Mergers & Acquisitions Quarterly Switzerland

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Uni-Fuel System, a Simple and Modern Way to Improve Fuel Consumption and Energy Generating Costs - the Sulzer S20 Diesel Engine As a Basic Model

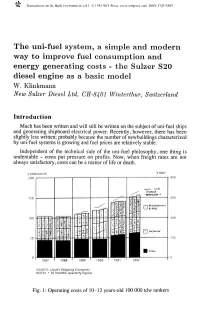

Transactions on the Built Environment vol 1, © 1993 WIT Press, www.witpress.com, ISSN 1743-3509 The uni-fuel system, a simple and modern way to improve fuel consumption and energy generating costs - the Sulzer S20 diesel engine as a basic model W. Klinkmann New Sulzer Diesel Ltd, CH-8401 Winterthur, Switzerland Introduction Much has been written and will still be written on the subject of uni-fuel ships and generating shipboard electrical power. Recently, however, there has been slightly less written; probably because the number of newbuildings characterized by uni-fuel systems is growing and fuel prices are relatively stable. Independent of the technical side of the uni-fuel philosophy, one thing is undeniable - costs put pressure on profits. Now, when freight rates are not always satisfactory, costs can be a matter of life or death. S'OOO* 600 200 1987 1988 1990 SOURCE: Lloyd's Shipping Economist NOTES: * 30 months; quarterly figures Fig. 1: Operating costs of 10-12 years-old 100 000 tdw tankers 12 8 MarinTransactionse Engineerin on the Built Environmentg vol 1, © 1993 WIT Press, www.witpress.com, ISSN 1743-3509 The Principal Economic Parameter Shipping and related activities are risky businesses with high investments and market environments which are highly volatile. The output of ships (tonne-miles) only takes place when vessels are at sea. Reliability of ships and their machinery are therefore of eminent economical importance. The following formula gives us a good basis for judging the influence which different parameters have on -

Customer Protection Climate and Insurance Education

Climate and insurance Trying to anticipate climate effects and to predict the course of water Education Apprentices abroad; gateways to working in insurance Customer protection Specialist knowledge at customer level; the ombuds office up close The annual magazine of the Swiss Insurance Association Annual General Meeting 2019 Table of contents SOCIAL SECURITY CLIMATE APPRENTICES AND EMPLOYEES CUSTOMER PROTECTION TECHNOLOGY 08 14 22 26 32 ANNUAL MAGAZINE 2018 MAGAZINE ANNUAL NEW HORIZONS POTENTIAL SCENARIOS RADICAL CHANGES CHOICE COMES WITH OBLIGATIONS SPECIFIC COMPETENCIES A Swiss community invents a new policy agenda on Ignoring climate change is not an option A year abroad for VersicherungsKV apprentices Efficient markets offer broad choices Trust is indispensable in artificial intelligence ageing. INVESTMENT BERNARD DIETRICH PETER MAAS CUSTOMER BENEFITS DONALD DESAX Sustainable investment – more than a mere idea Diversity is key – not least in employment Customers need to realise that regulation comes with Chatbots extend human know-how The Second Pillar is suffering from a systemic crisis. a price tag RONNY ZÜRCHER JÉRÔME COSANDEY Efficient insurance coverage may block MARTIN LORENZON Avenir Suisse in favour of mandatory care capital. prevention efforts Trust by both sides is essential in ombudswork DISCUSSION MEETING 77 HEAD OFFICE Rolf Dörig and Thomas Helbling discuss Swiss Insurance Association member firms Organisation of the SIA head office 06 the challenges in private insurance 36 39 PUBLISHING DETAILS Concept and editorial work: Takashi Sugimoto, Jan Mühlethaler, Sabine Alder, SIA. Content: SIA specialists and experts. Graphic design: Klar für Marken GmbH, Zurich. Photos by: Matthias Auer, KEY FIGURES Zurich, André Springer, Horgen, Keystone, iStock, unsplash. -

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1 [....] Annex A in relation to subsection 1.6 of the contract specifications: Futures on Shares of Produkt- Group Cash Contract Minimum Currency ID ID** Market- Size Price ID** Change* Julius Bär Holding AG - N. BAEG CH01 XSWX 50 0.0010.01 CHF BB Biotech AG BIOF CH01 XSWX 50 0.0010.01 CHF Logitech International S.A. - N. LOGF CH01 XSWX 100 0.00010.01 CHF Pargesa Holding S.A. PARF CH01 XSWX 10 0.0010.01 CHF Sonova Holding AG - N. PHBF CH01 XSWX 50 0.0010.01 CHF PSP Swiss Property AG - N. PSPF CH01 XSWX 50 0.0010.01 CHF Schindler Holding AG SINF CH01 XSWX 50 0.0010.01 CHF Straumann Holding AG STMF CH01 XSWX 10 0.0010.01 CHF Swatch Group AG, The - N. UHRF CH01 XSWX 100 0.00010.01 CHF Valiant Holding AG - N. VATF CH01 XSWX 10 0.0010.01 CHF ABB Ltd. ABBF CH02 XVTX 100 0.00010.01 CHF Adecco S.A. - N. ADEF CH02 XVTX 100 0.0010.01 CHF Actelion Ltd. - N. ATLG CH02 XVTX 50 0.0010.01 CHF Bâloise Holding AG BALF CH02 XVTX 100 0.0010.01 CHF Compagnie Financière Richemont AG CFRH CH02 XVTX 100 0.0010.01 CHF Ciba Spezialitätenchemie Holding AG - N. CIBF CH02 XVTX 10 0.0010.01 CHF Clariant AG - N. CLNF CH02 XVTX 100 0.00010.01 CHF Credit Suisse Group - N. CSGG CH02 XVTX 100 0.00010.01 CHF Geberit AG - N. -

Report of the Director

International Foundation HFSJG Activity Report 2007 Report of the Director After the jubilee period 2005 - 2006, the period covered by this report can be marked as “back to normal”. As documented by the individual reports that have been prepared by the respective research groups, the year 2007 was again extremely rich in scientific activity at both sites Jungfraujoch and Gornergrat. Therefore, the main goal of the International Foundation High Altitude Research Stations Jungfraujoch and Gornergrat (HFSJG), i.e. providing infrastructure and support for scientific research of international significance that must be carried out at an altitude of 3000-3500 meters above sea level or for which a high alpine climate and environment are necessary, was successfully pursued. The Foundation HFSJG On September 7, 2007, the Board of the Foundation HFSJG met at the Hotel Zermatterhof in Zermatt for its regular meeting. The president, Prof. Hans Balsiger, had the honor to welcome the members of the board, representatives of the Jungfraujoch Commission of the Swiss Academy of Sciences (scnat), of the Astronomic Commission HFSJG, of the Swiss National Science Foundation, and a small number of distinguished guests. Unfortunately, Mr. Balsiger had to excuse the absence of an Italian delegate. The Istituto Nazionale di Astrofisica INAF and the foundation HFSJG are currently in negotiations about INAF’s membership and financial contribution since there are no longer any scientific activities at Gornergrat involving Italian institutions. In the statutory part of the meeting the annual activity report 2006 as well as the statement of accounts for 2006 were approved unanimously and with no abstentions. -

Bericht Über Die Solvabilität Und Finanzlage 2016

Helvetia Versicherungs- Aktiengesellschaft Bericht über die Solvabilität und Finanzlage 2016 Ihre Schweizer Versicherung. Inhaltsverzeichnis Zusammenfassung 4 B.5. Funktion der internen Revision 22 B.6. Versicherungsmathematische Funktion 22 Geschäftstätigkeit und A. Geschäftsergebnis 5 B . 7. Outsourcing 22 A.1. Geschäftstätigkeit 5 B.8. Sonstige Angaben 23 A.1.1. Allgemeines 5 A.1.2. Konzernstruktur 5 C. Risikoprofil 24 A.1.3. Wesentliche Beteiligungen 7 C.1. Versicherungstechnisches Risiko 24 A.1.4. Aufsicht 7 C.2. Marktrisiko 25 A.1.5. Abschlussprüfer 7 C.2.1. Zinsrisiko 26 A.1.6. Wesentliche Geschäftsbereiche 8 C.2.2. Spreadrisiko 27 Wesentliche Ereignisse im C.2.3. Immobilienrisiko 27 A .1. 7. Geschäftsjahr 8 C.2.4. Risikosteuerung 28 A.2. Versicherungstechnische Leistung 8 C.3. Kreditrisiko 28 A.3. Anlageergebnis 10 C.4. Liquiditätsrisiko 31 A.4. Entwicklung sonstiger Tätigkeiten 11 C.5. Operationelles Risiko 32 A.5. Sonstige Angaben 11 C.6. Andere wesentliche Risiken 35 C . 7. Sonstige Angaben 36 B. Governance-System 12 Allgemeine Angaben zum Bewertung für B.1. Governance-System 12 D. Solvabilitätszwecke 37 B.1.1. Aufsichtsrat 12 D.1. Vermögenswerte 38 B.1.2. Vorstand 12 D.1.1. Finanzanlagen 38 B.1.3. Ausschüsse 13 D.1.2. Anlagefonds 39 B.1.4. Schlüsselfunktionen 14 Anteil Rückversicherer an B.1.4.1. Risikomanagementfunktion 14 den Rückstellungen für D.1.3. Versicherungsverträge 39 B.1.4.2. Versicherungsmathematische Funktion 15 D.1.4. Sonstige 39 B.1.4.3. Compliance-Funktion 15 D.2. Versicherungstechnische Rückstellungen 39 B.1.4.4. Interne Revision 15 D.3. -

Q1 2014 and Outlook 2014 3

Mergers & Acquisitions Quarterly Switzerland First quarter 2014 April 2014 edition DRAFT Contents 1. Introduction 2 2. Swiss M&A market Q1 2014 and outlook 2014 3 3. Private equity statistics: Germany, Switzerland and Austria 6 4. Industry overview ► Chemicals, Construction and Materials 7 ► Energy and Utilities 9 ► Financial Services 11 ► Healthcare 13 ► Industrial Goods and Services 15 ► Media, Technology and Telecommunications 17 ► Retail and Consumer Products 19 5. Deal of the quarter 21 6. Event calender 22 7. EY selection of M&A opportunities 23 8. Your EY M&A team in Switzerland 24 9. Subscription/Registration form 25 All rights reserved — EY 2014 Mergers & Acquisitions Quarterly Switzerland – Q1 2014 1 DRAFT Introduction Dear Reader We are pleased to present the latest edition of our M&A Quarterly Switzerland. This brochure provides a general overview of the Swiss M&A and European private equity market activity in the first quarter of 2014, as well as an outlook for the remainder of 2014. Following a year of subdued performance, the Swiss M&A market got off to a remarkable start in the first three months of 2014, with a significant increase in deal volume despite a decrease in the number of deals. Looking forward, large transactions are expected more often in the Swiss M&A market as executives’ risk appetite for strategic and transformational deals has increased. The favorable financing conditions prevailing at present will help drive this trend, although continuing economic and geopolitical risks in some areas could disrupt the bright outlook. Our next edition of Mergers & Acquisitions Quarterly Switzerland will be available in July 2014. -

Switzerland Fund A-CHF for Investment Professionals Only FIDELITY FUNDS MONTHLY PROFESSIONAL FACTSHEET SWITZERLAND FUND A-CHF 31 AUGUST 2021

pro.en.xx.20210831.LU0054754816.pdf Switzerland Fund A-CHF For Investment Professionals Only FIDELITY FUNDS MONTHLY PROFESSIONAL FACTSHEET SWITZERLAND FUND A-CHF 31 AUGUST 2021 Strategy Fund Facts The Portfolio Managers are bottom-up investors who believe share prices are Launch date: 13.02.95 correlated to earnings, and that strong earners will therefore outperform. They look to Portfolio manager: Andrea Fornoni, Alberto Chiandetti invest in companies where the market underestimates earnings because their Appointed to fund: 01.03.18, 01.08.11 sustainability is not fully appreciated. They also look for situations where the impact Years at Fidelity: 7, 15 company changes will have on earnings has not been fully recognised by the market. Fund size: CHF366m They aim to achieve a balance of different types of companies, so they can deliver Number of positions in fund*: 36 performance without adding undue risk. Fund reference currency: Swiss Franc (CHF) Fund domicile: Luxembourg Fund legal structure: SICAV Management company: FIL Investment Management (Luxembourg) S.A. Capital guarantee: No Portfolio Turnover Cost (PTC): 0.01% Portfolio Turnover Rate (PTR): 28.92% *A definition of positions can be found on page 3 of this factsheet in the section titled “How data is calculated and presented.” Objectives & Investment Policy Share Class Facts • The fund aims to provide long-term capital growth with the level of income expected Other share classes may be available. Please refer to the prospectus for more details. to be low. • The fund will invest at least 70% in Swiss company shares. Launch date: 13.02.95 • The fund has the freedom to invest outside its principal geographies, market sectors, industries or asset classes. -

Keyinvest Return Monitor Systematically Selected UBS Barrier Reverse Convertibles

Structured investment products for clients in Switzerland KeyInvest Return Monitor Systematically selected UBS Barrier Reverse Convertibles The Return Monitor provides an overview of UBS Barrier Reverse Convertibles (BRCs) offering attractive potential returns. All selected BRCs are listed on the SIX Structured Products Exchange and tradeable on each trading day under normal market conditions. In focus are products that have at least three months left until maturity and an intact barrier. The three categories examined are: Attractive sideways return, high barrier distance and underlyings with a Buy Rating by UBS Research. Further information can be found on: ubs.com/renditemonitor Attractive sideways return Barrier distance Coupon p.a. Underlying Ask Currency Expiry Valor Sideways return p.a. (worst performer) 5.50% Bayer / Novartis / Roche / Sanofi 74.30 CHF 14/08/2020 A 39945568 15.1% 30.6% 8.00% CENTRICA PLC / E.ON / Electricite de France 78.70 EUR 10/08/2020 A 42686847 18.7% 28.2% 9.00% Credit Suisse / Deutsche Bank 82.10 CHF 13/07/2020 A 42078534 15.8% 26.3% 9.75% Enel / Fiat Chrysler / UniCredit 85.20 EUR 29/06/2020 39167120 28.3% 23.9% 9.00% Hewlett-Packard / IBM 93.27 USD 06/07/2020 A 42271711 31.2% 15.1% High barrier distance Barrier distance Coupon p.a. Underlying Ask Currency Expiry Valor Sideways return p.a. (worst performer) 12.00% Alcoa Corporation / US STEEL CORP 96.32 USD 12/06/2020 A 44506090 47.5% 15.3% 7.75% Colgate-Palmolive / Estée Lauder / L'Oréal 98.55 USD 22/06/2020 A 41905920 43.9% 15.4% 10.00% Nike / Under Armour Inc. -

University of St. Gallen 2018 Report on Responsibility and Sustainability

University of St. Gallen 2018 Report on Responsibility and Sustainability UN Principles for Responsible Management Education Report on Progress Table of Content Introduction 4–8 Research – Institutes and Centers 9–20 Teaching 21–30 Executive Education 31–34 Student Engagement 35–42 Campus 43–48 Events and Dialogue 49–54 SDG’s 55–57 Policy Statement on Global Responsibility and Sustainability Based on its Vision 2025, the University of St. Gallen has defined the following Policy Statement on Responsibility and Sustainability: 1) As a leading business university, we want to contribute 4) Through our research, we contribute to solving current to solving the challenges of globally responsible action and future problems of globally responsible action and and sustainable development in business and society. sustainable development in business and society. 2) We therefore include pertinent demands in all our ac tivities, 5) We reach out to organizations in business and society to in particular education, student engagement, research, jointly explore and engage in effective approaches to post-experience education, public outreach, infrastructure, meeting the challenges of globally responsible action and and operations. sustainable development. 3) Through our education, we educate entrepreneurial personalities whose actions are informed by social re- sponsibility and sustainability. PICTURES © Universität St. Gallen (HSG) © STÜRMER FOTO St. Gallen Principles for Responsible Management Education (PRME) Principle 1 | Purpose P1 We will develop the capabilities of students to be future generators of sustainable value for business and society at large and to work for an inclusive and sustainable global economy. Principle 2 | Values P2 We will incorporate into our academic activities and curricula the values of global social responsibility as portrayed in international initiatives such as the United Nations Global Compact. -

Internal Combustion Engines Collection of Stationary

ASME International THE COOLSPRING POWER MUSEUM COLLECTION OF STATIONARY INTERNAL COMBUSTION ENGINES MECHANICAL ENGINEERING HERITAGE COLLECTION Coolspring Power Museum Coolspring, Pennsylvania June 16, 2001 The Coolspring Power Museu nternal combustion engines revolutionized the world I around the turn of th 20th century in much the same way that steam engines did a century before. One has only to imagine a coal-fired, steam-powered, air- plane to realize how important internal combustion was to the industrialized world. While the early gas engines were more expensive than the equivalent steam engines, they did not require a boiler and were cheap- er to operate. The Coolspring Power Museum collection documents the early history of the internal- combustion revolution. Almost all of the critical components of hundreds of innovations that 1897 Charter today’s engines have their ori- are no longer used). Some of Gas Engine gins in the period represented the engines represent real engi- by the collection (as well as neering progress; others are more the product of inventive minds avoiding previous patents; but all tell a story. There are few duplications in the collection and only a couple of manufacturers are represent- ed by more than one or two examples. The Coolspring Power Museum contains the largest collection of historically signifi- cant, early internal combustion engines in the country, if not the world. With the exception of a few items in the collection that 2 were driven by the engines, m Collection such as compressors, pumps, and generators, and a few steam and hot air engines shown for comparison purposes, the collection contains only internal combustion engines. -

Künstliche Intelligenz Oder

news September/Oktober 2017 – Ausgabe Schweiz Das Vontobel-Magazin für strukturierte für Produkte Vontobel-Magazin Das deri Künstliche Intelligenz oder: die Evolution des Denkens Titelthema Seite 7 2 derinews – Inhalt 4 Märkte 14 Aktuelle Entwicklungen auf Experteninterview dem Weltmarkt «KI verändert keine Wertschöpfungs- 7 Titelthema ketten, sondern opti- Künstliche Intelligenz oder: miert Prozesse» die Evolution des Denkens 7 12 Titelthema Experteninterview «Jeder Gewinner profitiert auf Künstliche Intelligenz seine Weise» oder: die Evolution des Denkens 13 Wussten Sie, dass … 14 Experteninterview Squirro ist ein Zürcher Jungunternehmen, «Wir stellen relevante Erkenntnisse das wertlose Daten in wirkungsvoll nutzbare Erkenntnisse verwandelt. Ein Gespräch den richtigen Mitarbeitern punkt mit Dorian Selz, dem CEO und Mitgründer. genau zur Verfügung» 16 Themenrückblick Automobilzulieferer profitieren von KI wird bald in nahezu all unseren Elektro und Hybridfahrzeugen Lebensbereichen Anwendung finden; die Dynamik ist stark. 18 Mit künstlicher Intelligenz zu neuen Anlageidee 17 Dimensionen. Eine KI hat beim Schweizer Aktien Bildmotiv dieser Ausgabe eine dritte Trends einfangen, Logitechs Geschäftsmodell ist solide Dimension erschaffen. Sie hat und die Strategieumsetzung ausge dabei selbstständig entschieden, wenn sie beginnen zeichnet wie die Projektionsfläche des ursprünglich zweidimen sionalen Bildes «geformt» werden sollte. 18 Anlageidee Trends einfangen, wenn sie beginnen 20 Know-how «Bitcoin Cash» – was Anleger wissen müssen 22 Aktuelles Vontobel tritt United Nations Global Compact bei 23 Hinweise Editorial – derinews 3 Künstliche Intelligenz – nur ein Erfolgs- rezept aus Science-Fiction-Filmen? Ein Trugschluss. Für uns unsichtbar, hält sie längst Einzug in viele Lebens bereiche. ur bemerken wir es meist nicht. In so gut wie allen Branchen werden selbstlernende Algorithmen dabei immer relevanter. Wie denkende Maschinen mensch liches Leben weiter prägen? Darüber gibt es geteilte NMeinungen. -

FTSE Developed Europe

2 FTSE Russell Publications 19 August 2021 FTSE Developed Europe Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 1&1 AG 0.01 GERMANY Avast 0.03 UNITED Cnp Assurance 0.02 FRANCE 3i Group 0.14 UNITED KINGDOM Coca-Cola HBC AG 0.06 UNITED KINGDOM Aveva Group 0.05 UNITED KINGDOM A P Moller - Maersk A 0.1 DENMARK KINGDOM Coloplast B 0.19 DENMARK A P Moller - Maersk B 0.15 DENMARK Aviva 0.19 UNITED Colruyt 0.03 BELGIUM A2A 0.03 ITALY KINGDOM Commerzbank 0.07 GERMANY Aalberts NV 0.05 NETHERLANDS AXA 0.43 FRANCE Compagnie Financiere Richemont SA 0.55 SWITZERLAND ABB 0.51 SWITZERLAND B&M European Value Retail 0.06 UNITED Compass Group 0.33 UNITED KINGDOM ABN AMRO Bank NV 0.04 NETHERLANDS KINGDOM BAE Systems 0.21 UNITED Acciona S.A. 0.03 SPAIN Continental 0.14 GERMANY KINGDOM Accor 0.06 FRANCE ConvaTec Group 0.05 UNITED Baloise 0.06 SWITZERLAND Ackermans & Van Haaren 0.03 BELGIUM KINGDOM Banca Mediolanum 0.02 ITALY ACS Actividades Cons y Serv 0.06 SPAIN Covestro AG 0.1 GERMANY Banco Bilbao Vizcaya Argentaria 0.36 SPAIN Adecco Group AG 0.09 SWITZERLAND Covivio 0.04 FRANCE Banco Santander 0.58 SPAIN Adevinta 0.04 NORWAY Credit Agricole 0.14 FRANCE Bank Pekao 0.03 POLAND Adidas 0.63 GERMANY Credit Suisse Group 0.22 SWITZERLAND Bankinter 0.03 SPAIN Admiral Group 0.08 UNITED CRH 0.35 UNITED Banque Cantonale Vaudoise 0.02 SWITZERLAND KINGDOM KINGDOM Barclays 0.35 UNITED Adyen 0.62 NETHERLANDS Croda International 0.12 UNITED KINGDOM KINGDOM Aegon NV 0.06 NETHERLANDS Barratt Developments 0.09 UNITED Cts Eventim 0.03 GERMANY Aena SME SA 0.1 SPAIN KINGDOM Cyfrowy Polsat SA 0.02 POLAND Aeroports de Paris 0.03 FRANCE Barry Callebaut 0.07 SWITZERLAND Daimler AG 0.66 GERMANY Ageas 0.09 BELGIUM BASF 0.64 GERMANY Danone 0.37 FRANCE Ahold Delhaize 0.26 NETHERLANDS Bayer AG 0.53 GERMANY Danske Bank A/S 0.1 DENMARK AIB Group 0.02 IRELAND Bechtle 0.04 GERMANY Dassault Aviation S.A.