Telecom Decision CRTC 2021-181

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Saskatoon Budget Book.Book

City of Saskatoon 2015 APPROVED CORPORATE BUSINESS PLAN AND OPERATING AND CAPITAL BUDGETS Approved by City Council, DECEMBER 9, 2014 This document contains the details for the 2015 Approved Corporate Business Plan and Operating and Capital Budgets. This document is accompanied by the following companion documents: • 2015 Corporate Business Plan and Budget • 2015 Approved Capital Project Details Community Support ................................................................................................................................... 29 Animal Services ..................................................................................................................................................... 33 Community Development....................................................................................................................................... 34 Community Investments & Supports...................................................................................................................... 36 Cemeteries............................................................................................................................................................. 40 Corporate Asset Management................................................................................................................... 43 Facilities Management ........................................................................................................................................... 47 Fleet Services ....................................................................................................................................................... -

Eastlink) Distribution

BRAGG (Eastlink) Distribution #58 Ownership – Broadcasting - CRTC 2020-07-06 UPDATE CRTC 2013-95 – revocation of the licence issued to K-Right Communications Limited for the terrestrial broadcasting distribution undertaking serving Bedford, Sackville and surrounding area. Update - 2013-11-26 – minor updates as per 2013 BOIAF. CRTC 2016-287 – revocation of the licence issued to K-Right Communications Limited for the terrestrial broadcasting distribution undertaking serving Dartmouth and surrounding areas. Update – 2020-07-06 – minor change. NOTICE The CRTC ownership charts reflect the transactions approved by the Commission and are based on information supplied by licensees. The CRTC does not assume any responsibility for discrepancies between its charts and data from outside sources or for errors or omissions which they may contain. #58 Ownership – Broadcasting - CRTC 2020-07-06 APPENDIX Notes: The percentages in this chart refer to voting rights only. OWNERHSIP Bragg Communications Incorporated is 100% held by Oxford Communications Incorporated. Oxford Communications Incorporated is held as follows: • 79.96% by Tidnish Holdings Limited • 20.04% by The John Bragg Family Trust Tidnish Holdings Limited is held as follows: • 55.56% by John Louis Bragg • 11.11% by Aljaben Inc. which in turn is 90.91% held by John Louis Bragg • 11.11% by B.A.F.X. Holdings Limited which in turn is 90.91% held by John Louis Bragg • 11.11% by Colombier Holdings Limited which in turn is 90.91% held by John Louis Bragg • 11.11% by Mattbragg Holdings Limited which in turn is 90.91% held by John Louis Bragg Bragg Communications Incorporated holds: • 100% of K-Right Communications Limited • 100% of Eastlink Persona Holdings Inc. -

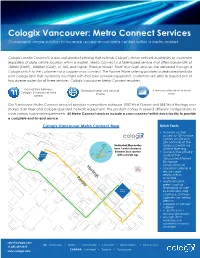

Cologix Vancouver: Metro Connect Services Convenient, Simple Solution to Increase Access Across Data Centres Within a Metro Market

Cologix Vancouver: Metro Connect Services Convenient, simple solution to increase access across data centres within a metro market Cologix’s Metro Connect is a low-cost product offering that extends Cologix’s dense network availability to customers regardless of data centre location within a market. Metro Connect is a fibre-based service that offers bandwidth of 100Mb (FastE), 1000Mb (GigE), or 10G and higher (Passive Wave). FastE and GigE services are delivered through a Cologix switch to the customer via a copper cross-connect. The Passive Wave offering provides a dedicated lambda over Cologix fibre that customers must light with their own network equipment. Customers are able to request one of two diverse routes for all three services. Cologix Vancouver Metro Connect enables: Connections between Extended carrier and network A low-cost alternative to local Cologix’s 2 Vancouver data choice loops centres Our Vancouver Metro Connect product provides connections between 1050 West Pender and 555 West Hastings over shared dark fiber and Cologix-operated network equipment. The product comes in several different confgurations to solve various customer requirements. All Metro Connect services include a cross-connect within each facility to provide a complete end-to-end service. Cologix Vancouver Metro Connect Map Quick Facts: • Network neutral access to 10+ unique carriers on-site plus 20+ networks at the Redundant bre routes ymor St. Harbour Centre via Se have 1 meter clearance diverse fibre ring 1 Meter between duct systems • Home to the primary -

Telecom Order CRTC 2010-917

Telecom Order CRTC 2010-917 PDF version Ottawa, 6 December 2010 TBayTel – Wireless Service Provider Enhanced 9-1-1 Network Access Service and 9-1-1 Public Emergency Reporting Service File numbers: Tariff Notices 151 and 151A Introduction 1. On 24 July 2009, TBayTel filed Tariff Notice 151, requesting approval for its revised General Tariff Section TB230, item 10, Wireless Service Provider Enhanced 9-1-1 Network Access Service (WSP E9-1-1 Service),1 and Section TB100, item 8, 9-1-1 Public Emergency Reporting Service (9-1-1 Public Service).2 TBayTel filed this application pursuant to certain requirements set out in Telecom Regulatory Policy 2009-40, in which the Commission mandated all incumbent local exchange carriers to file proposed revised WSP E9-1-1 Service tariffs associated with the implementation of Phase II Stage 1 of that service.3 The Commission approved the application, including TBayTel’s proposed monthly rate associated with the Phase I and Phase II Stage 1 elements of its WSP E9-1-1 Service and proposed rates associated with its 9-1-1 Public Service, on an interim basis in Telecom Order 2010-8, effective 1 February 2010. 2. On 4 February 2010, TBayTel filed Tariff Notice 151A to postpone the implementation date of its WSP E9-1-1 Service and 9-1-1 Public Service to 3 May 2010 due to technical and provisioning delays. The Commission approved that tariff notice on an interim basis in Telecom Order 2010-98, effective 3 May 2010. 3. The Commission received comments regarding TBayTel’s applications from Rogers Wireless Inc. -

BCE Inc. 2015 Annual Report

Leading the way in communications BCE INC. 2015 ANNUAL REPORT for 135 years BELL LEADERSHIP AND INNOVATION PAST, PRESENT AND FUTURE OUR GOAL For Bell to be recognized by customers as Canada’s leading communications company OUR STRATEGIC IMPERATIVES Invest in broadband networks and services 11 Accelerate wireless 12 Leverage wireline momentum 14 Expand media leadership 16 Improve customer service 18 Achieve a competitive cost structure 20 Bell is leading Canada’s broadband communications revolution, investing more than any other communications company in the fibre networks that carry advanced services, in the products and content that make the most of the power of those networks, and in the customer service that makes all of it accessible. Through the rigorous execution of our 6 Strategic Imperatives, we gained further ground in the marketplace and delivered financial results that enable us to continue to invest in growth services that now account for 81% of revenue. Financial and operational highlights 4 Letters to shareholders 6 Strategic imperatives 11 Community investment 22 Bell archives 24 Management’s discussion and analysis (MD&A) 28 Reports on internal control 112 Consolidated financial statements 116 Notes to consolidated financial statements 120 2 We have re-energized one of Canada’s most respected brands, transforming Bell into a competitive force in every communications segment. Achieving all our financial targets for 2015, we strengthened our financial position and continued to create value for shareholders. DELIVERING INCREASED -

Matters Related to the Reliability and Resiliency of the 9-1-1 Networks

Telecom Regulatory Policy CRTC 2016-165 PDF version Reference: Telecom Notice of Consultation 2015-305 Ottawa, 2 May 2016 File number: 8665-C12-201507008 Matters related to the reliability and resiliency of the 9-1-1 networks Canadians rely on the continuous operation of 9-1-1 services to seek help during an emergency. Given the importance of 9-1-1 services to the health and safety of Canadians, the Commission conducted a public proceeding to examine a number of relevant issues. Overall, the 9-1-1 networks in Canada are reliable and resilient. As a result, very few 9-1-1 service outages that impact the delivery of 9-1-1 voice calls have occurred over the last five years. Therefore, the Commission will not establish prescriptive regulatory measures but, instead, directs 9-1-1 network providers to take all reasonable measures to ensure that their 9-1-1 networks are reliable and resilient to the maximum extent feasible, and establishes certain notification and reporting requirements. Regarding concerns raised about MTS Inc.’s (MTS) 9-1-1 service backup solution, the Commission directs MTS and interconnecting telephone service providers in Manitoba to work together to establish interconnection arrangements with MTS’s backup solution. Background 1. Effective access to emergency services is critical to the health and safety of citizens, and is an important part of the Commission’s role in ensuring that Canadians have access to a world-class communication system.1 Canadians have come to rely on the continuous operation of 9-1-1 services to seek help during an emergency. -

Many Wireless Customers in Canada Underwhelmed by Network Reliability and Speed, J.D

Many Wireless Customers in Canada Underwhelmed by Network Reliability and Speed, J.D. Power Finds Bell Mobility and TELUS Mobility Rank Highest in Ontario; Videotron Ranks Highest in Eastern Region; TELUS Mobility Ranks Highest in Western Region TORONTO: 22 April 2021 – Although the overall performance of Canada’s wireless networks remains flat year over year with an average of 9 PP100 (problems per 100 connections), a significant portion of customers say performance was not up to par, according to the J.D. Power 2021 Canada Wireless Network Quality Study,SM released today. Only 67% of wireless customers agree that their carrier’s network is reliable when streaming music and videos, activities that account for a significant amount of time used on devices. In addition, just 7% of customers say network speeds are faster than expected. “Despite massive investments in infrastructure and technology, customers remain relatively unimpressed by their carriers’ wireless networks,” said Adrian Chung, director of the technology, media & telecom practice at J.D. Power Canada. “Customers perceive the quality and performance of the wireless networks mainly as fair and meeting expectations. More specifically, network strength is associated with traditional functionality like calling and texting rather than browsing and streaming, presenting a clear reliability gap that carriers need to bridge.” This reliability gap should serve as a red flag for carriers, especially because browsing and streaming account for nearly half (49%) of the time that customers say they spend on their mobile phones. Following are additional key findings of the 2021 study: • Data hungry: The past year has seen an increased need to stay connected and more customers in Canada are beefing up their wireless plans. -

ONN 6 Eng Codelist Only Webversion.Indd

6-DEVICE UNIVERSAL REMOTE Model: 100020904 CODELIST Need help? We’re here for you every day 7 a.m. – 9 p.m. CST. Give us a call at 1-888-516-2630 Please visit the website “www.onn-support.com” to get more information. 1 TABLE OF CONTENTS CODELIST TV 3 STREAM 5 STB 5 AUDIO SOUNDBAR 21 BLURAY DVD 22 2 CODELIST TV TV EQD 2014, 2087, 2277 EQD Auria 2014, 2087, 2277 Acer 4143 ESA 1595, 1963 Admiral 3879 eTec 2397 Affinity 3717, 3870, 3577, Exorvision 3953 3716 Favi 3382 Aiwa 1362 Fisher 1362 Akai 1675 Fluid 2964 Akura 1687 Fujimaro 1687 AOC 3720, 2691, 1365, Funai 1595, 1864, 1394, 2014, 2087 1963 Apex Digital 2397, 4347, 4350 Furrion 3332, 4093 Ario 2397 Gateway 1755, 1756 Asus 3340 GE 1447 Asustek 3340 General Electric 1447 Atvio 3638, 3636, 3879 GFM 1886, 1963, 1864 Atyme 2746 GPX 3980, 3977 Audiosonic 1675 Haier 2309, 1749, 1748, Audiovox 1564, 1276, 1769, 3382, 1753, 3429, 2121 2293, 4398, 2214 Auria 4748, 2087, 2014, Hannspree 1348, 2786 2277 Hisense 3519, 4740, 4618, Avera 2397, 2049 2183, 5185, 1660, Avol 2735, 4367, 3382, 3382, 4398 3118, 1709 Hitachi 1643, 4398, 5102, Axen 1709 4455, 3382, 0679 Axess 3593 Hiteker 3118 BenQ 1756 HKPro 3879, 2434 Blu:sens 2735 Hyundai 4618 Bolva 2397 iLo 1463, 1394 Broksonic 1892 Insignia 2049, 1780, 4487, Calypso 4748 3227, 1564, 1641, Champion 1362 2184, 1892, 1423, Changhong 4629 1660, 1963, 1463 Coby 3627 iSymphony 3382, 3429, 3118, Commercial Solutions 1447 3094 Conia 1687 JVC 1774, 1601, 3393, Contex 4053, 4280 2321, 2271, 4107, Craig 3423 4398, 5182, 4105, Crosley 3115 4053, 1670, 1892, Curtis -

2001 Annual Report

Part of your life. COMMITTED TO THE PEOPLE OF SASKATCHEWAN > 2001 ANNUAL REPORT View this annual report online at www.sasktel.com/about_sasktel/financial_reports/2001_annualreport/ For more information about SaskTel, our initiatives and operations, or to obtain additional copies of the 2001 SaskTel Annual Report, please contact SaskTel Corporate Affairs at 1-877-337-2445 or visit our website at www.sasktel.com. www.sasktel.com > LETTER OF TRANSMITTAL Regina, Saskatchewan March 31, 2002 To Her Honour The Honourable Lynda Haverstock Lieutenant Governor of the Province of Saskatchewan Dear Lieutenant Governor: I have the honour to submit herewith the annual report of SaskTel for the year ending December 31, 2001, including the financial statements, duly certified by auditors for the corporation, and in the form approved by the Treasury Board, all in accordance with The Saskatchewan Telecommunications > CONTENTS Holding Corporation Act. Financial Highlights . .01 Respectfully submitted, Letter from the President . .02 Year in Review . .04 Honourable Maynard Sonntag Minister Responsible for Crown Investments Corporation (CIC) E-Business . .09 SaskTel International . .12 Corporate Social Responsibility . .14 Management’s Discussion and Analysis . .17 Five Year Record of Service . .35 Consolidated Financial Statements . .37 Board of Directors . .50 Corporate Directory . .51 Corporate Governance . .52 > FINANCIAL HIGHLIGHTS Net Income Operating Revenues Cumulative percentage SaskTel has lowered average Operating Expenses ($ millions) ($ millions) per minute long distance charges since 1990 ($ millions) 125 1000 0% 1000 100 750 20% 750 75 40% 500 500 50 60% 250 250 25 80% 0 0 100% 0 1997 1998 1999 2000 2001 1997 1998 1999 2000 2001 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 1997 1998 1999 2000 2001 • NET INCOME was $101.5 million in 2001 and • INCREASED FOCUS on growth and diversification • During the year, SaskTel ACQUIRED RSL COM cash from operating activities was $268.8 million. -

3-Device Universal Remote NS-RMT3D18

USER GUIDE 3-Device Universal Remote NS-RMT3D18 Before using your new product, please read these instructions to prevent any damage. PACKAGE CONTENTS • 3-Device Universal Remote • Quick Setup Guide FEATURES • Works with a TV and a cable, satellite, or streaming box, plus a Blu-ray or DVD player and a soundbar or other audio-only device • Programming by popular brand names for quick and easy setup • Extensive code library for less common brands and devices • Premium design, materials, and construction for rugged use INSTALLING BATTERIES • Insert two AAA batteries (not included) into the remote. Make sure that the + and – symbols match the + and – symbols in the battery compartment. Note: To set up your remote, follow the setup steps below, in order, and STOP as soon as your remote works correctly. PROGRAMMING YOUR REMOTE There are three ways to set up your remote: • Use “Setup method A: Popular brands” for pre-set popular brands. • Use “Setup method B: Direct code entry” if your device’s direct code is in the code list starting on page 13. • Use “Setup method C: Code search” to perform a code search for your device. Note: This remote comes pre-set for Insignia TVs and DVDs and Apple TV cable/satellite/streaming set-top boxes. Setup method A: Popular brands 1 Turn on your target device. 2 Press and hold SETUP until your remote’s LED blinks twice. 3 Press TELEVISION or CABLE / SATELLITE / STREAMING, or BLURAY/ DVD to select the mode you want to set up. The LED stays lit. 4 Press either 0 (for cable/satellite/ streaming), 1 (for TVs), or 2 (for Blu-ray/DVD) to select the device type you want to set up. -

Eastlink Tivo Mobile App Terms of Service

EASTLINK TIVO MOBILE APP TERMS OF SERVICE IMPORTANT - PLEASE READ THE FOLLOWING TERMS AND CONDITIONS (“TERMS”) CAREFULLY BEFORE PROCEEDING WITH THE DOWNLOADING, INSTALLATION AND/OR USE OF THE EASTLINK TIVO MOBILE APP. THIS DOCUMENT IS A LEGAL AGREEMENT BETWEEN YOU AND BRAGG COMMUNICATIONS INC. (“EASTLINK”) AND CONTAINS VERY IMPORTANT INFORMATION ABOUT YOUR RIGHTS AND OBLIGATIONS, AS WELL AS LIMITATIONS AND EXCLUSIONS THAT MAY APPLY TO YOU (INCLUDING PROVISIONS THAT LIMIT OUR LIABILITY AND SET NOVA SCOTIA AS THE JURISDICTION FOR DISPUTES). 1. Introduction The Eastlink TiVo mobile app (the “Software”) is an application provided by Eastlink and its affiliates (collectively, “us”, “we”, “our” or "Eastlink") that allows Eastlink TV customers who subscribe to our TiVo DVR service to view the live feed of the television channels to which they subscribe, and to view, schedule and manage their DVR recordings (collectively, the “Content”) via a tablet or mobile device (“Digital Device”). Please note that changes to your TV channel subscriptions may not be reflected until the next day. No other services or software, and no maintenance, technical support or other services are provided to you under these Terms. By installing and using the Software you are acknowledging that you have read, understood and agree to be bound by these Terms and such other additional or alternative terms, conditions, rules and policies that are displayed or to which you may be directed by Eastlink in connection with the Software, as all of the same may be modified by Eastlink from time to time, all to the extent permitted by applicable law. If you do not agree to comply with these Terms, then you may not use the Software. -

TELUS Communications Company – Application for Forbearance from the Regulation of Business Local Exchange Services

Telecom Decision CRTC 2017-134 PDF version Ottawa, 5 May 2017 File number: 8640-T66-201612268 TELUS Communications Company – Application for forbearance from the regulation of business local exchange services The Commission approves TCC’s request for forbearance from the regulation of business local exchange services in 79 exchanges in Alberta, British Columbia, and Quebec. The Commission denies TCC’s request for forbearance from the regulation of business local exchange services in 1 exchange in British Columbia and 16 exchanges in Quebec. Introduction 1. The Commission received an application from TELUS Communications Company (TCC), dated 30 November 2016, in which the company requested forbearance from the regulation of business local exchange services1 in 96 exchanges in Alberta, British Columbia, and Quebec. A list of these exchanges is set out in Appendix 1 to this decision. 2. The Commission received submissions regarding TCC’s application from Bell Canada; Bragg Communications Incorporated, operating as Eastlink (Eastlink); Câble-Axion Digitel inc.; CityWest Cable & Telephone Corp. (CityWest); Cogeco Communications Inc. (Cogeco); CoopTel; DERYtelecom inc.; Distributel Communications Limited; Groupe Maskatel LP; Iristel Inc. (Iristel); Shaw Telecom G.P. (Shaw); and Quebecor Media Inc., on behalf of Videotron G.P. (Videotron). The public record of this proceeding, which closed on 6 March 2017, is available on the Commission’s website at www.crtc.gc.ca or by using the file number provided above. Commission’s analysis and determinations 3. Pursuant to the Commission’s requirements in Telecom Decision 2006-15, TCC provided evidence to support its forbearance request, including competitor quality of service (Q of S) results for the period of April to September 2016.