Download This PDF File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Issn 0856 – 8537 Directorate of Banking

ISSN 0856 – 8537 DIRECTORATE OF BANKING SUPERVISION ANNUAL REPORT 2017 21ST EDITION For any enquiries contact: Directorate of Banking Supervision Bank of Tanzania 2 Mirambo Street 11884 Dar Es Salaam TANZANIA Tel: +255 22 223 5482/3 Fax: +255 22 223 4194 Website: www.bot.go.tz TABLE OF CONTENTS ....................................................................................................... Page LIST OF CHARTS ........................................................................................................................... iv ABBREVIATIONS AND ACRONYMS ............................................................................................ v MESSAGE FROM THE GOVERNOR ........................................................................................... vi FOREWORD BY THE DIRECTOR OF BANKING SUPERVISION .............................................. vii CHAPTER ONE .............................................................................................................................. 1 OVERVIEW OF THE BANKING SECTOR .................................................................................... 1 1.1 Banking Institutions ................................................................................................................. 1 1.2 Branch Network ....................................................................................................................... 1 1.3 Agent Banking ........................................................................................................................ -

Our Values Underpin Our Growth

our values underpin our growth ABC HOLDINGS LIMITED ANNUAL REPORT 2014 ABOUT BancABC ABC HOLDINGS LIMITED IS THE PARENT COMPANY OF A NUMBER OF BANKS OPERATING UNDER THE BANCABC BRAND IN SUB- SAHARAN AFRICA, WITH OPERATIONS IN BOTSWANA, MOZAMBIQUE, TANZANIA, ZAMBIA AND ZIMBABWE. A GROUP SERVICES OFFICE IS LOCATED IN SOUTH AFRICA. Our vision is to be Africa’s preferred banking partner by offering world-class financial solutions. We will realise this by building profitable, lifelong customer relationships through the provision of a wide range of innovative financial products and services – to the benefit of all our stakeholders. The Group offers a diverse range of services, including but not limited to the following: Corporate Banking, treasury services, Retail & SME Banking, asset management and stockbroking. ABC Holdings Limited is registered in Botswana. During 2014, the ABC Holdings Group was acquired by Atlas Mara. As at 31 December 2014, Atlas Mara had a 98.7% equity stake in ABC Holdings, held directly (60.8%) and indirectly (37.9%). Subsequent to the takeover, ABC Holdings was delisted from the Botswana Stock Exchange (primary listing) on 30 January 2015, and from Zimbabwe Stock Exchange (secondary listing) on 12 February 2015. Atlas Mara is a British Virgin Islands registered company with a standard listing on the London Stock Exchange (“LSE”). CONTENTS 1 Our values and highlights 30 Directors and Group management 2 Five-year fi nancial highlights 35 Directors’ responsibility 3 Salient features statement 5 Group Chairman’s & CEO’s 36 Directors’ report report 39 Annual fi nancial statements 13 Corporate social responsibility report 154 Analysis of shareholders 21 Risk and governance report D ABC HOLDINGS LIMITED ANNUAL REPORT 2014 PAGE PAGE PAGE PAGE PAGE 4 12 20 38 116 VALUE 01 VALUE 02 VALUE 03 VALUE 04 VALUE 05 PEOPLE INTEGRITY PROFESSIONALISM PASSION INNOVATION Our core values centre on five distinct areas. -

A Case of Akiba Commercial Bank John

Adoption of mobile banking services by micro, small and medium enterprises in Tanzania: A Case of Akiba Commercial Bank John Leon Masters of Business Administration University of Dar es Salaam, Business School, 2017 Despite benefits of mobile banking technological advancement, customers running SMEs have continued to use traditional banking services characterized by long queues, long distance traveling and time wasting that negatively affect time allocated for other economic activities. This study aimed to assess the adoption of mobile banking services by SMEs in Tanzania using Akiba Commercial Bank as a case study. Out of 13 branches of Akiba Commercial Bank located in Dar es Salaam, 6 of them were selected randomly, where a random sample of 18 bank staff and 180 bank customers running SMEs in the respective branches were also selected to represent the study population. Questionnaires were administered to the randomly selected customers and purposive selected staff. It was found that, out of the interviewed 180 customers running SMEs at Akiba Commercial Bank, the majority of them (57.8%) had a positive perception on the use of the services. Out of them, 74.4% were aware of the existence of various mobile banking services, 17.8% of them were registered with mobile banking services but only 3.9% of the SMEs were using such services. Perceived risks of the banking services was a major reason (84.4%) for the non-use of the mobile banking services, followed by network problems (69.4%), transaction costs (49.7%), perceived complexity in using the services (43.9%), poor skills and knowledge in using the services (27.7%) and poor customer care of the bank (20.8%).Despite the fact that the majority of SMEs had a positive perception on the use of mobile banking services, the level of adoption of the services was very low. -

Peter Mapigano

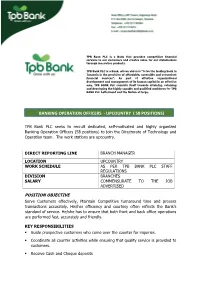

TPB Bank PLC is a Bank that provides competitive financial services to our customers and creates value for our stakeholders through innovative products. TPB Bank PLC is a Bank, whose vision is “to be the leading bank in Tanzania in the provision of affordable, accessible and convenient financial services”. As part of effective organizational development and management of its human capital in an effective way, TPB BANK PLC commits itself towards attaining, retaining and developing the highly capable and qualified workforce for TPB BANK PLC betterment and the Nation at large. BANKING OPERATION OFFICERS - UPCOUNTRY ( 58 POSITIONS) TPB Bank PLC seeks to recruit dedicated, self-motivated and highly organized Banking Operation Officers (58 positions) to join the Directorate of Technology and Operation team. The work stations are upcountry . DIRECT REPORTING LINE BRANCH MANAGER LOCATION UPCOUNTRY WORK SCHEDULE AS PER TPB BANK PLC STAFF REGULATIONS DIVISION BRANCHES SALARY COMMENSURATE TO THE JOB ADVERTISED POSITION OBJECTIVE Serve Customers effectively, Maintain Competitive turnaround time and process transactions accurately. His/her efficiency and courtesy often reflects the Bank’s standard of service. He/she has to ensure that both front and back office operations are performed fast, accurately and friendly. KEY RESPONSIBILITIES . Guide prospective customers who come over the counter for inquiries. Coordinate all counter activities while ensuring that quality service is provided to customers. Receive Cash and Cheque deposits . Posting Transactions . Verify teller proof of cash and teller proof of cheques against actual documents by ticking and signing the printouts. Scrutinize internal vouchers to ensure that they are properly drawn and authorized in line with the approval limits. -

Improving Life

Improving Life through inclusive finance 1 2 3 Preface Letshego Holdings Limited (“Letshego”) was incorporated in 1998, is headquartered in Gaborone and has been publicly listed on the Botswana Stock Exchange since 2002. Today it is one of Botswana’s largest indigenous groups, with a market capitalisation of approximately USD500mn, placing Contents it in the top 50 listed sub-Sahara African companies (ex-South Africa), with an agenda focused on inclusive finance. Through its eleven country presence across Southern, East and West Africa (Botswana, Ghana, Kenya, Lesotho, Mozambique, Namibia, Nigeria, Rwanda, Swaziland, Tanzania and Uganda), Preface 5 its subsidiaries provide simple, appropriate and accessible consumer and micro-finance banking solutions to the financially under-served in a sustainable manner. Letshego Group Structure 6 At Letshego, we are intent on operating a profitable business on a sustainable basis and we are committed to contributing to Our Business – Our Letshego 8 Africa’s growth and prosperity, as well as to improving the lives of our customers. Letshego’s vision is to become Africa’s leading inclusive finance group. Our inclusive finance solutions 9 In 2016, we have launched our customer engagement initiative, the Improving Life Campaign. For the duration of this campaign, we asked our customers to share their stories by telling us how Our history and milestones 10 they have used their loans productively. Prizes were awarded to the customers that had used their loans wisely, that is, generated income for their family while being able to service the loan and Our social impact 12 most of all, impacted society and left the community a better place than they had found it. -

The United Republic of Tanzania the Economic Survey

THE UNITED REPUBLIC OF TANZANIA THE ECONOMIC SURVEY 2017 Produced by: Ministry of Finance and Planning DODOMA-TANZANIA July, 2018 Table of Contents ABBREVIATIONS AND ACRONYMS ......................................... xiii- xvii CHAPTER 1 ................................................................................................. 1 THE DOMESTIC ECONOMY .................................................................... 1 GDP Growth ............................................................................................. 1 Price Trends .............................................................................................. 7 Capital Formation ................................................................................... 35 CHAPTER 2 ............................................................................................... 37 MONEY AND FINANCIAL INSTITUTIONS ......................................... 37 Money Supply ......................................................................................... 37 The Trend of Credit to Central Government and Private Sector ............ 37 Banking Services .................................................................................... 38 Capital Markets and Securities Development ......................................... 37 Social Security Regulatory Authority (SSRA) ....................................... 39 National Social Security Fund (NSSF) ................................................... 40 GEPF Retirement Benefits Fund ........................................................... -

Merger Notification Regarding the Intention Of

MERGER NOTIFICATION REGARDING THE INTENTION OF NATIONAL BANK OF MALAWI TO ACQUIRE 75 PERCENT OF SHARES IN AKIBA COMMERCIAL BANK PUBLIC LIMITED COMPANY PUBLIC NOTICE (Made under Section 65 (2) (g) of the Fair Competition Act No. 8 of 2003 and Rules 41 (6), 42 (5) and 49 of the Competition Rules, 2018) The Fair Competition Commission (FCC) is an independent statutory body established under section 62 of the Fair Competition Act No. 8 of 2003 (FCA) with the object of enhancing the welfare of the people of Tanzania by promoting and protecting effective competition in markets and preventing unfair and misleading market conduct throughout Tanzania Mainland. Under the same Act, the FCC has powers to investigate, inter alia, entry into and exit from markets. The FCC has received a merger notification to the effect that National Bank of Malawi (The Acquiring Firm) intends to acquire shares in Akiba Commercial Bank Public Limited Company (The Target Firm). The Acquiring Firm is a company incorporated in Malawi. It is a leading commercial bank in the Republic of Malawi specialize in a provision of commercial banking services ranging from wholesale banking, treasury and investment banking, to personal and business banking. The Target Firm is a company incorporated under the laws of Tanzania. A full- fledged commercial bank, providing banking, financial and other related commercial banking services. Based on the Share Subscription Agreement dated 31st January 2020, the Acquiring Firm proposed to acquire aggregate of 75 percent of equity stake in Target Firm. FCC is currently investigating the intended acquisition in line with the provisions of the Fair Competition Act and the Competition Rules, 2018. -

Letshego Group Condensed Financial Statements 31 December 2019.Pdf

LETSHEGO HOLDINGS LIMITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019 Letshego Holdings Limited Condensed Consolidated Financial Statements December 2019 TABLE OF CONTENTS Page No Directors' Report 2 Statement of Directors’ Responsibility 3 Report of The Independent Auditors 4 Condensed Consolidated Statements of Financial Position 5 Condensed Consolidated Statements of Profit or Loss and Other Comprehensive Income 6 Condensed Consolidated Statements of Changes in Equity 7 Condensed Consolidated Statements of Cashflows 8 Segment Reporting 9 - 10 Significant accounting policies 11 Notes to the Condensed Consolidated Financial Statements 12 - 18 Financial risk management and Financial instruments 19 - 20 Letshego Holdings Limited Condensed Consolidated Financial Statements December 2019 DIRECTORS’ REPORT For the year ended 31 December 2019 The Board of Directors is pleased to present their report to Shareholders together with the reviewed condensed consolidated financial statements for the year ended 31 December 2019. 1 Financial results The condensed consolidated financial statements adequately disclose the results of the group's operations for year ended 31 December 2019. 2 Dividends An interim dividend of 4.3 thebe per share (Prior year: 8.7 thebe per share) was declared on 28 August 2019. A second and final dividend of 7.7 thebe per share (prior year: 3.3 thebe per share) was declared on 26 February 2020 and will be paid on or about 15 May 2020. 3 The below were the changes that took place during the -

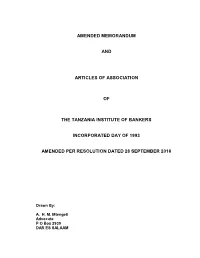

Amended Memorandum And

AMENDED MEMORANDUM AND ARTICLES OF ASSOCIATION OF THE TANZANIA INSTITUTE OF BANKERS INCORPORATED DAY OF 1993 AMENDED PER RESOLUTION DATED 28 SEPTEMBER 2016 Drawn By: A. H. M. Mtengeti Advocate P O Box 2939 DAR ES SALAAM THE COMPANIES ACT CAP 212 COMPANY LIMITED BY GUARANTEE AND NOT HAVING SHARE CAPITAL AMENDMENT TO THE MEMORANDUM OF ASSOCIATION OF THE TANZANIA INSTITUTE OF BANKERS LIMITED INCORPRATION AND NATURE OF THE INSTITUTE 1. The name of the Company is “THE TANZANIA INSTITUTE OF BANKERS LIMITED” a non-profit company incorporated and existing under the laws of the United Republic of Tanzania. 2. The Registered Office of the Institute shall be situated at Dar es Salaam, in the United Republic of Tanzania. 3. The main object for which the Institute is established is to certify professionally qualified bankers in Tanzania. 4. In furtherance of the object set out in clause 3 above, the Institute shall have the following roles: i. To play a leading role as the professional body for persons engaged in the banking and financial services industry, to promote the highest standards of competence, practice and conduct among persons engaged in the banking and financial services industry, and to assist in the professional development of its Members, whether by means of examination, awards, certification or otherwise and ensure quality assurance. ii. To promote, encourage and advance knowledge and best practices in banking and financial services in all their aspects, whether conventional or Islamic, and any other products or activities as may, from time to time, be undertaken by the banks and financial institutions. -

Pdf 165.9 KB

THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION FOR THE PURPOSES OF ARTICLE 7 OF THE MARKET ABUSE REGULATION (EU) NO. 596/2014. 30 April 2019 Proposed Strategic Transaction with Equity Group Holdings Atlas Mara Limited ("Atlas Mara" or the "Company" and including its subsidiaries, the “Group”), the sub- Saharan African financial services group, announces that it has entered into a binding term sheet with Equity Group Holdings Plc (“EGH”) for the exchange of certain banking assets of the Company in four countries for ordinary shares in EGH (the “Proposed Transaction”). The Proposed Transaction is subject to confirmatory due diligence, definitive transaction documentation, relevant regulatory approvals, and other conditions precedent customary for transactions of this nature. As part of the Proposed Transaction, EGH would acquire for shares in EGH Atlas Mara’s 62% shareholding in Banque Populaire du Rwanda (BPR) and, via the Company’s subsidiary ABC Holdings Limited, all of Atlas Mara’s indirect interests in African Banking Corporation Zambia (BancABC Zambia), African Banking Corporation Tanzania (BancABC Tanzania), and African Banking Corporation Mozambique (BancABC Mozambique). The parties would anticipate mergers of their respective banks within each of Rwanda and Tanzania. The Company expects to receive as consideration approximately 252,482,300 ordinary shares of EGH representing approximately 6.27% of the pro forma share capital of EGH post-closing. This implies the consideration to be paid is the equivalent of approximately USD 105.4 million. The aggregate consideration ultimately payable will be that set out in the definitive agreements negotiated following confirmatory due diligence, and may be subject to adjustment (positive or negative), based on the performance of the banks through consummation of the transactions, and on the net asset value of the banks at the time of closing relative to the net asset value they reported as at 31 December 2018. -

Investment in Agricultural Mechanization in Africa

cover_I2130E.pdf 1 04/04/2011 17:45:11 AGRICULTURAL ISSN 1814-1137 AND FOOD ENGINEERING 8 AGRICULTURAL AND FOOD ENGINEERING TECHNICAL REPORT 8 TECHNICAL REPORT 8 Investment in agricultural mechanization in Africa Conclusions and recommendations of a Round Table Meeting of Experts Many African countries have economies strongly dominated by the agricultural sector and in some this generates a Investment in agricultural significant proportion of the gross domestic product. It provides employment for the majority of Africa’s people, but mechanization in Africa investment in the sector remains low. One of the keys to successful development in Asia and Latin America has been mechanization. By contrast, the use of tractors in sub-Saharan Investment in agricultural mechanization Africa Africa (SSA) has actually declined over the past fourty years Conclusions and recommendations and, compared with other world regions, their use in SSA of a Round Table Meeting of Experts today remains very limited. It is now clear that, unless some positive remedial action is taken, the situation can only worsen. In most African countries there will be more urban C dwellers than rural ones in the course of the next two to M three decades. It is critical to ensure food security for the Y entire population but feeding the increasing urban CM population cannot be assured by an agricultural system that MY is largely dominated by hand tool technology. CY In order to redress the situation, FAO, UNIDO and many CMY African experts are convinced that support is urgently needed K for renewed investment in mechanization. Furthermore, mechanization is inextricably linked with agro-industrialization, and there is a need to clarify the priorities in the context of a broader agro-industrial development strategy. -

Tanzania Financial Inclusion Products National Risk Assessment Report

The United Republic of Tanzania Ministry of Finance and Planning NATIONAL MONEY LAUNDERING AND TERRORIST FINANCING RISK ASSESSMENT FINANCIAL INCLUSION PRODUCTS RISK ASSESSMENT REPORT DECEMBER 2016 0 TABLE OF CONTENTS TABLE OF CONTENTS ...................................................................................................................................... I DECLARATION ................................................................................................................................................... II ACRONYMS ....................................................................................................................................................... III EXECUTIVE SUMMARY ................................................................................................................................... VI 1. INTRODUCTION ......................................................................................................................................... 1 1.1. BACKGROUND .............................................................................................................................................. 1 1.2. WHAT IS FINANCIAL INCLUSION? ................................................................................................................. 1 1.3. OBJECTIVES OF PRODUCTS RISK ASSESSMENT IN FINANCIAL INCLUSION ................................................ 2 1.4. TANZANIA FINANCIAL SECTOR LANDSCAPE ...............................................................................................