BANGALORE October-December 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In the High Court of Karnataka at Bangalore Dated This the 8Th Day of April, 2014

- 1 - IN THE HIGH COURT OF KARNATAKA AT BANGALORE DATED THIS THE 8TH DAY OF APRIL, 2014 :BEFORE: THE HON’BLE MR.JUSTICE MOHAN .M. SHANTANAGOUDAR WRIT PETITION No.10108/2014(GM-CPC) C/W WRIT PETITION No.10109/2014(GM-CPC) BETWEEN: 1. TANGLIN DEVELOPMENTS LIMITED, A COMPANY INCORPORATED UNDER THE COMPANIES ACT,1956, HAVING ITS REGISTERED OFFICES AT NO.23/2, VITTAL MALLYA ROAD, BANGALORE-560 001. REPRESENTED BY ITS DIRECTOR: MR.SHANKAR.V. 2. MR. NITIN BAGAMANE, MANAGING DIRECTOR, AGED ABOUT 41 YEARS, TANGLIN DEVELOPMENTS LIMITED, RESIDING AT NO.69, LAVELLE ROAD, BAGAMANE HOUSE, BANGALORE-560 001. 3. MR. SHANKAR V. AGED ABOUT 45 YEARS, "MANGALA", 12, ANJANEYA NAGAR, 100FT. RING ROAD, BANASHANKARI 3 RD STAGE, BANGALORE-560 085. 4. N. BALRAJ SHETTY, AGED ABOUT 40 YEARS, OPP. TO K.P.T, KADRI HILLS, COMMON MANGALORE-575 004. ... PETITIONERS (BY SRI DILIP N.V. ADV. FOR TATRA LEGAL ADVS.) - 2 - AND: SYNOWLEDGE IT SERVICES INDIA PVT. LTD. A COMPANY INCORPORATED UNDER THE COMPANIES ACT.1956, NO.120A, ELEPHANT ROCK ROAD, 3RD BLOCK, JAYANAGAR, BANGALORE-560 011. REPRESENTED BY ITS DIRECTOR. COMMON MR. AJAYSIMHA ... RESPONDENT (BY SRI T. SURYANARAYANA, ADV. FOR M/S. KING & PATRIDGE, ADV.) WRIT PETITION NO.10108/2014 FILED UNDER ARTICLES 226 & 227 OF THE CONSTITUTION OF INDIA PRAYING TO SET ASIDE THE ORDER DATED 1.1.2014 BEING ANN-A PASSED BY THE HON'BLE XXX ADDL. CITY CIVIL JUDGE, BANGALORE CITY CIVIL JUDGE, BANGALORE CITY IN O.S. NO.4037/2010 REJECTING THE APPLICATION FILED BY THE PETITIONER UNDER ORDER 14 RULE 1 TO 5 R/W U/S 151 OF THE CPC TO FRAME THE PROPOSED ISSUE AND TREAT THE SAME AS THE PRELIMINARY ISSUE AND GIVE A FINDING ON IT AS BEING ERRONEOUS, ARBITRARY, PERVERSE AND ILLEGAL. -

Chaipoint Outlets

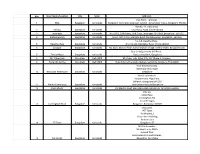

Sno Store Name/Location City State Address1 Chai Point , Terminal, 1 BIAL Bangalore Karnataka Bangalore International Airport Limited , Devanahali Taluka, Bangalore-560300 Plot No. 44, Electronics 2 Infosys Bangalore Karnataka City, Hosur Road, B'lore-560100 3 Jayanagar Bangalore Karnataka No.524/2, 10th Main, 33rd Cross, Jayanagar 4th Block, Bangalore - 560 011 4 Malleshwaram Bangalore Karnataka No.64, 18th Cross, Margosa Road, Malleshwaram, Bangalore - 560 055 No.A-8, Devatha Plaza, 5 Devatha Plaza Bangalore Karnataka No.131-132, Residency Road, B'lore-560025 6 Sarjapur Bangalore Karnataka No. 38/2, Ground Floor, Kaikondrahalli village, Varthur Hobli, Bangalore East Opp to Adigas hotel, MG Road , 7 Trinity Metro Bangalore Karnataka Next to Axis Bank, Bangalore 8 DLF Cyber Hub Gurugram Delhi NCR K5, Cyber hub, Cyber City, DLF Phase 3, Gurgaon 9 Huda City Centre Gurugram Delhi NCR Huda City Centre Metro Station, Sector 29, Gurgaon, HR 122009 Near Electronics City Bommasandra village 10 Narayana Healthcare Bangalore Karnataka Bangalore Mantri commercio Kariyammana Ahgrahara , Bellendur,Bangalore-560103 11 Mantri Commercio Bangalore Karnataka Near Sakara Hospital Bangalore 12 RMZ Infinity Bangalore Karnataka Old Madras Road, Bennigana Halli, Bangalore, Karnataka 560016 S No 50, Little Plaza, Cunningham Rd, Vasanth Nagar, 13 Cunningham Road Bangalore Karnataka Bangalore, Karnataka 560002 Chai point #77 Town Building No,3 Divya shree building Yamalur post 14 77 Town Bangalore Karnataka Bangalore -37 NH Cardio center NH Health city -258/a Ground floor, Bommasandra Industrial area, 15 NH Cardio Bangalore Karnataka Bangalore, Karnataka 16 Unitech Infospace Gurugram Delhi NCR Store No 6, Unitech Infospace SEZ Sector-21, Gurgaon 17 Salarpuria Softzone Bangalore Karnataka Salarpuria Softzone ,Outer ring road ,Near sarjapur junction ,Bangalore -43 John F. -

ロケーション カテゴリ ロケーション名 住所 市 ZIP- CODE Hotel Ashish Resort Ashish Resort,Tourist Complex A

ロケーション ZIP- ロケーション名 住所住所住所 市市市 カテゴリ CODE Hotel Ashish Resort Ashish Resort,Tourist complex area, Fatehabad road, agra-282001 Agra 282001 Hotel Chanakya,Shaheed Nagar Crossing,Near AIR Hotel Hotel Chanakya Agra 282001 Station,Shamshabad Road,Agra-282001 Restaurant US Pizza US PIZZA, F-1, 1st Floor, Shapath 3, SG Road , Ahmedabad Ahmedaba 380015 US PIZZA,106, Sundaram Arcade, Opposite Shukan Mall, Science Ahmedaba Restaurant US Pizza 380060 City Road, Sola, Ahmedabad d US PIZZA, #4, Aishwaria Complex, Prakash Nagar, Jawahar Ahmedaba Restaurant US Pizza 380008 Chowk Charrasta, Mani Nagar, Ahmedabad d Zen Café, Across Sardar Patel Seva Samaj Hall, Next to Artisan's Ahmedaba Cafe_Bar Zen Cafe 380009 Cottage, Mithakali, Ahmedabad d US Pizza, G12, GROUND FLOOR, SHIVALIK ARCADE100 FEET Ahmedaba Restaurant US Pizza 380015 ROAD, OPP PRAHALADNAGAR GARDEN d Restaurant US Pizza U.S.Pizza, Bapunagar, Ahmedabad Ahmedaba 380026 Mc Donalds, shop no UG-4,34-b, M.G marg, civil line, Allahabad, Restaurant Mc Donalds Allahabad 211012 Uttarpradesh Cafe_Bar Coffee 'N' U Coffee N U ,FF,8,9,10, SH-14, cross point mall, Alvar, Rajasthan Alvar 301402 Galaxy World Mall, Shop No- 9, Sec - 7 , Urban Estate, Ambala Restaurant Mc Donalds Ambala 133001 City, Ambala - 134003 Mc Donalds, Celebration Mall , AIPL ,Ground Floor, 16, Batala Restaurant Mc Donalds Amritsar 143001 Road, Amritsar Cafe_Bar 64 Bistro Cafe 64 Bistro Cafe, 1st Main, 7th Block, Koramangala, Bangalore Bangalore 560034 Restaurant AL - BEK AL - BEK,01- SS tower, RT Nagar, Main Road, Bangalore-56 Bangalore 560032 Alibaba Restaurant, #69, 1st Floor, M.M Road, Frazer town, Restaurant Alibaba Bangalore 560005 Bangalore - 560005 Restaurant Anjappar Anjappar - 50, 100 feet Road, 4 Block, Koramangala, Bangalore Bangalore 560034 Restaurant ATE 9 ATE ATE9ATE, No. -

Godrej United Whitefield-Flipchart Revised 29-06-2018 Copy

GODREJ UNITED WHITEFIELD, BANGALORE RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in PRESENTING GODREJ PROPERTIES' MOST PREMIUM PROJECT IN EAST BANGALORE Artist’s impression. Not an actual site photograph. RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in WELL-CONNECTED LOCATION RERA No.: PRM/KA/RERA/1251/446/PR/171010/000003 available at https://rera.karnataka.gov.in AN ADDRESS WHERE NOTHING IS TOO FAR FROM HOME The Brigade Phoenix School V.R. Mall Marketcity Decathlon KR Puram Xylem Bridge Tech RMZ Infinity Park GODREJ Baiyappanahalli Metro & Railway Gopalan UNITED Station Grand Mall Metro Cash Bhoruka Gopalan & Carry Tech Park Prestige Shantiniketan Signature Mall Hoodi Planned Brigade Metropolis Garudacharpalya Swami Vivekananda Road Metro Station HAL Engine Division The Zuri MAHADEVAPURA Gopalan Ascendas Park Hoodi Main Road C.V. Raman National School Square Mall Taj Vivanta Nagar Euro School EMC Corporation Whitefield International Technology Soulspace Park Arena Mall Bagmane Shailendra Tech Park Keys Hotel Tech Park Sri Sathya Sai Institute Doddanekundi of Medical Sciences Bagmane Lake Lake RMZ NXT SAP Labs Neil Rao Inorbit Mall Towers Landmark Hospital INDIRANAGAR Rainbow EPIP ZONE Vydehi Institute Children’s of Nursing Hospital Sciences School/College BROOKEFIELD Hotel Mall CMRIT Brookefields Hospital MARATHAHALLI Tech Park/Corporate 100-Feet Road 100-Feet KUNDALAHALLI Metro Railway HAL Heritage Centre N Domlur Flyover & Aerospace Museum Bridge Lake W E HAL Old Airport Road Embassy Flyover S Golf Link Source: http://www.english.bmrc.co.in/FileUploads/phase2forweb.pdf | Google Maps. Map not to scale. -

Alembic Urban Forest - Kadugodi, Bangalore Spacious and Ventilated Apartments

https://www.propertywala.com/alembic-urban-forest-bangalore Alembic Urban Forest - Kadugodi, Bangalore Spacious and ventilated apartments. Alembic Urban Forest is presented by Alembic Real Estate at Kadugodi , Bangalore offers residential project that hosts 2 and 3 BHK apartment with good features Project ID: J594611895 Builder: Alembic Real Estate Location: Alembic Urban Forest, Kadugodi, Bangalore (Karnataka) Completion Date: Jul, 2018 Status: Completed Description Alembics Urban Forest at Kadugodi, Bangalore. The project spread over 1314 - 1890 sq.ft. comprising 2 a n d 3 bhk apartments.It holds the reputation of exhibiting quality and technologically complex infrastructure of international standards, and that has been well justified through the design of The Urban Forest.Located in the IT center of Bangalore. The Urban Forest provides the convenience of being just a short distance from work places, schools, malls, and hospitals. Whitfield has an excellent connectivity with several key areas of Bangalore through a network of roads. Located in one of the most ideal locations of Bangalore. RERA No : PRM/KA/RERA/1251/446/PR/171031/001137 Amenities: Gymnasium Swimming pool Clubhouse Jogging Track Children’s Play Area Basket Ball Court Security Personal Badminton Court Cafeteria Meditation Hall CCTV Camera Basement Car Parking Party Area Rainwater Harvesting Alembic Real Estate is the brainchild of 108-year old Alembic Group of Companies that has diversified itself into various businesses, including pharmaceuticals, healthcare and engineering. With an experience of having developed over 10 million sq ft of land and more than two million sq ft of built-in space, Alembic Real Estate is one of the most sought-after real estate developers in Gujarat. -

INSITE ��Acres India’S No.1 Property Portal

www.99acres.com BANGALORE RESIDENTIAL MARKET UPDATE JANUARY - MARCH 2020 Market Sentiment INSITE 99acres India’s No.1 Property Portal FROM CBO’S DESK The calendar year 2020 began with some Real Estate (Regulation and Development) hopes of a revival for the residential realty Act 2016, Goods and Services Tax (GST), market in India with an increase in property and more lately the liquidity crisis amongst enquiries in January and February. Sales NBFCs and developers. The industry expects volume, too, reported growth over the home buyers to returning to the market only previous months in most metro cities, gradually as social distancing restrictions get barring Delhi NCR and Mumbai, where lifted, even though prices are likely to come supply overweighed demand. New housing down. Pro-realty measures announced by the launches remained low as the liquidity crisis Government, including loan moratorium and continued troubling developers; however, repo rate cut by 75 basis points have helped the silver lining was the upcoming festive soothe the sentiment of uncertainty among season in March. Fast-forward less than a homebuyers, but the industry is looking to month and the outbreak of novel COVID-19 in more support from the government. India turned tables as construction activities Currently sitting with an unsold inventory came to a sudden halt, and restrictions on of around 6.24 lakh residential units and site visits shrunk property sales significantly. 15 lakh under-construction homes in top The announcement of the 21-day lockdown eight metros, the real estate industry would further marred hopes of a quick revival in need more definite growth stimulators business activities. -

Hinduja Park Apartments

https://www.propertywala.com/hinduja-park-apartments-bangalore Hinduja Park Apartments - Brookefield, Banga… 2 & 3 BHK apartments available for sale in Hinduja Park Apartments Hinduja Park Apartments presented by Hinduja Holdings Pvt Ltd with 2 & 3 BHK apartments available for sale in Whitefield Road,Brookefield, Bangalore Project ID : J399022118 Builder: Hinduja Holdings Pvt Ltd Location: Hinduja Park Apartments, Brookefield, Bangalore (Karnataka) Completion Date: Jul, 2016 Status: Started Description Hinduja Park Apartments is a residential development by Hinduja Holdings Pvt Ltd. The project offers 2 & 3 BHK apartments which are well equipped with all the modern day amenities and basic facilities. The project is having the round the clock security facility. Amenities Garden Recreation Facilities 24Hr Backup Security Club House Swimming Pool Tennis Court Badminton Court Gymnasium Indoor Games Basket Ball Court Rain Water Harvesting Hinduja Holdings is one of the leading and reputed names as a promoter and developer in Bangalore. The promoters of the organization have expertise and knowledge in the field of construction activity and have constructed and promoted quite a few apartments in Bangalore. Features Luxury Features Security Features Power Back-up Centrally Air Conditioned Lifts Security Guards Electronic Security RO System High Speed Internet Wi-Fi Intercom Facility Interior Features Exterior Features Woodwork Modular Kitchen Reserved Parking Feng Shui / Vaastu Compliant Recreation Maintenance Swimming Pool Park Fitness Centre -

Panel Advocate List – Bangalore Co

PANEL ADVOCATE LIST – BANGALORE CO SL No Name of the Advocate Address Contact No E mail id 1. 5Ananthamurthy K R 3/3, Near STD English School, Prashanthanagar, T Dasarahalli, Bengaluru – 560040, III Floor, Dr. Ismail Building, Sardar Patrappa Road, Bengaluru - 560002 2. 6Ananthamurthy T K Off : 159/2, Rangaswamy Temple 3386640 (R) Street, Balepet, Bengaluru – 560003 Res : 598, II Cross, 7th Main, Vijayanagar, Bengaluru - 560040 3. 7Ananthanarayana B N Res : 7/48, 4th Cross, Lingarajapuram, Bengaluru – 560084 Off : 3/8, Karnic Road, Shankarapuram, Bengaluru 4. 8Annapurna Bevinje No. 4, Kodagi Building, Gundopanth Street, (Behind City Market) Bengaluru 5. 1Arakeshwara T N 232, Kadri nivas, 68th Cross, 3353431 / 0 Rajajinagar 5th Block, Bengaluru – 9845126875 560010 6. 1Arun Ponnappa M 702, Silver Lake Terrace, 167, 5583063 1 Richmond Road, Bengaluru - 560025 7. 1C K Annice Res : No.22, Prateeksha Unity Lane, 5714828 (R) 2 9th Cross, Ejipura Vivekanagar, Bengaluru – 560047 5550967 (O) Off : No.35, Lubbay Masjid Road, Bengaluru - 560001 8. 1Ashok N Nayak 105, III Cross, Gandhinagar, 2267332 (O) 4 Bengaluru - 560009 5252909 (R) 9. 1N H Ananthanarasimha No. 19, 10th Main, 27th Cross, 6715453 5Shastri Banashankari II Stage, Bengaluru - 560070 10. 1Ashwathaiah B 15, (I Floor), Link Road, 6 Seshadripuram, Bengaluru - 560020 11. 1Ashwatharanayana K Off : 21/1, Vasavi Vhambers, No. 14, I 6700521, 7 Floor, Kanya Kalyana Mantapa, 9448258115 Lalbagh Fort Road, Near Minerva Circle, Bengaluru – 560004 Res : 1034, 12th A Cross, J P Nagar I Phase, Bengaluru - 560078 12. 1D Ashwathappa 101/226, 25th Cross, 6th Block, 6548552 8 Jayanagar, Bengaluru - 560082 13. 1Ashwin Haladi Off : No. -

IAPT (PRMO) - 2017 Registered Centre Details Institution / Institution / Center Statename Centername Address Landline Center Incharge Center Incharge

IAPT (PRMO) - 2017 Registered Centre Details Institution / Institution / Center StateName CenterName Address LandLine Center Incharge Center Incharge Code Name Designation KARNATAKA INDIAN INSTITUTE OF SCIENCE CAMPUS, , KENDRIYA VIDYALAYA INDIAN INSTITUTE OF , YESWANTHPUR CIRCLE, BANGALORE KAK001 KARNATAKA 08023371316 JASEER K P PGT MATHEMATICS SCIENCE URBAN, BANGALORE, BANGALORE URBAN - 560012 T.B.DAM, , , T.B.DAM, BELLARY, SHREEDEVI S KAK002 KARNATAKA KENDRIYA VIDYALAYA HOSAPETE 08394259587 TGT WE HOSAPETE, BELLARY - 583225 GADAGIN OPP.RAILWAY GENERAL STORES, VINOBHA NAGAR, GADAG ROAD, KAK003 KARNATAKA KENDRIYA VIDYALAYA NO II HUBBALLI HUBBALLI, VINOBHA NAGAR, GADAG 08362265184 S T METRE PRINCIPAL ROAD, HUBBALLI, DHARWAD, HUBBALLI, DHARWAD - 580020 JALAHALLI EAST, BENGALURU, , AIR FORCE STATION JALAHALLI, BANGALORE D KAK004 KARNATAKA KENDRIYA VIDYALAYA NO TWO AFS URBAN, BENGALURU, BANGALORE 08028389700 VENKATESHWARALU PRINCIPAL URBAN - 560014 RAGIGUDDA, NAVULE POST, , KAK005 KARNATAKA KENDRIYA VIDYALAYA SHIVAMOGGA SHIVAMOGGA, SHIMOGA, 08182295700 B ANJAN TGT MATHS SHIVAMOGGA, SHIMOGA - 577204 CHIDRI ROAD AIR FORCE STATION, , , AIR SH P HARIKISHAN KAK006 KARNATAKA KENDRIYA VIDYALAYA AFS BIDAR FORCE STATION BIDAR, BIDAR, BIDAR, 08482236502 PGT CHEMISTRY RAO BIDAR - 585401 NEAR AFZALPR TAKKE, TORVI ROAD, VIJAYAPURA, BEHIND FIRE SATION, KAK007 KARNATAKA KENDRIYA VIDYALAYA VIJAYAPURA VIJAYAPURA, VIJAYAPURA, VIJAYAPURA - 08352270370 SIBY SEBASTIAN PRINCIPAL 586102 BYRAVESHWARA, NELAMANGALA, BANGALORE RURAL DISTRICT, HARSHA KAK008 KARNATAKA HARSHA INTERNATIONAL PUBLIC SCHOOL HOSPITAL, BANGALORE RURAL, 08028023500 MRS MANJU PILLAI PRINCIPAL NELAMANGALA TOWNBANGALORE, BANGALORE RURAL - 562123 NMDC, SANDUR TALUK, , NEAR DONI KAK009 KARNATAKA KENDRIYA VIDYALAYA DONIMALAI STADIUM, BELLARY, DONIMALAI, 08395274604 RAJENDRAN K PRINCIPAL BELLARY - 583118 PHASE I ,DRDO TOWNSHIP, C V RAMAN NAGAR, BENGALURU, OLD MADRAS KAK010 KARNATAKA KENDRIYA VIDYALAYA DRDO BENGALURU 08025243919 DR NUTAN PUNJ PRINCIPAL ROAD, BANGALORE URBAN, BENGALURU, BANGALORE URBAN - NO. -

OBW Digital Brochure.Pdf

SHOT AT LOCATION ONE HOME. INFINITE POSSIBILITIES. Discover Bangalore's most-awarded living precinct, replete with incredible amenities and facilities, a growing multi-cultural community, designer landscapes and a great, central location. ONE CENTRAL LOCATION.BOUNDLESS CONNECTIVITY. KEMPEGOWDA INTERNATIONAL AIRPORT RAJARAJESHWARI NAGAR 0.10 km - Orion Mall SAHAKAR NAGAR Aster CMI Hospital 0.10 km - Sheraton Hotel Tum kur Road 0.10 km - World Trade Center Hebbal Lake Esteem Mall Out er Ring Manyata 0.20 km - Metro Station Road Tech Park J.P. Park Movenpick HEBBAL Hebbal Junction 0.20 km - Brigade School Vivanta by Taj 0.20 km - Columbia Asia Hospital DOLLARS COLONY Indicative Metro Line Peenya Industrial Area PVR Vaishnavi Four Seasons 0.35 km - Metro Cash and Carry Sapphire Mall IISC Campus MAHALAKSHMI LAYOUT IISC Underpass 3.50 km - Sadashivanagar Mekhri Circle Metro Station C.V. Raman Road 8.00 km - MG Road R.M.V. EXTENSION Palace Grounds oad R Sankey Tank 34.0 km - KIAL Columbia Asia Hospital er Ring Palace Orchards 5.00 km - Peenya t Ou SADASHIVANAGAR oad Sheraton MALLESWARAM R oad R BENSON TOWN Temple Orion Mall d d umar KUMARA PARK Bangalore r k FRAZER TOWN Cho . Raj NANDINI LAYOUT r Bangalore Golf Club ITC Windsor D RAJAJINAGAR Manor Cantonment Railway Station Spandana Hospital Mantri Mall Cunningham Road oad R Le Meridien Indic a Millers Ulsoor Lake tive Met Suvarna r o Line Vidhana Soudha National Academy For Learning (NAFL) M.G. Road Lavelle Road J W Marriott UB City Cubbon Park The Ritz-Carlton To view our location on Google Maps, N W E please click here S MAP NOT TO SCALE ONE ABODE. -

Unpaid Dividend 2013

Sheet1 DISA INDIA LIMITED UNPAID DIVIDEND OF 2013 AS ON 31-12-2020 Proposed Date of Transfer to DIV_YEAR FOLIO NAME ADDRESS PIN AMOUNT IEPF 2013 0000007 K YESU RATNAM C/O B M D FOUNDRY MACHINERY LTD BASAPPA COMPLEX 40/1A LAVELLE ROAD BANGALORE560001 2.50 13-JUN-2021 2013 0000012 SHANTRAM KRISHNAJI KAREKAR C/O B M D FOUNDRY MACHINERY LTD BASAPPA COMPLEX 40/1A LAVELLE ROAD BANGALORE560001 2.50 13-JUN-2021 2013 0000014 V SRIDHARAN C/O B M D FOUNDRY MACHINERY LTD BASAPPA COMPLEX 40/1A LAVELLE ROAD BANGALORE560001 2.50 13-JUN-2021 2013 1201060000818818 RAKESH ROHIDAS PRABHU 39/6 SAHYADRI COLONY SIRSI 581402 10.00 13-JUN-2021 2013 1201060000949136 ARUN NARAYAN NAIK MALLIKA NILAYA GANDHINAGAR SIRSI 581403 2.50 13-JUN-2021 2013 1201090000035863 PRAKASH RAMCHANDRA PATWARDHAN SHIVAM COMPLEX , 3A/5, RAJAJI ROAD, THIRD LANE, DOMBIVLI (EAST) DOMBIVLI421201 2.50 13-JUN-2021 2013 1201090000260444 PAWANKUMAR JAGDISHPRASAD GOENKA A.B ROAD INDORE FLAT NO.402 SHANTI VILLA A/2/293,SILICON CITY,INDORE RAJENDRA452012 NAGAR 2.50INDORE 13-JUN-2021 2013 1201090003044230 SURYABEN AMITKUMAR PATEL 10, AKSHAR COLONY, TAL - ANKLESHWAR, DIST - BHARUCH. ANKLESHWAR 393001 2.50 13-JUN-2021 2013 1201090003056926 SROJBEN VASANTBHAI PATEL . GOKULNAGAR SOCIETY ANKHNI HOSPITAL PASE UNJHA TA UNJHA UNJHA 384170 12.50 13-JUN-2021 2013 1201090004656207 LATA AGARWAL H.N. 210 CHANIAPURA NEAR MUNNALAL DHARMASHAL JHANSI 284002 25.00 13-JUN-2021 2013 1201091900029521 SANTOSH VITTHAL KULKARNI NEAR LIMAYE MALA, GOVT COLONY, VISHRAMBAG, SANGLI SANGLI 416416 2.50 13-JUN-2021 2013 1201210100015839 -

A Detailed Property Analysis Report of Raja Housing Ritz

PROPINSIGHT A Detailed Property Analysis Report 40,000+ 10,000+ 1,200+ Projects Builders Localities Report Created On - 17 Aug, 2016 Price Insight This section aims to show the detailed price of a project and split it into its various components including hidden ones. Various price trends are also shown in this section. Project Insight This section compares your project with similar projects in the locality on construction parameters like livability rating, safety rating, launch date, etc. What is Builder Insight PROPINSIGHT? This section delves into the details about the builder and tries to give the user a perspective about the history of the builder as well as his current endeavours. Locality Info This section aims to showcase various amenities viz. pre-schools, schools, parks, restaurants, hospitals and shopping complexes near a project. Raja Housing Ritz Avenue Brookefield, Bangalore 33.4 Lacs onwards Livability Score 8.6/ 10 Project Size Configurations Possession Starts 9 Towers 1,2,3 Bedroom Apartment Mar `18 Pricing Comparison Comparison of detailed prices with various other similar projects Pricing Trends Price appreciation and trends for the project as well as the locality What is PRICE INSIGHT? Price versus Time to completion An understanding of how the current project’s prices are performing vis-a-vis other projects in the same locality Demand Comparison An understanding of how the strong/weak is the demand of current project and the current locality vis-a-vis others Price Trend Of Raja Housing Ritz Avenue Raja Housing