Assessment of Effects on the Environment July 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

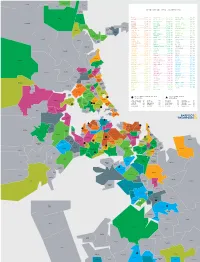

TOP MEDIAN SALE PRICE (OCT19—SEP20) Hatfields Beach

Warkworth Makarau Waiwera Puhoi TOP MEDIAN SALE PRICE (OCT19—SEP20) Hatfields Beach Wainui EPSOM .............. $1,791,000 HILLSBOROUGH ....... $1,100,000 WATTLE DOWNS ......... $856,750 Orewa PONSONBY ........... $1,775,000 ONE TREE HILL ...... $1,100,000 WARKWORTH ............ $852,500 REMUERA ............ $1,730,000 BLOCKHOUSE BAY ..... $1,097,250 BAYVIEW .............. $850,000 Kaukapakapa GLENDOWIE .......... $1,700,000 GLEN INNES ......... $1,082,500 TE ATATŪ SOUTH ....... $850,000 WESTMERE ........... $1,700,000 EAST TĀMAKI ........ $1,080,000 UNSWORTH HEIGHTS ..... $850,000 Red Beach Army Bay PINEHILL ........... $1,694,000 LYNFIELD ........... $1,050,000 TITIRANGI ............ $843,000 KOHIMARAMA ......... $1,645,500 OREWA .............. $1,050,000 MOUNT WELLINGTON ..... $830,000 Tindalls Silverdale Beach SAINT HELIERS ...... $1,640,000 BIRKENHEAD ......... $1,045,500 HENDERSON ............ $828,000 Gulf Harbour DEVONPORT .......... $1,575,000 WAINUI ............. $1,030,000 BIRKDALE ............. $823,694 Matakatia GREY LYNN .......... $1,492,000 MOUNT ROSKILL ...... $1,015,000 STANMORE BAY ......... $817,500 Stanmore Bay MISSION BAY ........ $1,455,000 PAKURANGA .......... $1,010,000 PAPATOETOE ........... $815,000 Manly SCHNAPPER ROCK ..... $1,453,100 TORBAY ............. $1,001,000 MASSEY ............... $795,000 Waitoki Wade HAURAKI ............ $1,450,000 BOTANY DOWNS ....... $1,000,000 CONIFER GROVE ........ $783,500 Stillwater Heads Arkles MAIRANGI BAY ....... $1,450,000 KARAKA ............. $1,000,000 ALBANY ............... $782,000 Bay POINT CHEVALIER .... $1,450,000 OTEHA .............. $1,000,000 GLENDENE ............. $780,000 GREENLANE .......... $1,429,000 ONEHUNGA ............. $999,000 NEW LYNN ............. $780,000 Okura Bush GREENHITHE ......... $1,425,000 PAKURANGA HEIGHTS .... $985,350 TAKANINI ............. $780,000 SANDRINGHAM ........ $1,385,000 HELENSVILLE .......... $985,000 GULF HARBOUR ......... $778,000 TAKAPUNA ........... $1,356,000 SUNNYNOOK ............ $978,000 MĀNGERE ............. -

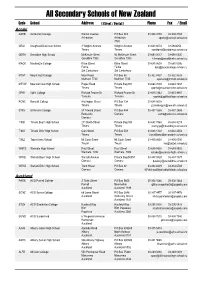

Secondary Schools of New Zealand

All Secondary Schools of New Zealand Code School Address ( Street / Postal ) Phone Fax / Email Aoraki ASHB Ashburton College Walnut Avenue PO Box 204 03-308 4193 03-308 2104 Ashburton Ashburton [email protected] 7740 CRAI Craighead Diocesan School 3 Wrights Avenue Wrights Avenue 03-688 6074 03 6842250 Timaru Timaru [email protected] GERA Geraldine High School McKenzie Street 93 McKenzie Street 03-693 0017 03-693 0020 Geraldine 7930 Geraldine 7930 [email protected] MACK Mackenzie College Kirke Street Kirke Street 03-685 8603 03 685 8296 Fairlie Fairlie [email protected] Sth Canterbury Sth Canterbury MTHT Mount Hutt College Main Road PO Box 58 03-302 8437 03-302 8328 Methven 7730 Methven 7745 [email protected] MTVW Mountainview High School Pages Road Private Bag 907 03-684 7039 03-684 7037 Timaru Timaru [email protected] OPHI Opihi College Richard Pearse Dr Richard Pearse Dr 03-615 7442 03-615 9987 Temuka Temuka [email protected] RONC Roncalli College Wellington Street PO Box 138 03-688 6003 Timaru Timaru [email protected] STKV St Kevin's College 57 Taward Street PO Box 444 03-437 1665 03-437 2469 Redcastle Oamaru [email protected] Oamaru TIMB Timaru Boys' High School 211 North Street Private Bag 903 03-687 7560 03-688 8219 Timaru Timaru [email protected] TIMG Timaru Girls' High School Cain Street PO Box 558 03-688 1122 03-688 4254 Timaru Timaru [email protected] TWIZ Twizel Area School Mt Cook Street Mt Cook Street -

Auckland Council District Plan (Manukau Section) Plan Amendment 88

Minister of Education Notice of Requirement for Flat Bush School 187 Flat Bush School Road Revision History Date Issue Description 28/09/15 1 Draft for review 11/01/16 2 Final draft for client review 15/02/16 3 Final for submission CONTENTS 1.0 THE REQUIRING AUTHORITY AND PROPERTY DETAILS .................................... 1 2.0 INTRODUCTION ................................................................................................ 2 3.0 SITE DESCRIPTION ............................................................................................ 2 3.1 Location ............................................................................................................ 2 3.2 Existing Site ...................................................................................................... 2 3.3 Surrounding Land use ...................................................................................... 3 4.0 NATURE OF THE PROPOSED DESIGNATION ..................................................... 3 4.1 Activity Outline ................................................................................................. 3 4.2 Site Development ............................................................................................. 4 4.3 Buildings ........................................................................................................... 5 4.4 Transport .......................................................................................................... 5 4.5 Outdoor recreation facilities ........................................................................... -

Auckland Metro

5/08/2021 Change in Delivery Partner- Auckland Metro Dear Valued Customer Effective Monday 9th August Auckland Metro deliveries and pick ups will be completed by Mainfreight. Map and Suburb list below for confirmation of affected areas Auckland Metro Ellerslie, Greenlane, Middlemore, Mt Wellington, Mt Wellington, One Tree Hill, Onehunga, Otahuhu, Area 1 Panmure, Penrose, Remuera, Royal Oak, Southdown, Tamaki, Te Papapa. Airport Oaks, Auckland Airport, Balmoral, Blockhouse Bay, Botany Downs, Clover Park, Burswood, Dannemora, East Tamaki, Epsom, Farm Cove, Favona, Flat Bush, Glen Innes, Goodwood Heights, Greenmount, Highbrook, Highland Park, Hillsborough, Lynfield, Mangere, Mangere Bridge, Manukau, Area 2 Meadowbank, Morningside, Mt Albert, Mt Eden, Mt Roskill, Northpark, Otara, Pakuranga, Papatoetoe, Pt England, Remuera, Sandringham, St Johns, St Lukes, Stonefields, Sunnyhills, Three Kings, Totara Heights, Wiri Avondale, Birkenhead, Castor Bay, Chatswood, Clendon, Conifer Grove, Edmonton, Forrest Hill, Glen Eden, Glendene, Glendowie, Glenfield, Green Bay, Hauraki, Half Moon Bay, Highbury, Hillcrest, Howick, Kelston, Area 3 Kohimaramara, Manurewa, Milford, Mission Bay, New Lynn, Northcote, Northcote Point, Orakei, Pt Chevalier, St Heliers, Te Atatu Peninsula, Takanini, Takapuna, Totara Vale, Wairau Valley, Waterview, Wattle Downs, Western Springs, Westmere, Weymouth Albany, Alfriston, Arch Hill, Auckland Central, Bayswater, Bayview, Beach Haven, Belmont, Birkdale, Bucklands Beach, Campbells Bay, Cockle Bay, Eastern Beach, Eden Terrace, Fairview Heights, Freemans Bay, Grafton, Grey Lynn, Henderson, Henderson Valley, Herne Bay, Hobsonville, Kingsland, Mairangi Bay, Area 4 Massey, Murrays Bay, Newmarket, Newton, North Harbour, Papakura, Parnell, Ponsonby, Ranui, Rosedale, Rosehill, Rothesay Bay, Royal Heights, St Marys Bay, Sunnynook, Swanson, Titirangi, West Harbour, Westgate Westhaven Ardmore, Bombay, Browns Bay, Devonport, Drury, Greenhithe, Herald Island, Karaka, Kumeu, Pukekohe, Area 5 Ramarama, Redvale, Torbay . -

View Our Media Kit

Times Media MEDIA KIT We are the readers choice CN 0 CN 0 CN 0 A Awards 202 A Awards 202 A Awards 202 Publishers of SOUTH EAST | FRANKLIN East design Auckland Settling In build App LEVEL 2 IN PICTURES Locals were so keen to get back to some normalcy when we dropped to Level 2 on Thursday. AWARD-WINNING VOICE OF THE COMMUNITY – NZCNA Est. 1972 See page 11. Have your own plans? Tuesday, May 19, 2020 General 09 271 8000 Classified 09 271 8055 Delivery Enquiries 09 271B 8000ring them Website to us.H avewww.times.co.nz your own plans? Vol 49, No 14 Building a home but prefer toB havering your them to us. plan drawn independently? BringBuilding them a home to but prefer to have your us and we will price them forplan you drawn. independently? Bring them to *Conditions apply us and we will price them for you. Come and see us at:*Conditions apply New Display Home open. 146 Eighth ViewOr if it's inspiration Avenue, you are afterNew come Display on Home open. over to Jennian Homes CBDOr & ifEast it's inspiration you are after come on Christopher Luxon Beachlands Auckland’s brand new Displayover Home to Jennian to Homes CBD & East see what this exceptional homeAuckland’s has to brand new Display Home to Botany • REPAIR • DESIGN • VALUE see what this exceptional home has to JH15993 offer - 146 Eighth View Ave, Beachlands.KC14848 P 09 918 9078 | jennian.co.nzoffer - 146 Eighth View Ave, Beachlands. Open: Monday - Sunday, 10am - 4pm P: 0800 628 268 HANDLING YOUR JEWELLERY WITH E [email protected] Open: Monday - Sunday, 10amwww.checkmein.co.nz - 4pm EXPERIENCE AND CARE E: [email protected] Made in Howick FB: @christopherluxon JennianSINCE Homes 1984 CBD & East AucklandJennian Homes CBD & East Auckland• Design & Build 59B Sir William Ave, East Tamaki 59B Sir William Ave, East Tamaki Major Sponsor Major Sponsor 09 534 7404 | 59 Picton Street, Howick • House & land P 09 918 9078 E [email protected] 09 918 9078 E [email protected] Phone 535 2002 Authorised by C. -

Auckland's Urban Form

A brief history of Auckland’s urban form April 2010 A brief history of Auckland’s urban form April 2010 Introduction 3 1840 – 1859: The inaugural years 5 1860 – 1879: Land wars and development of rail lines 7 1880 – 1899: Economic expansion 9 1900 – 1929: Turning into a city 11 1930 – 1949: Emergence of State housing provision 13 1950 – 1969: Major decisions 15 1970 – 1979: Continued outward growth 19 1980 – 1989: Intensifi cation through infi ll housing 21 1990 – 1999: Strategies for growth 22 2000 – 2009: The new millennium 25 Conclusion 26 References and further reading 27 Front cover, top image: North Shore, Auckland (circa 1860s) artist unknown, Auckland Art Gallery Toi o Tamaki, gift of Marshall Seifert, 1991 This report was prepared by the Social and Economic Research and Monitoring team, Auckland Regional Council, April 2010 ISBN 978-1-877540-57-8 2 History of Auckland’s Urban Form Auckland region Built up area 2009 History of Auckland’s Urban Form 3 Introduction This report he main feature of human settlement in the Auckland region has been the development This report outlines the of a substantial urban area (the largest in development of Auckland’s New Zealand) in which approximately 90% urban form, from early colonial Tof the regional population live. This metropolitan area settlement to the modern Auckland is located on and around the central isthmus and metropolis. It attempts to capture occupies around 10% of the regional land mass. Home the context and key relevant to over 1.4 million people, Auckland is a vibrant centre drivers behind the growth in for trade, commerce, culture and employment. -

Commercial Member Directory

Commercial Member Directory Barfoot & Thompson Commercial 34 Shortland Street +64 9 3076300 [email protected] Auckland, 1140 www.barfoot.co.nz Title Name Email Phone # Commercial Referral Coordinator John Urlich [email protected] +64 21395396 Commercial Broker in Charge Peter Thompson [email protected] +64 9 3075523 Certifications Applies Service Tiers Applies ALC Commercial Division/Office BOMA Dedicated Commercial Agent(s) Build-to-suit Resi-Mercial Agent(s) CCIM CPM Lease negotiation SIOR Service Types Applies Network Affiliations Applies Hotel / Resort CBRE CORFAC Industrial CRESA Investment CW/DTZ Land / Agricultural JLL Knight Frank Landlord Rep NAI Leasing Newmark TCN Service Types Applies Logistics Medical Office Multi-Family Office Property Management Retail Tenant Rep City State / Province Country Ahuroa NZL Albany NZL Albany Heights NZL Alfriston NZL Algies Bay NZL Ararimu NZL Ardmore NZL Arkles Bay NZL Army Bay NZL Auckland NZL Avondale NZL Awhitu NZL Bay Of Islands NZL Bay View NZL Bay of Plenty NZL Bayswater NZL Bayview NZL Beach Haven NZL Beachlands NZL Belmont NZL Big Bay NZL Birkdale NZL Birkenhead NZL Birkenhead Point NZL Bland Bay NZL Blockhouse Bay NZL Bombay NZL Botany Downs NZL City State / Province Country Broadwood NZL Brookby NZL Browns Bay NZL Buckland NZL Bucklands Beach NZL Burswood NZL Cable Bay NZL Campbells Bay NZL Canterbury NZL Castor Bay NZL Central Otago NZL Chatswood NZL City Centre NZL Clarks Beach NZL Clendon Park NZL Clevedon NZL Clover Park NZL Coatesville NZL Cockle -

Flat Bush Built Heritage Review

Flat Bush Built Heritage Review Conservation Planning / Building Archaeology / Heritage Studies Reynolds Cyclical Maintenance Planning / Historical Research / Interpretation 13 Gibraltar Crescent, Parnell, Auckland 1052 New Zealand Associates 64 9 379 7321/ 021 02 333 777 e-mail: [email protected] Contents 1.0 Scope of this report 3 2.0 Study methodology 3 3.0 Historical background 5 4.0 Existing built heritage recognition and protection 6 5.0 Appropriateness of existing scheduling 6 5.1.2 Flat Bush School recommendations 7 5.2.2 Murphy Homestead recommendations 8 6.0 Flat Bush built heritage today 8 6.1 Gillard House 8 6.1.4 Gillard House recommendations 12 6.2 Major Bremner‟s Cottage 13 6.2.4 Major Bremner‟s Cottage recommendations 16 Appendix 1: Evaluation criteria from District Plan 17 End notes 19 2 | P a g e 1.0 Scope of this report This report, undertaken by Reynolds & Associates in August 2010, was commissioned by Manukau City Council to revisit the identification and protection of built heritage features located within the boundaries of the Flat Bush Stage 2, Stage 2A and Stage 3 areas. The review involved the assessment of New Zealand Historic Places Trust and Manukau City Council records along with site visits to the study area, to ascertain whether there are any additional built heritage features that should be identified for protection in the District Plan. In addition, existing identified built heritage features in the District Plan were reviewed with a view to confirming whether their continued protection was warranted. Recommendations are made on potential changes to the District Plan. -

Auckland District Plan

Chapter 17.10 Flat Bush Page 1 17.10 Flat Bush [AM50][AM167] 17.10.1 Introduction The Flat Bush area covers approximately 1730 hectares of land adjacent to the southern boundary of the Auckland Regional metropolitan urban limits. Manukau City Council has identified the area as suitable for a mixture of urban and semi-urban development. As part of Council's responsibilities to promote sustainable management of the area, the likely effects of urban development have been examined. To assess and manage these effects in an integrated manner 'integrated catchment' based planning approach is considered necessary. As a result the Flat Bush area covers a larger area than the original 'Future Urban Development' zone. [AM49] Consultation with the community and stakeholder workshops resulted in adoption of a development concept for the area in 1999. This provides the basis for the provisions contained in this section. The zonings and plan provisions for Flat Bush are not inconsistent with the Auckland Regional Policy Statement and reflect the policy position of the Manukau City Council and the outcomes of the Auckland Regional Growth Strategy. These promote greater opportunities for more intensive building styles, along with greater attention to environmentally sound urban development approaches. The Flat Bush area is bounded in the north by Browns Lane. Its western extent is defined by Te Irirangi Drive. The southern boundary of this area is generally defined by Redoubt Road. The eastern extent is defined by the continuation of Redoubt Road which follows the top of the catchment and is proposed to be extended to join with Ormiston Road. -

AT MCC Policy Vol1 Leisurea

Leisure and Recreation 3.0 3 Leisure and Recreation What you’ve said so far: “One of the key aspects of future planning must be the facilities provided to the local community and particularly the youth. The need to provide facilities for leisure and creative activities have outstripped supply and leave many youth with nothing to do and nowhere to go.” What we do Contribution to community outcomes It’s important to our communities that they have The diagram below shows how this group of activities the facilities to be able to take part in leisure and contributes to the Tomorrow’s Manukau community outcomes. See also page 10 of this volume. recreation activity, as well as having access to educational resources and services. EDUCATED & KNOWLEDGABLE PEOPLE We provide libraries throughout the city so that people have HEALTHY PEOPLE access to a wide range of learning, literacy, information and MOVING MANUKAU SAFE COMMUNITIES leisure services and resources through books and the internet. SUSTAINABLE ENVIRONMENT & HERITAGE Manukau Libraries also has a substantial documentary THRIVING ECONOMY heritage and history collection that’s available to the public. VIBRANT & STRONG COMMUNITY Parks, funded from reserve contributions and cash from subdivisions and developments, are also important for recreation and for our natural environment. Manukau has KEY CONTRIBUTIONS around 900 reserves, sports parks and civic areas, as well as streetscapes which all help make Manukau an attractive Primary place to live and work. These parks and reserves range from Secondary neighbourhood parks to coastal and riparian reserves and heritage sites. While they’re important for leisure, events and relaxation, they’re also home for plants and animals important to our environment. -

This Is the Story of Tupu - the Dawson Road Youth Library

1 World Library and Information Congress: 69th IFLA General Conference and Council 1-9 August 2003, Berlin Code Number: 200-E Meeting: 154. Asia and Oceania & Public Libraries Simultaneous Interpretation: - Tupu - Promoting ‘New Growth’ through Innovative Resources and Services to Youth Daniel G. Dorner Victoria University of Wellington Wellington, New Zealand Introduction This is the story of Tupu - the Dawson Road Youth Library. Tupu is located on Dawson Road in the Clover Park area of Otara in Manukau City, which is one of six municipalities that form New Zealand’s largest city, Auckland. Otara is the poorest part of Auckland, and indeed, is most likely the poorest urban area in all of New Zealand. Today I am going to talk with you about the innovative resources and services offered at Tupu to the youth of Clover Park, and more importantly, about how and why those services came to be. The data that support this paper were gathered through interviews with many of the key people involved in creating Tupu, during a five-month period around the time of its official opening on 1 August 2001. These key people included the mayor of Manukau City, two Manukau City Councillors who were representing the people of Otara and were the main political proponents for the creation of Tupu, local primary and secondary school teachers, community gatekeepers such as the minister of the Samoan Church located right next door to the library, teachers from local schools, families in the Clover Park area of Otara, and the Manukau City library staff who helped create and staff Tupu. -

Residents' Perceptions Towards Asbestos Contamination of Land And

RESIDENTS’ PERCEPTIONS TOWARDS ASBESTOS CONTAMINATION OF LAND AND IT’S IMPACT ON RESIDENTIAL PROPERTY VALUES SANDY BOND University of Auckland and DAVID COOK CB Richard Ellis, New Zealand ABSTRACT Contaminated land issues have become more contentious with the introduction of environmental legislation in many western countries and the subsequent rise in the number of damage claims from land contamination that often result in litigation. This paper summarises the results of a study that focuses on residents’ perceptions towards a specific type of land contamination: asbestos contamination. In particular, the study investigates the attitudes and reactions of property owners living in a case study neighbourhood towards living on or near asbestos- contaminated land and how this might impact on property values. The results will be of particular interest to affected landowners, local authorities that have jurisdiction over the land, and valuers where compensation claims are being made against such property. Keywords: Site contamination, asbestos, stigma, property values, public opinion surveys. INTRODUCTION Contaminated land1 that represents potential hazards to human health and safety may cause property values to diminish due to the existence of "widespread public fear" and "widespread public perceptions of hazards". In relation to asbestos, opposition has arisen from property owners affected by proximity to soil 1 The term "contaminated land" as used in this paper is defined as "a site at which hazardous substances occur at concentrations above background concentrations and where assessment indicates it poses, or is likely to pose, an immediate or long-term risk to human health or the environment", (ANZECC, 1992). This definition has been widely adopted in New Zealand.