FLI 17A and FS Combined File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Business Directory Commercial Name Business Address Contact No

Republic of the Philippines Muntinlupa City Business Permit and Licensing Office BUSINESS DIRECTORY COMMERCIAL NAME BUSINESS ADDRESS CONTACT NO. 12-SFI COMMODITIES INC. 5/F RICHVILLE CORP TOWER MBP ALABANG 8214862 158 BOUTIQUE (DESIGNER`S G/F ALABANG TOWN CENTER AYALA ALABANG BOULEVARD) 158 DESIGNER`S BLVD G/F ALABANG TOWN CENTER AYALA ALABANG 890-8034/0. EXTENSION 1902 SOFTWARE 15/F ASIAN STAR BUILDING ASEAN DRIVE CORNER DEVELOPMENT CORPORATION SINGAPURA LANE FCC ALABANG 3ARKITEKTURA INC KM 21 U-3A CAPRI CONDO WSR CUPANG 851-6275 7 MARCELS CLOTHING INC.- LEVEL 2 2040.1 & 2040.2 FESTIVAL SUPERMALL 8285250 VANS FESTIVAL ALABANG 7-ELEVEN RIZAL ST CORNER NATIONAL ROAD POBLACION 724441/091658 36764 7-ELEVEN CONVENIENCE EAST SERVICE ROAD ALABANG SERVICE ROAD (BESIDE STORE PETRON) 7-ELEVEN CONVENIENCE G/F REPUBLICA BLDG. MONTILLANO ST. ALABANG 705-5243 STORE MUNT. 7-ELEVEN FOODSTORE UNIT 1 SOUTH STATION ALABANG-ZAPOTE ROAD 5530280 7-ELEVEN FOODSTORE 452 CIVIC PRIME COND. FCC ALABANG 7-ELEVEN/FOODSTORE MOLINA ST COR SOUTH SUPERH-WAY ALABANG 7MARCELS CLOTHING, INC. UNIT 2017-2018 G/F ALABANG TOWN CENTER 8128861 MUNTINLUPA CITY 88 SOUTH POINTER INC. UNIT 2,3,4 YELLOW BLDG. SOUTH STATION FILINVEST 724-6096 (PADIS POINT) ALABANG A & C IMPORT EXPORT E RODRIGUEZ AVE TUNASAN 8171586/84227 66/0927- 7240300 A/X ARMANI EXCHANGE G/F CORTE DE LAS PALMAS ALAB TOWN CENTER 8261015/09124 AYALA ALABANG 350227 AAI WORLDWIDE LOGISTICS KM.20 WEST SERV.RD. COR. VILLONGCO ST CUPANG 772-9400/822- INC 5241 AAPI REALTY CORPORATION KM22 EAST SERV RD SSHW CUPANG 8507490/85073 36 AB MAURI PHILIPPINES INC. -

FDC Annual Report 2005.Pdf

Contents 2 Consolidated Financial Highlights 3 Joint Message 6 Operating Highlights 14 Board of Directors and Officers 15 Consolidated Financial Statements Insert Consolidated Financial Statements and Report of Independent Auditors our cover Brighter Prospects. The sun seems to shine more brightly after the rain. In the same way, business prospects look brighter after the challenges of the previous years. Amidst the revitalized real estate sector and a more favorable economic environment, FDC is planning for major expansion in 2006, with its sights focused on long-term growth for the company. 1 Consolidated Financial Highlights (In Thousands of Pesos, Except Earnings Per Share Figures) 2005 2004 2003 2002 Operating Results Net Revenues 5,056,952 4,339,273 3,830,876 3,219,335 Net Income 1,266,251 775,720 426,074 308,085 Return on Assets (ave.) 1.6% 1.1% 0.7% 0.5% Return on Equity (ave.) 3.3% 2.2% 1.3% 0.9% Financial Position Total Assets 83,114,966 75,181,585 67,649,437 63,401,360 Total Debt 11,562,549 9,535,123 9,689,021 9,527,024 Stockholders’ Equity 38,651,052 37,078,302 33,127,507 32,089,368 No. of Shares Issued and Outstanding (‘000) 5,955,725 5,955,725 5,955,725 5,955,725 Gross Debt to Equity 29.9% 25.7% 29.2% 29.7% Net Debt to Equity 17.4% 16.8% 19.5% 23.1% Earnings Per Share 0.147 0.090 0.028 0.009 5,056 1,266 38,651 83,114 4,339 75,181 37,078 3,830 67,649 63,401 3,219 775 33,127 426 308 32,089 2002 2003 2004 2005 2002 2003 2004 2005 2002 2003 2004 2005 2002 2003 2004 2005 Net Income Net Revenues Total Assets Total Stockholders’ Equity In Millions of Pesos In Millions of Pesos In Millions of Pesos In Millions of Pesos 2005 ANNUAL REPORT 2005 ANNUAL FILINVEST 2 Joint Message Philippine economic growth declined to 5.1% last year from the 6% GDP increase posted in 2004. -

JG Summit Holdings Inc. Annual Report 2020

Annual Report 2020 About the Cover When faced with a monumental challenge, few are able to swiftly form high- impact solutions to make the situation better. It requires agility and adaptability to achieve a transformational outcome. This year, JG Summit swiftly addressed the effects of the pandemic, using its “How to Win” and “Where to Play” strategies to maximum effect. The company was agile in business, as well as steady and firm in uplifting communities to better endure this critical time. By focusing on employee health and safety, operations and supply chain continuity, cash, costs and liquidity management, and helping communities deal with the pandemic, JGS was able to weather the unexpected storm. The company also doubled its efforts to explore new business opportunities. This year’s cover demonstrates the diverse response throughout JG Summit’s businesses - its fluid and agile response that demonstrated firm leadership, mindfulness, and strength to balance business in the face of turmoil and change. 2 Annual Report 2020 Table of Contents JGS at a Glance 4 2020 Key Developments 7 JGS Investment Portfolio 9 Corporate Structure 10 Geographic Presence 12 Chairman’s Message 13 President and CEO’s Report 17 Leadership 21 Our COVID-19 Response 23 Laying the Foundation for the New Normal 27 Strategic Business Units & Investments 38 Strategic Business Units 39 Ecosystem Plays 57 Core Investments 63 Sustainability 65 Sustainability Performance in 2020 66 Gokongwei Brothers Foundation 77 Corporate Governance 86 Financial Statements 96 Contact Info 221 3 Annual Report 2020 JGS at a Glance 4 Annual Report 2020 JGS At A Glance: Key Business Metrics Our portfolio diversity cushioned the impact of COVID-19, driven by The Company’s robust balance sheet provides Continuous shareholder value maximization as JGS’ the resiliency of our food, banking, and office segments, while heavily- enough ballast to weather the pandemic. -

Investor Presentation November 2019 Section 1 FDC at a Glance Diversified Range of Market-Leading Businesses That Target the Underserved Middle Market

Investor Presentation November 2019 Section 1 FDC at a Glance Diversified range of market-leading businesses that target the underserved middle market Real Estate & Hospitality Banking Power Others – Sugar & Infra Pacific Sugar 65%1 100% 78%1 100% Holdings 100% 93%1 Clark Consortium 42.5% NAIA Consortium TBC • One of the leading • Manages c.1,800 keys • Most consumer • Early mover into the • Operates sugar mill, real estate developers in significant growth focused bank in retail Mindanao power refinery and sugarcane in the Philippines with areas across the and middle-market sector farms that provide residential land bank of Philippines corporate segments stable cash flows 2,236 ha • Operates a 405MW • First mover advantage • One of the largest clean coal thermal • Led a consortium that • Developed over to invest in the consolidated branch power plant in was awarded a 25-year 200 projects and Clark region store networks with Mindanao Operation and 3,000 ha of land a total of 467 branch Management (“O&M”) • Obtained a provisional stores • Offtake agreements for contract for Clark • Develops integrated casino license from a total of 302 MW4 International Airport self-contained PAGCOR2 for its 201 ha • Ranked 2nd in auto with 17 distribution masterplanned cities integrated resort in loans in the Philippines utilities and an • Member of the and “REIT-able” assets Clark industrial customer in consortium that was Mindanao awarded NAIA Original Proponent Status ("OPS") Respective bubbles represent % ownership Source: Company information Notes: 1 Directly and indirectly 2 PAGCOR = Philippine Amusement and Gaming Corporation 2 3 In terms of credit card receivables in 2018, according to Credit Cards Association of the Philippines 4 Includes 70MW subject to SC ruling requiring the distribution utility to submit a DOE certification to the ERC that they have complied with CSP Rules. -

(Aep/S) Atty. Sarah Buena S. Mirasol

PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 1 24/7 BUSINESS PROCESSING INC. Chen, Huigui Mandarin Speaking Customer 11/F Capella Bldg., L-3&4 B2, Asean Drive Filinvest, Service Representative Alabang, Muntinlupa City, Metro Manila Chinese 2 24/7 BUSINESS PROCESSING INC. Yang, Liu Mandarin Speaking Customer 11/F Capella Bldg., L-3&4 B2, Asean Drive Filinvest, Service Representative Alabang, Muntinlupa City, Metro Manila Chinese 3 24/7 BUSINESS PROCESSING INC. Li, Feng Mandarin Speaking Customer 11/F Capella Bldg., L-3&4 B2, Asean Drive Filinvest, Service Representative Alabang, Muntinlupa City, Metro Manila Chinese 4 24/7 BUSINESS PROCESSING INC. Guan, Shaohua Mandarin Speaking Customer 11/F Capella Bldg., L-3&4 B2, Asean Drive Filinvest, Service Representative Alabang, Muntinlupa City, Metro Manila Chinese 5 24/7 BUSINESS PROCESSING INC. Zhao, Ju Mandarin Speaking Customer 11/F Capella Bldg., L-3&4 B2, Asean Drive Filinvest, Service Representative Alabang, Muntinlupa City, Metro Manila Chinese If you have any information/objection to the above mentioned application/s, please communicate with the Regional Director thru Employment Promotion and Workers Welfare (EPWW) Division with Telephone No. 400-6011. ATTY. SARAH BUENA S. MIRASOL ATTY. SARAH BUENA S. MIRASOL REGIONAL DIRECTOR Page 1 of 297 PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 6 24/7 BUSINESS PROCESSING INC. -

Philippine Business News: China Firms Investing

Share 0 More Next Blog» Create Blog Sign In Philippine Business News Sunday, January 28, 2007 Links China firms investing P9B Rex Crisostomo Google News MOST ARE JOINT VENT URES ON BIOET HANOL-MAKING Go Green Philippines By Jennif er A. Ng OFW News Reporter PC Tips and Tricks THE Philippines and China are set to sign around 20 economic agreements expected to bring Philippine Cooperative News in as much as P9 billion in additional foreign investments, notably joint ventures in the manufacture of bioethanol. Philippine Education News Agriculture Secretary Arthur C. Yap disclosed that the agreements will be signed by the Philippine Educational Technology Philippine and Chinese governments during the visit of Chinese officials led by Premier Wen Jia News Bao in Manila next week in time for the Leaders' Summit of the Association of Southeast Asian Nations (Asean) in Cebu. Philippine Financial News "Not all of the agreements that will be signed, however, will take effect this year," said Yap at Philippine Netpreneur the sidelines of a press briefing on the decision of the Department of Agriculture (DA) to lift the ban on the Pacific white shrimp variety. Philippine Technical News Based on documents provided by the DA, among the memoranda of agreement (MOA) to be Quotable Quotes signed include joint-venture agreements between local and Chinese companies to manufacture bioethanol, as well as an agreement to put up a bioethanol plant in Palawan. Labels The Palawan Bioenergy Development Corp. will sign an agreement with the China CAMC Engineering Co. Ltd. for the establishment of a 150,000-liter per day capacity bioethanol plant acquisition (1) in Palawan. -

Resume 201512

COMPLETED CONSULTING PROJECTS Type of Project Project Name Client Airports Caticlan Airport San Miguel Corporation NAIA IPT 3 Review TCGI Engineers Embassies British Embassy British Embassy Qatar Embassy Astec US Embassy Manila Ayala Land Inc./MDC Excavation Protection 6786 Nova Century Properties 81 Newport IPM Alveo Highpark Ayala Land Inc./MDC Annapolis Building We Enterprises Ascott BGC Winsome Development Corp. Avida 34th Street Mega Philippines Avida Capital House Ayala Land Inc./MDC Bridgetowne (Exxa and Zeta) We Enterprises Bristle Ridge DMCI Homes Cebu Marco Polo Residences Federal Land, Inc. Century BGC Century Properties Century Spire We Enterprises Citynet Central We Enterprises Corinthian Hills Mansion Parade Megaworld Corp. Ecoprime Ecoprime Estancia Mall Hong Drill Estancia Mall We Enteprises Every Nation BGC Hong Drill Finance Centre Daiichi Properties Fortune Hills IPM Garden Towers Ayala Land Inc./MDC Globe Telecoms Building Ayala Land Inc./MDC Grand Hyatt Federal Land, Inc. Hamilton Tower 2 IPM Horizon 101 Taft Property HSS Tower 2 Mega Philippines Imperium Project We Enterprises Jabba Ayala Land Inc./MDC Lopez Tower We Enterprises Magnolia Residences IPM Makati North Gateway 1 Ayala Land Inc./MDC Marriott We Enterprises Marriott Tunnel We Enterprises Mayflower BPO IPM MDC HQ Ayala Land Inc./MDC Net Park We Enterprises Newport PP3 IPM Northwest Superblock Hong Drill One Meridien Ayala Land Inc./MDC One World Place Daiichi Properties Oxford Parksuites Anchor Land Holdings Inc. Park Triangle Ayala Land Inc./MDC Paseo de Roxas - Villar Underpass Ayala Land Inc./MDC Philamlife Cebu We Enterprises Project Jade We Enterprises Robinsons Galleria Cebu Monolith Construction Royalton We Enterprises Type of Project Project Name Client Senta Building Ayala Land Inc./MDC SM Keppel IPM Somerset Alabang We Enterprises Sotogrande We Enterprises Sun Residences SM Development Corp. -

Information Note for Participants

CBD Distr. GENERAL 6 November 2019 ENGLISH ONLY REGIONAL TRAINING WORKSHOP TO BUILD UNDERSTANDING AND CAPACITY ON GENDER AND BIODIVERSITY ISSUES IN SOUTH-EAST ASIA Manila, Philippines, 9 to 13 December 2019 INFORMATION NOTE FOR PARTICIPANTS QUICK LINKS: (Control + click on icons for web page) INFORMATION HIGHLIGHTS Meeting Venue (Page 2) 1. OPENING AND REGISTRATION ..................... 2 2. MEETING VENUE ............................ 2 4. DOCUMENTS ............................ 2 Visa Information (Page 3) 5. GENERAL INFORMATION ON ACCESS TO MANILA, PHILIPPINES ............................ 2 6. VISA INFORMATION ............................ 3 Meeting Documents (Page 2) 8. HOTEL INFORMATION ............................ 4 10. WEATHER AND TIME ZONE INFORMATION ............................ 5 Hotel Information (Page 4) 12. CURRENCY ............................ 5 Weather Information (Page 5) Currency information (page 5) 1 1. Opening and registration The Regional Training Workshop to Build Understanding and Capacity on Gender and Biodiversity Issues in South-East Asia will be held in Manila, Philippines from Monday, 9 December to Friday, 13 December 2019. Registration will take place at the venue of the meeting on 9 December, 8:30 a.m. and the workshop will start at 9:00 a.m. 2. Meeting venue The workshop will be held at: VIVERE HOTEL 5102 Bridgeway Avenue Filinvest City, Alabang, Muntinlupa City 1781 Philippines Tel: +632 8771 7777 Mobile:+63 917-6531777 (Vivere Hotel) E-mail: [email protected] Website: https://www.viverehotel.com.ph/ 3. Working language The workshop will be held in English. 4. Documents In order to minimize the environmental footprint of the workshop and in line with the UN policy towards greener meetings, participants are kindly reminded to bring their own copies of the workshop documents, or to use paperless versions, as there will be no extra copies made available on site during the workshop. -

2005 Annual Report-B

F I L I N V E S T LAND INCORPORATED A N2005N U A L R E P O R T FDC Building, 173 P. Gomez St., San Juan, Metro Manila Tel Nos.: 727-0431 to 55 / 727-0479 to 85 www.filinvestland.com W E B U I L D T H E F I L I P I N O D R E A M 1 FILINVEST LAND, INC. AND SUBSIDIARIES FINANCIAL HIGHLIGHTS (Amounts In Thousands of Pesos, Except Per Share Data) 2005 2004 2003 2002 Operating Results Revenues 2,908,191 2,422,291 1,587,896 1,732,463 Net Income 656,278 597,698 508,453 504,114 Return on Assets (ave.) 2% 2% 2% 2% CONTENTS Return on Equity (ave.) 4% 3% 3% 3% Financial Position 1 Financial Highlights Total Assets 28,267,517 25,097,831 24,275,947 22,688,383 Total Long-term Debt 5,575,000 3,950,000 3,240,778 3,269,004 2 - 4 Joint Message of the Chairman and Stockholders' Equity 18,127,419 17,476,132 17,353,550 16,845,097 the President No. of Shares Issued and Outstanding ('000) 7,819,261 7,819,261 7,819,261 7,819,261 Debt to Equity* 31% 23% 19% 19% 5 - 14 Operational Highlights Net Debt to Equity** 28% 22% 18% 18% 15 Board of Directors and Per Share Data Senior Management Primary Earnings 0.086 0.078 0.066 0.066 Fully Diluted Earnings 0.077 0.070 0.060 0.061 16 - 19 Consolidated Financial Statements * computed as long-term debt divided by stockholders' equity ** computed as long-term debt less cash and cash equivalents divided by stockholders' equity 20 Map of Projects NET TOTAL STOCKHOLDERS' REVENUES insert Consolidated Financial Statements INCOME ASSETS EQUITY and Report of Independent Auditors 7 1 5 , 7 1 9 6 1 9 7 1 2 2 0 3 1 4 , , 4 3 7 5 8 , 9 8 , 3 8 1 , 9 5 7 , 2 , 7 8 0 5 0 2 1 6 , 3 9 3 8 9 7 , , 1 9 7 5 5 0 7 , 2 , 8 2 2 4 , 4 3 2 8 COVER STORY , , , 5 8 8 , 4 8 1 2 7 , 7 2 9 6 6 2 , 2 1 5 1 6 5 , 2 4 1 6 , 7 2 Filinvest Land, Inc. -

Filinvest Development Corporation 2010 Annual Report COVER STORY

1 Filinvest Development Corporation 2010 Annual Report COVER STORY LIGHT OF PROGRESS. Filinvest Development Corporation (FDC) radiates growth and progress, lighting the way with the same dynamism and commitment to excellence that have sustained the company for over half a century. For 2011, FDC will take advantage of brighter economic conditions by diversifying into high-growth areas such as power generation and making strategic investments while keeping its foothold in its core property business. CONTENTS 1 Financial Highlights 2 Joint Message of the Chairman and the President 7 Operational Highlights 19 Board of Directors & Senior Management 20 Consolidated Financial Statements 1 Filinvest Development Corporation 2010 Annual Report FILINVEST DEVELOPMENT CORPORATION AND SUBSIDIARIES FINANCIAL HIGHLIGHTS (Amounts in Thousands of Pesos, Except Per Share Data) 2010 2009 2008 2007 2006 OPERATING RESULTS Total Revenues and Other Income 21,919,047 15,979,223 13,513,233 10,045,534 8,591,612 Net Income 4,936,824 2,765,144 2,570,978 3,343,527 2,080,731 Return on Assets (ave.) 2.9% 1.9% 2.1% 3.3% 2.5% Return on Equity (ave.) 7.7% 4.5% 4.4% 7.0% 5.8% FINANCIAL POSITION Total Assets 180,162,427 164,627,536 131,338,400 114,560,720 85,679,486 Total Long-term Debt 26,251,694 25,496,120 18,675,610 9,781,449 11,709,180 Equity 66,479,685 62,367,272 59,681,553 58,431,383 36,702,929 No. of Shares Outstanding (‘000) 7,505,725 7,505,725 7,505,725 7,505,725 5,955,725 Debt to Equity* 39.5% 40.9% 31.3% 16.7% 31.9% Net Debt to Equity** 11.6% 4.9% 8.5% -8.8% 8.3% -

Download Sales Kit

Embrace a life of ease * Artist’s perspective 01 | The Studio Life What You Dream, We Make What every Filipino can dream of, Filinvest Land Inc. (FLI) can do. From a humble first home to lasting legacies, the company accommodates it. - More than half a century in the business. - A great track record with a varied property portfolio. - Developed over 2,500 hectares of land and more than 600,000 square meters of prime office, residential, and retail spaces. Each square meter developed is a Filipino’s dream fulfilled. 02 | Studio N * Actual photo 03 | Where work and life meet balance Where work and life meet balance Filinvest City is a future-ready garden city in the middle of Alabang. An exceptional place to be, Filinvest lets you gain access to business hubs for working professionals, schools and colleges for students, and garden for everyone. Residing in Filinvest City means being away from the hustle and bustle of the city without compromising your work life and without going too far from civilization. 04 | Studio N Hospital TO DAANG HARI TO LAS PINAS Restaurant / Food WESTGATE Grocery SPECTRUM NORTHGATE PARKWAY COMMERCE AVENUE Shopping NORTHGATE AVENUE PROMENADE Parkway Corporate Center Corporate Building Northgate Cyberzone BRIDGEWAYBRIDGEWAY AVENUE AVENUE Transpo Terminal Festival Mall FILINVEST EXIT F@stbytes Filinvest City TO LAGUNA Grounds CITY CENTER Asian Hospital and Medical Center Ospital ng Muntinlupa SOUTH STATION CIVIC PLAZA TO AIRPORT TO SKYWAY TO MAKATI SOUTH LUZON EXPRESSWAY In the middle of Filinvest City is Northgate Cyberzone, where most of the business hubs are. Northgate Cyberzone is, by far, one of the most accessible areas in the South because of its 24/7 access to public transport. -

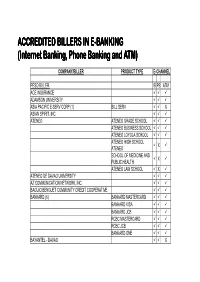

Internet Banking, Phone Banking and ATM)

ACCREDITED BILLERS IN EE----BANKINGBANKING (Internet Banking, Phone Banking and ATM) COMPANY/BILLER PRODUCT TYPE E-CHANNEL PESO BILLER: IB PB ATM ACE INSURANCE ADAMSON UNIVERSITY ASIA PACIFIC E-SERV CORP (1) BILL SERV X ASIAN SPIRIT, INC. ATENEO ATENEO GRADE SCHOOL ATENEO BUSINESS SCHOOL ATENEO LOYOLA SCHOOL ATENEO HIGH SCHOOL X ATENEO SCHOOL OF MEDICINE AND X PUBLIC HEALTH ATENEO LAW SCHOOL X ATENEO DE DAVAO UNIVERSITY AZ COMMUNICATION NETWORK, INC. BAGUIO BENGUET COMMUNITY CREDIT COOPERATIVE BANKARD (6) BANKARD MASTERCARD BANKARD VISA BANKARD JCB RCBC MASTERCARD RCBC JCB BANKARD ONE BAYANTEL - DAVAO X BAYANTEL - GMA X BDO CREDIT CARD (8) MASTERCARD VISA JCB AMEX VISA PURCHASING VISA DISTRIBUTION SM PARTNER PLUS COMMERCIAL CARD CHINA UNION PAY BDO INSURANCE BROKERS INC. (16) HULL BANKERS BLANKET BOND BOND CGL ENGINEERING FIRE/HOME SECURE GROUP LIFE GROUP PA HEALTH INDIVIDUAL LIFE/PESO SECURE INDIVIDUAL PA/ACCIDENT SECURE MARINE CARGO CASUALTY/FLOATER MOTOR/MOTOR SECURE TRAVEL PA/TRAVEL SECURE MRI BDO SUPERLITE CABLELINK-PARAÑAQUE CABLE TV CASTROL PHILIPPINES, INC. X CEBU PACIFIC AIR, INC. X X CENTRAL CATV (SKYCABLE) X CENTRAL CATV (ZPDEE) X CITIBANK (5) MASTERCARD VISA READY CREDIT MLA/CEBU READY CREDIT INSTALLMENT CITIBANK ISO CITISECONLINE.COM X CROSS CREEK DEVELOPMENT CORPORATION DHL EXPRESS (PHILIPPINES) CORP. DIAL CODE PHILIPPINES X DIGITEL X X DIRECTORY PHILS CORP (DPC) E-CENSUS (UNISYS) EASTERN TELECOMMUNICATIONS PHILIPPINES INC X EAST WEST BANK CREDIT CARD X ELITE UNION ONE SERVICES CORPORATION FEDERAL PHOENIX ASSURANCE CO X X FILINVEST LAND, INC. GENERALI-LIFE GENERALI-NON LIFE GLOBE TELECOM INC. (1) GLOBE HANDYPHONE GREENPEACE FOUNDATION INC HSBC CREDIT CARD HSBC PERSONAL LOAN ILIGAN CEMENT X INFOCOM TECHNOLOGIES INC.