHI LAROPI ELEGU OKOL !( (! !( !( !( KAL AKURUMOU KOMURIA MOYO LAROPI OMI Lamwo !( KULUBA Koboko PODO LIRI KAL PALORINYA DUFILE (! PADIBE Kaabong LOBONGIA !( LUDARA !( !( PANYANGA !( !( NYOKE ABAKADYAK BUNGU !( OROM KAABONG! TC !( GIMERE LAROPI PADWAT EAST !( KERILA BIAFRA !( LONGIRA PENA MINIKI Aringa!( ROMOGI PALORINYA JIHWA !( LAMWO KULUYE KATATWO !( PIRE BAMURE ORINJI (! BARINGA PALABEK WANGTIT OKOL KINGABA !( LEGU MINIKI -

THE UGANDA GAZETTE [13Th J Anuary

The THE RH Ptrat.ir OK I'<1 AND A T IE RKPt'BI.IC OF UGANDA Registered at the Published General Post Office for transmission within by East Africa as a Newspaper Uganda Gazette A uthority Vol. CX No. 2 13th January, 2017 Price: Shs. 5,000 CONTEXTS P a g e General Notice No. 12 of 2017. The Marriage Act—Notice ... ... ... 9 THE ADVOCATES ACT, CAP. 267. The Advocates Act—Notices ... ... ... 9 The Companies Act—Notices................. ... 9-10 NOTICE OF APPLICATION FOR A CERTIFICATE The Electricity Act— Notices ... ... ... 10-11 OF ELIGIBILITY. The Trademarks Act—Registration of Applications 11-18 Advertisements ... ... ... ... 18-27 I t is h e r e b y n o t if ie d that an application has been presented to the Law Council by Okiring Mark who is SUPPLEMENTS Statutory Instruments stated to be a holder of a Bachelor of Laws Degree from Uganda Christian University, Mukono, having been No. 1—The Trade (Licensing) (Grading of Business Areas) Instrument, 2017. awarded on the 4th day of July, 2014 and a Diploma in No. 2—The Trade (Licensing) (Amendment of Schedule) Legal Practice awarded by the Law Development Centre Instrument, 2017. on the 29th day of April, 2016, for the issuance of a B ill Certificate of Eligibility for entry of his name on the Roll of Advocates for Uganda. No. 1—The Anti - Terrorism (Amendment) Bill, 2017. Kampala, MARGARET APINY, 11th January, 2017. Secretary, Law Council. General N otice No. 10 of 2017. THE MARRIAGE ACT [Cap. 251 Revised Edition, 2000] General Notice No. -

LG Budget Estimates 201213 Wakiso.Pdf

Local Government Budget Estimates Vote: 555 Wakiso District Structure of Budget Estimates A: Overview of Revenues and Expenditures B: Detailed Estimates of Revenue C: Detailed Estimates of Expenditure D: Status of Arrears Page 1 Local Government Budget Estimates Vote: 555 Wakiso District A: Overview of Revenues and Expenditures Revenue Performance and Plans 2011/12 2012/13 Approved Budget Receipts by End Approved Budget June UShs 000's 1. Locally Raised Revenues 3,737,767 3,177,703 7,413,823 2a. Discretionary Government Transfers 5,373,311 4,952,624 5,648,166 2b. Conditional Government Transfers 28,713,079 27,512,936 32,601,298 2c. Other Government Transfers 6,853,215 4,532,570 10,697,450 3. Local Development Grant 1,757,586 1,949,046 1,756,183 Total Revenues 46,434,958 42,124,880 58,116,921 Expenditure Performance and Plans 2011/12 2012/13 Approved Budget Actual Approved Budget Expenditure by UShs 000's end of June 1a Administration 1,427,411 1,331,440 3,894,714 1b Multi-sectoral Transfers to LLGs 5,459,820 4,818,229 0 2 Finance 679,520 658,550 2,623,938 3 Statutory Bodies 1,017,337 885,126 1,981,617 4 Production and Marketing 3,060,260 3,015,477 3,522,157 5 Health 4,877,837 4,807,510 6,201,655 6 Education 21,144,765 19,753,179 24,948,712 7a Roads and Engineering 6,161,280 4,538,877 11,151,699 7b Water 802,836 631,193 1,063,321 8 Natural Resources 427,251 238,655 659,113 9 Community Based Services 610,472 678,202 1,175,071 10 Planning 630,334 302,574 560,032 11 Internal Audit 135,835 117,414 334,893 Grand Total 46,434,958 41,776,425 58,116,922 Wage Rec't: 22,456,951 21,702,872 24,924,778 Non Wage Rec't: 16,062,717 13,930,979 23,191,011 Domestic Dev't 7,915,291 6,142,574 10,001,133 Donor Dev't 0 0 0 Page 2 Local Government Budget Estimates Vote: 555 Wakiso District B: Detailed Estimates of Revenue 2011/12 2012/13 Approved Budget Receipts by End Approved Budget of June UShs 000's 1. -

Vote:781 Kira Municipal Council Quarter2

Local Government Quarterly Performance Report FY 2018/19 Vote:781 Kira Municipal Council Quarter2 Terms and Conditions I hereby submit Quarter 2 performance progress report. This is in accordance with Paragraph 8 of the letter appointing me as an Accounting Officer for Vote:781 Kira Municipal Council for FY 2018/19. I confirm that the information provided in this report represents the actual performance achieved by the Local Government for the period under review. Name and Signature: Accounting Officer, Kira Municipal Council Date: 24/01/2019 cc. The LCV Chairperson (District) / The Mayor (Municipality) 1 Local Government Quarterly Performance Report FY 2018/19 Vote:781 Kira Municipal Council Quarter2 Summary: Overview of Revenues and Expenditures Overall Revenue Performance Ushs Thousands Approved Budget Cumulative Receipts % of Budget Received Locally Raised Revenues 6,177,725 3,467,321 56% Discretionary Government Transfers 2,130,791 1,182,235 55% Conditional Government Transfers 5,982,048 2,899,735 48% Other Government Transfers 3,356,981 1,247,294 37% Donor Funding 280,000 32,370 12% Total Revenues shares 17,927,545 8,828,955 49% Overall Expenditure Performance by Workplan Ushs Thousands Approved Cumulative Cumulative % Budget % Budget % Releases Budget Releases Expenditure Released Spent Spent Planning 185,173 105,514 73,428 57% 40% 70% Internal Audit 102,947 46,004 44,248 45% 43% 96% Administration 1,542,634 1,004,160 782,571 65% 51% 78% Finance 1,378,790 867,332 728,057 63% 53% 84% Statutory Bodies 671,770 452,301 385,332 67% 57% -

Population by Parish

Total Population by Sex, Total Number of Households and proportion of Households headed by Females by Subcounty and Parish, Central Region, 2014 District Population Households % of Female Males Females Total Households Headed HHS Sub-County Parish Central Region 4,672,658 4,856,580 9,529,238 2,298,942 27.5 Kalangala 31,349 22,944 54,293 20,041 22.7 Bujumba Sub County 6,743 4,813 11,556 4,453 19.3 Bujumba 1,096 874 1,970 592 19.1 Bunyama 1,428 944 2,372 962 16.2 Bwendero 2,214 1,627 3,841 1,586 19.0 Mulabana 2,005 1,368 3,373 1,313 21.9 Kalangala Town Council 2,623 2,357 4,980 1,604 29.4 Kalangala A 680 590 1,270 385 35.8 Kalangala B 1,943 1,767 3,710 1,219 27.4 Mugoye Sub County 6,777 5,447 12,224 3,811 23.9 Bbeta 3,246 2,585 5,831 1,909 24.9 Kagulube 1,772 1,392 3,164 1,003 23.3 Kayunga 1,759 1,470 3,229 899 22.6 Bubeke Sub County 3,023 2,110 5,133 2,036 26.7 Bubeke 2,275 1,554 3,829 1,518 28.0 Jaana 748 556 1,304 518 23.0 Bufumira Sub County 6,019 4,273 10,292 3,967 22.8 Bufumira 2,177 1,404 3,581 1,373 21.4 Lulamba 3,842 2,869 6,711 2,594 23.5 Kyamuswa Sub County 2,733 1,998 4,731 1,820 20.3 Buwanga 1,226 865 2,091 770 19.5 Buzingo 1,507 1,133 2,640 1,050 20.9 Maziga Sub County 3,431 1,946 5,377 2,350 20.8 Buggala 2,190 1,228 3,418 1,484 21.4 Butulume 1,241 718 1,959 866 19.9 Kampala District 712,762 794,318 1,507,080 414,406 30.3 Central Division 37,435 37,733 75,168 23,142 32.7 Bukesa 4,326 4,711 9,037 2,809 37.0 Civic Centre 224 151 375 161 14.9 Industrial Area 383 262 645 259 13.9 Kagugube 2,983 3,246 6,229 2,608 42.7 Kamwokya -

The Uganda Gazette, General Notice No. 425 of 2021

LOCAL GOVERNMENT COUNCIL ELECTIONS, 2021 SCHEDULE OF ELECTION RESULTS FOR DISTRICT/CITY DIRECTLY ELECTED COUNCILLORS DISTRICT CONSTITUENCY ELECTORAL AREA SURNAME OTHER NAME PARTY VOTES STATUS ABIM LABWOR COUNTY ABIM KIYINGI OBIA BENARD INDEPENDENT 693 ABIM LABWOR COUNTY ABIM OMWONY ISAAC INNOCENT NRM 662 ABIM LABWOR COUNTY ABIM TOWN COUNCIL OKELLO GODFREY NRM 1,093 ABIM LABWOR COUNTY ABIM TOWN COUNCIL OWINY GORDON OBIN FDC 328 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OGWANG JOHN MIKE INDEPENDENT 31 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OKAWA KAKAS MOSES INDEPENDENT 14 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OTOKE EMMANUEL GEORGE NRM 338 ABIM LABWOR COUNTY ALEREK OKECH GODFREY NRM Unopposed ABIM LABWOR COUNTY ALEREK TOWN COUNCIL OWINY PAUL ARTHUR NRM Unopposed ABIM LABWOR COUNTY ATUNGA ABALLA BENARD NRM 564 ABIM LABWOR COUNTY ATUNGA OKECH RICHARD INDEPENDENT 994 ABIM LABWOR COUNTY AWACH ODYEK SIMON PETER INDEPENDENT 458 ABIM LABWOR COUNTY AWACH OKELLO JOHN BOSCO NRM 1,237 ABIM LABWOR COUNTY CAMKOK ALOYO BEATRICE GLADIES NRM 163 ABIM LABWOR COUNTY CAMKOK OBANGAKENE POPE PAUL INDEPENDENT 15 ABIM LABWOR COUNTY KIRU TOWN COUNCIL ABURA CHARLES PHILIPS NRM 823 ABIM LABWOR COUNTY KIRU TOWN COUNCIL OCHIENG JOSEPH ANYING UPC 404 ABIM LABWOR COUNTY LOTUKEI OBUA TOM INDEPENDENT 146 ABIM LABWOR COUNTY LOTUKEI OGWANG GODWIN NRM 182 ABIM LABWOR COUNTY LOTUKEI OKELLO BISMARCK INNOCENT INDEPENDENT 356 ABIM LABWOR COUNTY MAGAMAGA OTHII CHARLES GORDON NRM Unopposed ABIM LABWOR COUNTY MORULEM OKELLO GEORGE ROBERT NRM 755 ABIM LABWOR COUNTY MORULEM OKELLO MUKASA -

34 NEW VISION, Thursday, March 5, 2020 CLASSIFIED ADVERTS

34 NEW VISION, Thursday, March 5, 2020 CLASSIFIED ADVERTS Quality And Affordable Housing Honest Estate Developers BIG EASTER DISCOUNT!! Plots for sale with Land Titles ZION PLOTS WITH TITLES FLORIDA APARTMENTS Well located Residential Accessible with Public Means 1. BIIRA - BULENGA 1. ENTEBBE ROAD Located in Kira town, Estates with Mailo land titles TRINITY TRUSTED ESTATES More Plots in Developed Estates “Make the Right Move” 50x100ft - 37m LUTABA HILL VIEW VIA SSISA Mamerito Road on the 1. NEW OLIVES ESTATE 2. BOMBO TOWN EXT NEAR overlooking Akright Estate - 3km DEVELOPERS LTD 1. MATUGGA STAR CITY - 7M We Deal in Buying and Selling PLOTS FOR SALE Tarmac. NKUMBA With a water KAKUNGULU SECONDARY from the Main road @ 30M 2. GAYAZA-VVUMBA - AFFORDABLE front in a developed 50x100ft - 7m cash 2. NKUMBA LAKE VIEW Land & properties Countrywide 8M -10M 1. GAYAZA WABITUNGULU neighbourhood. 50x100ft - 8m Instalments touching the main rd, APARTMENTS FOR SALE ENTEBBE ROAD Mailo 50x100ft plots for Sale, 3. GAYAZA – NALUMULI- 45min drive from Kampala 50x100ft - 45m 3. MAYA MODERN ESTATE 50x100ft - 40m 70x100ft - 64m Ready Private Mailo Titles 11M Phase1- 4.5m Cash 50x100ft - 18M cash 3km from Tarmac 2. DELIGHT CITY ESTATE 4. GAYAZA – KIWENDA- 13M 5.5 Instalment 10% discount on 3. KAWUKU ZZIRU EXECUTIVE NEW ESTATE!!! BOMBO ROAD - MATUGGA 1. LUKWANGA, SENTEMA 1.5km from Tarmac SPECIAL OFFER cash payment ESTATE ENTEBBE Road 50x100ft - 9.5m ROAD. Power & Water is 5. GAYAZA-NAMULONGE- 4. MUKONO SATELITE CITY off 50x100ft - 26m 2. GAYAZA-WAKATAYI 100x100ft - 19m available on site. Taxis are 13M Katosi Road 4km from Tarmac 50x100ft: 3. -

Vote:016 Ministry of Works and Transport V1: Vote Overview I

Ministry of Works and Transport Ministerial Policy Statement FY 2021/22 Vote:016 Ministry of Works and Transport V1: Vote Overview I. Vote Mission Statement To promote adequate, safe and well maintained Works and Transport Infrastructure and Services for Social Economic Development of Uganda II. Strategic Objective 1. Develop adequate, reliable and efficient multimodal transport network in the Country 2. Improve the human resource and institutional capacity of the Ministry to efficiently execute her mandate 3. Strengthen the National Construction Industry 4. Increase the safety of transport services and infrastructure for all modes of transport and all categories of users III. Major Achievements in 2020/21 The approved budget for Vote 016-MoWT for FY 2020/2021 was UGX 1,571.903bn. Of this amount, UGX 11.866bn is for wages (0.8%), UGX 123.782bn for nonwage recurrent (7.9%), UGX 809.549bn for GoU development (51.5%), UGX 625.957bn for donor contribution-development (39.8%), and UGX 0.750bn for arrears. The release performance by the end of Q2 was UGX 581.161bn (36.9%) and of which UGX 571.446bn (98.3%) was expended. Ushs 5.933bn (50.0%) was released for wage and out of which UGX 5.534bn (93.3%) was spent; UGX 45.421bn (36.7%) was released for non-wage recurrent and out of which UGX 43.815bn (96.5%) was spent; UGX 406.615bn (50.2%) was released under GoU development budget and out of which UGX 403.814bn (99.3%) was spent; UGX 122.443bn (19.6%) was released as external financing and UGX 118.093bn (96.4%) was spent. -

BFP Kira Municipal Council FY 2021

PROPOSED STRUCTURE OF THE VOTE BFP Vote Budget Framework Paper FY 2021/22 _____________________________________________________________________________________________________ VOTE:[781] KIRA MUNICIPAL LOCAL GOVERNMENT _____________________________________________________________________________________________________ FORWARD This Budget Frame work Paper is a publication of Background to the budget of the forthcoming financial year 2021/2022. This BFP has been prepared with a focus of our mission "To serve the Municipality through coordinated and effective service delivery” which focuses on National and Local priorities in order to promote sustainable social and economic development of Municipality. To demonstrate the element of equal opportunity, the Municipality has been able to allocate resources to Local priorities under different departments, in consideration of factors that perpetuates inequalities among departments for example, number of staff in a department, their role, mandate, expected out puts whilst ensuring the achievement of "growth, employment, social economic Transformation for prosperity" in line with the National Development Plan III. As we advance towards the FY 2021/2022, our main agenda for period will focus on, addressing the problems of inequality through strengthening school inspection to ensure compliance to education guidelines which addresses gender and equity issues, promote Environment sustainability, solid waste management, better sanitation and hygiene and reduce urban poverty while addressing the national programms in addition Construction of administration Block for all staff at the Municipal headquarter, for good governance and enhancing good physical planning are among the priorities of the Municipality. On behalf of the Municipality and my self, i wish to thank the Council and Technical staff for their input in the 2021/2022 BFP, i also extend my sincere gratitude to central government for its continued and timely release of funds to Municipality which has enabled the Municipality to implement decentralized services. -

Uganda Gazette-.THE REPUBLI

The bos THE REPUBLIC OF UGANDA THE REPUBLI Registered at the Published General Post Officefor transmission within East~Africa as a Uganda Gazette-. Vol. CX No. 19 31st March, 2017 Price: Shs. 5,000 CONTENTS PAGE General Notice No. 248 of 2017. Fe aea Aci—Noees + s : a THE PARLIAMENTARYELECTIONSACT, e Companies Act— Notices te ee ACT NO. 17 OF 200 The Local Governments (Rating) Act—Notice ... 307-308 i : The Advocates Act— Notices... ves a 308 Section 9 (1) The Mining Act—Notices_... a vee 308 The Uganda National Examinations Board—Notices 309-311 AOTCE The Electricity Act—Notice ... a. 312 APPOINTMENT OF NOMINATION DAYS AND The Architects Registration Act—Notice a 312 VENUE FOR PURPOSES OF THE The Trademarks Act—Registration of Applications 312-317 PARLIAMENTARYBY-ELECTION FOR DIRECTLY ELECTED MEMBER Advertisements 317-332 OF PARLIAMENT, KAGOMA COUNTY CONSTITUENCY, JINJA DISTRICT. SUPPLEMENTS NOTICE IS HEREBY GIVENbythe Electoral Commission Bill in accordance with Section 9(1) of the Parliamentary Elections No. 8—The Appropriation Bill, 2017. Act, No 17 of 2005,that the 24th day of April, 2017 and 25th day of April, 2017 are hereby appointed nomination days and Act published for purposesofthe Parliamentary by-election for the No. 2—The East African Development Bank (Amendment) Directly Elected Member of Parliament, Kagoma County Act, 2017. Constituency, Jinja District. Nominationsshall be at the Kagoma Sub County Headquarters’ Hall, Kagoma County Constituency, Jinja District, from 9.00 General Notice No. 247 of 2017. a.m to 5.00 p.m oneachofthe appointed dates. THE LOCAL GOVERNMENTSACT, Issued at Kampala, this 28th CAP. -

Planned Shutdown March 2021

PLANNED SHUTDOWN FOR MARCH 2021 SYSTEM IMPROVEMENT AND ROUTINE MAINTENANCE REGION DAY DATE SUBSTATION FEEDER/PLANT PLANNED WORK DISTRICT AREAS & CUSTOMERS TO BE AFFECTED North Eastern Wednesday 03rd March 2021 UETCL Hoima Kinubi 33kV Creating h-p tee-off to install dropout fused isolator for direct Hoima Kibati TC, Kalyabuhire kibati t-off and line clearance Kampala West Wednesday 03rd March 2021 Kisugu 11kV and 33kV switchgear Routine Maintenance Kabalagala Kitaranga,Kiwafu,Meya Beach,Kemifa,Nabutiti,Wheeling Zone,Prayer Palace,Wonder world,Comrade bar,Galax FM,Seroma,Mutesasira zone,Internal East Africa University,Shell Kansanga,Elite supermarket,Saida Bumba, Olanya,Kadaga,Diplomatic hotel,Paradiso hotel,Internatiol Hospital Kampala,Kisugu church of Uganda,Zimwe road,Mukwano Apartment,Kabalagala Police station,Diposh bar,Kironde road,General Machinery,Bukasa, parts of Namuwongo, Seebo Green, Bukasa stone quarry,Musisi road,Water tank Hill,Muyenga Umeme mast,Benging Clinic,Muyenga High school, Muyenga chicken tonigt.Heritage International school, Kisugu ,Kibuli,Kikubamutwe,Kibuli mosque,CID Headquarters,Part of Police barracks,Namuwongo publication,Multiple Industry,Sure telecom switching station,Kakungulu Memorial,Kibuli sec sch,Green Hill Academy Kampala West Wednesday 03rd March 2021 Kisugu 11kV and 33kV Take-off MV Cable Inspection,Replacement of rotten structures & jumper Kabalagala Kitaranga,Kiwafu,Meya Beach,Kemifa,Nabutiti,Wheeling Zone,Prayer Palace,Wonder Structures, Lugogo repairs world,Comrade bar,Galax FM,Seroma,Mutesasira