Sysmex Corporation and Its Subsidiaries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sysmex Report

Sysmex Report2016 Sysmex Report 2016 For the year ended March 31, 2016 1-5-1 Wakinohama-Kaigandori, Chuo-ku, Kobe 651-0073, Japan Tel +81 (78) 265-0500 Fax +81 (78) 265-0524 www.sysmex.co.jp/en/ This brochure was printed in Japan on FSC R-certified paper using vegetable oil ink. Shaping the advancement of healthcare. Sysmex aims to contribute to the health of people around the world by creating new value. Shaping the advancement of healthcare. We continue to create unique and innovative values, while building trust and confi dence. With passion and fl exibility, we demonstrate our individual competence and unsurpassed teamwork. Core Behaviors To Our Customers We deliver reassurance to our customers, through unmatched quality, advanced technologies, superior support, and actions that consistently refl ect the viewpoint of our customers. We constantly look out for our customers’ true needs, and seek to generate new solutions to satisfy those needs. To Our Employees We honor diversity, respect the individuality of each employee, and provide them with a workplace where they can realize their full potential. We value the spirit of independence and challenge, provide employees with opportunities for self-fulfi llment and growth, and reward them for their accomplishments. To Our Business Partners We deliver commitment to our client companies through broad-ranging partnerships. We strive to be a company that can grow in step with our trade partners, through respect and mutual trust. To Our Shareholders Our shareholders can rest assured that we will continue to improve the soundness and transparency of our management policies, while promoting information disclosure and close communications. -

Announcement of Organizational and Personnel Changes

March 9, 2020 Sysmex Corporation Announcement of Organizational and Personnel Changes Sysmex Corporation (HQ: Kobe, Japan; Chairman and CEO: Hisashi Ietsugu) announces today its decision to implement organizational and personnel changes, effective April 1, 2020, as detailed below. Targeting sustainable growth for the Group, the organizational changes aim to enhance the business development structure to accelerate strategy deployment and reinforce the Group’s governance structure to enhance management quality. 1. Organizational Changes (1) Reinforcing the Business Development Structure 1) Augmenting Functions Related to Sales, Services and IT Products Leveraging Next- Generation Information Technologies · We will establish the Caresphere Innovation Division to spearhead planning and promotion with a view to fostering digital innovation in the sales, service and IT domains by leveraging our Caresphere™ network solution. 2) Strengthening Clinical Development Capabilities in the Life Science (LS) Field · In the aim of accelerating the provision of products and services with new diagnostic technologies, we will establish the LS Medical Affairs Division within the LS Business Unit. The new division will strategically plan and promote clinical performance testing within the scope of obtaining approval to manufacture and sell in vitro diagnostic pharmaceuticals (regulatory approval). (2) Buttressing the Global Governance Structure 1) Reinforcing the Group Governance Function to Enhance Management Quality · To realize a governance function that -

Sysmex America Customer Story

SYSMEX AMERICA CUSTOMER STORY DIGITALLY TRANSFORMING AP INTO A HIGH-VALUE, HIGH-VISIBILITY OPERATION ABOUT SYSMEX As a company on the leading edge of diagnostic healthcare sit in on sessions with actual customers and hear how they Industry: Medical Device Manufacturing solutions, Sysmex America has experienced double-digit used Esker. The product spoke for itself.” ERP: SAP® growth rates for an extended period of time. Unfortunately, Solution: Accounts Payable this success also exposed some of the outdated processes Sysmex America, Inc., the U.S. and systems inhibiting greater operational improvements — SPEED, SIMPLICITY & CENTRALIZATION headquarters of Sysmex Corporation specifically, within accounts payable (AP). Approximately 25% of the AP invoices Sysmex processes (Kobe, Japan), is a world leader in Today, Sysmex electronically processes 2,200+ monthly each day arrive via mail or email. Prior to Esker, these clinical laboratory systemization and invoices were handled manually, which forced staff to focus solutions, including clinical diagnostics, invoices through Esker’s Accounts Payable solution via ® most of their time on low-value tasks like data entry and automation and information systems. seamless integration with the company’s SAP software Serving customers for over 40 years, system. Driven by intelligent data extraction, electronic chasing down invoice approvals. To make matters worse, Sysmex focuses on extending the workflow management and reporting capabilities, Esker’s everyone at Sysmex was responsible for creating their own boundaries of diagnostic science while solution not only allows Sysmex employees to focus more on goods receipt, making tracking nearly impossible. providing the management information high-value tasks, it has also transformed how managers run “The manual nature of our previous process didn’t leave us tools that make a real difference in their day-to-day operations thanks to the added oversight. -

Helping Our Customers Every Step of the Way Keep This Tab for Easy Access to Customer and Technical Assistance Numbers

Helping our Customers Every Step of the Way Keep this tab for easy access to customer and technical assistance numbers. Customer Service Hotline For more information, please contact your Customer Service Representative. 1-800-462-1262 (U.S.) 1-888-479-7639 (Canada) Technical Assistance Hotline For technical assistance, our hotline is available 24/7. For all other purposes, use the Toll-free Customer Service Number. 1-888-879-7639 Customer Satisfaction is Our Goal… Welcome to Sysmex Congratulations on purchasing your Sysmex analyzer! Now that your instruments have been installed, your medical technologists have been trained, and you are ready to begin using your analyzer(s), it’s time to talk to your Customer Service Representative. This folder contains important information to walk you through your next steps as a Sysmex customer. Please take some time to review the information so you become familiar with the various ways in which Sysmex can support you — now and in the future. The business card for your Primary Customer Service Representative is attached. Please utilize the fax number and email address located on the business card to contact us electronically or to send us your purchase orders. Representatives are also available by phone. Obtaining Reagents and Controls* Customer Resource Center (CRC) Reagents and Controls can Please visit the Sysmex CRC to register or log in at: be obtained in two ways www.sysmex.com/us (US) or — via standing order, or by supplemental orders. www.sysmex.com/ca (Canada) By placing a standing Once registered, you will have 24-hour access order you will reduce to a wide range of information, including: paperwork, directly reduce your shipping costs, reduce potential for inventory shortages and help • Online Training • CLSI-formatted assure order accuracy. -

Sysmex Report 2018 Sysmex 31, 2018 Ended March the Year For

Sysmex Report 2018 Sysmex Report 2018 For the year ended March 31, 2018 1-5-1 Wakinohama-Kaigandori, Chuo-ku, Kobe 651-0073, Japan Tel +81 (78) 265-0500 Fax +81 (78) 265-0524 www.sysmex.co.jp/en/ This brochure was printed in Japan on FSC R-certified paper using non-VOC ink. Lighting the way with diagnostics Lighting the way with diagnostics Sysmex enhances diagnostic value with innovative testing, to bring greater trust and confidence to healthcare. Sysmex operates in the domain of healthcare testing, which involves examining blood, urine and other samples. We provide customers with a variety of products and services, in more than 190 countries and regions. Looking toward the future of healthcare, we are now undertaking new challenges in the field of diagnostics. 1 Sysmex Report 2018 Sysmex Report 2018 2 Corporate Philosophy for the Sysmex Group In line with changes in the global management environment, in we formulated a corporate philosophy for the Sysmex Group, carrying forward and expanding the perspective maintained since the time of our founding. Shaping the advancement of healthcare. We continue to create unique and innovative values, while building trust and confidence. With passion and flexibility, we demonstrate Our founder, Taro Nakatani (right), setting off on his visit to the United States our individual competence and unsurpassed teamwork. An Ideal Unchanged Since Our Founding Dedicated to Supporting People’s Health Our Core Behaviors In , Sysmex founder Taro Nakatani visited the United States, looking for new business ideas. His attention was drawn to the field of medical electronic devices. When he returned to Japan, Mr. -

Sysmex and Biomérieux Form a Global Partnership - Biomérieux Cor

Sysmex and bioMérieux Form a Global Partnership - bioMérieux Cor... http://www.biomerieux.com/servlet/srt/bio/global/printContent?node... Press Releases Sysmex and bioMérieux Form a Global Partnership Kobe (Japan), Marcy l'Etoile (France) - July 2, 2007. Sysmex Corporation (HQ: Kobe, Japan; President: Hisashi Ietsugu) and bioMérieux (Euronext: BIM) have signed an agreement today by which bioMérieux will become Sysmex’s global partner for distributing its UF-1000i urinalysis system in microbiology laboratories. This synergistic partnership between two major players in the in vitro diagnostic market brings together Sysmex’s recognized expertise in diagnostic analyzers and bioMérieux’s leadership position in microbiology. Current urinary screening methods, mainly based on microscope cell numeration, are still very manual, time-consuming and the source of errors. Sysmex has developed the fluorescence flow cytometry UF-1000i urinalysis system, a highly standardized and automated solution. bioMérieux will provide its extensive customer base with this new technology and leverage its expertise and reputation in microbiology to expand the market. Commercialization by bioMérieux will start in Europe in September 2007 and be followed by the U.S. and other countries at the beginning of 2008. “We are delighted with this very promising partnership with Sysmex, which will allow us to bring the gold standard for urinary screening to our customers”, said Mr. Stéphane Bancel, Chief Executive Officer of bioMérieux. “Sysmex’s UF-1000i perfectly complements our current offer. With this system and the forthcoming plate streaker instrument, bioMérieux has added two important pieces to the microbiology lab automation process since announcing its 2012 strategy last January”, he added. -

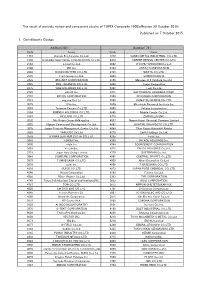

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Technical Services You Invested in Sysmex for Quality, Accuracy, Reliability and Functionality

Technical Services You Invested in Sysmex for Quality, Accuracy, Reliability and Functionality. Safeguard Your Investment With Sysmex Technical Service That Exceeds Your Expectations. Achieve your operational goals and objectives with responsive, comprehensive technical support for Sysmex instrument systems and software. Depend on Sysmex Just as you rely on Sysmex hardware and software for reliability, innovation and automation, you can depend on Sysmex Technical Support for leading edge, flexible service solutions to meet your requirements. H E O How Are We Different? T T O l M In E R E Consistently ranked #1 in service by our customers through independent surveys,* Sysmex’s unique and comprehensive service expands your peace of mind through: • On site response – prompt, highly qualified • Hotline – quick, experienced phone support E • Field upgrades – hardware and software F S I E n • Remote, secure internet access between l O D P U S P E your lab and our 24/7 staff for proactive G R R TE A SI instrument monitoring, automated DE n S O peer-comparison and easy calibration verification Our Qualifications Our skilled field service representatives are committed to keeping your laboratory operating at peak performance levels. Every member of this team has participated in more than 100 hours of hands-on, professional classroom training and has extensive experience in servicing Sysmex instruments. They continuously update their skills and product knowledge by participating in our mandatory training programs. Independent data shows that we have the best first-time repair rate and service response time in the industry.* *Ranked #1 by IMV ServiceTrak™ 2009. -

XS- I ™ Automated Hematology Analyzer

MKT-10-1139:MKT-10-1139 1/27/11 1:14 PM Page 1 XS- ,+++ i ™ Automated Hematology Analyzer Small Footprint. Big Difference. MKT-10-1139:MKT-10-1139 1/27/11 1:14 PM Page 2 Small But Powerful: The XS-,+++i Even with these challenges, the need for hematology testing has remained steady or continues to grow. Laboratories are searching for hematology analyzers that can improve productivity and efficiency while providing enhanced clinical information. Designed to be reliable and efficient, the Sysmex XS-1000i offers laboratories an automated hematology system that can truly meet and exceed their expectations. The XS-1000i streamlines your workflow by providing testing for up to 60 samples per hour, enabling rapid turnaround time. XS-1000i without Auto Sampler Today’s Laboratory Challenges Proven Technology Laboratories have continued to face a number of The proven technologies – Fluorescent Flow Cytometry, challenges for several years. These include clinical, Hydrodynamic Focusing and Non-cyanide Hemoglobin – operational and financial issues such as: of the XE and XT-Series have been incorporated into the XS-1000i Automated Hematology Analyzer. • Demand for clinically relevant information • Medical technologist labor shortage Leading-edge hematology diagnostics requiring • Increased workload only four feet of counter space: • Need for faster turnaround time • Requirement for high reliability • Effective diagnostic capabilities utilizing • Limited laboratory budgets fluorescent flow cytometry • CBC with 5-part differential • Simplicity in operation for streamlined workflow • Standardization across Sysmex platforms • Proven reliability as a member of the X-Series of products 1 MKT-10-1139:MKT-10-1139 1/27/11 1:14 PM Page 3 Improved Clinically Relevant Results with XS-Series Technology Rapid Results The XS-1000i provides rapid, reliable test results from just 20µL of sample for assistance in patient diagnosis and therapeutic monitoring. -

New Zealand Journal of Medical Laboratory Science Is the Offi Cial Publication of the New Zealand Institute of Medical Bernard Chambers

,661 9ROXPH1XPEHU1RYHPEHU blis sta he E d 1HZ=HDODQG -RXUQDORI i n 1946 0HGLFDO /DERUDWRU\ 6FLHQFH 2IILFLDO3XEOLFDWLRQRIWKH 1HZ=HDODQG,QVWLWXWHRI 0HGLFDO/DERUDWRU\6FLHQFH ,QFRUSRUDWHG HIT range - 07/2012 - Photo: Eric Meola/Gettyimages ©2010 Diagnostica Stago All rights reserved www.epicea.com STic Expert® HIT For suspected Heparin Induced Thrombocytopenia Allows exclusion of HIT when combined with the pretest clinical score IgG specific Unitary test, very easy to use Result available in 10 minutes Editor Rob Siebers, PGCertPH FNZIC FNZIMLS CBiol CSci FSB, University of New Zealand Journal of Otago, Wellington Deputy Editor Terry Taylor, BSc DipMLS MNZIMLS, Southern Community Laboratories, Dunedin Board Members Chris Kendrick, GradDipSc MSc MNZIMLS, Massey University, Palmerston North Michael Legge, PhD MSB FIBMS FNZIMLS FFSc(RCPA), University of Volume 66 Number 3 Otago, Dunedin November 2012 Holly Perry, MAppSc(Hons) DipMLT MNZIMLS, Auckland University of Technology ISSN 1171-0195 Cat Ronayne, BMLSc DipGrad MNZIMLS, University of Otago, Dunedin John Sterling, BSc(Hons) MLett AFRCPA MAIMS FRMS, SA Pathology, TH Pullar Memorial Address Adelaide Pathology: The study of structure and function in health and Ann Thornton, CertMS FNZIMLS, University of Otago, Wellington Tony Woods, BA BSc(Hons) PhD MAIMS FFSc(RCPA), University of diseases South Australia, Adelaide Robin Fraser ................................................................................67-69 Statistical Editor Original article Nevil Pierse, PhD, University of Otago, Wellington Evaluation of the new red cell research parameters on the Sysmex About the Journal XE-5000 The New Zealand Journal of Medical Laboratory Science is the offi cial publication of the New Zealand Institute of Medical Bernard Chambers ............................................................................70-72 Laboratory Science (NZIMLS) who owns the copyright. -

Sysmex and Biomérieux Agreed to Dissolve the Joint Venture Sysmex Biomérieux Co., Ltd

Sysmex and bioMérieux Agreed to Dissolve the Joint Venture Sysmex bioMérieux Co., Ltd. Kobe (Japan) and Marcy l’Etoile (France) – July 27, 2017 - Sysmex Corporation (“Sysmex”) and bioMérieux S.A. (“bioMérieux”) announce they have agreed to transfer all of Sysmex’ holdings in Sysmex bioMérieux Co., Ltd. (Tokyo, Japan) to bioMérieux thereby dissolving the joint venture created by and between the two companies in 2008 with the goal of bringing together bioMérieux’s innovative business and Sysmex’ expertise of the Japanese market. 1. Agreement on the Matter In discussions between Sysmex and bioMérieux, an agreement was reached by which Sysmex will transfer all of its holdings in Sysmex bioMérieux (34% of shares) to bioMérieux. As a consequence of the dissolution, the distribution agreement relating to the distribution of bioMérieux products in Japan between Sysmex and Sysmex bioMérieux will also terminate as of October 31, 2017. Sysmex will continue to provide customer service in Japan for bioMérieux products until March 31, 2018. Subsequently, bioMérieux will build its commercial structure in Japan for the long term to take over the activities previously led by Sysmex. 2. Overview of the Joint Venture (1) Name: Sysmex bioMérieux Co., Ltd. (2) Location: 1-2-2 Osaki, Shinagawa-ku, Tokyo (3) Representative: Kentaro Yoshida (4) Business: Manufacture and sale of in vitro diagnostic reagents and medical instruments related to microbes, genes and immunochemistry (5) Capital: 480 million JPY (6) Ownership: bioMérieux S.A. 66.0% Sysmex Corporation 34.0% (7) Established: October 4, 1988 3. Share Transfer Date October 31, 2017 (scheduled) About Sysmex Sysmex Corporation is a world leader in clinical laboratory systemization and solutions, including laboratory diagnostics, laboratory automation and clinical information systems. -

KX-21N Hematology Analyzer Results You Can Trust! KX-21N Hematology Analyzer

KX-21N Hematology Analyzer Results you can trust! KX-21N Hematology Analyzer Innovative technology • Performs rapid and accurate analysis of 17 parameters • Utilizes same Direct Current detection method as Sysmex high-end systems • Produces accurate results comparable to other Sysmex hematology analyzers Compact and fully integrated • Ideal as back-up for Sysmex 5-part differential systems • Small footprint • Fits easily on a laboratory bench or table Accurate and reliable • Sysmex robustness for the best possible up-time • Sensitive flagging to support diagnosis • Quality Assurance Program Easy operation and maintenance • Minimal training required • Simple menus • Push-button technology Safe and secure • Non-toxic, biodegradable reagents • Reliable results for clinician’s and patient’s peace of mind Network capability via your LIS With its simplified operations, the Sysmex KX-21N is ideal for clinic satellite lab or research testing. The KX-21N hematology analyzer provides 17 reportable parameters including a 3-part WBC differential, plus histograms for RBC, PLT and WBC. It provides a high level of accuracy through the use of automatic floating discriminators. Built on reliable, Sysmex technology, it features a simple start-up function, single button selection for sampling and daily maintenance, in a space-saving, compact design. KX-21N Hematology Analyzer KX-21N Specifications Detection Principles RBC, PLT Direct Current (DC) detection method WBC DC detection method HGB Non-cyanide method HCT Cumulative pulse height detection method