INSITE REPORT Bangalore

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Venue Details 12Th Step Corporation

Venue Details Venue Details Venue Details 12th Step - BEL Group - Ever Growing - Corporation Sports Club 95352 67966, 080 22340444 BEL Fine Arts Complex 90352 15403, 99800 50798 SFS School, Near Vimalaya Hospital 99452 63934, 99869 78686 4th Square - Jalahalli Eng, Kan, Tam Hosur Main Road - Austin Town Sun 10.00 am, Mon 10.00 am Bangalore 560 013 Mon 7.00 pm, Tue 7.00 pm, Thu Huskar Gate Stop Tue 7.00 pm, Fri 7.00 pm Acceptance - 7.00 pm, Fri 7.00 pm, Sun 11:00 Electronic City Nammura Sarkari Madari Pratamika Shale 90367 33061, 90352 15403 am Evergreen Prabhakar Jalahalli Village - Bembala - Taluk Office Compound 9344865860 Bangalore 560 013 Sat 7.00 pm Dr.Ambedkar Sena Samithi 70933 63621, 98863 70082 Hosur Kan, Tam Action - Near K.R.Puram Railway Station - Mon 7.00 pm CSI Church, CSI Colony, Kothnur Post 81974 88144, 78997 04143 Vijinapura Tue 7.00 pm, Sat 7.00 pm First Step - Kothnur - Carmel Convent Elumalai St Francis School, Opp. Krupanidhi 99869 78686, 080 22340444 Bangalore 560077 Thu 7.00 pm, Sat 11.00 am Near Sagar Apollo Hospital 81236 18438 College Eng Adaikalam - Tilak Nagar Kan, Tam Sarjapur Road Fri 7.00 pm Government School 95352 67966, 080 22340444 Jayanagar Mon, Fri, Sat 7.00pm Koramangala Near Anjaneya Temple And Passport - Chandrodaya - Fourth Dimension - Office Mon 7.00 pm, Wed 7.00 p.m, Fri Chandra High School 82962 88230, 080 2234 0444 Jyothi School 89044 17280, 080 22340444 Koramangala 7.00 pm, Sat 7.00 pm Prakash Nagar Kan, Tam Hennur Bagalur Main Road - Anbillam - Rajajinagar Mon 7.00 pm, Sat 7.00 pm, Sun Lingarajapuram Mon 6.30 pm, Wed 6.30 pm, Gospel Street 89044 17280, 88615 73981 7.00 pm Thu 6.30 pm, Sat 6.30 pm, Sun Old Bagalur Layout Kan, Tam Chetana - 6.30 pm Lingarajpuram Mon 7.00 pm, Thu 7.00 pm St. -

INSITE ��Acres India’S No.1 Property Portal

www.99acres.com BANGALORE RESIDENTIAL MARKET UPDATE JANUARY - MARCH 2020 Market Sentiment INSITE 99acres India’s No.1 Property Portal FROM CBO’S DESK The calendar year 2020 began with some Real Estate (Regulation and Development) hopes of a revival for the residential realty Act 2016, Goods and Services Tax (GST), market in India with an increase in property and more lately the liquidity crisis amongst enquiries in January and February. Sales NBFCs and developers. The industry expects volume, too, reported growth over the home buyers to returning to the market only previous months in most metro cities, gradually as social distancing restrictions get barring Delhi NCR and Mumbai, where lifted, even though prices are likely to come supply overweighed demand. New housing down. Pro-realty measures announced by the launches remained low as the liquidity crisis Government, including loan moratorium and continued troubling developers; however, repo rate cut by 75 basis points have helped the silver lining was the upcoming festive soothe the sentiment of uncertainty among season in March. Fast-forward less than a homebuyers, but the industry is looking to month and the outbreak of novel COVID-19 in more support from the government. India turned tables as construction activities Currently sitting with an unsold inventory came to a sudden halt, and restrictions on of around 6.24 lakh residential units and site visits shrunk property sales significantly. 15 lakh under-construction homes in top The announcement of the 21-day lockdown eight metros, the real estate industry would further marred hopes of a quick revival in need more definite growth stimulators business activities. -

Download Report

INSITE BANGALORE RESIDENTIAL MARKET UPDATE JANUARY - MARCH 2021 Market Sentiment WHAT’S INSIDE? • InFocus: Union Budget 2021-22 • National Outlook Snapshot of real estate ambience across top 8 metro cities • Market Movers News that impacted Bangalore’s realty market in Jan-Mar 2021 • Commercial real estate outlook • Residential demand and supply dynamics • 99acres’ Outlook Our perspective on the current market sentiment • Key trends in the buying and renting landscape • Price trends across key micro-markets FROM CBO’S DESK The first quarter of 2021 witnessed a resurgence in sales volume across On the supply front, over 600 residential projects were launched in metro cities, particularly in Pune and Mumbai, amid a stamp duty cut metro cities, adding approximately 75,000 new units to the market. until March. While continued adoption of work-from-home weighed down Mumbai contributed close to 40 percent of the total new supply, rental demand and ‘asks’, it pushed the desire to own a home further up. followed by Hyderabad at 20 percent and Pune at 15 percent. Owner This subsequently brought back interested homebuyers to the market, listings posted on 99acres also went up by 20 percent in Jan-Mar 2021 who leveraged on deals and discounts rolled out by developers and against Oct-Dec 2020. home loan interest rates slashed by lending institutions. In line with the recovering market sentiment, site visits and sales, pricing power returned The green shoots of recovery seen so far will have to stand the test of to the sellers. Based on properties listed on 99acres, none of the eight time with a steep surge in COVID-19 cases and the resultant restrictions metro cities recorded a downward revision in average listing prices of in some cities may impact economic recovery, project construction Maneesh Upadhyaya residential apartments in Jan-Mar 2021 against the previous quarter. -

Unpaid Dividend-17-18-I3 (PDF)

Note: This sheet is applicable for uploading the particulars related to the unclaimed and unpaid amount pending with company. Make sure that the details are in accordance with the information already provided in e-form IEPF-2 CIN/BCIN L72200KA1999PLC025564 Prefill Company/Bank Name MINDTREE LIMITED Date Of AGM(DD-MON-YYYY) 17-JUL-2018 Sum of unpaid and unclaimed dividend 696104.00 Sum of interest on matured debentures 0.00 Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Validate Clear Proposed Date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type transfer to IEPF Name Name Name First Name Middle Name Name Account Number transferred (DD-MON-YYYY) 49/2 4TH CROSS 5TH BLOCK MIND00000000AZ00 Amount for unclaimed and A ANAND NA KORAMANGALA BANGALORE INDIA Karnataka 560095 54.00 23-May-2025 2539 unpaid dividend KARNATAKA 69 I FLOOR SANJEEVAPPA LAYOUT MIND00000000AZ00 Amount for unclaimed and A ANTONY FELIX NA MEG COLONY JAIBHARATH NAGAR INDIA Karnataka 560033 72.00 23-May-2025 2646 unpaid dividend BANGALORE ROOM NO 6 G 15 M L CAMP 12044700-01567454- Amount for unclaimed and A ARUNCHETTIYAR AKCHETTIYAR INDIA Maharashtra 400019 10.00 23-May-2025 MATUNGA MUMBAI MI00 unpaid -

Details of Equity Shares Liable to Be Transfer to IEPF Suspense Account

DELTON CABLES LIMITED CIN:L31300DL1964PLC004255 Regd Off: Delton House, 4801, Bharat Ram Road, 24, Darya Ganj, New Delhi - 110002 Ph: 011 - 23273907 Website: www.deltoncables.com Details of equity shares to be transferred to IEPF suspense account S. No. Folio No. NAME ADD1 ADD2 ADD3 ADD4 Pin Code SHARES 1 000002H H C DEB 15/118,JHEEL ROAD BANK PLOT, CALCUTTA 700075 336 2 000003S S K AGARWAL 741, ASIAD VILLAGE, MAAKHAN SINGH MARG, NEW DELHI 110000 60 3 000006U U JAGADISH NAYAK VIII/1852 PRASHANTHA NILAYA LALAN ROAD COCHIN 682002 84 4 000008B B D AGARWAL 150 5 000008D D JACOB SATHIA DHAS SUB EDITOR INDIAN EXPRESS MADURAI (TAMIL NADU) 625001 75 6 000008E EBRAHIM SAIT C/O M/S HAJEE OOMER & SONS COMMERCIAL STREET BANGALORE 560001 9 7 000008L L MEERA 9/1 GNANI NIVAS III MAIN ROAD JAYAMAHAL EXTN 560046 150 BANGALORE 8 000008V V BALAKRISHNAN 14 PALAT SANKARAN NAIR ROAD MADRAS 600034 150 9 000008Y Y V CHANDRASEKHARIAH NO 430 ELEVENTH CROSS WILSON GARDEN BANGALORE 560027 150 10 000009O OLIVER SAMUEL JOSEPH SHARDA COTTAGE CHRISTAIN BEHRAMPURA AHMEDABAD 388001 75 SOCIETY 11 000009P P B C SEKHAR PLOT 22, GAYATHRI NAGAR, SRI SAI SAKTHI NILAYAM, CHITLAPAKKAM 600064 84 POST, CHENNAI 12 000010C C HANUMANTHA RAO 90/4 V CROSS HANUMANTHA NAGAR BANGALORE 560019 168 13 000011G G K DHANALAKSHMAMMA 249 IIIRD MAIN 2ND CROSS ROAD CHAMARAJAPET BANGALORE 560018 9 14 000012O OM PRAKASH CHITKARA H.NO. 843 SECTOR 16 FARIDABAD 121002 75 15 000012W W A ABREO 11 HUTCHINS RD, COOKE TOWN, BANGALORE 560005 126 16 000013F FAQIR CHAND JAIN M/S HINDUSTAN TRADING CHANDIGARH ROAD AMBALA CITY 134007 150 CORPORATION 17 000013L L RM LAKSHMANAN C/O L RAMANATHAN CLYFFEE ESTATE KENKARAI NILCIRIS 643246 84 18 000013O OM PRAKASH GUPTA MAYURA, FOREST OFFICE LANE, VAZHUTHACAUD, TRIVANDRUM 000014 75 19 000015C C KATHIRVEL 111 BAZAAR STREET CHIDANABARAM SOUTH TAMIL NADU 608001 75 ARCOT DIST 20 000015W WALTER P REBELLO CITI BANK N.A., INVESTMENT SERVICES, 293, DR. -

Bangalore City East

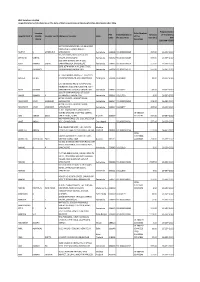

F-Register as on 31-03-2019 Sl.No. PCBID Year of Name of the Industry Address of the Organisations Area/ Place/ Ward Taluk District Name of the Type of Product Catego Size Colour date of capital Present Appli Water Act Air Air Act HW HWM B BMW Regist Regis Batter E- E-Waste MSW MSW Remar Identificatio No. Industrial Estates/ Organisation ry No (L/M/S/ (R/O/G/ establis investmen Workin cabilit (Validity) Act (Validity) M (Validity) M (Validity) ration tratio y Waste (Validity) (Y/N) (Validi ks n (YY-YY) areas / Activity* (I/ (XGN Micro) W) hment t (in g Status y (Y/N) (Y/N W under n (Y/N) (Y/N) ty) M/ catego (DD/M Lakhs) (O/C1/ under ) ( Plastic under (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) (14) (15) (16) (17) (18) (19) (20) (21) (22) (23) (24) (25) (26) (27) (28) (29) (30) (31) (32) (33) 1 12336 2006-07 August Ventures Pvt Ltd. Augest Park No:35,36,37,38&39.B.Narayan pur Village Kaggadasapura Main Bangalore Urban Bangalore Urban C Residential 1181Large Red 2007 4617 O Y 30.06.2021 N N N N N N N N NA NA NA K.R.Puram Hobli, No:03 1st B croos Road Kaggadasapura Road, District District Apartment with Main Road, Bangalore 210 flats with built up area of 36,977.10 Sqm. 2 12080 2006-07 Bagmane Developers, Lake View-2, (laurel & Tridib building) Khatha No.65/2, C.V.Raman Nagar, Bangalore Urban Bangalore Urban C Software 1180 Large Red 2006 40132 O Y 30.06.2022 Y 30.06.2022 Y 30.09.2019N N N N N N NA NA NA Byrasandra village, C.V.Raman Nagar, Bangalore-560093 District District development 3 10533 2006-07 Hindustan Aeronautics Limited (HAL), Engineering Division, PB NO.9310, Old Madras Road, Old Madras Road Bangalore Urban Bangalore Urban I Overhauling of 1370 Large Red 1961 31290 O Y 30.06.2021 Y 30.06.2021 Y 30-Jun-20 N N N N N N NA NA NA Bangalore - 560 093 District District Aeroengines & related components 4 2006-07 Mantri Corner Stone, Sy.No.2&3, Property No. -

Bangalore Branch 1 .Pdf

Id : 161162 Id : 10888 Id : 163066 Dr. Rachana C Dr. Sowmya Ramachandrachar Dr. Durga Akhila Rohith CH 3 Santara Magan Place Apt, A-121A, Shivpuri T Point Saguna Medical Center, Behind Maaruti Dental Collage New Vijjaynagar NTR Circle, Kammanahalli Ghaziabad - 201009 Dharmavaram Off Bannergatta Road Uttar Pradesh Anantapur - 515671 Bangalore - 080-26430022 09868055042 Andhra Pradesh Karnataka 9538905550 9886519792 Id : 85984 Id : 15717 Id : 10593 Dr. Saumitra Saravana Dr. M.R. Kasinath Dr. Suneetha Rao Stafford Dental Centre Kashis Dental Clinic # 565, 1st Floor No.315, Garrison Ville Road 21, Old Market Road 7th Main, HAL IInd Stage Stafford, Virginia V.V. Puram Bangalore - 560 008 Pin-521244 Bangalore - 560 004 Karnataka Karnataka 9844355701 Id : 10129 Id : 44281 Id : 2686 Dr. P B Cariappa Dr. Madan Nanjappa Dr. Nisha S. Hedge 11/1, Hayes Road 14, Palmgrove Road No. 309, Mukund Apartments Bangalore - 560 025 Austintown Palmgrove Road, Karnataka Bangalore - 560 047 Victoria Layout 9880364153 Karnataka Bangalore - 560 047 98450-35286 Karnataka 9886404342 Id : 10744 Id : 11009 Id : 44276 Dr. Nisha Mehta Dr. Vinay Krishnamurthy Rao Dr. Karthik Venkataraghavan Adarsh Dental Clinic B2-111, "KRISHNA", Sector - B, VI B Main Vibha Dental Care Centre 44, Kilari Road, B.V.K.Iyengar Rd. Cross Road, No.166, 22nd Cross Domlur Majestic Yelahanka Satellite Town 2nd Stage, Nr Kalki Temple Bangalore - 560 053 Bangalore - 560 064 Bangalore - 560 071 Karnataka Karnataka Karnataka 9341352044 9482229939 9845258974 Id : 10798 Id : 10110 Id : 10746 Dr. Jill Gnanamuthu Dr. B. Subhashchandra Shetty Dr. Manoj Christopher J. L-25, Sector - 14, Pete Channapa Indl. Estate H. H. Hospital Road No. -

List of Unpaid/Unclaimed Dividend As on AGM Date I.E

WeP Solutions Limited Unpaid/Unclaimed Dividend as on the date of 21st Annual General Meeting held on 22nd September 2016 Proposed Date Investor Folio Number PIN Folio Number of Amount of Transfer to Investor First NameMiddle Investor Last NameAddress of Investor State of the Code the Securities Due (Rs.) IEPF Name Securities (DD-MM-YEAR) WIPRO TECHNOLOGIES, NO.26 HOSUR MAIN ROAD, BOMANNAHILLI, ADITYA V MANPURIA BANGALORE Karnataka 560068 FOLIO00004284 257.00 26-SEP-2022 39 7TH CROSS, HMT LAYOUT, R T AIRUDHA SANYAL NAGAR, BANGALORE Karnataka 560032 FOLIO00004149 557.00 26-SEP-2022 333 18TH G MAIN, 6TH BLOCK, AJAY KUMAR OMER KARAMANGALA, BANGALORE Karnataka 560095 FOLIO00004169 557.00 26-SEP-2022 2375 16TH MAIN, H A L 2ND STAGE, AJIT KATANKOT INDIRANAGAR, BANGALORE` Karnataka 560038 FOLIO00004110 557.00 26-SEP-2022 G-1 SAI KAMALA NIVAS, 6-1-343/10/1, AKELLA LATHA PADMARAONAGAR, SECUNDERABAD Telangana 500061 DSL03498 20.00 26-SEP-2022 C/O MORZARIA PRODUCTS PVT LTD, MORZARIA INDUSTRIAL ESTATE, NO 4 ALOK MOHAN BANNERGHATTA ROAD, BANGALORE Karnataka 560029 DSL00032 83.00 26-SEP-2022 11 10TH D MAIN ROAD, IST BLOCK AMAR KUMAR K JAYANAGAR, BANGALORE Karnataka 560011 DSL01790 6.50 26-SEP-2022 40/1A II FLOOR, AIRPORT ROAD, AMARJEET KAUR SAWHNEY BANGALORE Karnataka 560017 FOLIO00003954 240.00 26-SEP-2022 40/1A II FLOOR, AIRPORT ROAD, AMARJEET KAUR SAWHNEY BANGALORE Karnataka 560017 DSL03877 205.50 26-SEP-2022 D-201 MALBAR HILL APARTMENT, BEHIND SARGAM SHOPPING CENTRE, IN-300183- AMI ASHISH DESAI PARLE POINT, SURAT Gujarat 395007 11375965 557.00 26-SEP-2022 -

04-05-2018 Pink Poling Final

CONSTITUENCY WISE NO OF POLLING STATIONS IDENTIFIED AS PINK POLLING STATION SL.N NAME OF THE ADEO NO & NAME OF THE LAC SL NO P.S No P.S NAME O United Theological College, Millers Road Room No-1 1 35 1 BBMP CENTRAL 162-SHIVAJINAGAR 2 41 Mount Carmel Collage, Palace, Road, Vasanthnagar Room No-1 RBANMS 1st Grade College . Annaswamy Modaliyar Road, ShivanaChetty Garden 3 147 Room No-1 NRI school 4 292 165- 2 BBMP CENTRAL RAJARAJESHWARINAGAR 5 332 Rajarajeshwari school 6 110 jnavahin public school 7 22 St. Clarat School BANGALORE MONTESSERY ENGLISH PRIMARY SCHOOL DOMLUR LAYOUT ROOM 8 143 3 BBMP CENTRAL 163-SHANTHINAGAR 9 25 SSB ENGLISH SCHOOL HAL 2ND STAGE ROOM BISHOP COTTON GIRLS SCHOOL NO.71, ST MARKS ROAD, 10 2 BANGALORE- 560001. ROOM NO 1 Deenasevasangha Labourer s Fellowship up Graded Primary School No. 22, Risaldar 11 81 Road Sheshadripuram Deenasevasangha Labourer s Fellowship up Graded Primary School No. 22, Risaldar 4 BBMP CENTRAL 164-GANDINAGAR 12 82 Road Sheshadripuram Padmashree Krishnaiah Shetty Govt School Sanjeevappa lane Avenue Road cross 13 183 Room No-01 14 60 Government Composite high school, 7th cross road, Prakashnagar 15 161 BBMP ward office, Ward no. 108, 60th cross, 5th block, Rajajingar Sri. Siddaganga High school, Jangama Matha, 12th main road, 7th cross, 1st stage, 5 BBMP CENTRAL 165-RAJAJINAGAR 16 54 3rd phase Government Block Model primary school, 3rd block, 3rd stage, Saneguruvana halli 17 38 St, Theresa Girls High School 18 146 Room No 1 Sulthan Road Chamrajapet St, Theresa Girls High School 6 BBMP CENTRAL 168-CHAMARAJPET -

Tuesday B.E.L

TUESDAY B.E.L. GROUP 7-00 PM B.E.L. SC/ST Office, 91-99019-67603 Jalahalli, BANGALORE 91-97431-03777 COURAGE 7-00 PM Government P.U. College 91-99168-02997 Yelahanka Subway, Opp. Police Station YELAHANKA BANGALORE DEVANAHALLI 6-00 PM GKBMS School 91-99168-02997 Near Guru Bhavana DEVANAHALLI BANGALORE DEVARA ANUGRAHA 7-00 PM St.Philomenas Church Compound 91-90089-48589 St.Mary’s School, Ashok Road, Lakshar MYSORE EVER GROWING 7-00 PM SFS School, Near Vimalya Hospital 91-88921-43052 Hosur Main Road, Huskur Gate Stop ELECTRONICS CITY BANGALORE FREEDOM 7-00 PM Infant Jesus Compound 91-96323-79407 Near Rose Garden Bus Stop 91-81058-64299 NEELASANDRA BANGALORE HOPE 7-00 PM St.Joseph Indian High School 91-95357-64055 Near Mallya Hospital VITTAL MALLYA ROAD BANGALORE JEEVITHAM 6-30 PM Good Shepherd Church Basement 91-97419-61891 Thamaraikannan Road, Murphy Town 91-82966-00295 ULSOOR BANGALORE JOY OF LIVING 7-00 PM Resurrection School 91-90663-49910 1st Stage 1st Cross, Krishna Temple Road 91-81232-30255 INDIRANAGAR BANGALORE TUESDAY LIVING SOBER 7-00 PM Ascension Church 91-77607-52288 D’Costa Layout, Cooke Town LINGARAJAPURAM BANGALORE MOKSHA 7-00 PM Lourdes Church, 91-97413-35440 Whitefield Main Road, WHITEFIELD BANGALORE NAMBIKE 7-00 PM Anganwadi 91-73489-97526 Opp.Kino Theatre, V.V.Giri Colony, SC Road 91-73489-97482 SESHADRIPURAM BANGALORE NEW FLOWER 7-00 PM Telugu PUM School, 91-99527-91141 Kamaraj Colony, Near Ayappa Temple 91-73392-10452 Hosur NEW WAY 7-00 AM DakshinaMatha Church, 91-90663-49910 2nd Main, 2nd Cross, Gowthampura 91-95918-30625 -

In the High Court of Karnataka at Bengaluru

1 IN THE HIGH COURT OF KARNATAKA AT BENGALURU DATED THIS THE 03 RD DAY OF JANUARY 2018 BEFORE THE HON’BLE MR. JUSTICE SREENIVAS HARISH KUMAR R.F.A.No.591/2013 BETWEEN: 1.BRUNO MICHAEL AGED 58 YEARS 2.EUGENE MICHAEL AGED 50 YEARS 3.CLEMENT SURESH MICHAEL AGED 45 YEARS 4.MRS SUSAN ARUNA AGED 48 YEARS 5.MRS INDIRA ELIZABETH AGED 49 YEARS 6.MRS MARY RACHAEL AGED 42 YEARS NOS. 1, 2 AND 3 ARE THE SONS AND NOS.4, 5 AND 6 ARE DAUGHTERS OF LATE SRI ALOYSIUS MICHAEL NO.19, CAMPBELL ROAD BANGALORE-560047. 7.MRS CARMEL AGED 53 YEARS WIFE OF SRI PREMKUMAR AND 2 DAUGHTER OF LATE SRI ALOYSIUS MICHAEL NO.19, CAMPBELL ROAD BANGALORE-560047 8.MRS CHRISTIANA AGED 51 YEARS WIFE OF SRI M MICHAEL AND DAUGHTER OF LATE SRI GEORGE RAJENDRAN NO.19, CAMPBELL ROAD BANGALORE-560047 9.MRS CECELIA AGED 46 YEARS WIFE OF SRI DOMINIC SAVIO AND DAUGHTER LATE SRI GEORGE RAJENDRAN NO.19, CAMPBELL ROAD, BANGALORE-560047 10.MRS PAMELA AGED 43 YEARS WIFE OF SRI SAGAYA RAJ AND DAUGHTER LATE SRI GEORGE RAJENDRAN NO.19, CAMPBELL ROAD, BANGALORE-560047. ... APPELLANTS (By Sri : KESTHUR N CHANDRA SHEKHER, ADVOCATE) AND 1.MRS KATE PHILIPS AGED 78 YEARS WIFE OF MR W PHILLIPS AND RESIDING AT NO. 46, 9TH CROSS GURUMURTHY ROAD, R S PALYA BANGALORE-560033 2.MR TERENCE AGED 74 YEARS 3 SON OF LATE T A MICHAEL RESIDING AT NO. 8 HIGH STREET CROSS COOKE TOWN, BANGALORE 3.MRS SHEELA FICKER MAJOR WIFE OF MR ANDREW FICKER DAUGHTER OF T A MICHAEL RESIDING AT NO. -

Jurisdiction of Income Tax Officers, Bengaluru with Telephone Directory

JURISDICTION OF INCOME TAX OFFICERS, BENGALURU WITH TELEPHONE DIRECTORY CONTENT PAGE NO. SPAN OF CONTROL 1-5 PINCODE JURISDICTION 6-8 RANGE 1 (1) TO RANGE 7 (2) RANGE 1, 1(1), 1(2), 1(3) 9-14 RANGE 2, 2(1), 2(2), 2(3) 15-19 RANGE 3, 3(1), 3(2), 3(3) 20-26 RANGE 4, 4(1), 4(2), 4(3) 27-33 RANGE 5, 5(1), 5(2), 5(3) 34-38 RANGE 6, 6(1), 6(2), 6(3) 39-45 RANGE 7, 7(1), 7(2) 46-49 TRANSFER PRICING 50-52 INTERNATIONAL TAXATION 53-54 AUDIT 55-56 TDS 57-59 DGIT - CENTRAL CIRCLE - I & II 60-61 INVESTIGATION - UNIT I, II, III 62 CIB (INTELLIGIENCE) 63 EXEMPTIONS 64 SPAN OF CONTROL Pr. CCIT, Bengaluru CCIT, Bengaluru - 1 CCIT, Bengaluru - 2 Pr. CIT, Bengaluru - 1 Pr. CIT, Bengaluru - 2 Pr. CIT, Bengaluru - 5 Range - 1(1), Bengaluru Range - 2(1), Bengaluru Range - 5(1), Bengaluru Range - 1(2), Bengaluru Range - 2(2), Bengaluru Range - 5(2), Bengaluru Range - 1(3), Bengaluru Range - 2(3), Bengaluru Range - 5(3), Bengaluru CIT (ADMN & CO), Bengaluru Pr. CIT, Bengaluru - 3 Pr. CIT, Bengaluru - 6 CIT (DR), ITAT, Bengaluru - 1 Range - 3(1), Bengaluru Range - 6(1), Bengaluru CIT (DR), ITAT, Bengaluru - 2 Range - 3(2), Bengaluru Range - 6(2), Bengaluru CIT (DR), ITAT, Bengaluru - 3 Range - 3(3), Bengaluru Range - 6(3), Bengaluru CIT (Judicial), Bengaluru Pr. CIT, Bengaluru - 4 Pr. CIT, Bengaluru - 7 Range - 4(1), Bengaluru Range - 7(1), Bengaluru CIT (Audit), Bengaluru Range - 4(2), Bengaluru Range - 7(2), Bengaluru Range - 4(3), Bengaluru CIT (A)-1, Bengaluru Pr.