A Guide to Personal Banking

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Core Terms PRIVATE CLIENT

Core Terms PRIVATE CLIENT 234028395.indd 1 5/7/2021 4:44:30 PM Core Terms PRIVATE CLIENT Overview 1.4 If you do not have Sufficient Funds for a payment, ThesePrivate Client Core Terms form part of the we may treat a payment instruction as a request for Private Client Agreement between you (the client) an Unarranged Overdraft. and us (Coutts & Co). 1.5 If we allow the Unarranged Overdraft, you must: The following documents also form part of the Private Client Agreement: • repay the overdrawn amount on demand. • The Important Information booklet, which we • pay interest on the overdrawn amount at our have given you. Unarranged Borrowing Rate. • Our Private Client Banking Tariff (the Tariff) and 1.6 Our Unarranged Borrowing Rate, as detailed in the Interest Rates Notice, which we have given to you. Tariff, is set over the Coutts & Co Base Rate which • Each Application for an account, product or service. tracks the Bank of England Base Rate. We will • Any terms specific to an account, product or service. notify you of changes to the Coutts & Co Base Rate The Private Client Agreement Agreement( ) applies to by advertising the change after it comes into effect accounts, products and related services that we provide to you. in three national daily newspapers and on our If there is any conflict between any account, product or website coutts.com, or by telephone. We will also service specific terms and these Core Terms, the relevant display a notice of the change in our offices and account, product or service specific terms apply. -

Bank of Scotland Bank Account Switching to Us 1/4520768-6

Current Accounts Switching to us Switching your account The Current Account Switch Service makes switching your bank account easy. The Current Account Switch Guarantee means that we will: Take care of closing your old account for you. Transfer your balance from your old to your new account. Move any payments coming in, or going out of your old account to your new one. Switch to the new account on a date of your choice. Take ownership of your switch and getting this right. If you would like to switch a joint bank account, both customers need to allow us to do this. To find out more visit bankofscotland.co.uk/switch If your old account includes an overdraft you can switch this using the Current Account Switch Service. Speak to us before starting your switch, we will be able to advise if you’re eligible for an overdraft, depending on our lending criteria and your credit status. How the switch happens The switch begins. We request payment details from Days your old bank, once received your switch can start. Until 1-2 the switch date you can still use your existing account in the normal way. We set up your new account and move the payment Days arrangements across. For example direct debits and 3-5 your salary. We contact your old bank to transfer over your balance. Day If you have a debit balance on your old account you 6 need to make sure you have sufficient funds available on your new account to pay the balance off. Day Your switch is complete. -

SWEDEN Executive Summary

Underwritten by CASH AND TREASURY MANAGEMENT COUNTRY REPORT SWEDEN Executive Summary Banking The Swedish central bank is the Sveriges Riksbank. Bank and other credit institution supervision is performed by the Swedish Financial Supervisory Authority (Finansinspektionen — FI). The Riksbank has commissioned Statistics Sweden (SCB) to compile balance of payment statistics on its behalf since September 1, 2007. The SCB uses a survey-based system to collate balance of payments statistics. The SCB selects companies to complete forms to record their cross- border transactions. Cross-border current account transactions are recorded by the use of sample surveys. Financial account items are recorded by the use of both cut-off and sample surveys measuring, for example, direct investment level. Resident entities are permitted to hold fully convertible foreign currency bank accounts domestically and outside Sweden. Residents are also permitted to hold fully-convertible domestic currency (SEK) bank accounts outside Sweden. Non-resident entities are permitted to hold fully convertible domestic and foreign currency bank accounts within Sweden. Sweden has 89 registered banks. Of these, there are 40 limited liability banks, 47 savings banks and two co-operative banks. There is a significant foreign banking presence in Sweden – 38 foreign banks have a branch and 12 foreign banks have a representative office in Sweden. In addition, 538 foreign banks are authorized to offer cross-border banking services. Payments Sweden’s three main payment clearing systems are RIX, Bankgiro and Data Clearing. The most important cashless payment instruments in Sweden in terms of value are electronic credit transfers. In terms of volume, the use of cards, especially debit cards, has increased rapidly over recent years. -

Quilter International Ireland Banking Details

Quilter International Ireland banking details This document was last updated in September 2021. Please confirm with your financial adviser that this is the most up-to-date document for your product or servicing needs. Please enclose a copy of receipt of your electronic payment with the application or use Quilter International Ireland’s Bank Instruction Letter. Your financial adviser will be able to provide you with a Quilter International Ireland Bank Instruction Letter. Banking details Sterling payments From UK banks (CHAPS* payments) From non-UK banks (SWIFT** payments) Sort Code: 56-00-68 Swift code: NWBKGB2147K Bank: National Westminster Bank, Sort code: 56-00-68 High Street, Southampton Bank: National Westminster Bank, Beneficiary: Quilter International Ireland dac High Street, Southampton Account number: 37519611 Beneficiary: Quilter International Ireland dac IBAN code: GB59NWBK56006837519611 Other currency payments (swift payments) Payments should be made to Quilter International Ireland dac’s accounts held with National Westminster Bank, London. Swift code**: NWBKGB2LXXX Bank: National Westminster Bank, 2 1/2 Devonshire Square, London, EC2M 4XB Beneficiary: Quilter International Ireland dac IBAN***: (select as applicable, see below) 1. US dollar IBAN – GB36NWBK60730140501418 7. New Zealand dollar IBAN – GB26NWBK60730167576141 2. Euro IBAN – GB26NWBK60720240501469 8. Norwegian krone IBAN – GB18NWBK60730166004012 3. Australian dollar IBAN – GB24NWBK60730166004195 9. Singapore dollar IBAN – GB53NWBK60730167598838 4. Canadian dollar IBAN – GB80NWBK60730167521916 10. Swedish krona IBAN – GB48NWBK60730140501493 5. Danish krone IBAN – GB43NWBK60730166004047 11. Swiss franc IBAN – GB74NWBK60730166004071 6. Japanese yen IBAN – GB87NWBK60730166004128 12. Hong Kong dollar IBAN – GB21NWBK60730166004152 *** CHAPS is an electronic bank-to-bank same day value payment made in the UK in pound sterling (£). *** SWIFT is an acronym for Society for Worldwide Interbank Financial Telecommunications. -

SEPA Direct Debit Core Creditor

SEPA Direct Debit Core Creditor The SEPA Direct Debit (SDD) is the Pan European Direct Debit Contact HSBC scheme that has replaced domestic Euro Direct Debits (DD) HSBC understands the opportunities and challenges that your throughout the SEPA zone. It enables individuals and businesses business is facing with the advance of SEPA. This factsheet to pay or collect Euro DDs across the Single Euro Payments Area has been prepared for general guidance to business customers (SEPA), potentially from one bank account. It is based on an on our SEPA proposition. As ever, we would be very happy to agreement between the company collecting funds (Creditor) and answer any questions you may have or discuss any aspect in the consumer paying the direct debit (Debtor). This agreement greater depth. (SEPA mandate) is a standardised document and valid direct debit mandates obtained by the Creditor before migration to the Please contact your HSBC Representative or visit our website: SDD Core scheme will remain in force for SDD Core collections. www.hsbcnet.com/sepa for more information. About SEPA SEPA represents a major step towards a true single European 36 SEPA countries: market. An initiative of the European Commission (EC), SEPA Eurozone members of EU has replaced all domestic (legacy) Euro schemes throughout Austria Belgium Cyprus Europe. For businesses, SEPA creates a borderless system Estonia Finland France of payments that adds clarity, consistency and efficiency as transactions are subject to a uniform set of standards, rules Germany Greece Ireland and conditions and can circulate as easily, quickly, securely and efficiently as in national markets. -

ITALY Executive Summary

Underwritten by CASH AND TREASURY MANAGEMENT COUNTRY REPORT ITALY Executive Summary Banking The Italian central bank is the Banca d’Italia. As Italy is a participant in the eurozone, some central bank functions are shared with the other members of the European System of Central Banks (ESCB). Bank supervision is performed by the Banca d’Italia. Italy applies central bank reporting requirements. A representative sample of around 7,000 companies are required to submit periodic reports directly to the Banca d’Italia. These resident companies must report all transactions with non-residents. Resident entities are permitted to hold fully convertible foreign currency bank accounts domestically and outside Italy. Residents are also permitted to hold fully convertible domestic currency (EUR) bank accounts outside Italy. Non-resident entities are permitted to hold fully convertible domestic and foreign currency bank accounts within Italy. Italy has a large number of credit institutions (641), most of which are small, Italian-owned banks, such as the 359 mutual savings and 31 cooperative banks. There is a significant foreign banking presence in Italy, with 84 branches of foreign banks and 23 subsidiaries of foreign banks. Payments The two main payment systems used in Italy are the pan-European TARGET2 RTGS system and a multilateral net settlement system, BI-COMP. The most important cashless payment instruments in Italy are payment cards in terms of volume and credit transfers in terms of value. Card payments have increased steadily, especially in the retail sector. The increased use of electronic and internet banking has led to a growth in the use of electronic payments. -

TERMS & CONDITIONS for PERSONAL CUSTOMERS

TERMS & CONDITIONS for PERSONAL CUSTOMERS APPLICABLE FROM JUNE 2017 This pamphlet contains the general terms and conditions that apply to our personal bank accounts and some related services for personal customers. Please read this pamphlet carefully and keep a copy for future reference. 1 Introduction 1.1 The terms and conditions set out in this pamphlet are the general terms and conditions for our bank accounts and related services for personal customers. They apply, unless otherwise specified, to all Personal bank account relationships. 1.2 Your agreement with us for personal bank accounts and related banking services is made up of the general terms and conditions set out below, your Personal Account application form and any “additional terms and conditions” (together, “the Terms”) we give you for any specific accounts and services. 1.3 Additional terms and conditions are the specific terms and conditions that apply to a particular service, for example, our interest rates and charges, notice periods on savings accounts and any minimum or maximum balances that may apply. 1.4 If there is any conflict between these general terms and conditions and any additional terms and conditions, then the additional terms and conditions will prevail. 1.5 This agreement only covers banking services that we provide for your personal use. We have different agreements for banking services that are provided for business use. 1.6 Some useful definitions: “we, us, our” means Turkish Bank (UK) Limited. “you, your” means the account holder or if the account is in joint names, all account holders. “account” means the account(s) in your name operated by us and may include additional services we may provide to you from time to time. -

Fighting Ach Fraud: an Industry Perspective

FIGHTING ACH FRAUD: AN INDUSTRY PERSPECTIVE Volume 2 TABLE OF CONTENTS EXECUTIVE SUMMARY ...................................................................................................................................................... 3 THE ACH FRAUD PROCESS ............................................................................................................................................. 3 FINDING THE NEEDLE IN THE HAYSTACK................................................................................................................. 5 LEGAL LANDSCAPE ............................................................................................................................................................ 5 THE CUSTOMER’S ROLE AND RESPONSIBILITIES ................................................................................................. 6 2 Fighting ACH Fraud: An Industry Perspective EXECUTIVE SUMMARY A recent press release from the National Automated Clearing House Association (NACHA) announced that in 2012, ACH volume in the United States increased by 4.19% to 21 billion transactions. That corresponded to a staggering $36.9 trillion in funds transferred, which represents an 8.76% increase over the amount transferred in 2011. The increased adoption of ACH as a form of payment is not limited to the United States. Bacs, the United Kingdom‘s equivalent to NACHA1, reported an increase in direct debit activity (ACH debit) from 2011 to 2012 of 3.23%. Across Europe, the blue book also reports growth in both credit and -

EUC SDD Position Paper

PAYMENT SYSTEM END-USERS COMMITTEE (EUC) POSITION PAPER ON SEPA DIRECT DEBIT July 2009 Contents . About the EUC . Executive summary . Chapter One: Introduction . Chapter Two: Direct Debit in Europe . Chapter Three: Problem Areas . Chapter Four: Alternative solution . Conclusion . Annexes i. Annex 1: Requirements of CMF+ ii. Annex 2: Current direct debit schemes (list) iii. Annex 3 and 4: differences in existing DD schemes. iv. Annex 5: Extract from McKinsey Report . Tables 1 About the EUC The authors of this research paper represent the community of users of payment system instruments at the European level. In particular, they constitute the group of users who sit on the European Payments Council (EPC) stakeholder consultation forum. They will be referred to in this paper as the End Users Committee (EUC). A full list of the organizations represented by the authors is given below. In early 2009, the EUC considered that, despite a number of meetings with the EPC and individual meetings had by various members of the committee with the European Commission and the European Central Bank, there was still insufficient understanding and clarity on the part of these three bodies as to the needs and views of SEPA users on the proposed SEPA direct debit scheme. There was also insufficient understanding within the user community of the issues at stake. The EUC therefore proposed to research and compile an analysis of the major problems confronting the adoption of the Single Euro Payments Area (SEPA), with specific focus on SEPA direct debit (SDD). To this end, the EUC appointed three experts who have written this paper, with the full collaboration of all members of the EUC who have endorsed it as fully representing their views. -

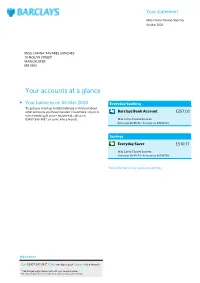

Your Accounts at a Glance

Your statement Miss Carina Tavares Sanches 06 Mar 2020 MISS CARINA TAVARES SANCHES 18 NOLAN STREET MANCHESTER M9 5UH Your accounts at a glance u Your balances on 06 Mar 2020 Everyday banking To get your most up to date balances or find out about other accounts you have that aren’t listed here, log on to Barclays Bank Account £257.02 online banking (if you’re registered), call us on 03457 345 345*, or come into a branch. Miss Carina Tavares Sanches Sort code 20-55-59 • Account no 23924319 Savings Everyday Saver £510.11 Miss Carina Tavares Sanches Sort code 20-55-59 • Account no 40785792 This is the end of your account summary. We’re here Call 03457 345 345* Click barclays.co.uk Come in to a branch *Call charges apply. Please check with your service provider. We may monitor or record calls for quality, security, and training. Statement date 06 Mar 2020 Barclays Bank Last statement 06 Feb 2020 Account 07 Feb - 06 Mar 2020 Miss Carina Tavares Sanches • Sort Code 20-55-59 • Account no. 23924319 • SWIFTBIC BUKBGB22 • IBAN GB75 BUKB 2055 5923 9243 19 MISS CARINA TAVARES SANCHES 18 NOLAN STREET At a glance MANCHESTER M9 5UH Start balance £24.92 Money in £3,256.20 Money out £3,024.10 End balance £257.02 Your arranged limits Your Barclays Bank Account statement Emergency Borrowing £0 Current account statement NOTICEBOARD u We've stopped charging fees for returned payments. Your deposit is eligible for protection by the Financial Good news – since 1 November 2019, we've stopped charging fees for returned payments on your Services Compensation Scheme. -

Transferring Funds

International Personal Bank Transferring Funds For Citi International Personal Bank clients who hold an Account with Citibank UK Limited. For maximum flexibility, money in a number of currencies can be sent CHAPS is a service which enables you to send and receive money on the from and received into your account in several ways. Citi International same day to bank accounts in the UK, Channel Islands, Isle of Man and Personal Bank will not levy any charges against money received Gibraltar. Sending money through CHAPS is fee-free and can be made into your account, however, please note that the Citi IPB Reference through your Relationship Manager. Exchange Rate will apply to transactions across currencies. How to receive money into your account A Citibank Global Transfer (“CGT”) allows you to send money instantly between your Citibank accounts in over 20 countries worldwide, To make sure money is received quickly and easily into your account, transaction fee-free. CGTs can also be made across currencies without you should provide the following information to the bank sending the charge when the currency of the destination account is the same. money. Limits may apply. CGTs can be carried out via Citi Online or your Relationship Manager. Intermediary Bank Name: Citibank N.A., London Branch Another way to send money from and receive money into your Citi Intermediary Bank SWIFT/BIC: CITIGB2L International Personal Bank account is through a service called SWIFT. The SWIFT method of sending and receiving money can be used in all of Beneficiary Bank: Citibank NA INT PERSONAL BANKING the currencies listed below and overleaf. -

An Overview of Ach

5500 Brooktree Road, Suite 104 Wexford, PA 15090 888-436-5101 www.profituity.com AN OVERVIEW OF ACH © COPYRIGHT 2013, PROFITUITY, LLC Page 2 of 11 Contents Automated Clearing House .................................................................................................................................... 3 The Role of NACHA ................................................................................................................................................... 3 Who Uses ACH ............................................................................................................................................................ 3 How ACH Works ......................................................................................................................................................... 4 Third-Party Service Provider ................................................................................................................................... 4 Various Types of ACH Transactions ..................................................................................................................... 4 Consumer and Non-consumer Checks .............................................................................................................. 6 Check 21......................................................................................................................................................................... 6 Drafts ..............................................................................................................................................................................