Cover New.Pmd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

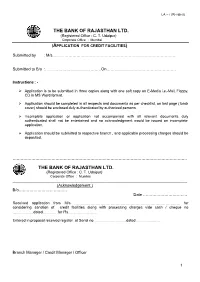

Credit Facility (LA-I Revised) Form

LA – I (REVISED) THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai (APPLICATION FOR CREDIT FACILITIES) Submitted by : M/s………………………………………………………………………………… Submitted to B/o :……………………………………On……………………………………………. Instructions : - Ø Application is to be submitted in three copies along with one soft copy on E-Media i.e.-Mail, Floppy, CD in MS Word format. Ø Application should be completed in all respects and documents as per checklist, on last page ( back cover) should be enclosed duly authenticated by authorized persons. Ø Incomplete application or application not accompanied with all relevant documents duly authenticated shall not be entertained and no acknowledgment would be issued on incomplete application. Ø Application should be submitted to respective branch , and applicable processing charges should be deposited. …………………………………………………………………………………………………………………. THE BANK OF RAJASTHAN LTD. (Registered Office : C. T. Udaipur) Corporate Office : Mumbai _____________________________________________________________________________ (Acknowledgement ) B/o……………………………… Date …………………………… Received application from M/s …………………………………………………………………………. for considering sanction of credit facilities along with processing charges vide cash / cheque no ……..………dated…………for Rs…………………. Entered in proposal received register at Serial no ……………………..dated ………………. Branch Manager / Credit Manager / Officer 1 Please tick Check List of Enclosures to the application for credit facilities :- Ö (Yes / No) 1. Audited Financial Statements for last three Financial Years with Directors’ Report, Auditor’s Report, Schedules, and Notes to Accounts relating to Yes No applicant & group concerns. 2. CMA Report including Computation of Funded & Non Funded Limits, based on Last two years (actuals), current years estimates and projections of next year Yes No 3. Profile & Banking Arrangement of the Group Companies/Sister Concerns as per format Annexure-I Yes No 4. -

JUNE 20, 2020 Vol LV No 25 ` 110

JUNE 20, 2020 Vol LV No 25 ` 110 A SAMEEKSHA TRUST PUBLICATION www.epw.in EDITORIALS The Policymaker and Uncertainty NEET Undermines Constitutional Provisions An examination of why the response to COVID-19 Sensitivity, Not Sensationalism has been dramatically different across different countries when they all face the same level of FROM THE EDITOR’S DESK virologic uncertainty page 13 Critique Caught in a Deadlock LAW & SOCIETY Gandhi and the ‘Flu Pandemic’ Lawless Lawmaking in a COVID-19 World Why did Gandhi show such indifference to the pandemic when, given what is known about him, the opposite would COMMENTARY be expected? An analysis of his letters and statements Procedural Rationality in the Time of COVID-19 from that time tries to find the answer. page 34 Towards More Inclusive Water Management The Overseer of the Plague: Reading Oedipus Rex during COVID-19 Democratic Water Systems Neo-liberal Restoration at the Barrel of a Gun: Dissecting the Racist Coup in Bolivia A look at how the ideas of some critical sociological thinkers can contribute to a more inclusive management of Remembering A Vaidyanathan (1931–2020) our water resources and truly ensure water for all page 16 BOOK REVIEWS Experience, Caste and the Everyday Social A True Social Scientist War over Words: Censorship in India, 1930–1960 A Vaidyanathan’s research work in top institutions and PERSPECTIVES the Planning Commission was marked by attempts to seek answers to the question of development beyond Gandhi and the Pandemic ECONOMIC & POLITICAL WEEKLY disciplinary boundaries. page 25 SPECIAL ARTICLES Decoding Ayushman Bharat: A Political Economy Perspective Neo-liberalism Plays Out in Bolivia Farmer Suicides in Maharashtra, 2001–2018: The 2019 coup in the country confirms the common Trends across Marathwada and Vidarbha patterns of the instrumental use of religion in politics, racism and the aggressive implementation of neo-liberal CURRENT STATISTICS policies in the route to the right. -

12. Existing Mergers and Acquisitions in Banking Sector

1.Executive Summary Merger - It's the most talked about term today creating lot of excitement and speculative activity in the markets. But before Mergers & Acquisitions (M&A) activity speeds up, it has to actually pass through a long chain of procedures (both legal and financial), which at times delays the deal. With the liberalization of the Indian economy in 1991, restrictions on Mergers and Acquisitions have been lowered. The numbers of Mergers and Acquisitions have increased many times in the last decade compared to the slack period of 1970-80s when legal hurdles trimmed the M&A growth. To put things in perspective, from 15 mergers in 1998, the number crossed to over 280 in FY01. With a downturn in the capital markets, valuations have come down to historic lows. It's high time that the consolidation game speeds up. In simple terms, a merger means blending of two or more existing undertakings into one, consequent to which each undertaking would lose their separate identity. The most common reasons for mergers are, operating synergies, market expansion, diversification, growth, consolidation of production capacities and tax savings. However, these are just some of the illustrations and not the exhaustive benefits. However, before the idea of Merger and Acquisition crystallizes, the firm needs to understand its own capabilities and industry position. It also needs to know the same about the other firms it seeks to tie up with, to get a real benefit from a merger. Globalization has increased the competitive pressure in the markets. In a highly challenging environment a strong reason for merger and acquisition is a desire 1 to survive. -

Technology Financials

Sector UpdateSector | 22 Update November | Financials 2020 Financials Technology RBI releases the Report of the Internal Working Group to Review RBI report on private sector banks’ ownership Extant Ownership Guidelines and Market share gains to accelerate for private sector banks Corporate Structure for Indian Private Sector Banks We view the RBI’s Internal Working Group (IWG) report related to the ownership of private sector banks as progressive in nature. a) Suggestions for corporate/industrial houses on how to get a banking license and b) allowing NBFCs (even belonging to industrial houses) above asset sizes of INR500b to get banking licenses would increase healthy competition, making the banking system more efficient, reducing intermediation cost, and ultimately increasing credit penetration in the system. Over the last five years, private sector banks have rapidly gained market share to ~30% (2020) from ~18% (2015), and we see this trend accelerating at a faster pace now. M&A opportunities may also increase in the system as corporates with deep pockets may adopt this route rather than building from scratch. Fit and proper criteria, increased surveillance on group entities, the maximum allowed promoter shareholding, and regulatory cost of CRR, SLR, etc. have been the key considerations thus far for applying and granting banking licenses. It remains to be seen how corporate India, NBFCs, and the RBI would approach the matter this time around, once final guidelines are out. Prima facie, we see IDFC Ltd, Bajaj Finance, L&TFH, Equitas, and Ujjivan to be key beneficiaries. Long-awaited opportunity for corporate/industrial houses One of the key suggestions in the report is to provide an opportunity for NBFCs with greater than INR500b corporate/industrial houses to get a share of the growing banking system pie. -

Regional Financial Disparity in India: Can It Be Measured?

Journal of Institutional Economics (2021), 17, 836–860 doi:10.1017/S1744137421000291 RESEARCH ARTICLE Regional financial disparity in India: can it be measured? Rashmi U. Arora* and P. B. Anand Faculty of Management, Law & Social Sciences, University of Bradford, Bradford, UK *Corresponding author. Email: [email protected] (Received 25 November 2019; revised 7 April 2021; accepted 8 April 2021) Abstract In this study, we examine disparities in financial development at the regional level in India. The major research questions of the study are: how do we measure the level of financial development at the sub- national level? How unequal is financial development across the states? Does it vary by ownership of financial institutions? To explore these research questions, our study develops a composite banking devel- opment index at the sub-national level for three different bank groups – public, private and foreign for 25 Indian states covering 1996–2015. Our findings suggest that despite reforms, banking development is sig- nificantly higher in the leading high income and more developed regions compared to lagging ones. Furthermore, we find that all bank groups including public banks are concentrated more in the developed regions. Overall, over the years the position of top three and bottom three states in the aggregate banking index have remained unchanged reflecting lop-sidedness of regional development. We also note improve- ment in the ranking of some north-eastern states during the period 2009–15. Key words: Banking development index; financial development; financial inclusion; India JEL codes: D63; G21; O16; O53 1. Introduction Recent discussions on inequality have focused on increasing global income and wealth inequality between individuals, inequality between countries and inequality among different population groups within a country (Atkinson, 2015; Pickety, 2014; Stiglitz, 2013, 2015). -

Is a 7 Digit Unique Number Issued by the Bank. What Are the Last Three

Mobile Money Identifier (MMID) is a 7 digit unique number issued by the bank. What are the last three digits represent? 1) to identify the account of the user 2) to identify the branch of the user 3) to identify the bank of the user 4) All of the above three 5) None of these Answer: to identify the account of the user What does the last character represent in PAN CARD? 1) type of holder 2) Surname of holder 3) Check digit 4) All of the above three 5) None of these Answer: Check digit What does I stands for, in PPI? 1) Instruments 2) Investment 3) Income 4) India 5) None of these Answer: Instruments Which of the below facility cannot be provided by Payment Banks? 1) ATM Card 2) Debit Card 3) Net banking 4) Mobile banking 5) Credit Card Answer: Credit Card Aapka Bank Aapke Dwar is a tagline of __________. 1) Airtel Payments Bank Limited 2) India Post Payments Bank Limited 3) Paytm Payments Bank Limited 4) Fino Payments Bank Limited 5) Vodafone M-Pesa Answer: India Post Payments Bank Limited Where is the headquarters of Paytm Payments Bank Limited? 1) Noida 2) New Delhi 3) Haryana 4) Lucknow 5) Varanasi Answer: Noida The headquarters of Equitas Small Finance Bank is _______________. 1) Guwahati 2) Thrissur 3) Coimbatore 4) Varanasi 5) Chennai Answer: Chennai Headquarters of Fino Payments Bank Limited is __________. 1) Kochi 2) New Delhi 3) Bangalore 4) Mangalore 5) Mumbai Answer: Mumbai Ho much % of FDI is allowed for Payment Banks in India? 1) 49% 2) 20% 3) 74% 4) 100% 5) 51% Answer: 74% Headquarters of FINCARE Small Finance Bank Limited is at? 1) Ahmedabad 2) Kochi 3) Mumbai 4) Bengaluru 5) Lucknow Answer: Bengaluru Loans to individuals up to ______ in metropolitan centres (with the population of ten lakh and above) under priority sector. -

India Knowledge@Wharton 1 Feb 2012.Cdr

February 01, 2012 Can YES Bank, India's Youngest and Fastest-Growing Bank, Be a Model for Newer Entrants? Published: February 01, 2012 in India Knowledge@Wharton In the first flush of liberalization post 1991, the Reserve Bank of other banks became more conservative. Kapoor, who did not have India (RBI) also imbibed some of the spirit of reform and opened up legacy issues to deal with, decided to press on the accelerator. He a trifle. New banking licenses were issued to several aspirants. But increased the number of branches, invested in the brand, continued many of those banks collapsed and ultimately had to be rescued by with hiring, intensified product management and customer the system. HDFC Bank (itself a new licensee) had to take over relationship. Most importantly in a money market that was almost Times Bank and Centurion Bank of Punjab. Global Trust Bank ran frozen, he showed risk appetite. into serious ethics issues and had to be merged with Oriental Bank of Commerce. And CRB Capital Markets, which was issued a “We were somewhat shaken and disturbed [by the crisis] because it banking license, never took off; the institution's chairman, C.R. was so early in the life [of the bank], but we also realized that it was a Bhansali, was arrested for various scams. great opportunity to acquire new customers and build confidence," Kapoor says. Jaideep Iyer, YES Bank's president of financial Currently, the RBI is set to issue a new set of licenses. The responses management, adds: "Given our scale and size we offered to the white paper on new guidelines are in. -

Do Bank Mergers, a Panacea for Indian Banking Ailment - an Empirical Study of World’S Experience

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 21, Issue 10. Series. V (October. 2019), PP 01-08 www.iosrjournals.org Do Bank Mergers, A Panacea For Indian Banking Ailment - An Empirical Study Of World’s Experience G.V.L.Narasamamba Corresponding Author: G.V.L.Narasamamba ABSTRACT: In the changed scenario of world, with globalization, the need for strong financial systems in different countries, to compete with their global partners successfully, has become the need of the hour. It’s not an exception for India also. A strong financial system is possible for a country with its strong banking system only. But unfortunately the banking systems of many emerging economies are fragmented in terms of the number and size of institutions, ownership patterns, competitiveness, use of modern technology, and other structural features. Most of the Asian Banks are family owned whereas in Latin America and Central Europe, banks were historically owned by the government. Some commercial banks in emerging economies are at the cutting edge of technology and financial innovation, but many are struggling with management of credit and liquidity risks. Banking crises in many countries have weakened the financial systems. In this context, the natural alternative emerged was to improve the structure and efficiency of the banking industry through consolidation and mergers among other financial sector reforms. In India improvement of operational and distribution efficiency of commercial banks has always been an issue for discussion for the Indian policy makers. Government of India in consultation with RBI has, over the years, appointed several committees to suggest structural changes towards this objective. -

Agricultural Development in Maharashtra Problems and Prospects

Occasional Paper—7 Agricultural Development in Maharashtra Problems and Prospects Ms. S.D. SAWANT B.N. KULKARNI C.V. ACHUTHAN K.J.S . SATYASAI National Bank for Agriculture and Rural Development Mumbai Occasional Paper—7 Agricultural Development in Maharashtra Problems and Prospects Ms. S.D. SAWANT B.N. KULKARNI C.V. ACHUTHAN K.J.S . SATYASAI } \T/ National Bank for Agriculture and Rural Development Mumbai 1999 ( Published by National Bank for Agriculture and Rural Development, Department of Economic Analysis and Research, Jeevan Seva Complex (Annexe), S.V. Road, Santacruz (W), Mumbai - 400 054 and Printed at Karnatak Orion Press, Fort, Mumbai - 400 001. Acknowledgement This occasional paper has been carved out of the research project untertaken by National Bank for Agriculture and Rural Development (NABARD), Mumbai, in collaboration with the Department of Economics, University of Mumbai, Mumbai. In its completion we owe a deep debt of gratitude to officials of NABARD and University of Mumbai who were instrumental in initiating this first collaborative study between NABARD and Department of Economics. We must put on record our special gratitude to Shri N.T. Jadhav and Ms. Sandhya Mhatre of Mumbai University who assisted us sincerely and devotedly and also through excellent management of field work at the village level. We owe a special debt to Shri N.T. Patil (retired Manager, Central Bank of India, Mumbai) who agreed to participate in the project field survey. We are specially indebted to late Prof. M.L. Dantwala for his comments and suggestions on the crucial chapters of the study. We also appreciate valuable support extended by our colleagues from University of Mumbai and NABARD, Mumbai. -

A Study on Merger of ICICI Bank and Bank of Rajasthan

SUMEDHA Journal of Management A Study on Merger of ICICI Bank and Bank of Rajasthan – Achini Ambika* Abstract The purpose of the present paper is to explore various reasons of merger of ICICI and Bank of Rajasthan. This includes various aspects of bank mergers. It also compares pre and post merger financial performance of merged banks with the help of financial parameters like, Credit to Deposit, Capital Adequacy and Return on Assets, Net Profit margin, Net worth, Ratio. Through literature Review it comes know that most of the work done high lightened the impact of merger and Acquisition on different companies. The data of Merger and Acquisitions since economic liberalization are collected for a set of various financial parameters. Paired T-test used for testing the statistical significance and this test is applied not only for ratio analysis but also effect of merger on the performance of banks. This performance being tested on the basis of two grounds i.e., Pre-merger and Post- merger. Finally the study indicates that the banks have been positively affected by the event of merger. Keywords : Mergers & Acquisition, Banking, Financial Performance, Financial Parameters. Introduction The main roles of Banks are Economics growth, Expansion of the economy and provide funds for investment. The Indian banking sector can be divided into two eras, the liberalization era and the post liberalization era. In the pre liberalization era government of India nationalized 14 banks as 19th July 1965 and later on 6 more commercial Banks were nationalized as 15th April 1980. In the year 1993 government merged the new banks of India and Punjab National banks and this was the only merged between nationalized Banks after that the number of Nationalized Banks reduces from 20 to 19. -

Maharashtra Economic Development Council

VOL. II NO. : 2 October 2019 Pages 36 ` 80 ISSN 2581-995X POLITICAL ECONOMY OF MAHARASHTRA 24.97 CAGR=14.3% 22.57 19.87 17.81 16.5 14.6 12.8 GSDP of Maharashtra( Rs. Trillion) Source: Central Statistic Office, Socio Economic Survey of Maharashtra. 2011‐12 2012‐13 2013‐14 2014‐15 2015‐16 2016‐17 2017‐18 Because your love for your loved ones, is forever... MEDC Digest - Cover_FOOD PROCESSING INDUSTRY Inner Pages.indd 1 27-Apr-19 12:13:30 PM 2 October 2019 MEDC Economic Digest MEDC Governing Board MEDC President: From the President’s Desk Mr. Ravindra Boratkar Managing Director, MM Activ Sci - Tech Communications Dear Members, Pvt. Ltd. In many fields of socioeconomic endeavour, Maharashtra remains the undisputed torchbearer MEDC Vice Presidents : of the country. Many government initiatives like Mrs. Meenal Mohadikar Make in India and Magnetic Maharashtra have CEO, Anand Trade had a deep impact to the industrial growth of Development Service the state. Maharashtra has shown continuous and sustained increments in industrial production Mr. Chandrakant Sadadekar since independence. The state is also blessed Chairman, Sadadekar Global with a 720 km coastline which makes the harnessing of the blue economy Group Export-Import a viable proposition in the overall growth and development strategy of Maharashtra. Mr. Mukund Kulkarni Director, Expert Global Maharashtra plans to grow into a trillion dollar economy by 2024- Solutions Pvt. Ltd. 25, which will likely make it the first state economy of the country to achieve this distinction. That is eminently doable considering that much MEDC Immediate Past- of the policymaking by Maharashtra’s visionary leaders has largely laid Presidents: the groundwork for this transformation. -

Leadership in Banking Through Technology

Leadership in banking through technology 22ND ANNUAL REPORT AND ACCOUNTS ON THE MOVE 2015 - 2016 AT OUR PLACE AT YOUR PLACE CONTENTS 1 Leadership through Technology 2 ICICI Bank at a Glance 4 Financial Highlights 6 Message from the Chairman 8 Message from the Managing Director & CEO 10 Board and Management 11 Messages from Executive Directors 12 Banking on the Move 16 Banking at Your Place REGISTERED OFFICE 18 Banking at Our Place Landmark 20 Promoting Inclusive Growth Race Course Circle 24 Awards Vadodara 390 007 25 Directors’ Report Tel : +91-265-3263701 CIN : L65190GJ1994PLC021012 77 Auditor’s Certificate on Corporate Governance 78 Business Overview CORPORATE OFFICE 92 Management’s Discussion and Analysis ICICI Bank Towers 116 Key Financial Indicators: Last Ten Years Bandra-Kurla Complex Mumbai 400 051 FINANCIALS Tel : +91-22-33667777 Fax : +91-22-26531122 117 Independent Auditors’ Report – Financial Statements of ICICI Bank Limited STATUTORY AUDITORS B S R & CO. LLP 122 Financial Statements of ICICI Bank Limited 1st Floor, Lodha Excelus 193 Independent Auditors’ Report – Consolidated Apollo Mills Compound Financial Statements N. M. Joshi Marg 198 Consolidated Financial Statements of Mahalaxmi ICICI Bank Limited and its Subsidiaries Mumbai 400 011 243 Statement Pursuant to Section 129 of Companies Act, 2013 REGISTRAR AND 245 Basel Pillar 3 Disclosures TRANSFER AGENTS 246 Glossary of Terms 3i Infotech Limited International Infotech Park Tower 5, 3rd Floor ENCLOSURES Vashi Railway Station Complex Vashi, Navi Mumbai 400 703 Notice Attendance Slip and Form of Proxy LEADERSHIP THROUGH TECHNOLOGY... Digital technology is transforming the way we lead our lives today. The banking and financial services industry is a clear representation of this transformation.