TASE 2019 ENG Annualrepor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

HOUSTON REAL ESTATE MISSION to ISRAEL March 3-9, 2018

Program dated: May 24, 2017 HOUSTON REAL ESTATE MISSION TO ISRAEL March 3-9, 2018 D a y O n e : Saturday, March 3, 2018 DEPARTURE . Depart the U.S.A. Overnight: Flight D a y T w o : Sunday, March 4, 2018 TLV 24/7 . 12:00 p.m. Meet your tour educator in the hotel lobby. Enjoy lunch at Blue Sky, with it’s a wide selection of fish, vegetables, olive oil and artisan cheese, accompanied with local wines and overlooking the stunning views of the Mediterranean Sea. A Look into Our Journey: Tour orientation with the Mission Chair and the tour educator. The Booming Tel Aviv Real Estate Market: Take a tour of various locations around Tel Aviv with Ilan Pivko, a leading Israeli Architect and entrepreneur. Return to the hotel. Cocktails overlooking the Mediterranean Sea. Combining Business Abroad and Real Estate in Israel: Dinner at 2C with Danna Azrieli, the Acting Chairman of The Azrieli Group, at the Azrieli Towers. Overnight: Tel Aviv D a y T h r e e : Monday, March 5, 2018 FROM RED ROOFTOPS TO HIGH-RISERS . The Laws of Urban Development in Israel: Private breakfast at the hotel with Dr. Efrat Tolkowsky, CEO of the Gazit-Globe Real Estate Institute at IDC. Stroll down Rothschild Boulevard to view examples of the intriguing Bauhaus-style architecture from the 1930s; the local proliferation of the style won Tel Aviv recognition as a UNESCO World Heritage site and the nickname of ‘the White City'. Explore the commercial and residential developments with Dr. Micha Gross, the head of the Tel Aviv Bauhaus Center. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

AFPM 2014 Annual Report

PROSPERITY FUELING AMERICAN FUEL & PETROCHEMICAL MANUFACTURERS 2014 ANNUAL REPORT AMERICAN ENERGY POLICY AT A CROSSROADS A MESSAGE FROM THE CHAIRMAN OF THE BOARD AND THE PRESIDENT OF AFPM Last year, the United States became the Today, American energy policy is at a For the refining and petrochemical world’s top producer of oil and natural gas, crossroads. The issues at stake and manufacturing industries, 2014 will prove a position that no one would have predicted the policy decisions to be made have to be a pivotal year. As a country, we face just five years ago. As a result, American never been more important. A surge crucial choices as we endeavor to maintain fuel and petrochemical manufacturers in regulations, coupled with a basic access to affordable, reliable and secure now have the opportunity and the ability to misunderstanding of the fossil fuel industry, energy sources. transform the nation’s economic outlook. hampers the ability to establish sound policies and regulations that will enable us Working on behalf of and in concert with Embracing the strong global demand to continue the progress we’ve made toward our members, AFPM will continue to: for high-quality, affordable refined renewed economic growth. petroleum and petrochemical products, • Advocate for a regulatory environment AFPM companies are putting economics Fossil fuels have been an essential part that is straightforward and effective. and infrastructure to work. Refiners are of our daily lives for so long that their true meeting America’s fuel needs, maintaining impact can easily be taken for granted. • Educate policymakers and the public a strategic inventory and becoming a key But make no mistake – they don’t just to ensure the benefits of fossil fuels are exporter. -

Tel Aviv Stock Exchange

Case Study Tel Aviv Stock Exchange migrates critical mainframe Objective applications with HPE Eliminate the risk of legacy mainframe environment operations while avoiding dependence on mainframe specialists Redefines its environment by implementing a and reducing costs low-risk, high-return mainframe migration Approach Leverage HPE Data Center Platform Consulting services to efficiently and safely migrate mainframe apps to distributed server infrastructure IT Matters • Migrating to standards-based solutions drives cost reductions • Shifting to open systems servers eliminates the need for hard-to-find mainframe specialists • Standardized Linux environment streamlines development, QA, and operations Business Matters • Migration and transformation was completed on time with no downtime or disruption The Tel Aviv Stock Exchange needed to The Tel Aviv Stock Exchange (TASE) is the • Management expects to continue to migrate its mission-critical applications from only stock exchange in Israel. It offers a “one- meet cost reduction and TCO objectives an IBM mainframe environment and turned to stop shop” that includes trading in equities, for the migration HPE Data Center Platform Consulting services bonds, and derivatives. TASE has 25 members • TASE expects a full return on to help plan and implement a platform including Israeli and international banks and investment for its migration within less migration strategy from its older, proprietary brokers, and TASE is trading in 1,900 equities than three years systems. With HPE Data Center Platform and bonds and 2,500 derivatives series. Consulting, the Tel-Aviv Stock Exchange was Its daily turnover in the equities market is also able to bring industry-leading availability, approximately 1.5 billion Israeli shekels, which increased performance, and uncompromising is about $400 million client choice to support all of its IT needs. -

Impact of the Transition to Continous Trading on Emerging financial Market’S Liquidity : Case Study of the West Africa Regional Exchange Market (BRVM)

CORE Metadata, citation and similar papers at core.ac.uk Provided by Munich Personal RePEc Archive MPRA Munich Personal RePEc Archive Impact of the transition to continous trading on emerging financial market's liquidity : Case study of the West Africa Regional Exchange Market (BRVM) Aboudou OUATTARA Centre Africain d'Etudes Sup´erieures en Gestion 2 December 2016 Online at https://mpra.ub.uni-muenchen.de/75391/ MPRA Paper No. 75391, posted 4 December 2016 06:04 UTC IMPACT OF THE TRANSITION TO CONTINUOUS TRADING ON EMERGING FINANCIAL MARKET’S LIQUIDITY : CASE STUDY OF WEST AFRICA REGIONAL EXCHANGE MARKET (BRVM) Aboudou OUATTARA, Assistant professor in finance1 African Center for Advanced Studies in Management (CESAG) Dakar, november 2016 SUMMARY After 18 years of activities and take-off difficulties due to socio-economic and political environment of the WAEMU zone, the west Africa regional exchange market (BRVM)’s authorities decided to move to continuous trading. The decision was effective on 16th september 2013. This action, beyond the upgrading of this stock exchange market to international standards, aims at improving market liquidity. Two years after its implementation, it seemed interesting to question the relevancy of this decision. In this empirical research, we are interested in evaluating the impact of the transition to continuous trading on market liquidity. Based on data collected from daily trading report and available databases, we mobilized the instrumental variables method to identify the part of the observed variation in liquidity due to the quotation mode change. This method was applied to evaluate the change in trading volume, TurnOver ratio, Martins index, Amihud ratio, Hui Heubel ratio and market impact due to quotation mode change. -

Lieux Exécution 201904

VENUE NAME VENUE SHORTNAME MIC COUNTRY ZONE ASSET CLASS TYPE * WIENER BOERSE WB XWBO AUSTRIA EUROPE SECURITIES RM NYSE EURONEXT BRUSSELS ENXBE XBRU BELGIUM EUROPE ETD & SECURITIES RM PRAGUE STOCK EXCHANGE PSE XPRA CZECH REPUBLIC EUROPE SECURITIES RM NASDAQ COPENHAGEN OMX DK XCSE DENMARK EUROPE ETD & SECURITIES RM NASDAQ HELSINKI OMX FI XHEL FINLAND EUROPE SECURITIES RM NYSE EURONEXT PARIS ENXFR XPAR FRANCE EUROPE ETD & SECURITIES RM BOERSE BERLIN BERLIN XBER GERMANY EUROPE SECURITIES RM BOERSE DUESSELDORF DUSSELDORF XDUS GERMANY EUROPE SECURITIES RM BOERSE MUENCHEN MUNICH XMUN GERMANY EUROPE SECURITIES RM BOERSE STUTTGART STUTTGART XSTU GERMANY EUROPE SECURITIES RM DEUTSCHE BOERSE DEUTSCHE BOERSE XFRA GERMANY EUROPE SECURITIES RM DEUTSCHE BOERSE AG FRANCFORT XFRA GERMANY EUROPE SECURITIES RM EQUIDUCT EQUIDUCT XBER GERMANY EUROPE SECURITIES RM EUREX DEUTSCHLAND EUREX XEUR GERMANY EUROPE ETD RM HANSEATISCHE WERTPAPIERBOERSE HAMBURG HAMBOURG XHAM GERMANY EUROPE SECURITIES RM NIEDERSAECHSISCHE BOERSE ZU HANNOVER HANOVRE XHAN GERMANY EUROPE SECURITIES RM ATHENS EXCHANGE ATHEX XATH GREECE EUROPE SECURITIES RM NASDAQ OMX ICELAND OMX IC XICE ICELAND EUROPE SECURITIES RM EURONEXT DUBLIN ENXIE XDUB IRELAND EUROPE SECURITIES RM BORSA ITALIANA BORSA ITALIANA XMIL ITALY EUROPE ETD & SECURITIES RM LONDON METAL EXCHANGE LME XLME LONDON EUROPE ETD RM EURO MTF EURO MTF XLUX LUXEMBOURG EUROPE SECURITIES MTF LUXEMBOURG STOCK EXCHANGE BDL XLUX LUXEMBOURG EUROPE SECURITIES RM FISH POOL FISH FISH NORWAY EUROPE ETD RM NASDAQ OMX COMMODITIES OMX CO NORX NORWAY -

Israel Chemicals Ltd. Notice of 2020 Annual General Meeting of Shareholders

ISRAEL CHEMICALS LTD. NOTICE OF 2020 ANNUAL GENERAL MEETING OF SHAREHOLDERS Notice is hereby given that the 2020 Annual General Meeting of Shareholders (the “Meeting”) of Israel Chemicals Ltd. (the “Company”) will be held on Thursday, April 23, 2020, at 10:00 a.m. (Israel time), at the offices of the Company, Millennium Tower, 23 Aranha Street, 22nd Floor, Tel Aviv, Israel, for the following purposes: (1) Election of Yoav Doppelt, Aviad Kaufman, Avisar Paz, Sagi Kabla, Ovadia Eli, Reem Aminoach, Lior Reitblatt and Tzipi Ozer Armon to serve as directors, effective as of the date of the Meeting, until the next annual general meeting of shareholders of the Company or until any of their earlier resignation or removal; (2) Reappointment of Somekh Chaikin, a Member Firm of KPMG International, as the Company’s independent auditor until the next annual general meeting of shareholders of the Company; (3) Approval of the award of equity-based compensation, consisting of restricted shares, to each director (who is not an officer or director of Israel Corporation Ltd.) serving in such capacity immediately following the Meeting, and to each other such director who may be duly appointed subsequent to the Meeting by the Company’s Board of Directors in 2020 (if any); and (4) Approval of an amendment to the Company’s Memorandum of Association and Articles of Association, to facilitate a change in the Company's formal name to "ICL" or to a similar name. At the Meeting, we will also present and discuss our audited financial statements for the year ended December 31, 2019 as previously made available to our shareholders as part of our Annual Report on Form 20-F for the year ended December 31, 2019, filed with the Securities and Exchange Commission (the “SEC”) on March 5, 2020, which may be accessed at www.sec.gov and via the “Investor” section of our Company’s website, www.icl-group.com, and as published on Magna (reference number 2020-02-018772). -

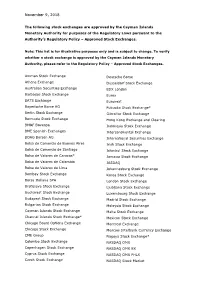

The List of Approved Stock Exchanges

November 9, 2018 The following stock exchanges are approved by the Cayman Islands Monetary Authority for purposes of the Regulatory Laws pursuant to the Authority’s Regulatory Policy – Approved Stock Exchanges. Note: This list is for illustrative purposes only and is subject to change. To verify whether a stock exchange is approved by the Cayman Islands Monetary Authority, please refer to the Regulatory Policy – Approved Stock Exchanges. Amman Stock Exchange Deutsche Borse Athens Exchange Dusseldorf Stock Exchange Australian Securities Exchange EDX London Barbados Stock Exchange Eurex BATS Exchange Euronext Bayerische Borse AG Fukuoka Stock Exchange* Berlin Stock Exchange Gibraltar Stock Exchange Bermuda Stock Exchange Hong Kong Exchange and Clearing BM&F Bovespa Indonesia Stock Exchange BME Spanish Exchanges Intercontinental Exchange BOAG Borsen AG International Securities Exchange Bolsa de Comercio de Buenos Aires Irish Stock Exchange Bolsa de Comercio de Santiago Istanbul Stock Exchange Bolsa de Valores de Caracas* Jamaica Stock Exchange Bolsa de Valores de Colombia JASDAQ Bolsa de Valores de Lima Johannesburg Stock Exchange Bombay Stock Exchange Korea Stock Exchange Borsa Italiana SPA London Stock Exchange Bratislava Stock Exchange Ljubljana Stock Exchange Bucharest Stock Exchange Luxembourg Stock Exchange Budapest Stock Exchange Madrid Stock Exchange Bulgarian Stock Exchange Malaysia Stock Exchange Cayman Islands Stock Exchange Malta Stock Exchange Channel Islands Stock Exchange* Mexican Stock Exchange Chicago Board Options Exchange -

US Assistance for the West Bank and Gaza for Fiscal Years 2012-2014

United States Government Accountability Office Report to Congressional Committees September 2015 FOREIGN AID U.S. Assistance for the West Bank and Gaza for Fiscal Years 2012-2014 GAO-15-823 September 2015 FOREIGN AID U.S. Assistance for the West Bank and Gaza for Fiscal Years 2012-2014 Highlights of GAO-15-823, a report to congressional committees Why GAO Did This Study What GAO Found Since 1993, the U.S. government has As of June 30, 2015, the U.S. Agency for International Development (USAID) committed more than $5 billion in had allocated about $1.1 billion of Economic Support Fund (ESF) assistance for bilateral assistance to the Palestinians the West Bank and Gaza for fiscal years 2012 through 2014, had obligated about in the West Bank and Gaza. $1 billion (94 percent), and had expended about $874 million (77 percent). Assistance to the Palestinians is a key Project assistance in five development sectors—for example, the water part of the United States’ commitment resources and infrastructure sector and the democracy and governance sector— to a negotiated two-state solution to accounted for approximately $619 million of the obligated funds, and cash promote peace in the Middle East. transfer assistance to the Palestinian Authority (PA) and its creditors accounted USAID is primarily responsible for for $448 million. Of this amount, $348 million went directly to the PA and then to administering ESF assistance for the its creditors and $100 million went directly to its creditors—two Israeli fuel West Bank and Gaza. companies, and six hospitals in East Jerusalem—through a line of credit. -

List of Approved Regulated Stock Exchanges

Index Governance LIST OF APPROVED REGULATED STOCK EXCHANGES The following announcement applies to all equity indices calculated and owned by Solactive AG (“Solactive”). With respect to the term “regulated stock exchange” as widely used throughout the guidelines of our Indices, Solactive has decided to apply following definition: A Regulated Stock Exchange must – to be approved by Solactive for the purpose calculation of its indices - fulfil a set of criteria to enable foreign investors to trade listed shares without undue restrictions. Solactive will regularly review and update a list of eligible Regulated Stock Exchanges which at least 1) are Regulated Markets comparable to the definition in Art. 4(1) 21 of Directive 2014/65/EU, except Title III thereof; and 2) provide for an investor registration procedure, if any, not unduly restricting foreign investors. Other factors taken into account are the limits on foreign ownership, if any, imposed by the jurisdiction in which the Regulated Stock Exchange is located and other factors related to market accessibility and investability. Using above definition, Solactive has evaluated the global stock exchanges and decided to include the following in its List of Approved Regulated Stock Exchanges. This List will henceforth be used for calculating all of Solactive’s equity indices and will be reviewed and updated, if necessary, at least annually. List of Approved Regulated Stock Exchanges (February 2017): Argentina Bosnia and Herzegovina Bolsa de Comercio de Buenos Aires Banja Luka Stock Exchange -

Bluestar Israel Equity Update First Quarter 2014

BlueStar Israel Equity Update First Quarter 2014 Q4 2013 in Review & 2014 Outlook All major global developed market equity benchmarks rose strongly in Q4 2013 despite the announcement of the Federal Reserve’s intentions to reduce the scope of its bond purchase What’s Inside program The BlueStar Israel Global Index rose 10.54% in Q4 2013 on an annualized basis while the TA-100 and MSCI Israel indices were up 7.38% and 6.34%, respectively. The BlueStar 1. Israeli Global benchmark also outperformed the TA-100 and MSCI Israel benchmarks for the full year 2013 by 4 and 15 percentage points, respectively. Equities in Q4 2013 For the second straight quarter the rally in Israeli equities was broad based and in each of the three largest sectors: Information Technology, Financials and Health Care. Additionally a long-awaited recovery in the telecom sector took hold during the quarter. Each of these sectors rose strongly during Q4 2013 indicating strength in the domestic economy and an 2.-6. About the BIGI & acceleration in the growth rates of the economies of Israel’s largest trading partners. BIGTech Indexes, The Israeli government budget deficit continued to shrink bringing on the prospect of lower Rebalance Review, taxes and higher government spending in 2014. The labor force participation rate rose in the and Risk/Return fourth quarter while the unemployment rate remained low. Data The revival in trading volume on the TASE, rise in equity prices in most developed countries, and several relatively large IPOs by Israeli companies during the second half of 2014 resulted in a net addition of 12 companies in the BlueStar Israel Global Index’s December rebalance. -

Bofa List of Execution Venues

This List of Execution Venues and the associated Bank of America EMEA Order Execution Policy Summary form part of the General Terms & Conditions of Business available on the Bank of America MifID II Website www.bofaml.com/mifid2 The tables below set out the execution venues accessed by entities in the Bank of America Entities List and Associated Companies. These tables are not exhaustive and we may amend them from time to time in accordance with our policies. MLI and BofASE may also use other execution venues from time to time where they deem appropriate but in accordance with their policies (including the Bank of America Order Execution Policy). Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA Aquis UK Equities EMEA Athex Group Equities EMEA Bloomberg BV Equities EMEA Bloomberg UK Equities EMEA Borsa Italiana Equities EMEA Cboe BV Equities EMEA Cboe UK Equities EMEA Deutsche Borse Xetra Equities EMEA Equiduct Equities EMEA Euronext Amsterdam Equities EMEA Euronext Brussels Equities EMEA Euronext Dublin Equities EMEA Euronext Lisbon Equities EMEA Euronext Oslo Equities EMEA Euronext Paris Equities EMEA ITG Posit Equities EMEA Liquidnet Equities EMEA Liquidnet Europe Equities EMEA London Stock Exchange 1 – ©2020 Bank of America Corporation Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA NASDAQ OMX Nordic – Helsinki Equities EMEA NASDAQ OMX Nordic – Stockholm Equities EMEA NASDAQ OMX