Staying Focused on Recovery

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG

Simplified Prospectus • October 2011 ® the SLI® as at August 15, 2011 were as follows: Nestlé SA, Roche CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG. The composition of the index is Subfund of the Umbrella Fund of the Category periodically updated by SIX Swiss Exchange. “Other Funds for Traditional Investments” Risk Profile of the Subfund Simplified Prospectus The value of the Subfund’s investments is governed by the market value of investments at any given time. Depending on the prevailing stock October 2011 market trend and the performance of the stocks held in the portfolio, the net asset value can fluctuate considerably. The possibility of a depreciation Distribution in Switzerland and Liechtenstein in value over longer periods cannot be ruled out. There is no guarantee that the investors will receive a certain return and that they will be able to return their units to the fund management company for redemption at a certain price. When redeeming units, it is possible that an investor will not Note recoup the amount originally invested in the Subfund. This simplified prospectus contains a summary of the key information on CS ETF (CH) on SLI®1 (the “Subfund”). The legal and financial aspects Performance of the Subfund (in %) are governed conclusively by the full sales prospectus with integrated fund (change in the net asset value where distributions are reinvested) contract. These govern, among other things, the rights of the investors, the duties and obligations of the fund management company and the 40.0% custodian bank, and the investment policy of the Fund. -

Nextgen WEALTH MANAGERS 30.06.2020

ESG Swiss Equities Certificate NextGen WEALTH MANAGERS 30.06.2020 Objective & Strategy ESG Swiss Equities certificate invests in a financial and ESG criteria scored weighted index. The index tracks Swiss financially sound companies that generate investment performance and integrate corporate social responsability, ethics and sustainability characteristics in order to have a long term positive environmental, social, governance (ESG) impact. It aims to be a reference by providing a specific solution that allows capital markets to redirect investment flows toward a more sustainable economy. Only companies with a financial and ESG score equal or above the median are eligible for inclusion in the ESG Swiss Equities Index. The dynamic strategy is based upon a synthetic notional investment allocation and reallocation in the Index Components following a specific and monitored process of eligibility defined by NextGen Wealth Managers SA. Monthly Comment Classification In June, the ESG Swiss Equities certificate registered a performance of 2.78% compared to Asset Type Equities May's 2.78%. The certificate’s benchmark, the Swiss Performance Index (SPI), performed Region Switzerland positively at 1.55% against 2.86% in the previous month. Since the beginning of the year, the Style ESG Systematic two baskets stand at -8.11% for the certificate and -3.13% for the benchmark. Since inception, cumulated performances are respectively at 12.34% and 34.73% (representing annualized performances of 2.72% and 7.12%) for annualized volatilities of 13.07% and 9.59%. The portfolio's allocation in large capitalization companies remains around 36% against 9% in middle capitalization companies and 54% in small capitalization companies. -

Ishares SMI®

For Professional Clients Only. iShares SMI® ETF (CH) CSSMI August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug- 2021 All other data as at 07-Sep-2021 Investors should read the Key Investor Information Document and Prospectus prior to investing. Capital at risk. All financial investments involve an element of risk. Therefore, the value The Fund seeks to track the performance of an index composed of the 20 largest Swiss companies. of your investment and the income from it will vary and your initial investment amount cannot Effective from 18 September 2017, the maximum weighting to any one stock is restricted to 18% on be guaranteed. a quarterly basis KEY FACTS Asset Class Equity KEY BENEFITS Fund Base Currency CHF Share Class Currency CHF Targeted exposure to the 20 largest Swiss companies 1 Fund Launch Date 06-Oct-1999 Direct investment into blue-chip companies representative of leaders in Switzerland Share Class Launch Date 06-Oct-1999 2 Benchmark Swiss Market Index (SMI®) 3 Single country and large market capitalisation companies exposure ISIN CH0008899764 Total Expense Ratio 0.35% Distribution Type Ad-Hoc Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Domicile Switzerland This means the Fund is more sensitive to any localised economic, market, political or regulatory Methodology Replicated events. The value of equities and equity-related securities can be affected by daily stock market Product Structure Physical movements. Other influential factors include political, economic news, company earnings and Rebalance Frequency Quarterly significant corporate events. Counterparty Risk: The insolvency of any institutions providing UCITS No services such as safekeeping of assets or acting as counterparty to derivatives or other Use of Income Distributing instruments, may expose the Fund to financial loss. -

Julius Baer Multistock

JULIUS BAER MULTISTOCK A SICAV UNDER LUXEMBOURG LAW PROSPECTUS 31 DECEMBER 2011 Subscriptions are validly made only on the basis of this Prospectus or the Key Investor Information Document in conjunction with the most recent annual report and the most recent semi-annual report where this is published after the annual report. No information other than that contained in this Prospectus or the Key Investor Information Document may be given. PROSPECTUS - 2 - JULIUS BAER MULTISTOCK TABLE OF CONTENTS 1. Introduction..................................................................................................................................................5 2. Organisation and management...................................................................................................................8 3. Investment objectives and policy..................................................................................................................10 4. Investor profile...........................................................................................................................................34 5. Investment limits........................................................................................................................................35 6. Special investment techniques and financial instruments ........................................................................41 6.1 Options on securities.................................................................................................................................... -

Swiss Leader Index Price Index Index

BLUE-CHIP INDICES 1 SWISS LEADER INDEX PRICE INDEX INDEX Index description Key facts The SLI Swiss Leader Index includes the 30 most liquid stocks traded in the » "In order to achieve the stated index objective SIX Swiss Ex-change defines Swiss equity market, the developments of which are reflected by the SPI® the general principles that govern the index methodology. SIX Swiss Family. Consequently, the index weighting of a given issue is limited by Exchange publishes the index objective and rules for all indices. means of a 9/4,5 capping model. In other words, the weighting of each of the four companies with the largest market capitalisation is capped at a » Representative: the development of the market is represented by the maximum of 9 %. The weightings of all lower-ranked companies are if index necessary capped at 4.5 %. This limitation will be calculated by applying a » Tradable: the index components are tradable in terms of company size capping factor, which as a general rule will remain constant for a three- and market month period. The SLI offers a number of advantages: for investors, the capping feature improves their stock- and sector specific diversification and, » Replicable: the development of the index can be replicated in practise with because the new index fulfils Swiss, EU and US regulatory requirements, a portfolio new markets can be opened with products based on the SLI. That, in turn, generates liquidity for the stocks included in the basket. » Stable: high index continuity » Rules-based: index changes and calculations -

Appendix D to Tradition SEF Rulebook Equities Product Listing

Appendix D to Tradition SEF Rulebook Equities Product Listing Broad-Market Equity Index Swap Product Listing Tradition SEF, Inc. I. Discussion of contracts; not readily susceptible to manipulation • Index Selection: Tradition SEF limits the indexes underlying its equity index swap offerings to well-established, publicly available third-party equity index market benchmarks. Tradition SEF believes that the size and liquidity of the cash market that underlies these indexes creates in each case a deliverable supply of underlying securities and volume of trading that would not make them easily susceptible to manipulation. Furthermore, Tradition SEF believes that the large number of participants in each market, and the calculation of each index being based on actual transaction data from major stock markets further limit the susceptibility of manipulation of these indexes. The broad-based equity indexes underlying swaps on Tradition SEF are the timeliest, recognized and reliable benchmarks for equity prices in their respective markets. The index levels are readily available and commercially acceptable as benchmarks for investors, portfolio managers and public policy makers. Tradition SEF believes that such benchmark indexes, which also underlie liquid index futures contracts on major Designated Contract Markets, and equity index exchange traded funds on stock exchanges, due to the large number of index members, ubiquity, and broad-market nature are not readily susceptible to manipulation. Furthermore, the associated index futures contracts and exchange traded funds offer a deep liquidity pool to hedge and risk-manage swaps based on such indexes’ index. Swap Contract Specifications: A discussion of Variance and Volatility Swaps: Equity Index Variance and volatility swaps pay out on the degree of stock price fluctuation, not the absolute level or direction of the underlying index. -

Rising Yields Benefit Rotation Trade

Global CIO Office Rising yields benefit rotation trade Investment Monthly | Japan edition / Credit Suisse Securities (Japan) Ltd. | March 2021 Japan investment strategy Japan asset allocation Global investment strategy Reduce risk for a stable investment Neutral on global equities Paring back some risk portfolio page 3 page 5 page 9 Important Information This report represents the views of the Investment Strategy Department of CS and has not been prepared in accordance with the legal requirements designed to promote the independence of investment research. It is not a product of the Credit Suisse Research Department even if it contains published research recommendations. CS has policies in place to manage conflicts of interest including policies relating to dealing ahead of the dis- semination of investment research. These policies do not apply to the views of Investment Strategists contained in this report. Please find further important information at the end of this material. Singapore: For accredited investors only. Hong Kong: For professional investors only. Australia: For wholesale clients only. Editorial In this issue Japan investment strategy 3 Reduce risk for a stable investment portfolio Japan asset allocation 5 Neutral on global equities Michael Strobaek Burkhard Varnholt Investment solutions 7 Global Chief Investment Officer Chief Investment Officer – Swiss Univer- Japan investment theme 2021: Pushing for a sal Bank carbon-free society In recent weeks, bond yields have stolen the limelight. In the Economics 8 USA, rapid progress with vaccinations and substantial addi- Much improved US outlook has driven global yields up tional fiscal stimulus led to a sharply improved growth outlook, lifting government bond yields there as well as globally. -

For Additional Information

April 2015 Attached please find the updated Foreign Listed Stock Index Futures and Options Approvals Chart, current as of April 2015. All prior versions are superseded and should be discarded. Please note the following developments since we last distributed the Approvals Chart: (1) The CFTC has approved the following contracts for trading by U.S. Persons: (i) Singapore Exchange Derivatives Trading Limited’s futures contract based on the MSCI Malaysia Index; (ii) Osaka Exchange’s futures contract based on the JPX-Nikkei Index 400; (iii) ICE Futures Europe’s futures contract based on the MSCI World Index; (iv) Eurex’s futures contracts based on the Euro STOXX 50 Variance Index, MSCI Frontier Index and TA-25 Index; (v) Mexican Derivatives Exchange’s mini futures contract based on the IPC Index; (vi) Australian Securities Exchange’s futures contract based on the S&P/ASX VIX Index; and (vii) Moscow Exchange’s futures contract based on the MICEX Index. (2) The SEC has not approved any new foreign equity index options since we last distributed the Approvals Chart. However, the London Stock Exchange has claimed relief under the LIFFE A&M and Class Relief SEC No-Action Letter (Jul. 1, 2013) to offer Eligible Options to Eligible U.S. Institutions. See note 16. For Additional Information The information on the attached Approvals Chart is subject to change at any time. If you have questions or would like confirmation of the status of a specific contract, please contact: James D. Van De Graaff +1.312.902.5227 [email protected] Kenneth M. -

We Love What We Do 2014 Annual Report 2014 Annual Report Annual 2014

We love what we do 2014 Annual Report 2014 Annual Report Annual 2014 Straumann Holding AG Peter Merian-Weg 12 4002 Basel Switzerland www.straumann.com 00_00_STR_GB2014_GB_Umschlag_en.indd 1 09.03.2015 16:44:50 About Straumann Straumann is a global leader in tooth replacement solu- tions including dental implants, prosthetics and regener- ative products. Headquartered in Basel, Switzerland, the Group is present in more than 70 countries through its broad network of distribution subsidiaries and partners. 1 Rebecca Hesse SAP Coordinator 2 Susan-Ann Welzbacher Corporate Safety Officer 3 Julia Hirtle Spend Coordinator 4 Roland Scacchi Administrator 5 Alessandro Annicchiarico IT Support 4 7 1 2 3 5 6 8 9 6 Heather Stanton Web Editor IMPRINT Published by: Institut Straumann AG, Basel 7 Dave Koster Lab Business Development Concept and realization: PETRANIX Corporate and Financial Communications AG, Adliswil/Zurich 8 Raul Perez Talent Management Photography: AMX Studio, Alex Stiebritz, Karlsruhe Consultant on sustainability: sustainserv, Zurich and Boston 9 Sandra Schürmann Events Coordinator Certain design elements by Eclat, Erlenbach/Zurich Print: Neidhart + Schön AG, Zurich Basel, 26 February 2015 We have a global culture with more than 28 nationalities represented at our headquarters alone. The front cover shows a few examples. ©2015, Straumann Holding AG 00_00_STR_GB2014_GB_Umschlag_en.indd 2 09.03.2015 16:45:02 We love what we do 2014 Annual Report Highly motivated, creative employees, together with innovative products, solutions and commercial ap- proach es are the keys to Straumann’s ambition of being the provider of choice in tooth replacement. The theme photographs in this report all feature products that we introduced or rolled out in 2014 alongside some of the talented people who have been involved in bringing them to customers and patients. -

Thomson One Symbols

THOMSON ONE SYMBOLS QUICK REFERENCE CARD QUOTES FOR LISTED SECURITIES TO GET A QUOTE FOR TYPE EXAMPLE Specific Exchange Hyphen followed by exchange qualifier after the symbol IBM-N (N=NYSE) Warrant ' after the symbol IBM' When Issued 'RA after the symbol IBM'RA Class 'letter representing class IBM'A Preferred .letter representing class IBM.B Currency Rates symbol=-FX GBP=-FX QUOTES FOR ETF TO GET A QUOTE FOR TYPE Net Asset Value .NV after the ticker Indicative Value .IV after the ticker Estimated Cash Amount Per Creation Unit .EU after the ticker Shares Outstanding Value .SO after the ticker Total Cash Amount Per Creation Unit .TC after the ticker To get Net Asset Value for CEF, type XsymbolX. QRG-383 Date of issue: 15 December 2015 © 2015 Thomson Reuters. All rights reserved. Thomson Reuters disclaims any and all liability arising from the use of this document and does not guarantee that any information contained herein is accurate or complete. This document contains information proprietary to Thomson Reuters and may not be reproduced, transmitted, or distributed in whole or part without the express written permission of Thomson Reuters. THOMSON ONE SYMBOLS Quick Reference Card MAJOR INDEXES US INDEXES THE AMERICAS INDEX SYMBOL Dow Jones Industrial Average .DJIA Airline Index XAL Dow Jones Composite .COMP AMEX Computer Tech. Index XCI MSCI ACWI 892400STRD-MS AMEX Institutional Index XII MSCI World 990100STRD-MS AMEX Internet Index IIX MSCI EAFE 990300STRD-MS AMEX Oil Index XOI MSCI Emerging Markets 891800STRD-MS AMEX Pharmaceutical Index -

Swiss Performance Index SPI® Price

Swiss Performance Index SPI® Price Index Description The Swiss Performance Index SPI® Price measures the development of the more liquid and therefore tradable equity instruments listed on SIX. It usually serves as a benchmark for the overall Swiss equity market. The index has a variable number of components - currently 218, which are weighted by their freefloat market capitalisation. The index is standardised at 100 points on June 01, 1987. As of today the index covers roughly 99% of the Swiss Equity Market. Its benchmark the Swiss All Shares Index covers by definition 100% of that market. Index Performance Annual Index Return¹ 300 Year SPI All Share 270 2021 25.98% 26.13% 240 2020 0.61% 0.66% 210 2019 26.51% 26.51% 180 150 2018 -11.43% -11.34% 120 2017 16.37% 16.28% 90 2016 -4.67% -5.02% 60 2015 -0.25% -0.13% 30 2014 9.73% 9.80% 0 1998 2001 2004 2007 2010 2013 2016 2019 Swiss Performance Index SPI® Price Swiss All Share Index Price Risk and Return Profile Dividend Yield & Turnover YTD 3 Mths 1 Yr¹ 3 Yrs¹ 7 Yrs¹ 15 Yrs¹ SPI All Share Return Div. Yield SPI 16.65% 8.68% 22.59% 10.78% 6.01% 3.23% 2021 2.58% 2.58% All Share 16.74% 8.75% 22.65% 10.84% 6.00% 3.22% 2020 3.19% 3.19% Volatility 2019 3.10% 3.10% SPI 0.61% 0.50% 0.72% 0.58% 0.36% 0.28% 2018 3.20% 3.21% All Share 0.61% 0.50% 0.72% 0.58% 0.36% 0.28% 2017 3.09% 3.10% Tracking Err. -

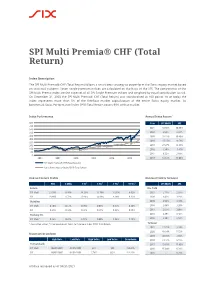

SPI Multi Premia® CHF (Total Return)

SPI Multi Premia® CHF (Total Return) Index Description The SPI Multi Premia® CHF (Total Return) follows a smart beta strategy to outperform the Swiss equity market based on statistical patterns. Seven single-premium indices are calculated on the basis of the SPI. The components of the SPI Multi Premia index are the superset of all SPI Single Premium indices and weighted by equal contribution to risk. On December 31, 2003 the SPI Multi Premia® CHF (Total Return) was standardised at 100 points. As of today the index represents more than 5% of the freefloat market capitalization of the entire Swiss equity market. Its benchmark Swiss Performance Index SPI® Total Return covers 99% of that market. Index Performance Annual Index Return¹ 800 Year SPI Multi SPI 720 2021 33.93% 30.89% 640 560 2020 4.98% 3.82% 480 2019 28.25% 30.40% 400 2018 -15.55% -8.59% 320 240 2017 27.27% 19.98% 160 2016 7.54% -1.41% 80 2015 8.32% 2.68% 0 2004 2007 2010 2013 2016 2019 2014 12.12% 13.00% SPI Multi Premia® CHF (Total Return) Swiss Performance Index SPI® Total Return Risk and Return Profile Dividend Yield & Turnover YTD 3 Mths 1 Yr¹ 3 Yrs¹ 7 Yrs¹ 15 Yrs¹ SPI Multi SPI Return Div. Yield SPI Multi 21.50% 6.16% 34.28% 11.76% 11.05% 9.02% 2021 2.15% 2.58% SPI 19.66% 8.72% 25.98% 14.08% 9.28% 6.32% 2020 3.42% 3.19% Volatility 2019 2.96% 3.10% SPI Multi 0.70% 0.57% 0.76% 0.63% 0.37% 0.26% 2018 2.68% 3.20% SPI 0.61% 0.50% 0.72% 0.58% 0.36% 0.28% 2017 2.67% 3.09% Tracking Err.