S P E C I a L R E P O

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Use of Remote Sensing and Geographic Information System in Land Use Management in Karu, Nasarawa State, Nigeria

THE USE OF REMOTE SENSING AND GEOGRAPHIC INFORMATION SYSTEM IN LAND USE MANAGEMENT IN KARU, NASARAWA STATE, NIGERIA BY JONAH, KUNDA JOSHUA M.Sc/SCIE/05624/2009/2010 A DISSERTATION SUBMITTED TO THE POSTGRADUATE SCHOOL, AHMADU BELLO UNIVERSITY, ZARIA, NIGERIA IN PARTIAL FULFILLMENT FOR THE AWARD OF MASTERS IN REMOTE SENSING AND GEOGRAPHIC INFORMATION SYSTEM DEPARTMENT OF GEOGRAPHY, AHMADU BELLO UNIVERSITY, ZARIA, NIGERIA APRIL, 2014 1 THE USE OF REMOTE SENSING AND GEOGRAPHIC INFORMATION SYSTEM IN LAND USE MANAGEMENT IN KARU, NASARAWA STATE, NIGERIA BY JONAH KUNDA JOSHUA M.Sc/SCIE/05624/2009/2010 A DISSERTATION SUBMITTED TO THE POSTGRADUATE SCHOOL, AHMADU BELLO UNIVERSITY, ZARIA, NIGERIA IN PARTIAL FULFILLMENT FOR THE AWARD OF MASTERS IN REMOTE SENSING AND GEOGRAPHIC INFORMATION SYSTEM DEPARTMENT OF GEOGRAPHY, AHMADU BELLO UNIVERSITY, ZARIA, NIGERIA APRIL, 2014 2 DECLARATION I declare that the work in the dissertation entitled “The Use of Remote Sensing and Geographic Information System in Land Use Management in Karu, Nasarawa State, Nigeria” has been performed by me in the Department of Geography under the supervision of Prof. EO Iguisi and Dr. DN Jeb. The information derived from the literature has been duly acknowledged in the text and list of references provided. No part of this dissertation was previously presented for another degree or diploma at any university. Jonah Kunda Joshua --------------------------- -------------------------- Signature Date 3 CERTIFICATION This thesis entitled “THE USE OF REMOTE SENSING AND GEOGRAPHIC INFORMATION SYSTEM IN LAND USE MANAGEMENT IN KARU, NASARAWA STATE, NIGERIA” by Jonah Kunda Joshua meets the regulations governing the award of the degree of MASTERS of Remote Sensing and Geographic Information System, Ahmadu Bello University, Zaria and is approved for its contribution to knowledge and literary presentation. -

Annual Report of the Colonies, Northern Nigeria, 1911

COLONIAL REPORTS—ANNUAL • • No. 788, NOBTHERN NIGERIA* REPORT fOn 1911. (For Report for 1910-11, see No. 704.) $xt*mttb to both %wi»t» at $*xlhmtnt fcg fcoromani *f P§ JR*)**tg» November, 10ft. LONDON: PUBLISHED BY HIS MAJESTY'S STATIONERY OFFICE. To be purchased, either directly or through any Bookseller, from WYMAN AND SONS, LIMITED, Fmn LANE, E.C., and 32, ABINGDON STREET, S.W., or H.M. STATIONERY OFFICE (SCOTTISH BRJLNCH), 23, FORTH STRUT, EDINBURGH ; or E. PONSONBY, LIMITED, 116. GRAFTON STRUT, Drawn; or from the Agencies in the British Colonies sad Dependencies, the United States of America, the Continent of Europe and Abroad of T. FISHER UNWIN, LONDON, W.d PRINTED BY DARLING AND SON, LTD., BACON STREET, E. bis. [CU. 6007-*$.] Price tyi Page H.—TRADE AND CUSTOMS ... ... ... ... .. ... 8 III.—LEGISLATION AND JUDICIAL ... ... 'M 8 IV.—OAMTOlfMBETS 11 VI.—HOSPITALS . ... ... ... ... ••• is VH^Btetis DEPARTMENT ... ... ... ... ... 13 mi.—POLICE ..< ... ... .... ... ... ... 16 IX.—PRISONS ... ... ... ... ... ... ... *•• 1& X.—CRIMINAL STATISTICS ... ... ... ... ... W XI.—VITAL STATISTICS ... ... ... ... ... ... ... *.• XII.—SANITATIOK ... ... ... ... ... ... ... ... 18 XHI.—VACCINATION ... ... sc. ... •** 19 XIV.—METEOROLOGY ... .<*. ... ... ... ... ... 20 XV.—POST AND TELEGRAPHS SERVICES ... ... ... ... 20 XVL—MILITARY ... ... ... , 21 XVII—MEANS OF COMMUNICATION ... 22 XVIII.—'RAILWAYS ... ... ... ..«* ... ... ... ... 24 XIX,—PUBLIC WORKS ... ... ... ... ... ... ... 25 XX.—PROVINCIAL ADMINISTRATION ... ... ... ... ... 26 APPRNDIX I.—REPORT ON INVESTIGATIONS CONDUCTED AT THE SI IMPERIAL INSTITUTE DURING 1911. APPENDIX II—BAEO-KANO RAILWAY ... 82 o TABLE I.—PROVINCIAL STATISTICS 86 TABLE II.—COST OP PROVINCIAL ADMINIBTBATION, &C. ... ... 88 TABLE III.-—BEIT-E^-MAL ... ... ... ... ... ... * ... 88 TABLE IV.—STATEMENT ot RECEIPTS (GOVERNMENT SHARE) PROM 89 LOCAL REVENUE. No. 738. NORTHERN NIGERIA. (For Report for 1910-11, see No. 704.) THE ACTING GOVEBKOB to THE SECRETARY OP STATE. -

Improved Quality of Rice Processing (NIG 225)

Winrock International Nigeria Farmer-to-Farmer Program Improved Quality of Rice Processing (NIG 225) Consultant Report: Richard (Dick) Tinsley1 Professor Emeritus, Colorado State University July 2011 1 http://lamar.colostate.edu/~rtinsley/Author.htm Table of Contents Table of Contents. i List of Figures . ii List of Tables. ii List of Acronyms. iii Executive Summary. iv Introduction . 1 Time of Consultancy . 2 Rice Production . 3 AADIL . 5 Limitations of Agronomy . 6 Estate Mode . 7 Chisel Plows . 8 Support Services . 8 Full Water Control . 9 Rice Value Chain . 10 Parboiling . 11 Rice Quality . 13 Paddy Results . 13 Parboiled Rice . .15 Raw Rice . 16 Milling . 17 Other Ways to Improve Quality & Recovery . 19 Small Combines . 20 Winnowing Machines . 21 Other Concerns to Consider . 21 Value Added vs. Outsourcing . 21 Basic Business Model . 22 Access to Mechanization . 23 Micro-Credit . 24 Summary and Recommendations . 24 Appendix Daily Activity Log . A – 1 Monthly Rainfall Varibility . A – 5 i List of Figures 1. Map of Nigeria with Adamawa State, and Yola in box . 1 2. Typical manual harvesting of rice in Ghana . 2 3. Intermediate deep water rice production system around Yola . 4 4. Destoner used to remove mud clods and stones from rice . 4 5. Section of a village used for buying paddy from farmers . .10 6. The parboiling process . 11 7. Larger vat used for parboiling rice and holding up to 10 bags . 12 8. Hotel staff assisting with separating head rice from brokens, etc. 13 9 Paddy samples showing degree of good paddy and trash . 14 10. Vietnamese women demonstrating how placing grain in the sun can help control weevils 14 11. -

Geographic Information System Approach in Evaluating Security Challenges to Critical Infrastructures

GEOGRAPHIC INFORMATION SYSTEM APPROACH IN EVALUATING SECURITY CHALLENGES TO CRITICAL INFRASTRUCTURES A. N. Jatong, PhD Department of Surveying and Geoinformatics, Federal Polytechnic Mubi PMB 35, Mubi, Adamawa state, Nigeria E-mail: [email protected] Abstract In the past, criminality was a taboo and almost everybody franked at it and thus security challenges were so minimal or non-existent. Unfortunately it has now become a means of livelihood or a means to address disagreements where lives as well as critical infrastructures are destroyed mindlessly. While there are recognized occasional natural security challenges such as volcanic eruptions, Hurricane Katrina among others, most frequent security challenges are man-made organized and executed with cut edge professionalism and sophistication. Conventional methods and hence measures of monitoring and addressing various man-made security challenges have in the past been adopted by security operatives but criminals have always responded with sophisticated countermeasures and overwhelming successes maiming and massively in most cases destroying badly needed critical infrastructures. The intention of this research is to adopt Geographic Information System (GIS) approach, a real- time and speedy as well as reliable approach to address real-time security challenges to lives and critical infrastructures. In this method the study area was subdivided into geographic cells and an evaluation on each cell from some chosen observation posts were analyzed in a GIS environment to establish intervisibility to identified target location(s) which includes human habitations, critical infrastructures among others. Advanced Spaceborne Thermal Emission and Reflection Radiometer (ASTER) Digital Elevation Model (DEM) was used as the platform for Line-Of-Sight (LOS) and Viewshed Analysis (VA).Observation points were selected on both high and lowlands. -

Mapping Poverty and Deprivation in Barikin-Sale, Minna, Nigeria

World Academics Journal of ______________________________________________ Research Paper . Management Vol.7, Issue.2, pp.54-59, December (2019) E-ISSN: 2321-905X Mapping Poverty and Deprivation in Barikin-Sale, Minna, Nigeria Isaac I.1*, Habila J.2, Salami H.3, Salami R.O.4, Abutu P.5 1Department of Urban and Regional Planning, Federal University of Technology, Minna 2Department of Urban and Regional Planning, Federal Polytechnic, Nekede, Imo State 3Department of Urban and Regional Planning, University of Ibadan 4,5University Library Services, Federal University of Technology, Minna *Corresponding Author: [email protected], Tel. +2349098575008 Available online at: www.isroset.org Received: 05/Dec/2019, Accepted: 20/Dec/2019, Online: 31/Dec/2019 Abstract- Poverty is a very serious problem facing currently bedevilling a large proportion of the global population. This problem is becoming intensified with the rapid rate of global population growth and unprecedented urbanisation. More worrisome is the fact that this phenomenon has translated into urbanisation of poverty. This study aimed at mapping poverty and deprivation in Barikin Sale neighbourhood of Minna, Nigeria; and the objectives are to obtain the base map of the study area, acquire data on household deprivation in the study area, assess the rate of deprivation in the neighbourhood and produce poverty maps of the study area. Barikin Sale was subdivided into 10 small areas which were termed sub-neighbourhoods which form the units of analysis and mapping. Ten households were randomly sampled from each sub-neighbourhood. Descriptive and inferential analyses were carried out and it was discovered that household deprivation is more obvious at sub- neighbourhoods level than at the general neighbourhood level. -

Geospatial Analysis of Flood Problems in Jimeta Riverine Community of Adamawa State, Nigeria

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by International Institute for Science, Technology and Education (IISTE): E-Journals Journal of Environment and Earth Science www.iiste.org ISSN 2224-3216 (Paper) ISSN 2225-0948 (Online) Vol.5, No.12, 2015 Geospatial Analysis of Flood Problems in Jimeta Riverine Community of Adamawa State, Nigeria Innocent E. Bello 1* Steve O. Ogedegbe 2 1. MP, IT and Data Management Dept., National Space Research and Development Agency (NASRDA), Obasanjo Space Centre, Airport Road, PMB 437 Garki, Abuja, Nigeria. 2. Department of Geography, College of Education, Igueben, Edo State, Nigeria Abstract Floods are among the most devastating natural disasters in the world, claiming more lives and causing more property damages than any other natural phenomena. In recent times, the incidence of flooding across Nigeria has left both the government and the governed devastated. It is no longer news that flooding and its attendant consequences are injurious to man while the spatial dimensions are often not mapped. This study, therefore, examined the nature of water level/extent and vulnerability in the riverine community of Jimeta, Adamawa State. Using time series analysis, four epoch satellite images covering the study area was used to evaluate the geospatial coverage of water along the watercourse of Upper Benue bordering the study area. Using ILWIS 3.8, ArcGIS 10.1 and statistical analysis, the spatial extent and vulnerability of settlements was mapped. Highly vulnerable (50m buffer) were differentiated from low risk zones (100m buffers). Study revealed that besides rainfall, excess water from Cameroun dam is largely responsible for the identified high level of inundation. -

Exxonmobil News (Edition 1 2017).Cdr

A publication of ExxonMobil affiliates in Nigeria ISSN 1597-0442 EDITION 1, 2017 Nolan O’Neal bows out, Paul McGrath steps in ExxonMobil discovers significant MPN bags Diamond oil offshore Nigeria Excellence Award NEWS CONTENTS ExxonMobil News ISSN: 1597-0442 Esso Exploration and Production Nigeria Limited (EEPNL) Esso Exploration and Production Nigeria (Offshore East) Limited Mobil Oil Nigeria Plc (MON) Mobil Producing Nigeria Unlimited (MPN) Edition 1, 2017 Chairman Managing Director, EEPNL & MPN and COMMUNITY RELATIONS Lead Country Manager Paul McGrath COVER Nolan O’Neal bows out, NNPC/MPN JV donates Chairman/Managing Director, MON Paul McGrath steps in 23million and water supply Adetunji A. Oyebanji 17 to communities and AKS 6 Schools Director, Lubricants & Specialties, MON A. J. MacNaughton Power Forward Program General Manager, Public & Government Affairs reaffirms EM commitment Paul C. Arinze 20 to Youth Empowerment Editor Oge Udeagha EM donates Geoscience West Saturn, the rig drilled Owowo textbooks, journals to Editorial Team 22 Varsities Ernest Omo-Ojo; Ozemoya Okordion; Patrick Utomi; Chukwuemeka Okonkwo Cover/Concept/Graphic Design Taiwo Ogunbiyi ExxonMobil discovers Registered Office NEWS EM discovers significant Mobil House, 1, Lekki Expressway, P.M.B 12054, oil offshore Nigeria Victoria Island, Lagos. significant oil offshore Nigeria 3 Published by Public & Government Affairs Department for Employees of ExxonMobil subsidiaries in Nigeria. EM wins West Africa’s Best in Company CSR, All correspondence to 4 The Editor, Public & Government Affairs Department, and the government on future sustainability Mobil Producing Nigeria Unlimited, Mobil House, xxonMobil Corporation recently The well was drilled 1, Lekki Expressway, P.M.B. 12054, Victoria Island, Ediscovered significant crude oil development plans." Lagos. -

Analysis of the Activities of Land Administration Machineries in Abuja and Minna, Nigeria

IOSR Journal Of Environmental Science, Toxicology And Food Technology (IOSR-JESTFT) e-ISSN: 2319-2402,p- ISSN: 2319-2399. Volume 8, Issue 1 Ver. VI (Feb. 2014), PP 31-38 www.iosrjournals.org Analysis of the Activities of Land Administration Machineries in Abuja and Minna, Nigeria 1Ayoola A. Babatunde, 2Kemiki O.A.(PhD),3S.Abdulkareem, 4F. Fabunmi Department of Estate Management & Valuation, Federal University of Technology, Minna, Niger State,Nigeria. Abstract: This study attempts to have a comparative analysis of the activities of land administration machineries in FCC, Abuja and Minna using some selected districts and neighbourhoodsas case study areas. Questionnaires were administered to Individual land owners, property developers or plot allottees who own land from ages Eighteen (18) and above as well as interview to somestaff of departments of land administration machineries in FCC, Abuja and Minna. Statistical Package for Social Scientists (SPSS), Geometric Mean Model and Linkert Scale were statistical tools employed. Findings revealed that the average growth in land allocations made available to people by government within the study period of 2000 – 2009 in FCC and Minna were191.25% and 29.22% respectively. In FCC, Delay of process and extortion of money by government officials are sufficient reasons why individual land owners will not be willing to process title documents to land. While in Minna, the reasons are Exorbitant Processing Cost, Delay of Process and extortion of money by government officials. The paper suggests among others that land administration officials should abstain from illegal acts during land transactions, government should ensure that adequate income packages are paid to land administration officials and ensures enlightening and educating customary land owners on the need for compulsory acquisition. -

The Blacksmiths Op Kano City : a Study in '

1 THE BLACKSMITHS OP KANO CITY : A STUDY IN ' TRADITION, INNOVATION AND ENTREPRENEURSHIP. ^y Philip John Jaggar Presented for the Degree of Master of Philosophy School of Oriental and African Studies University of London 1978 / I N 3 7. v I*IV, ProQuest Number: 10731195 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10731195 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 ABSTRACT This thesis examines the factors involved in the expansion, during the colonial and post-colonial periods, of a traditional, i.e. pre-European craft specialism — blacksrai thing, in Kano City, Nigeria — and its sub sequent conversion into a modem metal-working industry. In doing so, it sheds new light on the general proposition that such traditional crafts necessarily decline before the technological onslaught of colonialism* A notable feature of the recent development of this craft has been the differential responses of the various clusters of blacksmiths to the new socio-economic factors introduced by the British. Of these groups, the most far-reaching changes have occurred in that located within the Central Market area of Kano City, and it is the behaviour of these craftsmen - and/or trader-entrepreneurs which provides the focus of this study. -

Invitation to Tender

1 FEDERAL MINISTRY OF INTERIOR NIGERIA IMMIGRATION SERVICE HEADQUARTERS, SAUKA-ABUJA PUBLIC NOTICE INVITATION TO TENDER INTRODUCTION: LOT 21 CONSTRUCTION OF DIVISIONAL OFFICE AT ORUMBA SOUTH LGA 1.0. The Nigeria Immigration Service (NIS), in accordance With the Public Pro- ANAMBRA STATE curement Act, 2007, wishes to carry out some of its Capital Projects under LOT 22 CONSTRUCTION OF COMMAND OFFICE COMPLEX AT GUSAU 2018 Budget. To this end, interested and capable contractors with relevant ZAMFARA STATE experience are invited to submit tender documents for the following projects/ LOT 23 CONSTRUCTION OF COMMAND OFFICE COMPLEX AT KADUNA supplies. KADUNA STATE LOT 24 CONSTRUCTION OF COMMAND OFFICE COMPLEX AT YOLA DESCRIPTION OF WORK ADAMAWA STATE 1.1 The Projects description and scope are listed hereunder LOT 25 CONSTRUCTION OF COMMAND OFFICE COMPLEX, UYO AKWA-IBOM LOT 1 FENCING OF LAND FOR THE PROPOSED COMMAND COMPLEX AT STATE BAUCHI BAUCHI STATE LOT 26 CONSTRUCTION OF COMMAND OFFICE COMPLEX AT MINNA, LOT 2 FENCING OF IMMIGRATION BARRACKS LAND AT SAPELE DELTA STATE NIGER STATE LOT 3 FENCING OF LAND AT IDIIROKO BARRACKS, OGUN STATE LOT 27 CONSTRUCTION OF COMMAND OFFICE COMPLEX AT NIS LAND ALONG LOT 4 FENCING OF NIS LAND AT USHONGO LGA BENUE STATE SANGO ROAD, ILORIN KWARA STATE LOT 5 FENCING OF SPORTING ARENA AT SERVICE HEADQUARTERS, ABUJA LOT 28 CONSTRUCTION OF FUEL DUMP AT TUGA KEBBI STATE FCT LOT 29 REHABILITATION OF KITCHEN AT ITSK KANO STATE LOT 6 FENCING OF COMMAND OFFICE COMPLEX LAND AT LOKOJA KOGI LOT 30 REHABILITATION OF KITCHEN AT -

Urban Growth and Landuse Cover Change in Nigeria Using GIS and Remote Sensing Applications

Published by : International Journal of Engineering Research & Technology (IJERT) http://www.ijert.org ISSN: 2278-0181 Vol. 5 Issue 08, August-2016 Urban Growth and Landuse Cover Change in Nigeria using GIS and Remote Sensing Applications. Case Study of Suleja L.G.A., Niger State. Buba Y. Alfred, Makwin U. Gillian, Ogalla Mike, Okoro L. Ofonedum, Audu-Moses Justina Nigerian Building and Road Research Institute, Abuja, 900001, Nigeria. Corresponding author: Buba Yenhor Alfred, Abstract - Urbanization is among the problems confronting growth in settlement, observations of the earth from space most cities of the world which is attributed to rapid provide objective information of human utilization of the settlements expansion and population growth. The landscape, Bankole (2011). Over the past years, data from contemporary issues of urbanization are common in the Earth sensing satellites has become vital in mapping the developing countries where development goes ahead of urban Earth’s features and infrastructures, managing natural planning. Geographic Information System (GIS) and Remote Sensing Applications was used and three set of Landsat high resources and studying environmental change, Bankole resolution imageries were captured at different time interval (2011). (1980, 2000 and 2015)and projection of the Suleja Local Land is becoming a scarce resource due to immense Government Area (L.G.A) for both the landuse and the agricultural, city growth (settlements expansion) and population was made for 2035. However the study monitored demographic pressure on land. The information on landuse the landuse changes with focus on built-up (settlements) / landcover change and possibilities for their optimal use is growth in Suleja L.G.A to detect and estimate the rate of essential for research, planning and implementation of changes over the periods. -

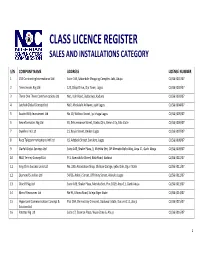

Class Licence Register Sales and Installations Category

CLASS LICENCE REGISTER SALES AND INSTALLATIONS CATEGORY S/N COMPANY NAME ADDRESS LICENSE NUMBER 1 CVS Contracting International Ltd Suite 16B, Sabondale Shopping Complex, Jabi, Abuja CL/S&I/001/07 2 Telesciences Nig Ltd 123, Olojo Drive, Ojo Town, Lagos CL/S&I/002/07 3 Three One Three Communications Ltd No1, Isah Road, Badarawa, Kaduna CL/S&I/003/07 4 Latshak Global Concept Ltd No7, Abolakale Arikawe, ajah Lagos CL/S&I/004/07 5 Austin Willy Investment Ltd No 10, Willisco Street, Iju Ishaga Lagos CL/S&I/005/07 6 Geoinformatics Nig Ltd 65, Erhumwunse Street, Uzebu Qtrs, Benin City, Edo State CL/S&I/006/07 7 Dwellins Intl Ltd 21, Boyle Street, Onikan Lagos CL/S&I/007/07 8 Race Telecommunications Intl Ltd 19, Adebola Street, Surulere, Lagos CL/S&I/008/07 9 Clarfel Global Services Ltd Suite A45, Shakir Plaza, 3, Michika Strt, Off Ahmadu Bello Way, Area 11, Garki Abuja CL/S&I/009/07 10 MLD Temmy Concept Ltd FF1, Abeoukuta Street, Bida Road, Kaduna CL/S&I/010/07 11 King Chris Success Links Ltd No, 230, Association Shop, Old Epe Garage, Ijebu Ode, Ogun State CL/S&I/011/07 12 Diamond Sundries Ltd 54/56, Adeniji Street, Off Unity Street, Alakuko Lagos CL/S&I/012/07 13 Olucliff Nig Ltd Suite A33, Shakir Plaza, Michika Strt, Plot 1029, Area 11, Garki Abuja CL/S&I/013/07 14 Mecof Resources Ltd No 94, Minna Road, Suleja Niger State CL/S&I/014/07 15 Hypersand Communication Concept & Plot 29A, Democracy Crescent, Gaduwa Estate, Durumi 111, abuja CL/S&I/015/07 Solution Ltd 16 Patittas Nig Ltd Suite 17, Essence Plaza, Wuse Zone 6, Abuja CL/S&I/016/07 1 17 T.J.