Special Audit Reports Nil Nil 6

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Muzaffargarh

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !! ! ! ! ! ! Overview - Muzaffargarh ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! Bhattiwala Kherawala !Molewala Siwagwala ! Mari PuadhiMari Poadhi LelahLeiah ! ! Chanawala ! ! ! ! ! ! ! Ladhranwala Kherawala! ! ! ! Lerah Tindawala Ahmad Chirawala Bhukwala Jhang Tehsil ! ! ! ! ! ! ! Lalwala ! Pehar MorjhangiMarjhangi Anwarwal!a Khairewala ! ! ! ! ! ! ! ! ! Wali Dadwala MuhammadwalaJindawala Faqirewala ! ! ! ! ! ! ! ! ! MalkaniRetra !Shah Alamwala ! Bhindwalwala ! ! ! ! ! Patti Khar ! ! ! Dargaiwala Shah Alamwala ! ! ! ! ! ! Sultanwala ! ! Zubairwa(24e6)la Vasawa Khiarewala ! ! ! ! ! ! ! Jhok Bodo Mochiwala PakkaMochiwala KumharKumbar ! ! ! ! ! ! Qaziwala ! Haji MuhammadKhanwala Basti Dagi ! ! ! ! ! Lalwala Vasawa ! ! ! Mirani ! ! Munnawala! ! ! Mughlanwala ! Le! gend ! Sohnawala ! ! ! ! ! Pir Shahwala! ! ! Langanwala ! ! ! ! Chaubara ! Rajawala B!asti Saqi ! ! ! ! ! ! ! ! ! BuranawalaBuranawala !Gullanwala ! ! ! ! ! Jahaniawala ! ! ! ! ! Pathanwala Rajawala Maqaliwala Sanpalwala Massu Khanwala ! ! ! ! ! ! Bhandniwal!a Josawala ! ! Basti NasirBabhan Jaman Shah !Tarkhanwala ! !Mohanawala ! ! ! ! ! ! ! ! ! ! Basti Naseer Tarkhanwala Mohanawala !Citiy / Town ! Sohbawala ! Basti Bhedanwala ! ! ! ! ! ! Sohaganwala Bhurliwala ! ! ! ! Thattha BulaniBolani Ladhana Kunnal Thal Pharlawala ! ! ! ! ! ! ! ! ! ! ! Ganjiwala Pinglarwala Sanpal Siddiq Bajwa ! ! ! ! ! Anhiwala Balochanwala ! Pahrewali ! ! Ahmadwala ! ! ! -

To View NSP QAT Schedule

EMIS CODE New QAT Program Sr. No Shift Time SCHOOL NAME Address TEHSIL DISTRICT REGION QAT Day /SCHOOL CODE Date Name 12.30 pm NEW AGE PUBLIC UC Name Dhurnal, UC # 39, Moza FATEH 1 B ATK-FJG-NSP-VIII-3061 ATTOCK North 14 18.12.18 NSP to 2.30 pm SCHOOL Dhurnal, Chak / Basti Dhurnal Ada, JANG Tehsil Fateh Jung District Attock 12.30 pm Village Bai, PO Munnoo Nagar, Tehsil HASSANAB 2 B ATK-HDL-NSP-IV-210 Sun Rise High School ATTOCK North 11 14.12.18 NSP to 2.30 pm Hassan Abdal, District Attock DAL 12.30 pm Science Secondary Thatti Sado Shah, Po Akhlas, Tehsil PINDI 3 B ATK-PGB-NSP-IV-214 ATTOCK North 16 20.12.18 NSP to 2.30 pm School Pindi Gheb, District Attock GHEB 12.30 pm Al Aziz Educational Village Gangawali, Teshil Pindi Gheb, PINDI 4 B ATK-PGB-NSP-IV-216 ATTOCK North 17 09.01.19 NSP to 2.30 pm School System District Attock GHEB Basti Haider town(Pindi Gheb), Mouza 12.30 pm PINDI 5 B ATK-PGB-NSP-VII-2477 Hamza Public School Pindi Gheb, UC Name Chakki, UC # 53, ATTOCK North 17 09.01.19 NSP to 2.30 pm GHEB Tehsil Pindi Gheb, District Attock. Mohallah Jibby. Village Qiblabandi, PO 12.30 pm Tameer-e-Seerat Public 6 B ATK-HZO-NSP-IV-211 Kotkay, Via BaraZai, Tehsil Hazro, HAZRO ATTOCK North 12 15.12.18 NSP to 2.30 pm School District Attock 9.00 am to Stars Public Elementary 7 A ATK-ATK-NSP-IV-207 Dhoke Jawanda, Tehsil & District Attock ATTOCK ATTOCK North 12 15.12.18 NSP 11.00 School 12.30 pm Muslim Scholar Public Dhoke Qureshian, P/O Rangwad, tehsil 8 B ATK-JND-NSP-VI-656 JAND ATTOCK North 15 19.12.18 NSP to 2.30 pm School Jand 12.30 pm Farooqabad -

DERA-GHAZI-KHAN-Rend60.Pdf

Renewal List S/NO REN# / NAME FATHER'S PRESENT ADDRESS DATE OF ACADEMIC REN DATE NAME BIRTH QUALIFICATION 1 39939 ZAFAR PEER BUKHSH CHAK TOPI WALA MOUZA KHAKHI P/O SAMEDISTT. 7-10-1984 MATRIC 13/7/2014 HUSSAIN D.G. KHAN , DERA GHAZI KHAN, PUNJAB 2 37693 ABDUL RASHID ELAHI BAKHSH IDREES TOWN GADAI SHUMALI P/O SAMIN TEH & 1-10-1970 MATRIC 14/7/2014 DISTT. D.G. KHAN , DERA GHAZI KHAN, PUNJAB 3 21707 ABID HUSSAIN KHADIM CHOTI ZARIN BASTI MARI WALAP.O. HASSAN ABAD, 10/5/1978 MATRIC 14/07/2014 HUSSAIN DERA GHAZI KHAN, PUNJAB 4 32701 SAAD ULLAH MUHAMMAD H/NO. 92 BLOCK NO. 15 EID GAH ROAD D, G, KHAN , 26-12- MATRIC 15/07/2014 SAFDAR SAFDAR DERA GHAZI KHAN, PUNJAB 1975 5 47704 GHULAM ALLAH WASAYA VILL, BAQIR WALA P/O NUTKANI TEH, TAUNSA 7-7-1978 MATRIC 19/07/2014 MUSTAFA SHARIF DISTT,, DERA GHAZI KHAN, PUNJAB 6 31539 MUNIR AHMED MOLVI BASHIR MORAH P/O NANKANI TEH, TOUNSAH DISTT, D G 28-5-1973 MATRIC 04/09/2014 AHMED KHAN, DERA GHAZI KHAN, PUNJAB 7 22237 SALEEM MIRZA H.N.82BLOCK G, DERA GHAZI KHAN, PUNJAB 1/4/1974 MATRIC 20/09/2014 AKHTAR MUHAMMAD RAFIQ 8 37680 MUHAMMAD MUHAMMAD HOUSE NO. 92, BLOCK -9, , DERA GHAZI KHAN, 31-8-1968 MATRIC 23/9/2014 SALEEM SHARIF PUNJAB SHARIF 9 40134 MUHAMMAD MUHAMMAD H NO. 102 BLOCK F D G KHAN, DERA GHAZI KHAN, 24-2-1984 MATRIC 27/9/2014 ALI ANSARI RIAZ ANSARI PUNJAB 10 40135 MUHAMMAD MUHAMMAD BLOCK NO. -

Find Address of Your Nearest Loan Center and Phone Number of Concerned Focal Person

Find address of your nearest loan center and phone number of concerned focal person Loan Center/ S.No. Province District PO Name City / Tehsil Focal Person Contact No. Union Council/ Location Address Branch Name Akhuwat Islamic College Chowk Oppsite Boys College 1 Azad Jammu and Kashmir Bagh Bagh Bagh Nadeem Ahmed 0314-5273451 Microfinance (AIM) Sudan Galli Road Baagh Akhuwat Islamic Muzaffarabad Road Near main bazar 2 Azad Jammu and Kashmir Bagh Dhir Kot Dhir Kot Nadeem Ahmed 0314-5273451 Microfinance (AIM) dhir kot Akhuwat Islamic Mang bajri arja near chambar hotel 3 Azad Jammu and Kashmir Bagh Harighel Harighel Nadeem Ahmed 0314-5273451 Microfinance (AIM) Harighel Akhuwat Islamic 4 Azad Jammu and Kashmir Bhimber Bhimber Bhimber Arshad Mehmood 0346-4663605 Kotli Mor Near Muslim & School Microfinance (AIM) Akhuwat Islamic 5 Azad Jammu and Kashmir Bhimber Barnala Barnala Arshad Mehmood 0346-4663605 Main Road Bimber & Barnala Road Microfinance (AIM) Akhuwat Islamic Main choki Bazar near Sir Syed girls 6 Azad Jammu and Kashmir Bhimber Samahni Samahni Arshad Mehmood 0346-4663605 Microfinance (AIM) College choki Samahni Helping Hand for Adnan Anwar HHRD Distrcict Office Relief and Hattian,Near Smart Electronics,Choke 7 Azad Jammu and Kashmir Hattian Hattian UC Hattian Adnan Anwer 0341-9488995 Development Bazar, PO, Tehsil and District (HHRD) Hattianbala. Helping Hand for Adnan Anwar HHRD Distrcict Office Relief and Hattian,Near Smart Electronics,Choke 8 Azad Jammu and Kashmir Hattian Hattian UC Langla Adnan Anwer 0341-9488995 Development Bazar, PO, Tehsil and District (HHRD) Hattianbala. Helping Hand for Relief and Zahid Hussain HHRD Lamnian office 9 Azad Jammu and Kashmir Hattian Hattian UC Lamnian Zahid Hussain 0345-9071063 Development Main Lamnian Bazar Hattian Bala. -

Village List of Multan Division , Pakistan

Cel'.Us 51·No. 30B (I) M.lnt.6-19 300 CENSUS OF PAKISTAN, 1951 VILLAGE LIST PUNJAB Multan Division OFFICE Of THE PROVINCIAL · .. ·l),ITENDENT CENSUS, J~ 1952 ,~ :{< 'AND BAHAWALPUR, P,IC1!iR.. 10 , , FOREWOf~D This Village Ust has been prepared from the material collected in con nection with the Census of Pakistan, 1951. The object of the List is to present useful information about our villages. It was considered that in a predominantly rural country like Pakistan, reliable village statistics should be available and it is hoped that the Village List will form the basis for the continued collection of such statistics. A summary table of the totals for each tehsil showinz its area to the nearest square mile, and its population and the number of houses to the nearest hundred is given on page I together with the page number on which each tehsil begins. The general village table, which has been compiled district-wise and arranged tehsil-wise, appears on page 3 et seq. Within each tehsll th~ Revenue Kanungo ho/qas are shown according to their order in the census records. The Village in which the Revenue Kanungo usually resides is printed in bold type at the beginning of each Kanungo halqa and the remaining villages comprising the halqas, are shown thereunder in the order of their revenue hadbast numbers, which are given in column a. Rakhs (tree plantations) and other similar area,. even where they are allotted separate revenue hadbast nurY'lbcrs have not been shown as they were not reported in the Charge and Household summaries, to be inhabited. -

8. ANNEX-1- List of District and Ucs.Pdf

Annex- 1 List of Target UCs of NPGP Sr. No. Province/Region District Tehsil/Taluka/Sub-Division UC/Village 1 AJK HAVELI HAVELI BADHAL SHARIF 2 AJK HAVELI HAVELI SANGAL/SANGALI 3 AJK HAVELI HAVELI BHEDI KALALI 4 AJK HAVELI HAVELI CHANJAL 5 AJK HAVELI HAVELI DEGWAR/DEGWAR TIRWAN 6 AJK HAVELI HAVELI KALA MULA MILTARY AREA/MC HAVELI/KAHUTA 7 AJK HAVELI HAVELI (TOWNSHIP AREA) 8 AJK HAVELI HAVELI KHURSHIDABAD (KAILAR) 9 AJK HATTIAN HATTIAN LEEPA/NO KOT 10 AJK Cluster 1 HATTIAN HATTIAN BANA MULA 11 AJK HATTIAN HATTIAN CHIKAR/CHIKKAR DAHI 12 AJK HATTIAN HATTIAN SALMIA/SULMIAH 13 AJK HATTIAN HATTIAN CHAKHAMA 14 AJK HATTIAN HATTIAN CHINARI/SARAK CHINARI 15 AJK HATTIAN HATTIAN GUJAR BANDI 16 AJK HATTIAN HATTIAN HATTIAN BALA 17 AJK HATTIAN HATTIAN KHALANA 18 AJK HATTIAN HATTIAN LAMNIAN 19 AJK HATTIAN HATTIAN LANGLA 20 AJK HATTIAN HATTIAN SENA DAMAN 21 BALOCHISTAN JHAL MAGSI GANDAWA SUB-DIVISION GANDAWA 22 BALOCHISTAN JHAL MAGSI GANDAWA SUB-DIVISION KHARI 23 BALOCHISTAN JHAL MAGSI GANDAWA SUB-DIVISION MIRPUR 24 BALOCHISTAN JHAL MAGSI GANDAWA SUB-DIVISION PATRI 25 BALOCHISTAN JHAL MAGSI JHAL MAGSI SUB-DIVISION BARIJA 26 BALOCHISTAN JHAL MAGSI JHAL MAGSI SUB-DIVISION HATHYARI 27 BALOCHISTAN JHAL MAGSI JHAL MAGSI SUB-DIVISION JHAL MAGSI 28 BALOCHISTAN JHAL MAGSI JHAL MAGSI SUB-DIVISION KOT MAGSI 29 BALOCHISTAN JHAL MAGSI JHAL MAGSI SUB-DIVISION PANJUK 30 BALOCHISTAN ZHOB KAKAR KHURASAN SUB-DIVISION QAMAR DIN KAREZ 31 BALOCHISTAN ZHOB KAKAR KHURASAN SUB-DIVISION SHAGHALU/SHEGHALO 32 BALOCHISTAN ZHOB ZHOB SUB-DIVISION BABU MUHALLAH 33 BALOCHISTAN ZHOB -

PUNJAB Sheet 12 of 31

D.G KHAN AND MUZAFFARGARH DISTRICTS. PUNJAB Sheet 12 of 31 3000000 3005000 Basti Qa3d0ir1 B0a0k0h0sh Kacchi Katria G 3015000 3020000 3025000 3030000 M C Tahliwala Nurangwala Khu A Tamachewala A G N G Basti Syiadan A L I Mohd Kot M_Indus 3 Ranuja Chirhoiwala Basti Churewala Gharibabad ± Sojhalwali Manzurwala Rh(canal) Kaiskalwala Lohanawala Majranwala Daulatwala Pir Adil Samarwala Deulatabad Basti Muhammad Yar Mochiwala Shahbazwala Basti Basti Ali Lal Khan Pakka Khu Pir Haji Sahib Muhammad Asad Khan 0 Dhinga Qaimwala 0 0 Dholpur 0 0 0 0 0 6 Bakht Baland Dargah 6 6 Gulabwala Khu 6 Veterinary HaspitalGujrat Basti Ari Buzdarwala Meranwala Chhajrewala Nawan Sial Chak Bodla Basti GhariyaliBasti Rahbaranwala R Ari Kaheriwali O L Kalu Arainwala - Dongawala N 1 I Nunwala Ghoriwala M Tarkhanwala M_Indus 4 Wadwali Basti Brahuiwala Pattuwala Hukam Chandawala P De Shah Basti Maulviwala IP Water Levels for 5 yr = 124.05 m, 50 yr = 124.68 m ( X-Sec:4_IN_080 ) Tibbi Isran L Aria Smaj A Chah Districtwala N D Majhawala H A IS C Basti Pirwala T G Basti Angri N Y Basti Zaur A R N Hazratwala I Mashuriwali O R Basti Golwala I D N B B I Jalwala B Mahmudwala Chah Dorattawala M Basti Karakwala A Mohanewala H D Basti Ranjha A D Basti AwanwalaMochiwala Sarwarwala . Baghwala H A Chanwala H Khajjiwala S Lasuri L K Haji Shah Almani T Bewlewala Khu I O A K H S Laghariwala Basti Bhatti Sidlwali Jamalwala Ali Shahwali Basti Chan Nawan Basti Kundarwali Basti Angra Oamin Chhabri Zerin Lohar Jatoiwala Bahadurwala D . -

Dera Ghazi Khan

Overview - Dera Ghazi Khan Zhob Basti ! ! Sheerani Khanu !! Khanu Dera Khel Khel ! Jhok Haibatwali Jhok Mitthewali ! Ismail Jhok Mithuwali ! ! Jhok Jhok Atrewali Jhok Machandi ! Hotwali Legend ! Ahmad Angu Jhok Jhok Wajan ! Jhok ! ! Jhok ! ! Jhok Nur Muhammadwali Khan Baghewali Nangera Jhok Nur Muhammad Ahmad Angu Jhok ! ! ! ! Khanwali Jhok Hamzewali Jhok Jadewali Jhok Muradwali Jhok Hajiwali Basti Jhok Qamwala Kanewali Karenwali ! Jhok Musa Ghalhu Basti Mian Juma Jhok ! ! Sharqi Jhok Jarwar ! Jhok Qaimwala ! ! Haidarwali ! Jhok Shakirwali Triman ! Tarmin ! ! ! ! Bukhara !^ Shadiwala Jhok Kakrenwala Shakirwali Taramman Bhakkar Chuni ! Jhok Jhok ! ! Basti Langra National Fr D.i.khan Jhok Jhok Nasirwali ! Rustamani ! Rustamwali Raghnewali Basti Hasuwali ! Kiri Pathan Nasir Daulatwala ! Jhok Rahiwali ! ! Jhok Ganjewali Jhok Kaluwala Dawlatwala ! ! ! ! ! Lakhani Bhuch Gulanwali ! Jhok Bakhro ! Jhok Kaluwali Jhok Bakhrowali Jhok Hajuwali ! Kot Jhok MewewaliJhok Mitthe Khan ! Mubarak Mawewali ! ! Taunsa Jhok Mithewali !! ! Lishari Jhok Mahpal ! Jhok Gaman Jhok Gamanwali ! Jhok ! Basti Province Tehsil Lushari ! Mapal Basti Kharan Lashari Jhok Mitthewali Basti Marani Dagarwali ! Basti ! Buzdar ! Dhangar Gadi ! Basti Chand Basti Gadi ! Mithewali Shimali Azizwala JalluwaliJalluwali ! ! ! ! ! Buzdar Basti Mandal Jhok Amra ! Kotani Nadar Badar Jallowali Murra Laghari BastiMandal Basti ! ! Naddar Baddar ! Basti Shah !! ! Jhok Gat ! Jhok Gattenwali Shah di ! Kuhar Basti District Jhok Dullewali Jhok Kohar ! Churkin ! !Sikandarabad Basti Balwanian ! -

Dera Ghazi Khan

NSTITUTE OF NFORMATION ECHNOLOGY COMSATS I I T Dera Ghazi Khan Pervaiz Kareem 2012 FA11- BS( ECE ) - 024 State: Community of person more or less numerous occupying a definite portion of area, posses an organized sovereign government, to unhide a great number of people renders habitual obedience. It has four pillars. 1-legislatives. 2-Exective. 3-Judiciary. 4-Media. Province: The English word "province" is attested since about 1330 and derives from the 13th-century Old French "province," which itself comes from the Latin word "provincia," which referred to the sphere of authority of a magistrate; in particular, to a foreign territory. In geology, the term "province" refers to a specific physiogeographic area that comprises a grouping of like bathymetric or former bathymetric elements. In many countries, a province is a relatively small non-constituent level of sub-national government. (Wikipedia). Division: Divisions are the third tier of government in Pakistan, between the provinces and districts. They were abolished in 2000 by the government of former president Pervez Musharraf to make way for local governance via district governments. As of August 2008, divisions in some provinces have been restored with Punjab taking the lead and restoring its eight divisions. The four provinces of Pakistan are subdivided into administrative "divisions", which are further subdivided into districts and tehsils. The divisions do not include the Islamabad Capital Territory or the Federally Administered Tribal Areas, which are counted at the same level as provinces.(Wikipedia). District: are the ( ا ض ﻻع پ اک س تان :The Districts of Pakistan (Urdu second order administrative divisions of Pakistan. -

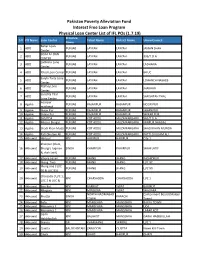

Physical Loan Center List of IFL Pos (1.7.19)

Pakistan Poverty Alleviation Fund Interest Free Loan Program Physical Loan Center List of IFL POs (1.7.19) Province S # PO Name Loan Center Tehsil Name District Name Union Council Name Bahar Loan 1 ADO PUNJAB LAYYAH LAYYAH JAMAN SHAH Center SOJHLA LOAN 2 ADO PUNJAB LAYYAH LAYYAH 306/T.D.A CENTER Ladhana Lone 3 ADO PUNJAB LAYYAH LAYYAH LADHANA Center 4 ADO Ithad Loan Center PUNJAB LAYYAH LAYYAH 64 UC Sanjhi Tarqi Lone 5 ADO PUNJAB LAYYAH LAYYAH LOHANCH NASHEB Center Ittefaq Lone 6 ADO PUNJAB LAYYAH LAYYAH JHAKHAR Center Sarishta Thal 7 ADO PUNJAB LAYYAH LAYYAH SARISHTAH THAL Lone Center noorpur 8 Agahe PUNJAB RAJANPUR RAJANPUR NOOR PUR machiwal 9 Agahe Jhaan Pur PUNJAB RAJANPUR RAJANPUR JAHANPUR 10 Agahe Shikar Pur PUNJAB RAJANPUR RAJANPUR SHIKAR PUR 11 Agahe 565/TDA PUNJAB KOT ADDU MUZAFFARGARH 565/T.D.A 12 Agahe Mirpur Bhagal PUNJAB KOT ADDU MUZAFFARGARH MIRPUR BHAGAL 13 Agahe Shadi Khan Muda PUNJAB KOT ADDU MUZAFFARGARH SHADI KHAN MUNDA 14 Agahe Pati Ghulam Ali PUNJAB KOT ADDU MUZAFFARGARH PATTI GHULAM ALI 15 Akhuwat Haripur KPK HARIPUR HARIPUR City 1 khairpur (Jilani, 16 Akhuwat Bhurgri, luqman SINDH KHAIRPUR KHAIRPUR SHAH LATIF & shah latif) 17 Akhuwat athara hazari PUNJAB JHANG JHANG RASHIDPUR 18 Akhuwat Jhang Two PUNJAB JHANG JHANG U/C 97 Jhung one ( U/C 19 Akhuwat PUNJAB JHANG JHANG U/C 90 90 & U/C 91) Charsada ( U/C 1, 20 Akhuwat KPK CHARSADDA CHARSADDA U/C 1 U/C 2 & U/C 3) 21 Akhuwat Bari Kot KPK BARIKOT SWAT BARIKOT 22 Akhuwat Mingora KPK MINGORA SWAT SHADARA NORTH NAZIMABAD Cantonment Board (Maleer 23 Akhuwat Bhattai SINDH -

List of Eligible Candidates for the Post of Attendant

LIST OF ELIGIBLE CANDIDATES FOR THE POST OF ATTENDANT Sr. Application Name Father Name Residence DOMICILE No. No. 1 2 M.Dilshad Hussain Wajid Hussain Basti Bandwali P/O Mamori Dera Ghazi Khan D.G.Khan 2 11 Sadeeq Ahmmd Allah Bukhsh Chaa Gorstani choti zarin DG khan D.G.Khan 3 12 M.Abdull Jabbar M. Umir Block #25 mahalla greeb abbad makan #240 DG khan D.G.Khan 4 23 Farhan Talib Talib Hussain Aamir Book Deppo, B#6, DGKhan D.G.Khan 5 38 Imtaiz Ahmad M.Ramzan Allah bad Colony D G Khan D.G.Khan 6 70 Wasim Ishfaq Muhammad Ishfaq Block 46 DG khan D.G.Khan 7 76 Zeeshan Kareem Ashiq Hussain Blockno. 46 Bata kaloni DG khan D.G.Khan 8 77 Muhammad Irfan Ghulam Sarwar Basti Daod por kala DG khan D.G.Khan 9 79 Ammanullah Muhammad Bakhsh Aaq kaloni chok chortta D.G.Khan 10 92 Muhammad Adnan Muhammad Bakhsh Makan no 3 Block 42 DG khan D.G.Khan 11 93 Muhammad Hussain Hafiz Muhammad Shafiq Skhmani kaloni makan no 160 DG khan D.G.Khan 12 99 Muhammad Ayub Khuda bakhsh moza basti Cha Bahador wala Dakhana basti china jam poor rajn D.G.Khan poor Sha wala Jaker Imam Sha Mal Bloch ,U, near Hadiree Imam 103 Muhammad Ameen Fateh Muhammad D.G.Khan 13 Bargha DG khan 14 105 Mukhtyar Hussain Khadim Hussain House no 100 Mahala D.G.Khan 15 121 Muhammad Nazim Abdull Hameed Chowk Rori p/o chti bala kot chota Dg khan D.G.Khan 16 130 Khuram Shahzad Abdull Majeed Chabree zareen Basti dhorpur pir adil Dg khan D.G.Khan 17 141 Muhammad Imran Rafique Muhammad Rafique Abdullah Town Dera Ghazi Khan D.G.Khan 18 143 Wasim Anjum Nazeer Ahmad House No. -

SCI Pak Livelihood Baseline Report

Livelihood Baseline Report Acknowledgements Funding for the Livelihoods Baseline Project was provided by Save the Children UK. The assessment was done by Save the Children Staff, Sadia Khan, Sumera Yasmin, Muhammad Adnan Khan, Shahzad Mukhtar, Umar Farooq, Sohail Ahmed, Sajid Khan and Ruhul Amin. Technical lead and guidance of the assessment was provided by Daison Ngirazi. The assessment team wishes to thank the various stakeholders that made this work possible, special mention goes to community members who afforded their valuable time to speak to the assessment team. 2 Table of Contents List of Figures .......................................................................................................................................... 5 List of Tables ........................................................................................................................................... 5 1 SUMMARY ...................................................................................................................................... 6 1.1 Objectives of the Study ............................................................................................................ 6 1.2 Methodology ........................................................................................................................... 6 1.3 Results ..................................................................................................................................... 6 2 Introduction ...................................................................................................................................