JOHCM UK Equity Income Fund Monthly Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2017 Annual Report & Accounts 2017 & Accounts Annual Report to Information Presented in the Financial Statements

Annual report & accounts 2017 Redefining Packaging Contents Our business Strategic report DS Smith is a leading provider of 1 Redefining packaging 8 2017 operational and financial highlights corrugated packaging in Europe 9 Chairman’s statement and of specialist plastic packaging 10 2017 at a glance 12 Our customers worldwide. We create sustainable 14 In conversation with the Group value by working in balance, to Chief Executive 16 Our markets develop our business, our people 18 Our business model and our environment. 20 What we do 21 Our key differentiators 22 Our strategic goals and KPIs 24 Our people Our vision 28 Group Chief Executive’s review 31 Operating review 32 Financial review 36 Sustainability review To be the leading supplier of 39 Principal risks sustainable packaging solutions. 41 Viability statement Governance 46 Introduction to corporate governance Our culture 48 Nomination Committee report 50 Our leadership team 52 Role and responsibilities of the Board 54 Board activities We have a clear set of values that we 56 Effectiveness expect all of our employees to own 57 Relations with stakeholders 58 Directors’ report and live by. 61 Audit Committee report 64 Remuneration Committee report 80 Directors’ responsibilities statement Be caring Financial statements We take pride in what we do and we care about our customers, 81 Independent Auditor’s report our people and the world around us. 85 Consolidated income statement Be challenging 86 Consolidated statement of comprehensive income We are not afraid to constructively challenge each other and ourselves to find a better way forward. 87 Consolidated statement of financial position Be trusted 88 Consolidated statement of changes in equity We can always be trusted to deliver on our promises. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

This Is the Message

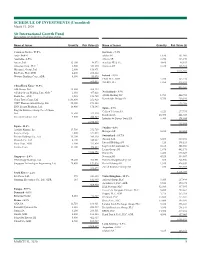

SCHEDULE OF INVESTMENTS (Unaudited) March 31, 2020 Sit International Growth Fund Investments are grouped by geographic region. Name of Issuer Quantity Fair Value ($) Name of Issuer Quantity Fair Value ($) Common Stocks - 97.0% Germany - 5.3% Asia - 30.6% adidas AG 1,630 361,905 Australia - 4.5% Allianz SE 2,250 383,170 Amcor, Ltd. 12,100 96,873 Aurelius SE & Co. 4,660 84,819 Atlassian Corp., PLC * 2,500 343,150 Siemens AG 2,225 186,311 Macquarie Group, Ltd. 2,600 138,471 1,016,205 Rio Tinto, PLC, ADR 4,400 200,464 Westpac Banking Corp., ADR 8,300 85,075 Ireland - 2.3% CRH, PLC, ADR 6,100 163,724 864,033 STERIS, PLC 1,950 272,942 China/Hong Kong - 11.8% 436,666 AIA Group, Ltd. 32,200 288,339 Alibaba Group Holding, Ltd., ADR * 2,350 457,028 Netherlands - 3.5% Baidu, Inc., ADR * 1,525 153,705 ASML Holding NV 1,700 444,788 China Tower Corp., Ltd. 1,136,000 252,420 Koninklijke Philips NV 5,750 230,920 CSPC Pharmaceutical Group, Ltd. 88,000 173,104 675,708 ENN Energy Holdings, Ltd. 18,400 178,245 Spain - 4.7% Ping An Insurance Group Co. of China, Cellnex Telecom SA 6,123 277,755 Ltd. 33,500 327,170 Iberdrola SA 45,900 448,949 Tencent Holdings, Ltd. 9,000 444,849 Industria de Diseno Textil SA 6,900 178,804 2,274,860 905,508 Japan - 10.1% Sweden - 0.8% Astellas Pharma, Inc. 17,700 272,710 Hexagon AB 3,800 160,684 Keyence Corp. -

This Is the Message

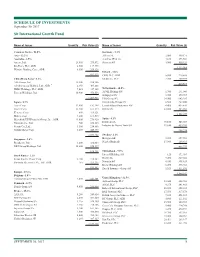

SCHEDULE OF INVESTMENTS September 30, 2017 Sit International Growth Fund Name of Issuer Quantity Fair Value ($) Name of Issuer Quantity Fair Value ($) Common Stocks - 96.0% Germany - 5.3% Asia - 22.2% Allianz SE 2,000 449,171 Australia - 2.5% Aurelius SE & Co. 4,160 273,564 Amcor, Ltd. 23,400 279,872 Siemens AG 3,900 550,324 Rio Tinto, PLC, ADR 2,500 117,975 1,273,059 Westpac Banking Corp., ADR 8,300 209,326 Ireland - 1.8% 607,173 CRH, PLC, ADR 5,800 219,588 China/Hong Kong - 6.2% Medtronic, PLC 2,700 209,979 AIA Group, Ltd. 32,200 238,386 429,567 Alibaba Group Holding, Ltd., ADR * 2,350 405,868 HSBC Holdings, PLC, ADR 7,025 347,105 Netherlands - 10.5% Tencent Holdings, Ltd. 10,900 476,556 ASML Holding NV 1,700 291,040 Galapagos NV * 3,725 379,717 1,467,915 ING Groep NV 34,900 643,285 Japan - 8.7% Koninklijke Philips NV 6,500 267,800 Asics Corp. 12,900 192,398 LyondellBasell Industries NV 4,400 435,820 Daicel Corp. 13,400 161,574 RELX NV 22,800 485,033 Keyence Corp. 600 319,121 2,502,695 Makita Corp. 4,200 169,515 Mitsubishi UFJ Financial Group, Inc., ADR 43,000 276,920 Spain - 4.1% Nintendo Co., Ltd. 700 258,113 Iberdrola SA 70,100 545,069 Secom Co., Ltd. 3,500 254,886 Industria de Diseno Textil SA 11,650 439,205 Suzuki Motor Corp. 8,400 440,875 984,274 2,073,402 Sweden - 2.1% Singapore - 2.6% Hexagon AB 5,200 257,962 Broadcom, Ltd. -

M&G Investment Funds

M&G Investment Funds (3) Interim Long Report and unaudited Financial Statements for the six months ended 31 December 2020 Contents Authorised Corporate Director’s Report .......... 1 Directors’ statement .......................... 4 Financial statements and notes.................. 5 Authorised Corporate Director’s Reports, including the financial highlights and financial statements and notes for: M&G Corporate Bond Fund .................... 6 M&G Dividend Fund .......................... 38 M&G Emerging Markets Bond Fund............. 61 M&G European Corporate Bond Fund ........... 87 M&G Global Government Bond Fund............ 112 M&G Recovery Fund .......................... 135 M&G Smaller Companies Fund ................. 159 Other regulatory disclosures .................... 178 Glossary ..................................... 179 M&G Investment Funds (3) Interim Long Report and unaudited Financial Statements • December 2020 Authorised Corporate Director’s Report The Authorised Corporate Director (ACD) of M&G A shareholder is not liable for the debts of the Company Investment Funds (3) presents its Interim Long Report and will never be liable to make any further payment to and unaudited Financial Statements for the six months the Company after paying the purchase price of the ended 31 December 2020. shares. The unaudited financial statements of Fund managers M&G Investment Funds (3) and the investment report The following fund managers are employed by M&G FA and unaudited financial statements and notes of each Limited which is an associate of M&G Securities sub-fund are presented in their individual sections of Limited. this report as set out in the contents page. M&G Corporate Bond Fund Please note that we have included an explanation of key Richard Woolnough & Ben Lord investment terminology in the ‘Glossary’ (at the back of this report). -

Market Roundup Company Focus: Ashtead 9 March 2018

9 March 2018 Market Roundup Chart 1: UK Services PMI The FTSE 100 index bounced off a 14-month low on Monday, adding 65 0.7% as packaging manufacturers Smurfit Kappa and DS Smith led the risers. 60 Tuesday saw a further 0.4% gain for the blue-chip index. Tesco 55 benefited after industry data showed strong sales in recent weeks. Just Eat led the fallers however, as the takeaway ordering website 50 announced a £50m-plus business investment, which is expected to cut 45 2018 earnings by a quarter. Smurfit Kappa, having rejected a bid from International Paper, hit a 40 record high on Wednesday after a report that it would be open to a Jul-17 Jul-16 Jul-15 Jan-18 Jan-17 Jan-16 Sep-17 Sep-16 Sep-15 Nov-17 Nov-16 Nov-15 Mar-17 Mar-16 Mar-15 May-17 May-16 takeover at €40 per share. May-15 Rolls-Royce was Wednesday’s biggest blue-chip riser after full-year IHS Markit UK Services PMI earnings beat expectations. Source: Bloomberg Data at 9/3/2018 Retailers were under pressure on Thursday after John Lewis Partnership warned that the weak pound and rising costs were Chart 2: Annual house price growth (%l) squeezing earnings. 6.0 But Aviva rose after increasing its full-year dividend by 18% - its fourth 5.0 consecutive year of double-digit dividend growth. Carnival was also up on positive broker comment. The FTSE 100 added 0.6%. 4.0 UK shares were mixed in early trading on Friday ahead of the monthly 3.0 US jobs report. -

QSMARTLAB WEEKLY NEWSLETTER 1 Equity Markets

Equity Markets The QE ALL SHARES /d Index was up -0.2077% week to date. The top 5 gainers for the week were Gulf International Services QPSC up 5.9172%, Commercial Bank PSQC up 3.0233%, Masraf Al Rayan QPSC up 2.4%, Qatar International Islamic Bank QPSC up 2.3134% and Mannai Corporation QPSC up 1.9231%. The top 5 decliners for the week were Vodafone Qatar PQSC down -4.8779%, Qatar Navigation QPSC down -4.6153%, Medicare Group QPSC down - 3.3332%, Qatar Islamic Insurance Company QPSC down -2.1582% and United Development Company QPSC down -2.1428%. QSMARTLAB WEEKLY NEWSLETTER 1 U.S Markets The S&P 500 INDEX/d Index was up 0.8533% week to date. The top 5 gainers for the week were DaVita Inc up 17.3161%, Ralph Lauren Corp up 16.1037%, Xerox Holdings Corp up 16.0394%, Capri Holdings Ltd up 13.3746% and Discovery Inc up 13.3712%. The top 5 decliners for the week were Expedia Group Inc down -26.473%, TripAdvisor Inc down -20.891%, Under Armour Inc down -16.9346%, Under Armour Inc down -16.0232% and Diamondback Energy Inc down -13.089%. European Markets The FTSE 100 INDEX/d Index was up 0.78% week to date. The top 5 gainers for the week were Associated British Foods PLC up 8.5778%, Rolls-Royce Holdings PLC up 7.204%, DS Smith PLC up 5.6489%, Glencore PLC up 5.5821% and British American Tobacco PLC up 5.2526%. The top 5 decliners for the week were Hiscox Ltd down - 13.966%, Ocado Group PLC down -11.1649%, BT Group QSMARTLAB WEEKLY NEWSLETTER 2 PLC down -7.9714%, Fresnillo PLC down -6.4721% and British Land Company PLC down - 6.3112%. -

Holdings As of June 30, 2021

Units Cost Market Value INTERNATIONAL EQUITY FUND-I International Equities 97.27% International Common Stocks AUSTRALIA ABACUS PROPERTY GROUP 4,781 10,939 11,257 ACCENT GROUP LTD 3,078 2,769 6,447 ADBRI LTD 224,863 495,699 588,197 AFTERPAY LTD 18,765 1,319,481 1,662,401 AGL ENERGY LTD 3,897 48,319 23,926 ALTIUM LTD 11,593 214,343 319,469 ALUMINA LTD 10,311 14,655 12,712 AMP LTD 18,515 29,735 15,687 APA GROUP 2,659 20,218 17,735 APPEN LTD 20,175 310,167 206,065 ARENA REIT 2,151 5,757 5,826 ASX LTD 678 39,359 39,565 ATLAS ARTERIA LTD 5,600 25,917 26,787 AURIZON HOLDINGS LTD 10,404 32,263 29,075 AUSNET SERVICES LTD 9,482 10,386 12,433 AUSTRALIA & NEW ZEALAND BANKIN 22,684 405,150 478,341 AVENTUS GROUP 2,360 4,894 5,580 BANK OF QUEENSLAND LTD 2,738 17,825 18,706 BEACH ENERGY LTD 5,466 6,192 5,108 BEGA CHEESE LTD 1,762 6,992 7,791 BENDIGO & ADELAIDE BANK LTD 2,573 19,560 20,211 BHP GROUP LTD 9,407 243,370 341,584 BHP GROUP PLC 75,164 1,584,327 2,212,544 BLUESCOPE STEEL LTD 2,905 24,121 47,797 BORAL LTD 4,848 16,859 26,679 BRAINCHIP HOLDINGS LTD 5,756 2,588 2,112 BRAMBLES LTD 153,566 1,133,082 1,318,725 BRICKWORKS LTD 375 4,689 7,060 BWP TRUST 2,988 8,177 9,530 CARSALES.COM LTD 466 6,896 6,916 CENTURIA INDUSTRIAL REIT 2,943 6,264 8,191 CENTURIA OFFICE REIT 190,589 261,156 334,222 CHALICE MINING LTD 464 3,129 2,586 CHALLENGER LTD 3,038 15,904 12,335 CHARTER HALL LONG WALE REIT 3,600 12,905 12,793 CHARTER HALL RETAIL REIT 148,478 395,662 422,150 CHARTER HALL SOCIAL INFRASTRUC 2,461 5,340 6,404 CIMIC GROUP LTD 409 6,668 6,072 COCHLEAR LTD 2,492 -

DS Smith Annual Report 2021 Double Page Spreaddownload

DS Smith Plc Redefining Annual Report 2021 Packaging for a Changing World Annual Report 2021 GROUP CHIEF EXECUTIVE’S INTRODUCTION STRATEGIC REPORT Contents 2020/21 Financial highlights Strategic Report Foreword Highlights 1 Group Chief Executive’s introduction 2 Redefining Packaging for a Changing World 3 Our stakeholders +3.5% £5,976m 4 Our business – at a glance Corrugated box volumes Revenue2 6 The changing relationship with packaging (2020: +0.6%) (2020: £6,043m) “In this report we set out details of 9 Helping customers meet their biggest challenges our performance and strong 10 Leading the transition to the circular momentum in the second half of economy 12 Now and Next – our sustainability strategy the year 2020/21, and how our 14 Chairman’s statement 8.4% £311m business is extremely well 15 Section 172 statement Return on sales1 Operating profit2 16 Our business model (2020: 10.9%) (2020: £455m) positioned through our circular 18 Our differentiation and market drivers 20 Group Chief Executive’s interview business model to meet the 22 Our strategy – customers challenges of the changing world.” 24 Our strategy – people 30 Our strategy – sustainability Miles Roberts, Group Chief Executive 34 Our strategy – financial £502m 12.1p 36 Operating review Adjusted operating profit1 Dividend per share 40 Financial review (2020: £660m) (2020: nil) 47 Principal risks 49 Viability statement 56 Task Force on Climate-related Financial Disclosures (TCFD) 59 Non-financial information statement -£306m £486m Over the course of 2020/21 we have not only responded to the We also recognise that this changing world has placed increased Governance impact of Covid-19, we have continued to make significant demands on our employees’ wellbeing, which is why we have Free cash flow1 62 Board of Directors to £1,795m net debt progress in furthering our strategy to be the leading supplier of launched a new framework to support this critical area. -

Black Sun Template

Board of Directors N R N A N R A N R Geoff Drabble Miles Roberts Adrian Marsh Celia Baxter Alina Kessel Chairman Group Chief Executive Group Finance Director Non-Executive Director Non-Executive Director Key strengths: Key strengths: Key strengths: Key strengths: Key strengths: • Wealth of industrial and • Clear strategic mindset • Strong financial expertise • Extensive HR experience • Broad and wide-ranging international experience • Strong leadership skills within an international and ESG knowledge and marketing experience • Extensive experience as a context experience • International outlook External appointment: chairman • Wealth of finance • Board experience in • Miles is a non-executive External appointment: experience in large listed non-UK listed companies External appointments: director of Aggreko plc • Alina is a Global Client multinationals • Geoff is Non-Executive External appointments: Leader at WPP, a leading Miles was appointed to the Chairman of Ferguson plc External appointment: • Celia is the senior international marketing Board on 4 May 2010 as and a Non-Executive • Adrian is a non-executive independent director and communications Group Chief Executive. Director of Howden director and audit the remuneration company Joinery Group Plc. Following his engineering committee chairman at committee chair at Senior Alina was appointed to the degree he became a John Wood Group PLC plc and remuneration Geoff was appointed to the Board on 1 May 2020 as a chartered accountant and committee chair at RHI Board on 1 September 2020 Adrian was appointed to the Non-Executive Director. brings to the Board Magnesita NV as a Non-Executive Director Board on 24 September extensive financial and She has over 25 years and became the Chairman of 2013 as Group Finance Celia was appointed to the operational experience. -

Citi VIBE Equity UK Net TR Index (CIISRLGT)

Date: 16-Apr-21 Index Weights as of quarterly rebalance date 08-Apr-21 Citi VIBE Equity UK Net TR Index (CIISRLGT) Constituent Bloomberg Ticker Constituent Name Weight(%) 1 AAL LN Equity Anglo American Plc 0.46% 2 ABF LN Equity Associated British Foods 0.43% 3 ADM LN Equity Admiral Group 5.35% 4 AHT LN Equity Ashtead Group 0.85% 5 AV/ LN Equity Aviva 0.50% 6 AZN LN Equity AstraZeneca Plc 1.67% 7 BA/ LN Equity BAE Systems Plc 0.55% 8 BARC LN Equity Barclays 0.45% 9 BATS LN Equity British American Tobacco Plc 0.63% 10 BDEV LN Equity Barratt Developments 0.48% 11 BKG LN Equity Berkeley Group Holdings Plc 0.62% 12 BLND LN Equity British Land Co 0.46% 13 BHP LN Equity BHP GROUP PLC ORD USD0.50 0.50% 14 BNZL LN Equity Bunzl 5.22% 15 BP/ LN Equity BP 0.36% 16 BRBY LN Equity Burberry Group 0.54% 17 BT/A LN Equity BT Group 0.45% 18 CNA LN Equity Centrica 0.48% 19 CPG LN Equity Compass Group 0.40% 20 CRDA LN Equity Croda Intl 2.11% 21 DGE LN Equity Diageo Plc 0.66% 22 DLG LN Equity Direct Line Insurance Group PL 0.88% 23 EXPN LN Equity Experian Plc 1.16% 24 GLEN LN Equity Glencore International PLC 0.39% 25 GSK LN Equity GlaxoSmithKline 0.75% 26 ENT LN Equity GVC HLDGS PLC ORD EUR0.01 0.92% 27 HL/ LN Equity Hargreaves Landsdown Plc 0.64% 28 HLMA LN Equity Halma 1.21% 29 HSBA LN Equity HSBC Holdings Plc 0.73% 30 IAG LN Equity International Consolidated Airlines Group SA 0.31% 31 IHG LN Equity INTERCONTL HOTELS ORD GBP0.208521303 0.61% 32 III LN Equity 3I Group 0.67% 33 IMI LN Equity IMI 1.28% 34 IMB LN Equity Imperial Tobacco 0.46% 35 INF LN Equity -

Stewardship Fund Holdings (PDF 36KB)

Holdings are as of 25th September 2019 Stewardship Fund Holidings UK Equity Income UK Equity International Bond ASHTEAD GROUP ASHTEAD GROUP ALPHABET AA BOND NATIONAL GRID ELECTRICITY TRANSMIS ASTRAZENECA ASTRAZENECA ARCH CAPITAL GROUP AKELIUS RESIDENTIAL PROPERTY NETWORK RAIL INFRA FIN BELLWAY B&M EUROPEAN VALUE RETAIL ASML HOLDING AMGEN NEW YORK LIFE GLOBAL FUNDING BT GROUP BELLWAY ASSA ABLOY ANGLIAN WATER NGG FINANCE CINEWORLD GROUP BT GROUP AXA ANNINGTON FUNDING NIE FINANCE COMPASS GROUP BURBERRY GROUP BECTON DICKINSON APT PIPELINES NORDEA BANK AB COUNTRYSIDE PROP CME GROUP INC CLASS A BROADCOM ASSURA FIN NORTHERN GAS NETWORKS EXPERIAN COMPASS GROUP CHINA CONCH VENTURE HOLDINGS ASTER TREASURY NOTTING HILL GENESIS GLAXOSMITHKLINE COUNTRYSIDE PROP COMCAST CORP AT&T ORANGE GREENCOAT UK WIND EXPERIAN DANAHER CORP AXA ORSTED HSBC HOLDINGS FERGUSON EQUIFAX BANCO SANTANDER PHOENIX GROUP HOLDINGS IMI GLAXOSMITHKLINE ESTEE LAUDER BANK OF AMERICA CORP PROLOGIS LP INFORMA HSBC HOLDINGS FIRST REPUBLIC BANK BARCLAYS BANK PRUDENTIAL INTERMEDIATE CAPITAL GROUP INFORMA HDFC BANK BPCE RABOBANK NEDERLAND ITV INTERCONTINENTAL HOTELS GROUP HOME DEPOT BRITISH TELECOMMUNICATIONS RL FINANCE BONDS JOHN LAING GROUP INTERMEDIATE CAPITAL GROUP INFINEON TECHNOLOGIES CHANNEL LINK ROYAL BANK OF SCOTLAND GROUP JOHNSON MATTHEY ITV KDDI CORP CITIGROUP SANTANDER UK LAND SECURITIES GROUP REIT JOHN LAING GROUP KINGSPAN GROUP CLARION FUNDING SCOTLAND GAS NETWORKS LEGAL AND GENERAL GROUP JOHNSON MATTHEY LONZA GROUP CLARION HOUSING GROUP SCOTTISH AND SOUTHERN ENERGY LLOYDS