INSITE ��Acres India’S No.1 Property Portal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prabhavathi Elegant

https://www.propertywala.com/prabhavathi-elegant-bangalore Prabhavathi Elegant - Whitefield, Bangalore Apartment for sale in White field 1, 2, 3 BHK near ashram road Prabhavathi Elegant is luxurious project of Prabhavathi Developers, offering you 1/2/3 BHK Residential apartments and located at Whitefield, Bangalore. Project ID : J781190017 Builder: Prabhavathi Properties: Apartments / Flats, Independent Houses Location: Prabhavathi Elegant,Kadugodi, Whitefield, Bangalore - 560037 (Karnataka) Completion Date: Jan, 2015 Status: Started Description Prabhavathi Elegant is available on peaceful, posh, and pollution free surrounding of Whitefield, Bangalore. It offers you 1/2/3 BHK Residential apartments with all aspect modern amenities features like well-equipped gym, covered car parking, automatic lift, swimming pool etc. The project having 60% of the total land as open space, this open space will provide you fresher air to the residents. Many significant area and prime location is very close to from the project where you can easily access the city for your daily needs. Type - 1/2/3 BHK Apartments Sizes - 970 - 1200 Sq. Ft. Price - On Request Amenities Automatic Lift Swimming Pool Party Hall Covered Car Parking Well Equipped Gym Prabhavathi Builders and Developers Pvt. Ltd. made its debut in 2007 under the leadership of Mr. BE Praveen Kumar, who is founder of Managing director. I have proud in announcing that we are today one of the fastest growing realtors in Bangalore with our primary focused being on Residential apartments. We have been credited with over 25 completed projects in Bangalore, Prabhavathi Bliss I, Prabhavathi Plasma, Prabhavathi Rishab, Prabhavathi Woods, Prabhavathi Meridian are a few names which are now given possession to its buyer. -

Venue Details 12Th Step Corporation

Venue Details Venue Details Venue Details 12th Step - BEL Group - Ever Growing - Corporation Sports Club 95352 67966, 080 22340444 BEL Fine Arts Complex 90352 15403, 99800 50798 SFS School, Near Vimalaya Hospital 99452 63934, 99869 78686 4th Square - Jalahalli Eng, Kan, Tam Hosur Main Road - Austin Town Sun 10.00 am, Mon 10.00 am Bangalore 560 013 Mon 7.00 pm, Tue 7.00 pm, Thu Huskar Gate Stop Tue 7.00 pm, Fri 7.00 pm Acceptance - 7.00 pm, Fri 7.00 pm, Sun 11:00 Electronic City Nammura Sarkari Madari Pratamika Shale 90367 33061, 90352 15403 am Evergreen Prabhakar Jalahalli Village - Bembala - Taluk Office Compound 9344865860 Bangalore 560 013 Sat 7.00 pm Dr.Ambedkar Sena Samithi 70933 63621, 98863 70082 Hosur Kan, Tam Action - Near K.R.Puram Railway Station - Mon 7.00 pm CSI Church, CSI Colony, Kothnur Post 81974 88144, 78997 04143 Vijinapura Tue 7.00 pm, Sat 7.00 pm First Step - Kothnur - Carmel Convent Elumalai St Francis School, Opp. Krupanidhi 99869 78686, 080 22340444 Bangalore 560077 Thu 7.00 pm, Sat 11.00 am Near Sagar Apollo Hospital 81236 18438 College Eng Adaikalam - Tilak Nagar Kan, Tam Sarjapur Road Fri 7.00 pm Government School 95352 67966, 080 22340444 Jayanagar Mon, Fri, Sat 7.00pm Koramangala Near Anjaneya Temple And Passport - Chandrodaya - Fourth Dimension - Office Mon 7.00 pm, Wed 7.00 p.m, Fri Chandra High School 82962 88230, 080 2234 0444 Jyothi School 89044 17280, 080 22340444 Koramangala 7.00 pm, Sat 7.00 pm Prakash Nagar Kan, Tam Hennur Bagalur Main Road - Anbillam - Rajajinagar Mon 7.00 pm, Sat 7.00 pm, Sun Lingarajapuram Mon 6.30 pm, Wed 6.30 pm, Gospel Street 89044 17280, 88615 73981 7.00 pm Thu 6.30 pm, Sat 6.30 pm, Sun Old Bagalur Layout Kan, Tam Chetana - 6.30 pm Lingarajpuram Mon 7.00 pm, Thu 7.00 pm St. -

Feel Centered Located Just 3 Kms from Indiranagar

C.V. Raman Nagar Feel Centered Located just 3 Kms from Indiranagar. Large premium homes Centrally located homes give you more time in life. Work close by, shop close by, entertain close by. Welcome to Purva Season. At a mere 3 kms from Indiranagar, this project is next door to the overwhelmingly green DRDO Township and Center for Articial Intelligence. Special features: * 1, 2 and 3 bhk premium apartments set in a elite neighbourhood of 660 residents. * A 22,000 sft. , 7-star clubhouse with all the modern amenities. * Project set on 10.35 acres of pristine greenery. * Very close to city’s shopping hubs, entertainment zones and schools. Location Map Google Byappanhalli Big Bazaar Metro Station NGEF & Robotics adras Road DRDO Defence Avionics Old M Township Research Establishment N R e I i ndiranagar 80 Ft. Road l D l g i a o i r n m i s W c e i 100 Ft. Road a n I ndirangar F y t o C.V. Raman Nagar r ’ s o HAL Air e Bus Stop s P h i z z a por Tech Park t CMH Road Tippasandra Main Road CMH BEML Gate METRO LINE NPS HAL Hospital New Horizon School Jeevan Bhimanagar Hotel Thomson HAL Market Leela Palace Reuters & Oracle HAL Airport Road Way to Marathahalli T o Koramangala Manipal Royal Hospital Orchid Hotel Map not to scale Dell KGA Golf Course Proximity to Purva Season Indiranagar - 3 Kms M.G. Road, Trinity Circle - 6 Kms Byappanahalli Metro Station - 3 Kms C.V. Raman Nagar Tech Park - 1.5 Kms International Airport - 38 Kms ITPL - 8 Kms Central Railway Station - 12 Kms HAL - 3 Kms K.R. -

Ward Number Ward Name Zone Assembly

Ward Number Ward Name Zone Assembly Constituency Covid Zone Containment Zone 135 Padarayanapura West Chamajpet Red Yes 189 Hongasandra Bommanahalli Bommanahalli Red Yes 93 Vasanth Nagar East Shivajinagar Orange Yes 133 Hampinagara South Vijayanagar Orange Yes 134 Bapuji Nagar South Vijayanagar Orange Yes 136 Jagajivanram Nagar West Chamajpet Orange Yes 139 K R Market West Chamajpet Orange Yes 158 Deepanjali Nagara South Vijayanagar Orange Yes 177 J P Nagar South Jayanagar Orange Yes 140 Chamajpet South Chamajpet Orange No 172 Madivala South B.T.M Layout Orange No 25 Horamavu Mahadevapura K.R.Puram Yellow Yes 37 Yeshwanthpura RR Nagar Rajarajeswarinagar Yellow Yes 59 Maruthi Seva Nagar East Sarvagnanagar Yellow Yes 62 Ramaswamy Palya East Shivajinagar Yellow Yes 118 Sudham Nagar West Chikpet Yellow Yes 160 Rajarajeshwari Nagar RR Nagar Rajarajeswarinagar Yellow Yes 171 Gurappanapalya South Jayanagar Yellow Yes 179 Shakambari Nagar South Jayanagar Yellow Yes 19 Sanjay Nagar East Hebbal Yellow No 31 Kushal Nagar East Pulakeshinagar Yellow No 119 Dharmaraya Swamy te South Chamajpet Yellow No 129 Jnana Bharathi RR Nagar Rajarajeswarinagar Yellow No 145 Hombegowda Nagar South Chikpet Yellow No 170 Jayanagar East South Jayanagar Yellow No 0 18 Radhakrishna Temple East Hebbal Green Yes 78 Pulikeshi Nagar East Pulakeshinagar Green Yes 84 Hagadur Mahadevapura Mahadevpura Green Yes 124 Hosahalli South Vijayanagar Green Yes 138 Balavadhinagar West Chamrajpet Green Yes 166 Karisandra South Padmanabhanagar Green Yes 169 Byrasandra South Jayanagar Green -

Alumni Association of MS Ramaiah University of Applied Sciences

Alumni Association of M.S. Ramaiah University of Applied Sciences (SAMPARK), Bangalore M.S. Ramaiah University of Applied Sciences Department of Automotive & Aeronautical Engineering Program Year of Name Contact Address Photograph E-mail & Mobile Sl NO Completed Admiss ion # 25 Biligiri, 13th cross, 10th A Main, 2nd M T Layout, [email protected] M. Sc. (Automotive 574 2013 Pramod M Malleshwaram, Bangalore- 9916040325 Engineering) 560003 S/o L. Srinivas Rao, Sai [email protected] Dham, D-No -B-43, Near M. Sc. (Automotive m 573 2013 Lanka Vinay Rao Torwapool, Bilaspur (C.G)- Engineering) 9424148279 495001 9406114609 3-17-16, Ravikunj, Parwana Nagar, [email protected] Upendra M. Sc. (Automotive Khandeshwari road, Bank m 572 2013 Padmakar Engineering) colony, 7411330707 Kulkarni Dist - BEED, State – 8149705281 Maharastra No.33, 9th Cross street, Dr. Radha Krishna Nagar, [email protected] M. Sc. (Automotive Venkata Krishna Teachers colony, 571 2013 0413-2292660 Engineering) S Moolakulam, Puducherry-605010 # 134, 1st Main, Ist A cross central Excise Layout [email protected] M. Sc. (Automotive Bhoopasandra RMV Iind 570 2013 Anudeep K N om Engineering) stage, 9686183918 Bengaluru-560094 58/F, 60/2,Municipal BLDG, G. D> Ambekar RD. Parel [email protected] M. Sc. (Automotive Tekavde Nitin 569 2013 Bhoiwada Mumbai, om Engineering) Shivaji Maharashtra-400012 9821184489 Thiyyakkandiyil (H), [email protected] M. Sc. (Automotive Nanminda (P.O), Kozhikode / 568 2013 Sreedeep T K m Engineering) Kerala – 673613 4952855366 #108/1, 9th Cross, themightyone.lohith@ M. Sc. (Automotive Lakshmipuram, Halasuru, 567 2013 Lohith N gmail.com Engineering) Bangalore-560008 9008022712 / 23712 5-8-128, K P Reddy Estates,Flat No.A4, indu.vanamala@gmail. -

Godrej United Whitefield-Flipchart Revised 29-06-2018 Copy

GODREJ UNITED WHITEFIELD, BANGALORE RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in PRESENTING GODREJ PROPERTIES' MOST PREMIUM PROJECT IN EAST BANGALORE Artist’s impression. Not an actual site photograph. RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in WELL-CONNECTED LOCATION RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in AN ADDRESS WHERE NOTHING IS TOO FAR FROM HOME The Brigade Phoenix School V.R. Mall Marketcity Decathlon KR Puram Xylem Bridge Tech RMZ Infinity Park GODREJ Baiyappanahalli Metro & Railway Gopalan UNITED Station Grand Mall Metro Cash Bhoruka Gopalan & Carry Tech Park Prestige Shantiniketan Signature Mall Hoodi Planned Brigade Metropolis Garudacharpalya Swami Vivekananda Road Metro Station HAL Engine Division The Zuri MAHADEVAPURA Gopalan Ascendas Park Hoodi Main Road C.V. Raman National School Square Mall Taj Vivanta Nagar Euro School EMC Corporation Whitefield International Technology Soulspace Park Arena Mall Bagmane Shailendra Tech Park Keys Hotel Tech Park Sri Sathya Sai Institute Doddanekundi of Medical Sciences Bagmane Lake Lake RMZ NXT SAP Labs Neil Rao Inorbit Mall Towers Landmark Hospital INDIRANAGAR Rainbow EPIP ZONE Vydehi Institute Children’s of Nursing Hospital Sciences School/College BROOKEFIELD Hotel Mall CMRIT Brookefields Hospital MARATHAHALLI Tech Park/Corporate 100-Feet Road 100-Feet KUNDALAHALLI Metro Railway HAL Heritage Centre N Domlur Flyover & Aerospace Museum Bridge Lake W E HAL Old Airport Road Embassy Flyover S Golf Link Source: http://www.english.bmrc.co.in/FileUploads/phase2forweb.pdf | Google Maps. Map not to scale. -

Alembic Urban Forest - Kadugodi, Bangalore Spacious and Ventilated Apartments

https://www.propertywala.com/alembic-urban-forest-bangalore Alembic Urban Forest - Kadugodi, Bangalore Spacious and ventilated apartments. Alembic Urban Forest is presented by Alembic Real Estate at Kadugodi , Bangalore offers residential project that hosts 2 and 3 BHK apartment with good features Project ID: J594611895 Builder: Alembic Real Estate Location: Alembic Urban Forest, Kadugodi, Bangalore (Karnataka) Completion Date: Jul, 2018 Status: Completed Description Alembics Urban Forest at Kadugodi, Bangalore. The project spread over 1314 - 1890 sq.ft. comprising 2 a n d 3 bhk apartments.It holds the reputation of exhibiting quality and technologically complex infrastructure of international standards, and that has been well justified through the design of The Urban Forest.Located in the IT center of Bangalore. The Urban Forest provides the convenience of being just a short distance from work places, schools, malls, and hospitals. Whitfield has an excellent connectivity with several key areas of Bangalore through a network of roads. Located in one of the most ideal locations of Bangalore. RERA No : PRM/KA/RERA/1251/446/PR/171031/001137 Amenities: Gymnasium Swimming pool Clubhouse Jogging Track Children’s Play Area Basket Ball Court Security Personal Badminton Court Cafeteria Meditation Hall CCTV Camera Basement Car Parking Party Area Rainwater Harvesting Alembic Real Estate is the brainchild of 108-year old Alembic Group of Companies that has diversified itself into various businesses, including pharmaceuticals, healthcare and engineering. With an experience of having developed over 10 million sq ft of land and more than two million sq ft of built-in space, Alembic Real Estate is one of the most sought-after real estate developers in Gujarat. -

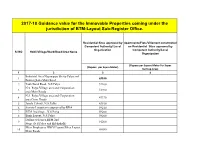

BTM-Layout Sub-Register Office

2017-18 Guidance value for the Immovable Properties coming under the jurisdiction of BTM-Layout Sub-Register Office. Residential Sites approved by Apartments/Flats/Villament constructed Competent Authority/ Local on Residential Sites approved by Organization Competent Authority/Local SI NO Hobli/Village/Ward/Road/Area Name Organization (Rupees per Square Meter For Super (Rupees per Squre Meter) Built up Area) 1 2 3 4 Industrial Area Nayanappa Shetty Palya and 1 65100 Bannerghatta Main Road 2 Tank Bund Road, N.S.Palya 52100 N.S. Palya Village area and Corporation 3 53290 area Main Roads N.S. Palya Village area and Corporation 4 47370 area Cross Roads 5 Janata Colony, N.S.Palya 43810 6 Society Layout area approved by BDA 59210 7 BTM 2nd Stage , N.S.Palya 59200 8 Bank Layout, N.S.Palya 59200 Dollars Schemes,BTM 2nd 9 91200 Stage (N.S.Palya and Bilekahalli) Mico Employees HBCS Layout/Mico Layout 10 68680 Main Roads Mico Employees HBCS Layout/Mico Layout 11 62170 Cross Roads 16th Main Road, Metropolitan, HBCS Layout 12 to 100 ft Ring Road (Mico Layout, BTM 2nd 87030 stage) 16th Main Road ( EWS Schemes to 13 Mahadeshwara Layout, N S Palya, Tankbund 62170 60 ft Road) 14 Mahadeshwara Layout Main Roads 49730 15 Mahadeshwara Layout Cross Roads. 43810 16 bharath house building co-operative society 59200 17 Abbayappa Layout, N S Palya, Main Roads 46180 18 Abbayappa Layout, N S Palya, cross Roads 37890 19 Reva Paradise 44800 20 Anand Apartment 44800 21 Tirumala Splendor 44800 22 Cholarenkil Lake view apartment 37100 23 Dream Sarovar apartment 37100 -

INSITE REPORT Bangalore

99acres India’s No.1 Property Portal INSITE REPORT Bangalore January - March 2018 www.99acres.com 99acres 99acres 2 INSITE : BANGALORE India’s No.1 Property Portal India’s No.1 Property Portal INSITE : BANGALORE 3 Methodology FOREW0RD The Insite Report by 99acres.com captures the quarterly capital trends and the annual rental analysis of residential apartments in key The first quarter of 2018 countersigned a revival in market real estate markets – Delhi sentiment and enquiries, amid a modest impact on overall sales NCR, Mumbai Metropolitan volume across metros. Supply in the ready residential segment Region (MMR), Bangalore, outstripped demand, particularly in case of luxury and ultra- Pune, Chennai, Hyderabad, luxury units. The under-construction market, too, narrated a Kolkata and Ahmedabad. In similar tale putting a downward pressure on average weighted order to assess the prevailing capital ‘asks’. With new launches down by around 40 percent, sentiment, the report delves YoY, any improvement in property prices is now dependent on the deep into demand and absorption of excess housing stock, which ranges between 15 and supply of properties across 48 months for different metros. Additionally, the increasing cost varied budget segments and of compliance resulting from stringent rules and adherences may occupancy stages. While push the real estate prices up, especially for new launches. Resale demand is a function of segment, however, may not witness any substantial change in ‘ask’ queries received, supply is rates due to the inherent competition characteristic to the segment. based on property listings posted on 99acres.com in On a micro-level, Hyderabad, Pune and Bangalore exhibited Jan-Mar 2018. -

Storename Address Ramamurthy Nagar Vodafone Store,Nithin

Storename Address Vodafone Store,Nithin Arcade, No 8, Ramamurthy Nagar, Banaswadi Main road, Bangalore Ramamurthy Nagar – 560043 Vodafone Store, Ground floor, No.35, 1st Main Road, Opp to Commercial Tax Office, Gandhinagar Gandhinagar, Bengaluru-560009 Vodafone Store, c/o, Maruthi clothing Co., Plot No.7-D, 1st phase,Doddanekundi industrial Whitefield area, Whitefield road, Bengaluru-560048 Vodafone Store, G-06 Lower ground floor, Innovater Building, concorase mall, Itpl International Tech park, Bengaluru-560066 Bommanahalli Vodafone store No.75/32/2, Begur main Road, Bommanahaali, Bangalore-560068 Vodafone Store, Ground Floor, CJR Complex, Outer Ring Road, Bellandur, Near Sarjapur Bellandur road junction, Opp to Café Coffee Day, Bengaluru-560 037. Vodafone Store, No 90, Sighmond Towers, Marthahalli Outer Ring Road, Bangalore – Marthahalli 566037 Hsr Layout Vodafone Store, No 806,27th Main, 80 Feet Road, HSR Layout Sector 1, Bengaluru-560102 Vodafone Store, Mehta Arcade, No.71, 15th Cross, 100 Feet Road, JP Nagar 6th Phase, Jp Nagar Bengaluru-560076 Vodafone Store, #113, Prestige Pinnacle, Koramangala Industrial Estate, Opp. Raheja Koramangala Arcade, Koramangala, Bengaluru-560095 Vodafone Store, No65/1A, Opp to Bata Showroom, Kaikondanhalli, Sarjapur Main Road, SARJAPUR ROAD Bangalore - 35 Vodafone Store, No Suraj Towers, Ground Floor, 27th cross, 3rd block, Jayanagar, Jayanagar bangalore-560011 Infosys-Blr Vodafone Store, Infosys technologies Ltd., Plot no. 40, Electronic city, Bengaluru-560100 Vodafone Store,No 21/A, 7th Main, 80 Feet Road, 1st Block, Koramangala, Bangalore Koramangala 80 feet road 560034 Vodafone Store,No 62-B, Majestic Terraces, ground floor, electronic city phase-1, Electronic City Bangalore - 560100 Vodafone Store, No 565,30th Main Road,DG Petrol Bunk Road,Banagiri Nagar,Next To Banshankari Mega Mart ,Bengaluru-560085 Vodafone Store, No. -

BANGALORE October-December 2015

InsiteQuarterly Real Estate Analysis for BANGALORE October-December 2015 Price Trends Growth Drivers Supply Analysis INTRODUCTION The 99acres.com Bangalore Insite report brings to you Capital Growth major movements in the real estate market of the city, in Oct-Nov-Dec 2015 as compared to Jul-Aug-Sep 2015. Bangalore North The report not only captures the significant trends across various localities in Bangalore, but also brings to you -1% the analysis and the insights that will make this report valuable for investors and end users. The report also includes an in-depth supply analysis to enable sellers and buyers determine the direction of the market. Bangalore Central Bangalore West -2% 0% Content Bangalore East City-Highlights: 06 -1% Price Trend Analysis: East and South Zone 07 Bangalore South North, West and Central Zone 12 -1% Supply Analysis: 14 Bangalore -1% Methodology City Insite Report We have reported quarterly price movement of capital and rental values measured in per square feet for the analysis Oct-Dec 2015 Falling sales volume force developers to of Bangalore’s residential market. Effort has been made to provide comparable and accurate city level data, since SLASH ‘ask’ prices prices and rents are floating and at any point may vary from the actual numbers. 99acres Insite 2 3 Realty Round-up Capital Rental Values Values Supply Delhi NCR Delhi NCR Mumbai Kolkata Bangalore Chennai Mumbai Pune Pune Hyderabad Hyderabad Chennai Bangalore Kolkata * Capital values represent quarterly change * Rental values represent yearly change * Supply is basis properties listed on 99acres.com 99acres Insite 4 5 East and South Bangalore BANGALORE City Highlights Capital Analysis Rental Analysis The residential real estate market in Bangalore is gradually moving towards the price correction mode. -

Hinduja Park Apartments

https://www.propertywala.com/hinduja-park-apartments-bangalore Hinduja Park Apartments - Brookefield, Banga… 2 & 3 BHK apartments available for sale in Hinduja Park Apartments Hinduja Park Apartments presented by Hinduja Holdings Pvt Ltd with 2 & 3 BHK apartments available for sale in Whitefield Road,Brookefield, Bangalore Project ID : J399022118 Builder: Hinduja Holdings Pvt Ltd Location: Hinduja Park Apartments, Brookefield, Bangalore (Karnataka) Completion Date: Jul, 2016 Status: Started Description Hinduja Park Apartments is a residential development by Hinduja Holdings Pvt Ltd. The project offers 2 & 3 BHK apartments which are well equipped with all the modern day amenities and basic facilities. The project is having the round the clock security facility. Amenities Garden Recreation Facilities 24Hr Backup Security Club House Swimming Pool Tennis Court Badminton Court Gymnasium Indoor Games Basket Ball Court Rain Water Harvesting Hinduja Holdings is one of the leading and reputed names as a promoter and developer in Bangalore. The promoters of the organization have expertise and knowledge in the field of construction activity and have constructed and promoted quite a few apartments in Bangalore. Features Luxury Features Security Features Power Back-up Centrally Air Conditioned Lifts Security Guards Electronic Security RO System High Speed Internet Wi-Fi Intercom Facility Interior Features Exterior Features Woodwork Modular Kitchen Reserved Parking Feng Shui / Vaastu Compliant Recreation Maintenance Swimming Pool Park Fitness Centre