Hm1.3 Housing Tenures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Affordable Housing Lease Addendum HOME And/Or NHTF Assisted

Affordable Housing Lease Addendum HOME and/or NHTF Assisted It is possible that the unit for which you are applying has been assisted with federal funds and is governed by the HOME Investment Partnerships Program 24 CFR Part 92 or the National Housing Trust Fund Program (NHTF) 24 CFR Part 93, as amended. The HOME program requires that in order to be eligible for admittance into this unit, your total household annual income must be at or below 50% of median income (very low- income as defined under 24 CFR Part 92). The National Housing Trust Fund program requires that in order to be eligible for admittance into this unit, your total household annual income must be at or below 30% of median income (extremely low-income as defined under 24 CFR Part 93). If your unit is initially designated as a HOME unit and after initial occupancy and income determination, your total household annual income increases above 80% of median income (low-income as defined under 24 CFR Part 92), you will be required to pay 30% of your adjusted gross monthly income for rent and utilities, except that tenants of HOME-assisted units that have been allocated low-income housing tax credits by a housing credit agency pursuant to section 42 of the Internal Revenue Code of 1986 (26 U.S.C.42) must pay rent governed by section 42. If your unit is initially designated as a NHTF unit and after initial occupancy and income determination, your total household annual income increases above 30% of median income (household is no longer extremely low income), you may stay in your NHTF assisted unit. -

Ending Homelessness for Families: the Evidence for Affordable Housing

Ending Homelessness for Families The Evidence for Affordable Housing Marybeth Shinn Community development corporations (CDCs) help revitalize communities and meet the affordable housing needs of low-income families. By offering residents such services as employ- ment support, financial literacy training and after-school activities, many organizations also effectively propel families to greater social well-being and economic self-sufficiency. CDCs can further strengthen families and communities by working to end family homeless- ness. Communities are increasingly adopting new strategies to prevent homelessness and to rapidly secure permanent housing for families when they do become homeless. These commu- nity-based organizations are shifting practices and achieving results. But substantive progress requires broader networks and commitments, including the expertise and resources of the affordable housing and community development industry. Enterprise Community Partners and the National Alliance to End Homelessness are committed to working together to forge local part- nerships that end family homelessness. he continuing crisis in affordable housing has led returns to stable housing and shows that housing Tto a situation in which all too many poor fami- that families can afford is sufficient to end home- lies have become homeless. Many of these parents lessness – or to prevent it – for most families. came of age when housing costs were high, and they Extensive research demonstrates that housing sub- were never able to break into the housing market. sidies solve homelessness for the majority of fami- Others have lost housing and cannot find a new lies. In some jurisdictions, programs have home that they can afford. For the vast majority of succeeded in re-housing families even without families, affordable housing, typically secured with a ongoing subsidies. -

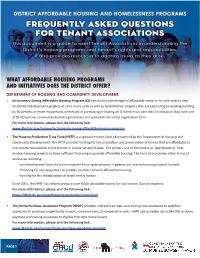

What Affordable Housing Programs and Initiatives

WHAT AFFORDABLE HOUSING PROGRAMS AND INITIATIVES DOES THE DISTRICT OFFER? DEPARTMENT OF HOUSING AND COMMUNITY DEVELOPMENT: • Inclusionary Zoning Affordable Housing Program (IZ) sets aside a percentage of affordable rental or for-sale units in new residential development projects of 10 or more units as well as rehabilitation projects that are expanding an existing building by 50 percent or more. Households interested in purchasing or leasing an IZ home must take the IZ orientation class with one of DHCD partner community-based organizations and complete the online registration form. For more information, please visit the following link: www.dhcd.dc.gov/service/inclusionary-zoning-affordable-housing-program • The Housing Production Trust Fund (HPTF) is a special revenue fund administered by the Department of Housing and Community Development. The HPTF provides funding for the production and preservation of homes that are affordable to low-income households in the District in a wide variety of ways. The primary use of the fund is as “gap financing” that enables housing projects to have sufficient financing to provide affordable housing. The fund also provides other forms of assistance including: - pre-development loans to assist nonprofit housing developers in getting low income housing projects funded; - financing for site acquisition to provide locations to build affordable housing; - funding for the rehabilitation of single family homes. Since 2001, the HPTF has helped produce over 9,000 affordable homes for low income District residents. For more information, please visit the following link: https://dhcd.dc.gov/page/housing-production-trust-fund • The Home Purchase Assistance Program (HPAP) provides interest-free loans and closing cost assistance to qualified applicants to purchase single-family houses, condominiums, or cooperative units. -

PVD Affordable Housing Appraisal Guide 2019

KANSAS DEPARTMENT OF REVENUE DIVISION OF PROPERTY VALUATION AFFORDABLE HOUSING APPRAISAL GUIDE for the STATE OF KANSAS 2021 EFFECTIVE DATE OF APPRAISAL GUIDE JANUARY 1, 2021 Division of Property Valuation, 300 SW 29th St., PO Box 3506, Topeka, KS 66601-3506 Phone (785)296-2365 Fax (785)296-2320 http://www.ksrevenue.org/pvd Affordable Housing Appraisal Guide - 2021 TABLE OF CONTENTS INTRODUCTION ................................................................................................................. 2 PURPOSE ........................................................................................................................... 4 APPRAISAL REQUIREMENTS .............................................................................................. 4 WHAT IS AFFORDABLE HOUSING? ..................................................................................... 8 AFFORDABLE HOUSING PROGRAM OVERVIEW .................................................................. 9 AFFORDABLE HOUSING RESOURCES ................................................................................. 13 AFFORDABLE HOUSING APPRAISAL INFORMATION .......................................................... 14 CAPITALIZATION RATE ANALYSIS ...................................................................................... 17 INCOME VALUATION TEMPLATE ....................................................................................... 25 NON-STABILIZED PROPERTIES .......................................................................................... -

Single-Room Occupancy Uses

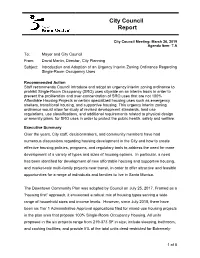

City Council Report City Council Meeting: March 26, 2019 Agenda Item: 7.A To: Mayor and City Council From: David Martin, Director, City Planning Subject: Introduction and Adoption of an Urgency Interim Zoning Ordinance Regarding Single-Room Occupancy Uses Recommended Action Staff recommends Council introduce and adopt an urgency interim zoning ordinance to prohibit Single-Room Occupancy (SRO) uses citywide on an interim basis in order to prevent the proliferation and over-concentration of SRO uses that are not 100% Affordable Housing Projects or certain specialized housing uses such as emergency shelters, transitional housing, and supportive housing. This urgency interim zoning ordinance would allow for study of revised development standards, land use regulations, use classifications, and additional requirements related to physical design or amenity plans, for SRO uses in order to protect the public health, safety and welfare. Executive Summary Over the years, City staff, decisionmakers, and community members have had numerous discussions regarding housing development in the City and how to create effective housing policies, programs, and regulatory tools to address the need for more development of a variety of types and sizes of housing options. In particular, a need has been identified for development of new affordable housing and supportive housing, and market-rate multi-family projects near transit, in order to offer attractive and feasible opportunities for a range of individuals and families to live in Santa Monica. The Downtown Community Plan was adopted by Council on July 25, 2017. Framed as a “housing first” approach, it envisioned a robust mix of housing types serving a wide range of household sizes and income levels. -

DC's Vanishing Affordable Housing

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-8173 www.dcfpi.org March 12, 2015 Going, Going, Gone: DC’s Vanishing Affordable Housing By Wes Rivers Introduction Rapidly rising housing costs led to a substantial loss of low-cost rental housing in the District over the last decade, yet there was little growth in wages for many residents, which means that rent is increasingly eating away at household budgets. As the District’s high cost of living continues to outpace incomes, more and more residents struggle to pay for housing while also meeting other necessities like food, clothing, health care, and transportation. The loss of affordable housing threatens the physical and mental health of families, makes it harder for adults to find and keep a job, creates instability for children that makes it hard to focus at school, and leaves thousands at risk of homelessness at any given moment. This analysis looks at the costs of rent and utilities paid by District residents over the last decade, and how these trends have affected residents’ ability to afford and live in DC, using data from the Census Bureau’s American Community Survey. The findings suggest that policymakers need a comprehensive strategy to preserve the low-cost housing that now exists and to create more affordable housing options in the city. Rents have grown sharply but incomes have not for many DC households. For example, rents for residents with incomes of about $22,000 a year increased $250 a month over the past decade, adjusting for inflation, while incomes remained flat. -

Ph6.1 Rental Regulation

OECD Affordable Housing Database – http://oe.cd/ahd OECD Directorate of Employment, Labour and Social Affairs - Social Policy Division PH6.1 RENTAL REGULATION Definitions and methodology This indicator presents information on key aspects of regulation in the private rental sector, mainly collected through the OECD Questionnaire on Affordable and Social Housing (QuASH). It presents information on rent control, tenant-landlord relations, lease type and duration, regulations regarding the quality of rental dwellings, and measures regulating short-term holiday rentals. It also presents public supports in the private rental market that were introduced in response to the COVID-19 pandemic. Information on rent control considers the following dimensions: the control of initial rent levels, whether the initial rents are freely negotiated between the landlord and tenants or there are specific rules determining the amount of rent landlords are allowed to ask; and regular rent increases – that is, whether rent levels regularly increase through some mechanism established by law, e.g. adjustments in line with the consumer price index (CPI). Lease features concerns information on whether the duration of rental contracts can be freely negotiated, as well as their typical minimum duration and the deposit to be paid by the tenant. Information on tenant-landlord relations concerns information on what constitute a legitimate reason for the landlord to terminate the lease contract, the necessary notice period, and whether there are cases when eviction is not permitted. Information on the quality of rental housing refers to the presence of regulations to ensure a minimum level of quality, the administrative level responsible for regulating dwelling quality, as well as the characteristics of “decent” rental dwellings. -

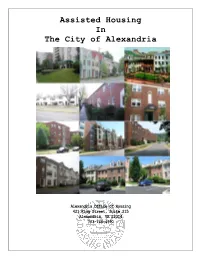

2019 Assisted Housing List

Assisted Housing In The City of Alexandria Alexandria Office of Housing 421 King Street, Suite 215 Alexandria, VA 22314 703-746-4990 ASSISTED HOUSING PROGRAMS IN THE CITY OF ALEXANDRIA Within Alexandria, both public and private owners of rental housing offer assisted housing affordable to low and moderate income residents of the City through participation in state, local or federal programs. These units are available to income eligible households and some programs give priority or restrict admission to specific populations such as elderly or disabled residents. Public Housing and the Housing Choice Voucher Program The Alexandria Redevelopment and Housing Authority (ARHA) owns and manages public housing in the City of Alexandria. ARHA also administers the federal Housing Choice Voucher program (formerly known as the Section 8 program.) Both programs have waiting lists maintained by ARHA. ARHA owns almost 1200 housing units in the City of Alexandria, most of which were built or acquired using federal public housing funds. These units include townhouses, apartments and condominium units, and are located throughout the City. Public housing residents pay 30% of the household’s adjusted income for rent ARHA also administers the Federal Housing Choice Voucher rental subsidy program (formerly knows as the Section 8 Program) for the City of Alexandria. Participants in the Housing Choice Voucher Program receive assistance to rent privately-owned housing units that are located in apartment complexes, condominiums, townhouses, or single-family homes. For more information contact ARHA directly at (703) 549-7115. Additional information can be found on ARHA’s website at www.arha.us. Privately Owned Subsidized Housing Some multifamily apartment complexes participate in federal programs that are subsidized through programs that allow eligible households to pay 30% of their income for rent. -

The Impact of Affordable Housing on Communities and Households

Discussion Paper The Impact of Affordable Housing on Communities and Households Spencer Agnew Graduate Student University of Minnesota, Humphrey Institute of Public Affairs Research and Evaluation Unit Table of Contents Executive Summary ............................................................................................................ 3 Chapter 1: Does Affordable Housing Impact Surrounding Property Values? .................... 5 Chapter 2: Does Affordable Housing Impact Neighborhood Crime? .............................. 10 Chapter 3: Does Affordable Housing Impact Health Outcomes? ..................................... 14 Chapter 4: Does Affordable Housing Impact Education Outcomes? ............................... 19 Chapter 5: Does Affordable Housing Impact Wealth Accumulation, Work, and Public Service Dependence? ........................................................................................................ 24 2 Executive Summary Minnesota Housing finances and advances affordable housing opportunities for low and moderate income Minnesotans to enhance quality of life and foster strong communities. Overview Affordable housing organizations are concerned primarily with helping as many low and moderate income households as possible achieve decent, affordable housing. But housing units do not exist in a vacuum; they affect the neighborhoods they are located in, as well as the lives of their residents. The mission statement of Minnesota Housing (stated above) reiterates the connections between housing, community, and quality -

Secure Tenure for Home Ownership and Economic Development on Land Subject to Native Title

Secure tenure for home ownership and economic development on land subject to native title Ed Wensing and Jonathan Taylor AIATSIS Research DiscussioN Paper NUMBER 31 August 2012 Wensing, E & Taylor, J 2012, Secure tenure options for home ownership and economic development on land subject to native title, AIATSIS research discussion paper no. 31, AIATSIS Research Publications, canberra. Secure tenure for home ownership and economic development on land subject to native title Ed Wensing and Jonathan Taylor AIATSIS Research Discussion Paper No. 31 First published in 2012 by AIATSIS Research Publications © Ed Wensing and Jonathan Taylor, 2012 All rights reserved. Apart from any fair dealing for the purpose of private study, research, criticism or review, as permitted under theCopyright Act 1968 (the Act), no part of this article may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording or by any information storage and retrieval system, without prior permission in writing from the publisher. The Act also allows a maximum of one chapter or 10 per cent of this book, whichever is the greater, to be photocopied or distributed digitally by any educational institution for its educational purposes, provided that the educational institution (or body that administers it) has given a remuneration notice to Copyright Agency Limited (CAL) under the Act. The views expressed in this series are those of the authors and do not necessarily reflect the official policy or position of the Australian Institute of Aboriginal and Torres Strait Islander Studies. Australian Institute of Aboriginal and Torres Strait Islander Studies (AIATSIS) GPO Box 553, Canberra ACT 2601 Phone: (61 2) 6246 1111 Fax: (61 2) 6261 4285 Email: [email protected] Web: www.aiatsis.gov.au National Library of Australia Cataloguing-in-Publication entry: Author: Wensing, Ed (Edward George) Title: Secure tenure for home ownership and economic development on land subject to Native Title / Ed Wensing & Jonathan Taylor. -

Connecting Residents of Subsidized Housing with Mainstream Supportive Services: Challenges and Recommendations

Connecting Residents of Subsidized Housing with Mainstream Supportive Services: Challenges and Recommendations Rebecca Cohen December 2010 Connecting Residents of Subsidized Housing with Mainstream Supportive Services: Challenges and Recommendations Rebecca Cohen Center for Housing Policy December 2010 The research contained herein is part of the What Works Collaborative, which provides rapid response analysis and research to HUD to help inform the implementation of a forward‐looking housing and urban policy agenda. The Research Collaborative is supported by The Rockefeller Foundation, Surdna Foundation Inc., The Ford Foundation and the John D. and Catherine T. MacArthur Foundation. The findings in this report are those of the authors alone, and do not necessarily reflect the opinions of the What Works Collaborative or The Rockefeller Foundation, Surdna Foundation, Inc., The Ford Foundation, The John D. and Catherine T. MacArthur Foundation, The Kresge Foundation, or the Annie E. Casey Foundation. Acknowledgements The author would like to acknowledge the invaluable assistance of Bill Kelly and Paul Weech of Stewards of Affordable Housing for the Future in conceptualizing and providing feedback on earlier drafts of this report, as well as the assistance of Judy Chavis, Mary Cunningham, Ted Houghton, Stuart Kaplan, Jan Monks, Ruth Schwartz, Lexi Turner, and Evelyn Wolff. Special thanks to Maureen Friar, Rick Haughey, and Jeffrey Lubell. Individuals from the following organizations were also consulted in preparation of this report: Alternative -

Owning Or Renting in the US: Shifting Dynamics of the Housing Market

PENN IUR BRIEF Owning or Renting in the US: Shifting Dynamics of the Housing Market BY SUSAN WACHTER AND ARTHUR ACOLIN MAY 2016 Photo by Joseph Wingenfeld, via Flickr. 2 Penn IUR Brief | Owning or Renting in the US: Shifting Dynamics of the Housing Market Full paper is Current Homeownership Outcomes available on the Penn IUR website at penniur.upenn.edu The nation’s homeownership rate was remarkably steady between the 1960s and the 1990s, following a rapid rise in the two decades after World War II, with two-thirds of the nation’s households owning. Over the most recent 20 years, however, homeownership outcomes have been volatile. The research we summarize here identifies drivers of this volatility and the newly observed lows in homeownership. We ask under what circumstances this is a “new normal.” We begin by reviewing current homeownership outcomes. In the section which follows we present evidence on the causes of the current lows. In the third section we develop scenarios for homeownership rates going forward. The U.S. homeownership rate is now at a 48 year low at 63.7 percent (Fig. 1). Homeownership rates have declined for all demographic age groups (Table 1). Since 2006, the number of households who own their home in the U.S. has decreased by 674,000 while the number of renters has increased by over 8 million (Fig. 2). This is a dramatic reversal from the rate of increase of more than 1 percent annually in the number of homeowners from 1980 to 2000 (U.S. Census 2016a)1.