Private Joint Stock Company Kyivstar International Financial Reporting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Italian Guidelines About Wind Turbine Sound: How to Improve Them And

Italian guidelines about wind turbine sound: PO. ID How to improve them and make them work better C001 Martina Repossi Alerion Clean Power S.p.A. – Milan (Italy) Abstract Critical topics about Italian landscape Wind turbines can produce unwanted sound (referred to as noise) during operation. The nature of sound As a matter of facts, Italian population density, at 197 inhabitants per square kilometre (ISTAT Report, 2013), depends on wind turbine design. Propagation of the sound is primarily a function of distance, but it can also be is higher than that of most Western European countries. However, the distribution of the population is widely affected by turbine placement, surrounding terrain, and atmospheric conditions. uneven. The most densely populated areas are the Po Valley (that accounts for almost a half of the national In Italy, unlike other European countries, we don’t have specific legislation about windmills sound population) and the metropolitan areas of Rome and Naples, while vast regions such as the Alps and measurement and noise limits from Law no.447 are not functional for noise verifical for wind farms. Public Apenins highlands, the island of Sardinia and the plateaus of Basilicata are very sparsely populated. health is an essential Constitutional right (art.32 from Italian Constitution: "la Repubblica tutela la salute come Besides that, Italian landscape is full of protected areas in order to guarantee environmental conservation. The fondamentale diritto dell'individuo e interesse della collettività”) and disagreements related to wind farms noise consequence is that designers need to adapt wind farms layouts to these constraints, also because most are actually recurring. -

Download PDF Dossier

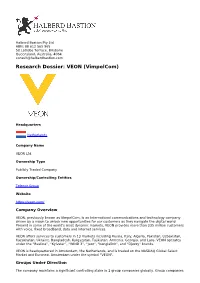

Halberd Bastion Pty Ltd ABN: 88 612 565 965 58 Latrobe Terrace, Brisbane Queensland, Australia, 4064 [email protected] Research Dossier: VEON (VimpelCom) Headquarters Netherlands Company Name VEON Ltd. Ownership Type Publicly Traded Company Ownership/Controlling Entities Telenor Group Website https://veon.com/ Company Overview VEON, previously known as VimpelCom, is an international communications and technology company driven by a vision to unlock new opportunities for our customers as they navigate the digital world. Present in some of the world's most dynamic markets, VEON provides more than 235 million customers with voice, fixed broadband, data and internet services. VEON offers services to customers in 13 markets including Russia, Italy, Algeria, Pakistan, Uzbekistan, Kazakhstan, Ukraine, Bangladesh, Kyrgyzstan, Tajikistan, Armenia, Georgia, and Laos. VEON operates under the “Beeline”, “Kyivstar”, “WIND 3”, “Jazz”, “banglalink”, and “Djezzy” brands. VEON is headquartered in Amsterdam, the Netherlands, and is traded on the NASDAQ Global Select Market and Euronext Amsterdam under the symbol "VEON". Groups Under Direction The company maintains a significant controlling stake in 1 group companies globally. Group companies are those maintaining a parent relationship to individual subsidiaries and/or mobile network operators. Global Telecom Holding Headquarters: Netherlands Type: Publicly Traded Company, Subsidiary Subsidiaries The company has 8 subsidiaries operating mobile networks. Beeline Armenia Country: Armenia 3G Bands: -

(Each As Defined Below) Or (2) Non-U.S

IMPORTANT NOTICE THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE EITHER (1) QIBS THATARE QPS (EACH AS DEFINED BELOW) OR (2) NON-U.S. PERSONS OR ADDRESSEES OUTSIDE OF THE U.S. IMPORTANT: You must read the following before continuing. The following applies to the prospectus following this page (the “Prospectus”), and you are therefore advised to read this carefully before reading, accessing or making any other use of the Prospectus. In accessing the Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE ISSUER HAS NOT BEEN AND WILL NOT BE REGISTERED UNDER THE U.S. INVESTMENT COMPANYACT OF 1940, AS AMENDED (THE “INVESTMENT COMPANY ACT”) AND THE SECURITIES HAVE NOT BEEN, AND WILL NOT, BE REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIES LAWS OFANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S. OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS AND WHICH DOES NOT REQUIRE THE ISSUER TO REGISTER UNDER THE INVESTMENT COMPANYACT. -

Financial Information at September 30, 2020

FINANCIAL INFORMATION AT SEPTEMBER 30, 2020 This document has been translated into English for the convenience of the readers. In the event of discrepancy, the Italian language version prevails. CONTENTS HIGHLIGHTS __________________________________________________________________________________ 3 INTRODUCTION _______________________________________________________________________________ 7 MAIN CHANGES IN THE SCOPE OF CONSOLIDATION OF THE TIM GROUP _____________________________ 8 RESULTS OF THE TIM GROUP FOR THE FIRST NINE MONTHS OF 2020 ________________________________ 9 RESULTS OF THE BUSINESS UNITS _____________________________________________________________ 14 AFTER LEASE INDICATORS _____________________________________________________________________ 18 BUSINESS OUTLOOK FOR THE YEAR 2020 _______________________________________________________ 19 EVENTS SUBSEQUENT TO SEPTEMBER 30, 2020 __________________________________________________ 19 MAIN RISKS AND UNCERTAINTIES ______________________________________________________________ 19 ATTACHMENTS ______________________________________________________________________________ 21 TIM GROUP – FINANCIAL HIGHLIGHTS ___________________________________________________________ 21 TIM GROUP – RECLASSIFIED STATEMENTS _______________________________________________________ 22 SEPARATE CONSOLIDATED INCOME STATEMENTS OF THE TIM GROUP _____________________________ 22 CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME OF THE TIM GROUP ____________________ 23 CONSOLIDATED STATEMENTS OF FINANCIAL POSITION -

2008-Annual-Report.Pdf

2008 VimpelCom Annual Report ВымпелКом Годовой отчет CONTENTS СОДЕРЖАНИЕ 2 Company Profile 2 Информация о Компании 6 Financial Highlights 6 Основные финансовые показатели 13 Letter to Shareholders 13 Письмо акционерам 18 Strategic Achievements of 2008 18 Стратегические достижения 2008 года 22 Broadening Horizons 22 Новые горизонты 25 Increasing Functionality 25 Новые функциональные возможности 28 Maintaining Customer Focus 28 Фокус на потребностях клиента 30 The Legacy of VimpelСom Founders’ 3o Традиции «ВымпелКома»: Pioneering Spirit новаторский дух учредителей 32 Board of Directors 32 Совет директоров 34 Senior Management 34 Старший менеджмент 37 Corporate Information 37 Корпоративная информация 38 Financial Information 38 Финансовая информация 2 COMPANY PROFILE ИНФОРМАЦИЯ О КОМПАНИИ The VimpelCom Group is one of the leading Группа компаний «ВымпелКом» – один из telecommunications operators providing voice ведущих операторов в сфере телекоммуни- and data services through a range of mobile, каций, предоставляющий услуги голосовой fixed and broadband technologies. The Group связи и передачи данных на основе широкого includes companies operating in Russia, спектра технологий мобильной и фиксирован- Kazakhstan, Ukraine, Uzbekistan, Tajikistan, ной связи, а также широкополосного доступа Armenia and Georgia as well as Vietnam and в Интернет. В группу компаний «ВымпелКом» Cambodia, in territories with a total population входят компании, предоставляющие свои услу- VimpelCom / Annual Report 2008 of about 340 million. ги в России, Казахстане, -

Unaudited Interim Condensed Consolidated Financial Statements

Unaudited interim condensed consolidated financial statements Public Joint Stock Company “Vimpel-Communications” (a wholly-owned subsidiary of VEON Ltd.) as of 30 September 2017 and for the three and nine months ended 30 September 2017 Public Joint Stock Company “Vimpel-Communications” (a wholly-owned subsidiary of VEON Ltd.) Unaudited interim condensed consolidated financial statements as of 30 September 2017 and for the three and nine months ended 30 September 2017 Contents Report on Review of Interim Financial Information Interim consolidated income statement for the three and nine months ended 30 September 2017 .................. 1 Interim consolidated statement of comprehensive income for the three and nine months ended 30 September 2017. ........................................................................................................................................ 2 Interim consolidated statement of financial position as of 30 September 2017 ................................................. 3 Interim consolidated statement of changes in equity for the three and nine months ended 30 September 2017 ......................................................................................................................................... 4 Interim consolidated statement of changes in equity for the three and nine months ended 30 September 2016 ......................................................................................................................................... 5 Interim consolidated statement of cash flows for -

Operátor Stát MTN Afghanistan Afghanistan Afghan Wireless

Operátor Stát MTN Afghanistan Afghanistan Afghan Wireless Communications Company Afghanistan Etisalat Afghanistan Telecom Development Company Limited Afghanistan Telekom Albania Sh.A Albania ALBtelecom sh.a. Albania Vodafone Albania Sh.A. Albania ATM Mobilis Algeria OPTIMUM TELECOM ALGERIE Spa Algeria Wataniya Algeria s.p.a. Algeria Andorra Telecom, S.A.U. Andorra Unitel Angola Angola Cable & Wireless Anguilla Anguilla APUA imobile (former APUA PCS Ltd.) Antigua and Barbuda Cable & Wireless Antigua Antigua and Barbuda TELECOM ARGENTINA S.A Argentina AMX Argentina S.A. Argentina NII Holdings, Inc. (Nextel Argentina S.R.L.) Argentina Telefonica Moviles Argentina S.A. Argentina VEON Armenia CJSC Armenia MTS Armenia CJSC Armenia Karabakh Telecom Armenia New Millennium Telecom Services NV Aruba Servicio di Telecomunicacion di Aruba (SETAR) N.V. Aruba Telstra Corporation Limited Australia Yes Optus Australia Vodafone Hutchison Australia Pty Limited Australia Hutchison Drei Austria GmbH Austria Hutchison Drei Austria GmbH Austria A1 Telekom Austria AG Austria T-Mobile Austria GmbH Austria A1 Telekom Austria AG Austria A1 Telekom Austria AG Austria T-Mobile Austria GmbH Austria Azercell Telekom B.M. Azerbaijan Azerfon LLC Azerbaijan Bakcell LLC Azerbaijan BTC Bahamas Bahamas Bahrain Telecommunication Company Bahrain Zain Bahrain B.S.C Bahrain Viva Bahrain Robi Axiata Limited Bangladesh Banglalink Digital Communications Ltd. Bangladesh GrameenPhone Limited Bangladesh Teletalk Bangladesh Limited Bangladesh Cable & Wireless Barbados Barbados Mobile TeleSystems Belarus Belarusian Telecommunications Network CJSC Belarus FE VELCOM Belarus Telenet Group BVBA/SPRL Belgium Telenet Group BVBA/SPRL Belgium Orange Belgium SA/NV Belgium Proximus PLC (former Belgacom SA/NV) Belgium Belize Telemedia Limited Belize Etisalat Benin Benin Spacetel-Benin S.A. -

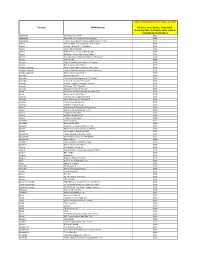

New Simplification Rates

NEW VOICE RATES AS OF JULY 14, 2009 Country GSM Operator All Voice calls: Back to Canada/US, Incoming Calls, In Country Calls, Calls to International Destinations Afghanistan MTN Afganistan, "MTN" $4.00 Afghanistan Afghan Wireless Communications Company $4.00 Afghanistan Telecom Development Company Afghanistan Ltd "TDCA" $4.00 Albania Albanian Mobile Communications "A M C Mobil" $2.00 Albania Vodafone Albania Sh. A. "Vodafone" $2.00 Algeria Algerie Telecom Mobile $3.00 Algeria Orascom Telecom Algeria SPA "Djezzy" $3.00 Algeria Wataniya Telecom Algerie s.p.a."Nedjma" $3.00 Andorra Servei de Telecomunicacions d'Andorra "Mobiland" $2.00 Angola Unitel S.A.R.L. $4.00 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla $3.00 Anguilla Digicel (Jamaica) Ltd "Digicel" $3.00 Antigua & Barbuda Antigua Public Utilities Authority "APUA PCS" $3.00 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Ltd. $3.00 Antigua & Barbuda Digicel (Jamaica) Ltd "Digicel" $3.00 Argentina AMX Argentina S.A. $3.00 Argentina Telefonica Moviles Argentina S.A. "Movistar" $3.00 Argentina Telecom Personal S.A. "Personal" $3.00 Armenia Armenia Telephone Company "ArmenTel" $2.00 Armenia K Telecom CJSC "Vivacell" $2.00 Armenia Karaback Telecom "K Telecom" $2.00 Aruba Servicio di Telecomunicacion di Aruba "SETAR" $3.00 Aruba Digicel (Jamaica) Ltd "Digicel" $3.00 Australia Hutchison 3G Australia Pty Limited $2.00 Australia Optus Mobile Pty Ltd. "Yes Optus" $2.00 Australia Telstra Corporation Limited $2.00 Australia Vodafone Network Pty Ltd. $2.00 Austria Orange Austria Telecommunication GmbH $2.00 Austria Hutchison 3G Austria GmbH "3 AT" $2.00 Austria T-Mobile Austria GmbH $2.00 Austria Mobilkom Austria AG "A1" $2.00 Austria T-Mobile Austria GmbH $2.00 Azerbaijan Azercell Telecom $4.00 Azerbaijan Bakcell "GSM 2000" $4.00 Bahamas Bahamas Telecommunications Co. -

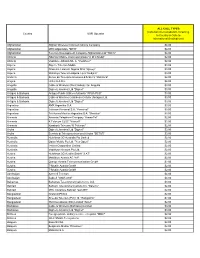

New Simplification Rates

ALL CALL TYPES (Calls back to Canada/US, Incoming, Country GSM Operator In Country & Calls to International Destinations) Afghanistan Afghan Wireless Communications Company $4.00 Afghanistan MTN Afganistan, "MTN" $4.00 Afghanistan Telecom Development Company Afghanistan Ltd "TDCA" $4.00 Albania Albanian Mobile Communications "A M C Mobil" $2.00 Albania Vodafone Albania Sh. A. "Vodafone" $2.00 Algeria Algerie Telecom Mobile $3.00 Algeria Orascom Telecom Algeria SPA "Djezzy" $3.00 Algeria Wataniya Telecom Algerie s.p.a."Nedjma" $3.00 Andorra Servei de Telecomunicacions d'Andorra "Mobiland" $2.00 Angola Unitel S.A.R.L. $4.00 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla $3.00 Anguilla Digicel (Jamaica) Ltd "Digicel" $3.00 Antigua & Barbuda Antigua Public Utilities Authority "APUA PCS" $3.00 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Ltd. $3.00 Antigua & Barbuda Digicel (Jamaica) Ltd "Digicel" $3.00 Argentina AMX Argentina S.A. $3.00 Argentina Telecom Personal S.A. "Personal" $3.00 Argentina Telefonica Moviles Argentina S.A. "Movistar" $3.00 Armenia Armenia Telephone Company "ArmenTel" $2.00 Armenia K Telecom CJSC "Vivacell" $2.00 Armenia Karaback Telecom "K Telecom" $2.00 Aruba Digicel (Jamaica) Ltd "Digicel" $3.00 Aruba Servicio di Telecomunicacion di Aruba "SETAR" $3.00 Australia Hutchison 3G Australia Pty Limited $2.00 Australia Optus Mobile Pty Ltd. "Yes Optus" $2.00 Australia Telstra Corporation Limited $2.00 Australia Vodafone Network Pty Ltd. $2.00 Austria Hutchison 3G Austria GmbH "3 AT" $2.00 Austria Mobilkom Austria AG "A1" $2.00 Austria Orange Austria Telecommunication GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Azerbaijan Azercell Telecom $4.00 Azerbaijan Bakcell "GSM 2000" $4.00 Bahamas Bahamas Telecommunications Co. -

Financing Technology Entrepreneurs & Smes in Developing Countries: Challenges and Opportunities

+ innovation & entrepreneurship FINANCING TECHNOLOGY ENTREPRENEURS & SMES IN DEVELOPING COUNTRIES: CHALLENGES AND OPPORTUNITIES FINANCING TECHNOLOGY ENTREPRENEURS & SMES IN DEVELOPING COUNTRIES: CHALLENGES AND UKRAINE OPPORTUNITIES Country Study AN infoDev PUBLICATION PREPARED BY Roberto Zavatta Economisti Associati SRL in collaboration with Zernike Group BV Meta Group SRL June 2008 Information for Development Program www.infoDev.org www.infoDev.org FINANCING TECHNOLOGY ENTREPRENEURS & SMES IN DEVELOPING COUNTRIES: CHALLENGES AND UKRAINE OPPORTUNITIES Country Study AN infoDev PUBLICATION PREPARED BY Roberto Zavatta Economisti Associati SRL in collaboration with Zernike Group BV Meta Group SRL June 2008 Information for Development Program www.infoDev.org ©2008 The International Bank for Reconstruction and Development/ The World Bank 1818 H Street NW Washington DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org E-mail: [email protected] All rights reserved The findings, interpretations and conclusions expressed herein are entirely those of the author(s) and do not necessarily reflect the view of infoDev, the Donors of infoDev, the International Bank for Reconstruction and Development/The World Bank and its affiliated organizations, the Board of Executive Directors of the World Bank or the governments they represent. The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply on the part of the World Bank any judgment of the legal status of any territory or the endorsement or acceptance of such boundaries. Rights and Permissions The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. -

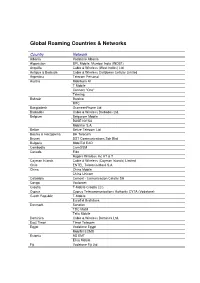

Global Roaming Countries & Networks

Global Roaming Countries & Networks Country Network Albania Vodafone Albania Afganistan BPL Mobile, Mumbai India (INDB1) Anguilla Cable & Wireless (West Indies) Ltd. Antigua & Barbuda Cable & Wireless Caribbean Cellular Limited Argentina Telecom Personal Austria Mobilkom A1 T-Mobile Connect "One" Telering Bahrain Batelco MTC Bangladesh GrameenPhone Ltd Barbados Cable & Wireless Barbados Ltd. Belgium Belgacom Mobile BASE NV/SA Mobistar S.A. Belize Belize Telecom Ltd Bosnia & Herzgovina BH Telecom Brunei DST Communications Sdn Bhd Bulgaria MobilTel EAD Cambodia CamGSM Canada Fido Rogers Wireless Inc AT & T Cayman Islands Cable & Wireless (Cayman Islands) Limited Chile ENTEL Telefonia Movil S.A China China Mobile China Unicom Colombia Comcel - Comunicacion Celular SA Congo Vodacom Croatia T-Mobile Croatia LLC Cyprus Cyprus Telecommunications Authority CYTA (Vodafone) Czech Republic T-Mobile EuroTel Bratislava Denmark Sonofon TDC Mobil Telia Mobile Dominica Cable & Wireless Dominica Ltd. East Timor Timor Telecom Egypt Vodafone Egypt MobiNil ECMS Estonia AS EMT Elisa Mobile Fiji Vodafone Fiji Ltd Country Network Finland Elisa Sonera Mobile Networks France Bouygues Telecom SFR Orange France French Polynesia (Tahiti) Tikiphone Georgia Geocell Ltd Germany T-Mobil Vodafone D2 GmbH E-Plus O2 - DEUE2 Greece Cosmote Vodafone Stet Hellas Telecommunications S.A. Grenada Cable & Wireless Grenada Ltd. Guernsey Cable & Wireless Guernsey Ltd Hong Kong Hutchison Telephone Co. Ltd Sunday / Mandarin Communications Ltd New World PCS Ltd China Resources Peoples -

2 5 F E B R U a R Y 2 0 1 9

25 FEBRUARY 2019 VEON REPORTS G O O D FULL YEAR 2018 RESULTS FY 2018 FINANCIAL TARGETS ACHIEVED FINAL DIVIDEND OF US 17 C E N T S D ECLARED Amsterdam (25 February 2019) – VEON Ltd. (NASDAQ: VEON, Euronext Amsterdam: VEON), a leading global provider of connectivity and internet services, today announces financial and operating results for the quarter and year ended 31 December 2018. KEY Q4 2018 RESULTS 1 • Solid organic2 revenue growth in Q4 2018: total revenue increased organically by 5.3% year on year to USD 2,249 million, led by strength in Russia, Pakistan and Ukraine • Strong data revenue growth across VEON’s emerging markets: data revenue continued to grow strongly, rising by 30.2% organically year on year in the quarter, with Ukraine (84.5%), Pakistan (86.7%) and Algeria (67.1%) delivering large increases year on year following investment in 4G/LTE networks • Double-digit organic2 growth in EBITDA of 10.0% during the quarter, helped by good operational performance in Pakistan and Ukraine • Currency movements negatively impacted total revenue and EBITDA: total revenue decreased by 3.1% to USD 2,249 million, due to currency headwinds of USD 285 million. EBITDA decreased by 5.1% to USD 714 million, impacted by currency headwinds of USD 111 million • EBITDA margin of 31.8% was down 0.7 percentage points year on year in Q4 2018, owing mainly to the change in revenue mix in Russia towards increased sales of equipment and accessories as a consequence of the move to monobrand stores (an impact of 1.3 percentage points) • Corporate costs were USD 135 million in Q4 2018, including USD 52 million of severance costs, down 34% year on year excluding severance.