Telenor Short Introduction Telenor Short Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Easypaisa and Grameenphone Win Global Mobile Awards

Easypaisa and Grameenphone win Global Mobile Awards Yesterday, at the Mobile World Congress in Barcelona Telenor Pakistan’s Easypaisa was awarded two Global Mobile Awards. Telenor's Bangladeshi operation, Grameenphone was also a winner! On Tuesday 25 February, the GSM Association announced the winners of the 19th Annual Global Mobile awards. “The Global Mobile Awards once again showcase the outstanding level of innovation and creative products and services being developed across a diverse and growing industry,” said John Hoffman, CEO, GSMA Ltd. in a press release. “With more than 680 high calibre entries this year, the competition was stronger than ever and it is a significant achievement to have been honoured today.” Easypaisa wins Best Mobile Money and Best Service for Women Awards Easypaisa, the first and largest branchless banking service in Pakistan, owned by Telenor Pakistan and Tameer Bank was announced winner in the following two categories: Best Mobile Money Service and Best Mobile Service for Women in Emerging Markets. “This is a great recognition of the efforts Easypaisa has made in providing financial inclusion to the unbanked population of Pakistan. We have innovative products and strong distribution channels in combination with a high performing team. Our approach has been very focused on addressing customer’s key needs and also entering into close partnerships with organisations like Benazir Income Support Program. Last night’s awards give encouragement and motivation for continuous efforts to improve people’s lives in Pakistan,” said Roar Bjærum, Head of Financial Services Asia who received the award. Today Easypaisa serves over six million customers every month through a wide network of 35,000 agents in 750 cities across Pakistan. -

Telenor Pakistan and Careem Announce Partnership

Telenor Pakistan and Careem announce partnership Telenor Pakistan customers will have access to Wi-Fi equipped rides in addition to discounted rates. Telenor Pakistan has joined forces with Careem to provide discounted rides to Telenor customers. Careem is the premium transportation network company in Pakistan, connecting captains (drivers) to customers via its software platform. Under the agreement, Careem will provide 35% discount to Telenor customers on their first ride. In addition, all customers will be able to enjoy free WiFi service during their ride. As part of the deal, captains will also enjoy special data packages from Telenor Pakistan. Careem’s digital transportation network operates in three major metropolises of Pakistan, including Karachi, Lahore and Islamabad, in addition to 24 cities across the UAE and the Kingdom of Saudi Arabia. Careem is preferred by commuters for its convenient access via mobile app and online portal, superior quality rides and competitive rates. Michael Foley, CEO Telenor Pakistan, said, “We are pleased to enter into this partnership with Careem as it is in line with Telenor’s commitment to deliver the best possible services to our customers. With Careem, Telenor subscribers will not only enjoy cheaper and more comfortable rides, but also WIFI connectivity on the go. We will continue to look for newer avenues of serving our valued customers.” Junaid Iqbal, Managing Director Careem, said, “We are delighted to have struck this crucial deal with Telenor Pakistan which is the biggest proponent to digital enablement in the country. The agreement will not only help facilitate our mutual customers but go on to explore new prospects of making our businesses more accommodating and preferable to our customers. -

Download PDF Dossier

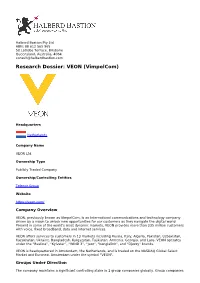

Halberd Bastion Pty Ltd ABN: 88 612 565 965 58 Latrobe Terrace, Brisbane Queensland, Australia, 4064 [email protected] Research Dossier: VEON (VimpelCom) Headquarters Netherlands Company Name VEON Ltd. Ownership Type Publicly Traded Company Ownership/Controlling Entities Telenor Group Website https://veon.com/ Company Overview VEON, previously known as VimpelCom, is an international communications and technology company driven by a vision to unlock new opportunities for our customers as they navigate the digital world. Present in some of the world's most dynamic markets, VEON provides more than 235 million customers with voice, fixed broadband, data and internet services. VEON offers services to customers in 13 markets including Russia, Italy, Algeria, Pakistan, Uzbekistan, Kazakhstan, Ukraine, Bangladesh, Kyrgyzstan, Tajikistan, Armenia, Georgia, and Laos. VEON operates under the “Beeline”, “Kyivstar”, “WIND 3”, “Jazz”, “banglalink”, and “Djezzy” brands. VEON is headquartered in Amsterdam, the Netherlands, and is traded on the NASDAQ Global Select Market and Euronext Amsterdam under the symbol "VEON". Groups Under Direction The company maintains a significant controlling stake in 1 group companies globally. Group companies are those maintaining a parent relationship to individual subsidiaries and/or mobile network operators. Global Telecom Holding Headquarters: Netherlands Type: Publicly Traded Company, Subsidiary Subsidiaries The company has 8 subsidiaries operating mobile networks. Beeline Armenia Country: Armenia 3G Bands: -

Telenor Pakistan

Security v Access: The Impact of Mobile Network Shutdowns Case Study: Telenor Pakistan Case Study Number 3 SEPTEMBER 2015 Case Study Number 3 SEPTEMBER 2015 Security v Access: The Impact of Mobile Network Shutdowns Case Study: Telenor Pakistan About IHRB The Institute for Human Rights and Business (IHRB) is a global centre of excellence and expertise (a think & do tank) on the relationship between business and internationally proclaimed human rights standards. We work to shape policy, advance practice and strengthen accountability to ensure the activities of companies do not contribute to human rights abuses, and in fact lead to positive outcomes. IHRB prioritises its work through time-bound programmes that can have the greatest impact, leverage and catalytic effect focusing on countries in economic and political transition, as well as business sectors that underpin others in relation to the flows of information, finance, workers and commodities. www.ihrb.org About Digital Dangers “Digital Dangers: Identifying and Mitigating Threats in the Digital Realm” is a project developed by IHRB in collaboration with the School of Law at the University of Washington in Seattle. The project builds on IHRB’s involvement in the European Commission ICT Sector Guide on Implementing the UN Guiding Principles on Business and Human Rights1. Digital Dangers identifies a number of areas including security, safety, free assembly, free expression and privacy where ICT companies and other actors would benefit from in-depth human rights analysis and policy oriented recommendations. One of the aims of the Digital Dangers project is to encourage companies to be open and transparent about the complex dilemmas they face in respecting freedom of expression and privacy by sharing their experiences to spark debate with governments and civil society and bring about positive change. -

EDI International Settlements Presentation by Eddy Patient September 2001 Contents

ITU SEMINAR (SLOVAKIA) EDI International Settlements Presentation by Eddy Patient September 2001 Contents • EDI & ETIS - Defined • Facts about the ETIS/EDI International Settlements Group • History of the EDI Group and D190 recommendation • EDI Group & Structure • EDI - Defined & how it works • EDI Global Members EDI Electronic Data Interchange EDI/ELECTRONIC COMMERCE IS ..... DATA EXCHANGED ELECTRONICALLY BETWEEN COMPUTERS OVER A NETWORK DATA EXCHANGE TODAY ? Why EDI ? Business BENEFITS uDemand from industry for E-Commerce uSpeed of transaction uAccuracy of data uEase of processing uCost reduction on many levels uSecurity ETIS ETIS e- and telecommunications information services is the platform for the interchange of information, experiences and professional networking at the heart of the Telecommunications industry. It is an industry led group, which brings together telecommunications operators, suppliers and content providers on key information and communication technology issues and facilitates co-operation among them. Facts about ETIS • ETIS is a global organization and has its origins in Europe • It’s members consist of Telecom Operators • ETIS is a non-profit making organization and relies on membership fees to cover costs • In addition to many other activities ETIS has several working groups which focus on specific topics • The International Settlements EDI forum is one such group • ETIS facilitates, supports, coordinate and provides the neutral presence for this group Facts about EDI Group • Members must be International Operators who are licensed to carry international traffic and enter into international agreements • EDI group is a non-profit making group • Relies on membership funding, members input and voluntary contribution from Operators • EDI Group is considered a non-competitive group due to the nature of the topic and its objective • Members are allowed to vote and influence decisions • EDI member Carriers are 40+ ; Approx. -

Opera Mini Opera Mobile Shipments Pre-Installed in 4Q08: 7.3 Million

Opera Software Fourth quarter 2008 A note from our lawyers 2 This presentation contains and is, i.a., based on forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements . Forward-looking statements may in some cases be identified by terminology such as “may”, “will”, “could”, “should”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict”, “pp,gpgyotential” or “continue”, the negative of such terms or other comparable terminology. These statements are only predictions. Actual events or results may differ materially, and a number of factors may cause our actual results to differ materially from any such statement. Although we believe that the expectations and assumptions reflected in the statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievement. Opera Software ASA makes no representation or warranty (express or implied) as to the correctness or completeness of the presentation, and neither Opera Software ASA nor any of its direc tors or emp loyees assumes any lia bility resu lting from use. Excep t as requ ire d by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this presentation to conform these statements to actual results or to changes in our expectations. You are advised, however, to consult any further public disclosures made by us, su ch as filings made w ith the OSE or press releases . -

Case No COMP/M.6948 - TELENOR/ GLOBUL/ GERMANOS

EN Case No COMP/M.6948 - TELENOR/ GLOBUL/ GERMANOS Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 03/07/2013 In electronic form on the EUR-Lex website under document number 32013M6948 Office for Publications of the European Union L-2985 Luxembourg EUROPEAN COMMISSION Brussels, 3.7.2013 C(2013) 4282 final In the published version of this decision, some information has been omitted pursuant to Article PUBLIC VERSION 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible MERGER PROCEDURE the information omitted has been replaced by ranges of figures or a general description. To the notifying party Dear Sir/Madam, Subject: Case No COMP/M.6948 - Telenor/ Globul/ Germanos Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 (1) On 30 May 2013, the European Commission received the notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Telenor ASA ("Telenor", Norway or the "Notifying Party") acquires within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of the undertakings Cosmo Bulgaria Mobile EAD (trading as "Globul", Bulgaria) and Germanos Telecom Bulgaria EAD ("Germanos", Bulgaria), by way of purchase of shares2. Globul and Germanos are together referred to as the "Target Companies". Telenor, Globul and Germanos are collectively referred to as the "Parties". 1 OJ L 24, 29.1.2004, p. -

Acquisition of Vodafone Sweden Completed

Acquisition of Vodafone Sweden completed Telenor has today paid EUR 994 million to Vodafone, thereby completing the acquisition of the mobile operator Vodafone Sweden. Including debt, the purchase price is EUR 1,035 million. Johan Lindgren will from today enter as CEO of the company. With the completion of the acquisition, Telenor's Scandinavian mobile customer base increases by 37 per cent, reaching a total of 5.6 million subscribers. The transaction secures Telenor a strong position in the Swedish mobile market. Vodafone Sweden is the third largest mobile operator in Sweden with 1.5 million subscribers and a market share of 16 per cent (22 per cent measured in revenues). The company is the second largest player in the Swedish business market with a 30 per cent market share in the corporate segment. Johan Lindgren will from today enter as CEO of the company. Johan Lindgren was previously CFO and Deputy CEO of Bredbandsbolaget, a company that was acquired by Telenor in May 2005. "We are very pleased that Johan Lindgren accepted the position as CEO of Vodafone Sweden. He has extensive experience from executive work, and possesses all the necessary commercial qualities required to take both the company and Telenor's position in the Swedish market further," said Morten Karlsen Sørby, Executive Vice President and Head of Telenor Nordic operations. "I approach this task with a considerable amount of humility. Vodafone Sweden is an operation with a solid position and many excellent services. At the same time we are seeing that the competition is getting tougher, and the company has started an important restructuring process which will also involve cost-reductions," says Johan Lindgren. -

Telenor Seeking to Acquire Control of Digi in Malaysia

Telenor seeking to acquire control of DiGi in Malaysia Telenor, through its wholly-owned subsidiary Telenor Asia Pte. Ltd., today announced that it is seeking to increase its shareholdings in DiGi.Com Berhad ("DiGi"). Telenor presently holds 247 million ordinary shares in DiGi, or approximately 32.9 percent. Telenor has informed the Board of Directors of DiGi of its intention to make a Voluntary Partial Take-over Offer for up to a maximum of 210.5 million additional shares, increasing its total ownership in DiGi to 61 percent, the current maximum foreign ownership allowed by Malaysian authorities. The partial offer was approved by the Securities Commission of Malaysia on June 20, 2001. Under the terms of the offer, Telenor will offer to all holders of the remaining 503 million DiGi shares a cash consideration of RM 6.60 per share for up to 210.5 million shares. The partial tender offer is conditional on Telenor receiving tenders such that it will hold at least 375,000,001 DiGi shares, representing more than 50 percent, at the completion of the offer. If upon completion of the offer Telenor holds 50 percent plus one share or 61 percent, the investment amounts to approx. USD 222 million or USD 365 million respectively. Following the offer, Telenor intends to maintain the public listing status of DiGi on the Kuala Lumpur Stock Exchange (KLSE: DIGI). Telenor is seeking to increase its long-term interest in the Malaysian mobile market through the partial tender offer for DiGi shares. The company is a full-service mobile telecommunications operator in Malaysia, with more than one million mobile subscribers on its GSM1800 network by the end of March 2001. -

Easypaisa Introduces Mobile Accounts

Easypaisa Introduces Mobile Accounts Telenor Pakistan is offering transactions through the customer's own mobile phone. This is a first of its kind product in Pakistan. easypaisa Mobile Accounts are virtual bank accounts and work just like a normal bank account. Once an easypaisa Mobile Account is opened, users can go to any of the thousands of easypaisa shops in Pakistan to deposit or withdraw cash from their easypaisa Mobile Account. A mobile bank account Using easypaisa Mobile Accounts, Telenor subscribers are also able to pay bills and transfer money in addition to a range of other services from their own mobile phones. The bank account is provided through the customer's Telenor connection and can be used at anytime and anywhere. Customers will be able to carry out deposits and withdrawals from any of more than 5500 easypaisa Retail Merchants, 23 Sales and Service Centers, 50 Tameer Microfinance Bank Branches and 225 Telenor Franchises from all over the country. Opening an account Accounts can be opened from any Telenor Sales and Service Centers, Telenor Franchise or Tameer Bank branch. Mobile Accounts have no minimum balance requirements and account opening is instant. Upcoming services include: fund transfers to any bank in Pakistan withdrawals through ATM cards payment of Telenor Persona bills (a post paid service) purchase of easyload receiving International Remittances from abroad Easier access to banking services Considering that close to 90 per cent of the adult population in Pakistan has no bank account and more than 60 per cent use mobile phone services, easypaisa aims to provide financial inclusion for the urban as well as the rural population. -

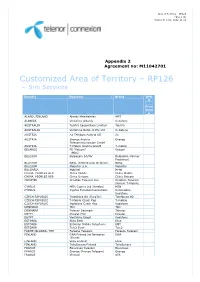

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd. -

Operators' Approaches to Customer Data Monetisation in Europe And

Operators’ approaches to customer data monetisation in Europe and the USA are diverging due to regulation February 2018 Enrique Velasco-Castillo Telecoms operators have enormous amounts of information about their customers and should, at least in theory, be able to extract value from it. However, operators worldwide have struggled to earn more than marginal revenue from this data. Undeterred, and aided by favourable regulatory developments, operators in the USA are increasing their efforts in the advertising market. However, in Europe, the introduction of the European Union’s General Data Protection Regulation (GDPR) makes similar initiatives even less likely. Advertising is the obvious opportunity to develop Advertising is an obvious way for operators to capitalise on customer data by providing it to advertisers. Operators, with their own inventory such as websites or video properties, can take a greater share of the advertising spend. In the USA, telecoms operators can sell their customers’ data (including location and browsing history) to advertisers without the users’ consent. This type of data usage has not been possible in Europe, even in advance of the introduction of the GDPR. GDPR will be enforced from 25 May 2018, when European operators will have even greater restrictions on how they can use their customers’ data. As a result, this is likely to limit the ways in which operators within the region can generate revenue from customer data. Operators in the USA have been more active in the advertising market than European counterparts The table in Figure 1 highlights recent acquisitions by operators in both Europe and the USA.