View of Where We Are As Developing the Metro Rail Full-Service Telephony

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Deity's Beer List.Xls

Page 1 The Deity's Beer List.xls 1 #9 Not Quite Pale Ale Magic Hat Brewing Co Burlington, VT 2 1837 Unibroue Chambly,QC 7% 3 10th Anniversary Ale Granville Island Brewing Co. Vancouver,BC 5.5% 4 1664 de Kronenbourg Kronenbourg Brasseries Stasbourg,France 6% 5 16th Avenue Pilsner Big River Grille & Brewing Works Nashville, TN 6 1889 Lager Walkerville Brewing Co Windsor 5% 7 1892 Traditional Ale Quidi Vidi Brewing St. John,NF 5% 8 3 Monts St.Syvestre Cappel,France 8% 9 3 Peat Wheat Beer Hops Brewery Scottsdale, AZ 10 32 Inning Ale Uno Pizzeria Chicago 11 3C Extreme Double IPA Nodding Head Brewery Philadelphia, Pa. 12 46'er IPA Lake Placid Pub & Brewery Plattsburg , NY 13 55 Lager Beer Northern Breweries Ltd Sault Ste.Marie,ON 5% 14 60 Minute IPA Dogfishhead Brewing Lewes, DE 15 700 Level Beer Nodding Head Brewery Philadelphia, Pa. 16 8.6 Speciaal Bier BierBrouwerij Lieshout Statiegeld, Holland 8.6% 17 80 Shilling Ale Caledonian Brewing Edinburgh, Scotland 18 90 Minute IPA Dogfishhead Brewing Lewes, DE 19 Abbaye de Bonne-Esperance Brasserie Lefebvre SA Quenast,Belgium 8.3% 20 Abbaye de Leffe S.A. Interbrew Brussels, Belgium 6.5% 21 Abbaye de Leffe Blonde S.A. Interbrew Brussels, Belgium 6.6% 22 AbBIBCbKE Lvivske Premium Lager Lvivska Brewery, Ukraine 5.2% 23 Acadian Pilsener Acadian Brewing Co. LLC New Orleans, LA 24 Acme Brown Ale North Coast Brewing Co. Fort Bragg, CA 25 Actien~Alt-Dortmunder Actien Brauerei Dortmund,Germany 5.6% 26 Adnam's Bitter Sole Bay Brewery Southwold UK 27 Adnams Suffolk Strong Bitter (SSB) Sole Bay Brewery Southwold UK 28 Aecht Ochlenferla Rauchbier Brauerei Heller Bamberg Bamberg, Germany 4.5% 29 Aegean Hellas Beer Atalanti Brewery Atalanti,Greece 4.8% 30 Affligem Dobbel Abbey Ale N.V. -

M. Cojuangco, Jr., Chairman and Ceo of San Miguel Corporation, Former Diplomat and Public Servant

EIGHTEENTH CONGRESS OF THE ) REPUBLIC OF THE PHILIPPINES ) Second Regular Session ) RECEIVEDFILED DATC SENATE P.S. Res. No. 449 E4LLS Introduced by SENATOR RAMON BONG REVILLA, JR. RESOLUTION EXPRESSING PROFOUND SYMPATHY AND SINCERE CONDOLENCES OF THE SENATE OF THE PHILIPPINES ON THE DEATH OF EDUARDO "DANDING" M. COJUANGCO, JR., CHAIRMAN AND CEO OF SAN MIGUEL CORPORATION, FORMER DIPLOMAT AND PUBLIC SERVANT 1 WHEREAS, the Senate of the Philippines has, on numerous occasions, 2 recognized and honored distinguished Filipinos for their important contribution to their 3 respective fields and for their positive impact and influence in the development of our 4 society; 5 WHEREAS, Eduardo "Danding" M. Cojuangco, Jr., a former diplomat, public 6 servant, industrialist, businessman, and sports patron, died on 16 June 2020, just a 7 few days after he celebrated his 85th birthday; 8 WHEREAS, he is a well-known and respected businessman who served as 9 Chairman and Chief Executive Officer of San Miguel Corporation, considered as the 10 biggest food and beverage corporation in the Philippines and Southeast Asia, whose 11 several businesses include San Miguel Brewery, Inc., the oldest brewery in Southeast 12 Asia and the largest beer producer in the Philippines, and Ginebra San Miguel, Inc., 13 the largest gin producer in the world by volume1; 14 WHEREAS, under his stewardship, San Miguel Corporation greatly expanded 15 and transformed into a highly diversified conglomerate with valuable investments in 1 https://www.sanmicuel.coin.ph/article/food-and-beverages -

Preliminary Prospectus Dated May 20, 2019 – Part 1

n PETRON CORPORATION (a company incorporated under the laws of the Republic of the Philippines) ffer Shares may not be sold nor may an offer to an offer may be sold nor not may ffer Shares Offer in the Philippines of which such offer, solicitation or sale would be unlawful be unlawful or would sale solicitation such offer, which 15,000,000 Perpetual Preferred Shares Series 3 n inn with Oversubscription Option of up to 5,000,000 Perpetual Preferred Shares Series 3 consisting of Series 3A Preferred Shares (PRF3A): [●]% p.a. Series 3B Preferred Shares (PRF3B): [●]% p.a. at an Offer Price of ₱1,000.00 per Preferred Share to be listed and traded on the Main Board of The Philippine Stock Exchange, Inc. JOINT ISSUE MANAGERS, JOINT LEAD UNDERWRITERS AND JOINT BOOKRUNNERS1 SENIOR CO-LEAD UNDERWRITERS [●] CO-LEAD UNDERWRITERS issued in final form. Under no circumstances shall this Preliminary Prospectus constitute an offer to sell or the solicitatio the or to sell an offer constitute Prospectus Preliminary this shall circumstances Under no form. in final issued [●] PARTICIPATING UNDERWRITERS [•] SELLING AGENTS Trading Participants of The Philippine Stock Exchange, Inc. THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE AND SHOULD BE REPORTED IMMEDIATELY TO THE SECURITIES AND EXCHANGE COMMISSION. This Preliminary Prospectus is dated 20 May 2019. 1 BPI Capital Corporation, one of the Joint Issue Managers, Joint Lead Underwriters and Joint Bookrunners, is the [wholly-owned] investment banking subsidiary of Bank of the Philippine Islands which is the bank which the buy be accepted prior to the time that the Prospectus is is the Prospectus time that to the accepted prior be buy jurisdictio in any Offer the Shares of sale or solicitation offer, any be there shall nor Shares Offer any to buy of an offer jurisdiction. -

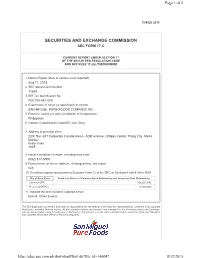

Securities and Exchange Commission Sec Form 17-C

Page 1 of 2 C04520-2015 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2(c) THEREUNDER 1. Date of Report (Date of earliest event reported) Aug 11, 2015 2. SEC Identification Number 11840 3. BIR Tax Identification No. 000-100-341-000 4. Exact name of issuer as specified in its charter SAN MIGUEL PURE FOODS COMPANY INC. 5. Province, country or other jurisdiction of incorporation Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 23/F The JMT Corporate Condominium, ADB Avenue, Ortigas Center, Pasig City, Metro Manila Postal Code 1605 8. Issuer's telephone number, including area code (632) 317-5000 9. Former name or former address, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common (PF) 166,667,096 Preferred (PFP2) 15,000,000 11. Indicate the item numbers reported herein Item 9. Other Events The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. -

Hong Kong Exchanges and Clearing Limited and the Stock Exchange Of

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. OVERSEAS REGULATORY ANNOUNCEMENT Please refer to the filing submitted by Philippine Long Distance Telephone Company (“PLDT”), a major operating associate of First Pacific Company Limited, with the Philippine Stock Exchange, in relation to the SEC Form 17-C together with the press release relating to the acquisition by PLDT of equity interest of the telecommunications business of San Miguel Corporation with Globe Telecom Inc. on a 50:50 basis. Dated this the 30th day of May, 2016 As at the date of this announcement, the board of directors of First Pacific Company Limited comprises the following directors: Executive Directors: Manuel V. Pangilinan, Managing Director and CEO Edward A. Tortorici Robert C. Nicholson Non-executive Directors: Anthoni Salim, Chairman Benny S. Santoso Tedy Djuhar Napoleon L. Nazareno Independent Non-executive Directors: Prof. Edward K.Y. Chen, GBS, CBE, JP Margaret Leung Ko May Yee, SBS, JP Philip Fan Yan Hok Madeleine Lee Suh Shin COVER SHEET SEC Registration Number Company Name Principal Office (No./StreetlBarangay/City/T own/Province) Form Type Department requiring the report Secondary License Type, If Applicable COMPANY INFORMATION Company's Email Address Company's Telephone Number/s Mobile Number 8168553 Annual Meeting Month/Day Fiscal Year No. of Stockholders Month/Day 11,808 Every 2nd Tuesday of June December 31 As of A ril 30, 2016 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Ma. -

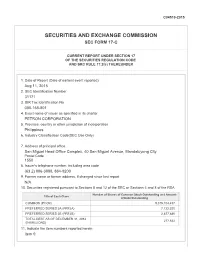

Securities and Exchange Commission Sec Form 17-C

C04510-2015 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2(c) THEREUNDER 1. Date of Report (Date of earliest event reported) Aug 11, 2015 2. SEC Identification Number 31171 3. BIR Tax Identification No. 000-168-801 4. Exact name of issuer as specified in its charter PETRON CORPORATION 5. Province, country or other jurisdiction of incorporation Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office San Miguel Head Office Complex, 40 San Miguel Avenue, Mandaluyong City Postal Code 1550 8. Issuer's telephone number, including area code (63 2) 886-3888, 884-9200 9. Former name or former address, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Number of Shares of Common Stock Outstanding and Amount Title of Each Class of Debt Outstanding COMMON (PCOR) 9,375,104,497 PREFERRED SERIES 2A (PRF2A) 7,122,320 PREFERRED SERIES 2B (PRF2B) 2,877,680 TOTAL DEBT AS OF DECEMBER 31, 2014 277,632 (IN MILLIONS) 11. Indicate the item numbers reported herein Item 9. The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. -

Portuguese in Shanghai

CONTENTS Introduction by R. Edward Glatfelter 1 Chapter One: The Portuguese Population of Shanghai..........................................................6 Chapter Two: The Portuguese Consulate - General of Shanghai.........................................17 ---The Personnel of the Portuguese Consulate-General at Shanghai.............18 ---Locations of the Portuguese Consulate - General at Shanghai..................23 Chapter Three: The Portuguese Company of the Shanghai Volunteer Corps........................24 ---Founding of the Company.........................................................................24 ---The Personnel of the Company..................................................................31 Activities of the Company.............................................................................32 Chapter Four: The portuguese Cultural Institutions and Public Organizations....................36 ---The Portuguese Press in Shanghai.............................................................37 ---The Church of the Sacred Heart of Jesus...................................................39 ---The Apollo Theatre....................................................................................39 ---Portuguese Public Organizations...............................................................40 Chapter Five: The Social Problems of the Portuguese in Shanghai.....................................45 ---Employment Problems of the Portuguese in Shanghai..............................45 ---The Living Standard of the Portuguese in Shanghai.................................47 -

Exclusions As of 06/30/2018 Company Name Country Ticker ISIN Issue

Exclusions as of 06/30/2018 Company Name Country Ticker ISIN Issue Alpha Natural Resources Inc. US ANR US02076X1028 Climate Change (thermal coal) Arch Coal Inc. US ACI US0393801008 Climate Change (thermal coal) China Coal Energy Company Limited Non US 1898 CNE100000528 Climate Change (thermal coal) China Resources Power Holdings HKG: 0836 Company Limited Non US HK0836012952 Climate Change (thermal coal) China Shenhua Energy Company SHA: 601088 Limited Non US CNE1000002R0 Climate Change (thermal coal) China Shenhua Overseas Capital - Company Limited Non US XS1165128239 Climate Change (thermal coal) Cloud Peak Energy Inc. US CLD US18911Q1022 Climate Change (thermal coal) NSE: COAL Coal India Limited Non US INE522F01014 Climate Change (thermal coal) JSE: EXX Exxaro Resources Limited Non US ZAE000084992 Climate Change (thermal coal) Glencore plc Non US LSE:GLEN JE00B4T3BW64 Climate Change (thermal coal) Hallador Energy Company US HNRG US40609P1057 Climate Change (thermal coal) Inner Mongolia Yitai Coal Co. Ltd. Non US 900948 CNE000000SK7 Climate Change (thermal coal) Peabody Energy Corp. US BTU US7045491047 Climate Change (thermal coal) IDX: ADRO PT Adaro Energy Tbk Non US ID1000111305 Climate Change (thermal coal) IDX: PTBA PT Bukit Asam (Persero) Tbk Non US ID1000094006 Climate Change (thermal coal) Westmoreland Coal Co. US WLB US9608781061 Climate Change (thermal coal) Whitehaven Coal Limited Non US WHC AU000000WHC8 Climate Change (thermal coal) Avichina Industry & Technology Co. Non US SEHK:2357 CNE1000001Y8 Human Rights Bank Hapoalim B.M. Non US TASE:POLI IL0006625771 Human Rights Bank Leumi Le-Israel BM Non US TASE:LUMI IL0006046119 Human Rights China Communications Construction Co. Non US SEHK:1800 CNE1000002F5 Human Rights China Petroleum & Chemical Corporation Non US SEHK:386 CNE1000002Q2 Human Rights Consolidated Infrastructure Group ltd. -

Serving the Nation 2019 ANNUAL REPORT ABOUT SAN MIGUEL FOOD and BEVERAGE, INC

serving the nation 2019 ANNUAL REPORT ABOUT SAN MIGUEL FOOD AND BEVERAGE, INC. San Miguel Food and Beverage, Inc. (SMFB) is a leading food and beverage company in the Philippines. The brands under which we produce, market, and sell our products are among the most recognizable and top-of-mind brands in the industry and hold market- leading positions in their respective categories. Key brands in the SMFB portfolio include San Miguel Pale Pilsen, San Mig Light, and Red Horse for beer; Ginebra San Miguel for gin; Magnolia for chicken and dairy products; Monterey for fresh and marinated meats; Purefoods for refrigerated, prepared, processed, and canned meats; Star and Dari Creme for margarine; and B-MEG for animal feeds. We have three primary operating divisions— beer and non-alcoholic beverages (NAB), spirits, and food. The Beer and NAB Division, through San Miguel Brewery Inc., and Spirits Division, through Ginebra San Miguel Inc., comprise our beverage business. On the other hand, our Food Division, San Miguel Foods, OUR CORE VALUE is operated through a number of key subsidiaries such as San Miguel Foods, Inc., Magnolia Inc., and MALASAKIT The Purefoods-Hormel Company, Inc. We serve It is in this spirit that we will look after the welfare and the Philippine archipelago through an extensive interests of our stakeholders. distribution and dealer network and export our products to over 60 markets worldwide. We will delight our customers with products and services of uncompromising quality, great taste and SMFB is a subsidiary of San Miguel Corporation (SMC), value, and are easily within their reach. -

Harry Colmery Collection, 1911-1979

Overview of the Collection Repository Kansas State Historical Society Creator Harry W. Colmery Title The Harry W. Colmery Collection Dates c.a. 1911 – c.a. 1979 (bulk c.a. 1925 – c.a. 1965) Quantity 266 cu. ft. Abstract Harry Walter Colmery: lawyer, insurance agent, politician, legionnaire; of Topeka, Kan., Washington, D.C. Legal case files of Harry Colmery from more than five decades of practicing law, includes legal documents and correspondence with clients; insurance materials from Pioneer National Life Insurance Company of Topeka, insurance books and journals, and other material regarding Colmery’s work on the boards of insurance companies; political material from Colmery’s Senatorial run in 1950, work with the Republican Party, and work on campaigns for other Republican candidates, including John Hamilton, Wendell Willkie, and Barry Goldwater; materials concerning Colmery’s civic involvement in organizations like the Kiwanis Club, Topeka Chamber of Commerce, YMCA, YWCA, and Boy Scouts of America; material from Colmery’s service as Civilian Aide to the Secretary of the War for Kansas; material from Colmery’s involvement with Colonel Andres Soriano of the Philippines, including legal material, information on Soriano’s businesses, and other material regarding the Philippines; personal information relating to Colmery, including correspondence, scrapbooks, newspaper clippings, autobiographical sketches, and yearbooks; financial information, both personal and business, including records, receipts, bookkeeping, etc.; materials from Colmery’s involvement with the American Legion, including his service as National Commander, information on the Servicemen’s Readjustment Act of 1944 (the G.I. Bill of Rights), and work with the Kansas Department of the American Legion and Capitol Post No. -

Dawn of a New Day for Filipinos in Canada 2019

Feel Good News www.filipinosmakingwaves.com JANUARY 2019 VOL. 8, NO. 01 TORONTO, CANADA Dawn of a New Day for Filipinos in Canada By Riley Mendoza change from one insignifi- cant speck in the world's second largest land mass The good augury of 2019, that is Canada to a bounti- the New Year, for the Filipi- ful community unified by no community came in Oc- their common ancestry and tober last year by the con- seen for their active partici- sideration of Parliament in pation in nation-building. Ottawa. It's in the form of a motion that institutionaliz- That spirit is captured in es the raison d'être for our Motion 155, which passed presence in the length and unanimously in the House breadth of Canada. of Commons. For nearly 80 years, Filipi- "The government," said its nos are in the margins of sponsor, Member of Parlia- the mainstream, hardly ev- ment Salma Zahid, "should er acknowledged except for recognize the contributions our back-breaking labour, that Filipino-Canadians and unrecognized despite have made to Canadian so- our modest contributions ciety, the richness of the in making Canada the fount Filipino language and cul- Canadian Prime Minister Trudeau surrounded by a large crowd of Filipinos in a surprise visit at Taste of multiculturalism. ture, and the importance of of Manila Festival in August 2016. He thanked the Filipino-Canadian community for the “incredible” reflecting upon Filipino contributions to make Canada better and stronger. PMO Photo by Adam Scotti That has changed. It should (Continued on page4 ) 2019: Shaping up to be Pacquiao retains st a busy year for Fil-Cans title with 61 win By Mon Torralba IT IS ELECTION YEAR FOR BOTH CANADA AND THE PHILIPPINES. -

Investors' Briefing

INVESTORS’ BRIEFING 2021 FIRST QUARTER RESULTS May 06, 2021 SAN MIGUEL CORPORATION FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 201,160 214,066 -6% Income from Operations 32,211 11,728 175% Net Income 17,174 1,093 1471% EBITDA 41,021 26,972 52% 2 SAN MIGUEL FOOD AND BEVERAGE, INC. FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 76,362 69,018 11% Income from Operations 12,569 8,643 45% Net Income 9,679 5,826 66% 3 SAN MIGUEL BREWERY INC. (a Division of San Miguel Food and Beverage, Inc.) FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 28,846 28,404 2% Income from Operations 6,751 5,383 25% Net Income 5,458 3,770 45% 4 GINEBRA SAN MIGUEL INC. (a Division of San Miguel Food and Beverage, Inc.) FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 11,338 7,452 52% Income from Operations 1,290 686 88% Net Income 1,042 474 120% 5 SAN MIGUEL FOODS (a Division of San Miguel Food and Beverage, Inc.) FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 36,180 33,161 9% Income from Operations 4,533 2,585 75% Net Income 3,387 1,636 107% 6 SAN MIGUEL FOODS (a Division of San Miguel Food and Beverage, Inc.) New Products Magnolia Ready-to-Cook chicken products Purefoods Ready-to-Eat Plant-based Seafood Line 7 SAN MIGUEL PACKAGING GROUP FIRST QUARTER 2021 IN MILLION FIRST QUARTER 2021 PESOS 1Q2021 1Q2020 CHANGE Net Sales 7,354 8,496 -13% Income from Operations 393 570 -31% 8 SMC GLOBAL POWER HOLDINGS CORP.