ECON2001 Microeconomics Lecture Notes Budget Constraint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Quasilinear Approximations

Quasilinear approximations Marek Weretka ∗ August 2, 2018 Abstract This paper demonstrates that the canonical stochastic infinite horizon framework from both the macro and finance literature, with sufficiently patient consumers, is in- distinguishable in ordinal terms from a simple quasilinear economy. In particular, with a discount factor approaching one, the framework converges to a quasilinear limit in its preferences, allocation, prices, and ordinal welfare. Consequently, income effects associated with economic policies vanish, and equivalent and compensating variations coincide and become approximately additive for a set of temporary policies. This ordi- nal convergence holds for a large class of potentially heterogenous preferences that are in Gorman polar form. The paper thus formalizes the Marshallian conjecture, whereby quasilinear approximation is justified in those settings in which agents consume many commodities (here, referring to consumption in many periods), and unifies the general and partial equilibrium schools of thought that were previously seen as distinct. We also provide a consumption-based foundation for normative analysis based on social surplus. Key words: JEL classification numbers: D43, D53, G11, G12, L13 1 Introduction One of the most prevalent premises in economics is the ongoing notion that consumers be- have rationally. The types of rational preferences studied in the literature, however, vary considerably across many fields. The macro, financial and labor literature typically adopt consumption-based preferences within a general equilibrium framework, while in Industrial Organization, Auction Theory, Public Finance and other fields, the partial equilibrium ap- proach using quasilinear preferences is much more popular. ∗University of Wisconsin-Madison, Department of Economics, 1180 Observatory Drive, Madison, WI 53706. -

The Soft Budget Constraint

Acta Oeconomica, Vol. 64 (S1) pp. 25–79 (2014) DOI: 10.1556/AOecon.64.2014.S1.2 THE SOFT BUDGET CONSTRAINT An Introductory Study to Volume IV of the Life’s Work Series* János KORNAI** The author’s ideas on the soft budget constraint (SBC) were first expressed in 1976. Much progress has been made in understanding the problem over the ensuing four decades. The study takes issue with those who confine the concept to the process of bailing out loss-making socialist firms. It shows how the syndrome can appear in various organizations and forms in many spheres of the economy and points to the various means available for financial rescue. Single bailouts do not as such gener- ate the SBC syndrome. It develops where the SBC becomes built into expectations. Special heed is paid to features generated by the syndrome in rescuer and rescuee organizations. The study reports on the spread of the syndrome in various periods of the socialist and the capitalist system, in various sectors. The author expresses his views on normative questions and on therapies against the harmful effects. He deals first with actual practice, then places the theory of the SBC in the sphere of ideas and models, showing how it relates to other theoretical trends, including institutional and behav- ioural economics and theories of moral hazard and inconsistency in time. He shows how far the in- tellectual apparatus of the SBC has spread in theoretical literature and where it has reached in the process of “canonization” by the economics profession. Finally, he reviews the main research tasks ahead. -

Lecture 4 " Theory of Choice and Individual Demand

Lecture 4 - Theory of Choice and Individual Demand David Autor 14.03 Fall 2004 Agenda 1. Utility maximization 2. Indirect Utility function 3. Application: Gift giving –Waldfogel paper 4. Expenditure function 5. Relationship between Expenditure function and Indirect utility function 6. Demand functions 7. Application: Food stamps –Whitmore paper 8. Income and substitution e¤ects 9. Normal and inferior goods 10. Compensated and uncompensated demand (Hicksian, Marshallian) 11. Application: Gi¤en goods –Jensen and Miller paper Roadmap: 1 Axioms of consumer preference Primal Dual Max U(x,y) Min pxx+ pyy s.t. pxx+ pyy < I s.t. U(x,y) > U Indirect Utility function Expenditure function E*= E(p , p , U) U*= V(px, py, I) x y Marshallian demand Hicksian demand X = d (p , p , I) = x x y X = hx(px, py, U) = (by Roy’s identity) (by Shepard’s lemma) ¶V / ¶p ¶ E - x - ¶V / ¶I Slutsky equation ¶p x 1 Theory of consumer choice 1.1 Utility maximization subject to budget constraint Ingredients: Utility function (preferences) Budget constraint Price vector Consumer’sproblem Maximize utility subjet to budget constraint Characteristics of solution: Budget exhaustion (non-satiation) For most solutions: psychic tradeo¤ = monetary payo¤ Psychic tradeo¤ is MRS Monetary tradeo¤ is the price ratio 2 From a visual point of view utility maximization corresponds to the following point: (Note that the slope of the budget set is equal to px ) py Graph 35 y IC3 IC2 IC1 B C A D x What’swrong with some of these points? We can see that A P B, A I D, C P A. -

Preview Guide

ContentsNOT FOR SALE Preface xiii CHAPTER 3 The Behavior of Consumers 45 3.1 Tastes 45 CHAPTER 1 Indifference Curves 45 Supply, Demand, Marginal Values 48 and Equilibrium 1 More on Indifference Curves 53 1.1 Demand 1 3.2 The Budget Line and the Demand versus Quantity Consumer’s Choice 53 Demanded 1 The Budget Line 54 Demand Curves 2 The Consumer’s Choice 56 Changes in Demand 3 Market Demand 7 3.3 Applications of Indifference The Shape of the Demand Curve 7 Curves 59 The Wide Scope of Economics 10 Standards of Living 59 The Least Bad Tax 64 1.2 Supply 10 Summary 69 Supply versus Quantity Supplied 10 Author Commentary 69 1.3 Equilibrium 13 Review Questions 70 The Equilibrium Point 13 Numerical Exercises 70 Changes in the Equilibrium Point 15 Problem Set 71 Summary 23 Appendix to Chapter 3 77 Author Commentary 24 Cardinal Utility 77 Review Questions 25 The Consumer’s Optimum 79 Numerical Exercises 25 Problem Set 26 CHAPTER 4 Consumers in the Marketplace 81 CHAPTER 2 4.1 Changes in Income 81 Prices, Costs, and the Gains Changes in Income and Changes in the from Trade 31 Budget Line 81 Changes in Income and Changes in the 2.1 Prices 31 Optimum Point 82 Absolute versus Relative Prices 32 The Engel Curve 84 Some Applications 34 4.2 Changes in Price 85 2.2 Costs, Efficiency, and Gains from Changes in Price and Changes in the Trade 35 Budget Line 85 Costs and Efficiency 35 Changes in Price and Changes in the Optimum Point 86 Specialization and the Gains from Trade 37 The Demand Curve 88 Why People Trade 39 4.3 Income and Substitution Summary 41 -

Preference Conditions for Invertible Demand Functions

Preference Conditions for Invertible Demand Functions Theodoros Diasakos and Georgios Gerasimou School of Economics and Finance School of Economics and Finance Discussion Paper No. 1708 Online Discussion Paper Series 14 Mar 2017 (revised 23 Aug 2019) issn 2055-303X http://ideas.repec.org/s/san/wpecon.html JEL Classification: info: [email protected] Keywords: 1 / 31 Preference Conditions for Invertible Demand Functions∗ Theodoros M. Diasakos Georgios Gerasimou University of Stirling University of St Andrews August 23, 2019 Abstract It is frequently assumed in several domains of economics that demand functions are invertible in prices. At the primitive level of preferences, however, the characterization of such demand func- tions remains elusive. We identify conditions on a utility-maximizing consumer’s preferences that are necessary and sufficient for her demand function to be continuous and invertible in prices: strict convexity, strict monotonicity and differentiability in the sense of Rubinstein (2012). We show that preferences are Rubinstein-differentiable if and only if the corresponding indifference sets are smooth. As we demonstrate by example, these notions relax Debreu’s (1972) preference smoothness. ∗We are grateful to Hugo Sonnenschein and Phil Reny for very useful conversations and comments. Any errors are our own. 2 / 31 1 Introduction Invertibility of demand is frequently assumed in several domains of economic inquiry that include con- sumer and revealed preference theory (Afriat, 2014; Matzkin and Ricther, 1991; Chiappori and Rochet, 1987; Cheng, 1985), non-separable and non-parametric demand systems (Berry et al., 2013), portfolio choice (Kubler¨ and Polemarchakis, 2017), general equilibrium theory (Hildenbrand, 1994), industrial or- ganization (Amir et al., 2017), and the estimation of discrete or continuous demand systems. -

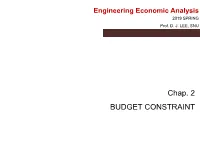

2. Budget Constraint.Pdf

Engineering Economic Analysis 2019 SPRING Prof. D. J. LEE, SNU Chap. 2 BUDGET CONSTRAINT Consumption Choice Sets . A consumption choice set, X, is the collection of all consumption choices available to the consumer. n X = R+ . A consumption bundle, x, containing x1 units of commodity 1, x2 units of commodity 2 and so on up to xn units of commodity n is denoted by the vector xx =(1 ,..., xn ) ∈ X n . Commodity price vector pp =(1 ,..., pn ) ∈R+ 1 Budget Constraints . Q: When is a bundle (x1, … , xn) affordable at prices p1, … , pn? • A: When p1x1 + … + pnxn ≤ m where m is the consumer’s (disposable) income. The consumer’s budget set is the set of all affordable bundles; B(p1, … , pn, m) = { (x1, … , xn) | x1 ≥ 0, … , xn ≥ 0 and p1x1 + … + pnxn ≤ m } . The budget constraint is the upper boundary of the budget set. p1x1 + … + pnxn = m 2 Budget Set and Constraint for Two Commodities x2 Budget constraint is m /p2 p1x1 + p2x2 = m. m /p1 x1 3 Budget Set and Constraint for Two Commodities x2 Budget constraint is m /p2 p1x1 + p2x2 = m. the collection of all affordable bundles. Budget p1x1 + p2x2 ≤ m. Set m /p1 x1 4 Budget Constraint for Three Commodities • If n = 3 x2 p1x1 + p2x2 + p3x3 = m m /p2 m /p3 x3 m /p1 x1 5 Budget Set for Three Commodities x 2 { (x1,x2,x3) | x1 ≥ 0, x2 ≥ 0, x3 ≥ 0 and m /p2 p1x1 + p2x2 + p3x3 ≤ m} m /p3 x3 m /p1 x1 6 Opportunity cost in Budget Constraints x2 p1x1 + p2x2 = m Slope is -p1/p2 a2 Opp. -

Decisions and Games

DECISIONS AND GAMES. PART I 1. Preference and choice 2. Demand theory 3. Uncertainty 4. Intertemporal decision making 5. Behavioral decision theory DECISIONS AND GAMES. PART II 6. Static Games of complete information 7. Dynamic games of complete information 8. Static games of incomplete information 9. Dynamic games of incomplete information 10. Behavioral game theory References Gibbons, R. 1992. Game theory for applied economists. Princeton University Press. Princeton, New Jersey. Varian, H.1992. Microeconomic analysis. Norton & Company. New York. Chapters 7, 8, 9, 10, 11, 19. Camerer, C. , Loewenstein, G. , and Rabin, M. 2004. Advances in Behavioral Economics. Princeton University Press. Mas-Colell, A., Whinston, M., and Green, J. 1995. Microeconomic theory. Oxford University Press. Chapters 1, 2, 3, 4, 6. 1 Two approaches to analyze behavior of decision makers. 1. From an abstract construction generate choices that satisfy rationality restrictions. 2. Directly from choice, ask for some structure to these choices and derive properties. Relation between the two approaches. 2 1. Preference and choice Consider a set of alternatives (mutually exclusives) X and we consider a preference relation on X. Preferences The preference relation “at least as good as” is a binary relation − over the set of alternatives X. Preferences express the ordering between alternatives resulting from the objectives of the decision maker. Properties: Rational Preference Relation (or Weak order, or Complete preorder) if -Completeness, Transitivity (and Reflexivity) A relation is complete if ∀∈x,,yXxy or yx. A relation is transitive if and only if ∀∈x,yz, X, if x≺≺y and y z, then x≺z. 3 Transitiveness is more delicate than completeness. -

3 Lecture 3: Choices from Budget Sets

3 Lecture 3: Choices from Budget Sets Up to now, we have been rather demanding about the data that we need in order to test our models. We have made two important assumptions: that we observe choices from all possible choice sets, and that we observe choice correspondences (i.e. we see all the options that a decision maker would be ‘happy with’). In many cases, we may not be so lucky with our data. Unfortunately, without these two properties, conditions and are no longer necessary or sufficient to guarantee a utility representation. Consider the following example of an incomplete data set. Example 1 Let = and say we observe the following (incomplete) choice correspondence { } ( )= { } { } ( )= { } { } ( )= { } { } This choice correspondence satisfies properties and trivially. is satisfied because we do not observe any choices from sets that are subsets of each other. is satisfied because we never see two objects chosen from the same set. However, there is no way that we can rationalize these choices with a complete preference relation. The first observation implies that ,thesecond  that and the third that 3. Thus, any binary relation that would rationalize these choices   would be intransitive. In fact, in order for theorem 1 to hold, we don’t have to observe choices from all subsets of , but we do have to need at least all subsets of that contain two and three elements (you should go back and look at the proof of theorem 1 and check that you agree with this statement). What about if we drop the assumption that we observe a choice correspondence, and instead observe a choice function? For example, we could ask the following question: Question 1 Let :2 ∅ be a choice function. -

EC9D3 Advanced Microeconomics, Part I: Lecture 2

EC9D3 Advanced Microeconomics, Part I: Lecture 2 Francesco Squintani August, 2020 Budget Set Up to now we focused on how to represent the consumer's preferences. We shall now consider the sour note of the constraint that is imposed on such preferences. Definition (Budget Set) The consumer's budget set is: B(p; m) = fx j (p x) ≤ m; x 2 X g Francesco Squintani EC9D3 Advanced Microeconomics, Part I August, 2020 2 / 49 Budget Set (2) 6 x1 2 L = 2 X = R+ c c c c c c c c c c c c B(p; m) c c c c c c c - x2 Francesco Squintani EC9D3 Advanced Microeconomics, Part I August, 2020 3 / 49 Income and Prices The two exogenous variables that characterize the consumer's budget set are: the level of income m the vector of prices p = (p1;:::; pL). Often the budget set is characterized by a level of income represented by the value of the consumer's endowment x0 (labour supply): m = (p x0) Francesco Squintani EC9D3 Advanced Microeconomics, Part I August, 2020 4 / 49 Utility Maximization The basic consumer's problem (with rational, continuous and monotonic preferences): max u(x) fxg s:t: x 2 B(p; m) Result If p > 0 and u(·) is continuous, then the utility maximization problem has a solution. Proof: If p > 0 (i.e. pl > 0, 8l = 1;:::; L) the budget set is compact (closed, bounded) hence by Weierstrass theorem the maximization of a continuous function on a compact set has a solution. Francesco Squintani EC9D3 Advanced Microeconomics, Part I August, 2020 5 / 49 First Order Condition Result If u(·) is continuously differentiable, the solution x∗ = x(p; m) to the consumer's problem is characterized by the following necessary conditions. -

A Macroeconomic Model with Financially Constrained Producers and Intermediaries ∗

A Macroeconomic Model with Financially Constrained Producers and Intermediaries ∗ Vadim Elenev Tim Landvoigt Stijn Van Nieuwerburgh NYU Stern UT Austin NYU Stern, NBER, and CEPR October 24, 2016 Abstract We propose a model that can simultaneously capture the sharp and persistent drop in macro-economic aggregates and the sharp change in credit spreads observed in the U.S. during the Great Recession. We use the model to evaluate the quantitative effects of macro-prudential policy. The model features borrower-entrepreneurs who produce output financed with long-term debt issued by financial intermediaries and their own equity. Intermediaries fund these loans combining deposits and their own equity. Savers provide funding to banks and to the government. Both entrepreneurs and intermediaries make optimal default decisions. The government issues debt to finance budget deficits and to pay for bank bailouts. Intermediaries are subject to a regulatory capital constraint. Financial recessions, triggered by low aggregate and dispersed idiosyncratic productivity shocks result in financial crises with elevated loan defaults and occasional intermediary insolvencies. Output, balance sheet, and price reactions are substantially more severe and persistent than in non-financial recession. Policies that limit intermediary leverage redistribute wealth from producers to intermediaries and savers. The benefits of lower intermediary leverage for financial and macro-economic stability are offset by the costs from more constrained firms who produce less output. JEL: G12, -

Soft Budget Constraint Theories from Centralization to the Market1

Economics of Transition Volume 9 (1) 2001, 1–27 Soft budget constraint theories From centralization to the market1 Eric Maskin* and Chenggang Xu** *Institute for Advanced Study, Princeton and Department of Economics, Princeton University. Institute for Advanced Study, Einstein Drive, Princeton, NJ 08540, USA. Tel: + 1 609-734- 8309; E-mail: [email protected] **Department of Economics and CEP, London School of Economics, London WC2A 2AE, UK. Tel: +44 (0)207 955 7526; E-mail: [email protected] Abstract This paper surveys the theoretical literature on the effect of soft budget constraints on economies in transition from centralization to capitalism; it also reviews our understanding of soft budget constraints in general. It focuses on the conception of the soft budget constraint syndrome as a commitment problem. We show that the two features of soft budget constraints in centralized economies – ex post renegotiation of firms’ financial plans and a close administrative relationship between firms and the centre – are intrinsically related. We examine a series of theories (based on the commitment-problem approach) that explain shortage, lack of innovation in centralized economies, devolution, and banking reform in transition economies. Moreover, we argue that soft budget constraints also have an influence on major issues in economics, such as the determination of the boundaries and capital structure of a firm. Finally, we show that soft budget constraints theory sheds light on financial crises and economic growth. JEL classification: D2, D8, G2, G3, H7, L2, O3, P2, P3. Keywords: soft budget constraint, renegotiation, theory of the firm, banking and finance, transition, centralized economy. -

Giffen Behaviour and Asymmetric Substitutability*

Tjalling C. Koopmans Research Institute Tjalling C. Koopmans Research Institute Utrecht School of Economics Utrecht University Janskerkhof 12 3512 BL Utrecht The Netherlands telephone +31 30 253 9800 fax +31 30 253 7373 website www.koopmansinstitute.uu.nl The Tjalling C. Koopmans Institute is the research institute and research school of Utrecht School of Economics. It was founded in 2003, and named after Professor Tjalling C. Koopmans, Dutch-born Nobel Prize laureate in economics of 1975. In the discussion papers series the Koopmans Institute publishes results of ongoing research for early dissemination of research results, and to enhance discussion with colleagues. Please send any comments and suggestions on the Koopmans institute, or this series to [email protected] ontwerp voorblad: WRIK Utrecht How to reach the authors Please direct all correspondence to the first author. Kris De Jaegher Utrecht University Utrecht School of Economics Janskerkhof 12 3512 BL Utrecht The Netherlands. E-mail: [email protected] This paper can be downloaded at: http:// www.uu.nl/rebo/economie/discussionpapers Utrecht School of Economics Tjalling C. Koopmans Research Institute Discussion Paper Series 10-16 Giffen Behaviour and Asymmetric * Substitutability Kris De Jaeghera aUtrecht School of Economics Utrecht University September 2010 Abstract Let a consumer consume two goods, and let good 1 be a Giffen good. Then a well- known necessary condition for such behaviour is that good 1 is an inferior good. This paper shows that an additional necessary for such behaviour is that good 1 is a gross substitute for good 2, and that good 2 is a gross complement to good 1 (strong asymmetric gross substitutability).