Franklin First Ticknor Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

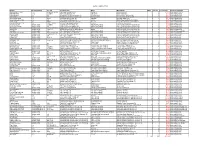

Seafood Violations 2010.Xls Product Declared Quantity Lot Code

Seafood violations 2010.xls Product Declared quantity Lot code Location Found Brand Mfg/packager MAV's Lot size Lot cost error Reason for Rejection Sea Scallops (10-20ct) 12 oz sell by Nov 20/2010 Aldi Foods; Fond du Lac, WI Sea Queen Aldi Inc- Batavia, IL 12 12 ($16.78) short weight/12 MAV's Mahi Mahi fillets 16 oz 8/13/2010 Aldi Foods; Watertown, WI Sea Queen Aldi Inc- Batavia, IL 2 10 ($1.10) short weight/2 MAV's Catfish Nuggets 2 lb N/A Woodmans Food Market; Onalaska, WI Americas Catch Americas Catch- Itta Bena, MS 2 2 ($0.74) short weight/2 MAV's Catfish Fillets 2 lb N/A Woodmans Food Market; Onalaska, WI Americas Catch Americas Catch- Itta Bena, MS 1 2 ($0.73) short weight/1 MAV Sea Scallops 20/30 1 lb 8199 ? Econofood; Sturgeon Bay, WI Aqua Star Aqua Star- Seattle, WA 4 9 ($3.19) short weight/4 MAV's Snow Crab Legs & Claws 2 lb N/A Pick n Save; Fort Atkinson, WI Luxury Atlantic Queen Seafoods- NL Canada 2 2 ($1.76) short weight/2 MAV's Whole Tilapia 3 lb 39989 Wal-Mart Stores East; Janesville, WI Sea Best Beaver Street Fisheries- Jacksonville, FL 2 2 ($0.84) short weight/2 MAV's Uncooked Shrimp 8/12 ct 2 lb 690891, 690881 Fox Bros Piggly Wiggly- Hartland CenSea CenSea, Inc- Northfield IL 2 11 ($4.35) short weight/2 MAV's Frozen Cod Loins Random weight 12102010 Copps Food Center; Anitgo, WI Natures Best Seafood Custom Seafood Packers- Waukesha, WI 4 5 ($2.90) short weight/4 MAV's Jumbo Sea Scallops Random weight N/A Copps Food Center; Appleton, WI Natures Best Seafood Custom Seafood Packers- Waukesha, WI 6 12 ($6.12) short weight/6 MAV's Frozen Cod Random weight sell by Dec22, 10 Copps Food Center; Wis. -

Reg Test 5-14-GCCE.Xlsx

J.P. WIGGINS 3GTMS SHELTON CT CLAUDIO FIAONI 3GTMS SHELTON CT CHUCK FUERST 3GTMS SHELTON CT DEANNA SEGRAVE-DALY A TEASPOON OF SPICE WASHINGTON DC JOSH GRAY A&B PACKING EQUIPMENT LAWRENCE MI MICHAEL WILLIAMSON A&B PACKING EQUIPMENT LAWRENCE MI MONIQUE BUSHEE A&B PACKING EQUIPMENT LAWRENCE MI TRACY DUDA CHAPMAN A. DUDA & SONS, INC. OVIEDO FL ANITA GRACE ABASTO WINSTON SALEM NC GUS CALABRO ABASTO WINSTON SALEM NC DANIEL THULLEN AC FOODS DINUBA CA JENNIFER HORTON ACADEMY OF NUTRITION & DIETETICS CHICAGO IL JEFF HOWARD ADVANCE STORAGE PRODUCTS HUNTINGTON BEACH CA JEFF BECKER ADVANCE STORAGE PRODUCTS HUNTINGTON BEACH CA KEVIN DARBY ADVANCE STORAGE PRODUCTS HUNTINGTON BEACH CA JOSH ROUSE ADVANCE STORAGE PRODUCTS HUNTINGTON BEACH CA GAIL KELSO ADVANCE STORAGE PRODUCTS HUNTINGTON BEACH CA ANDY SHOEMAKER AG1 SOURCE GREENVILLE SC JOSE CRUZ AGRICOLA LOS GIRASOLES SANTIAGO CHILE JOSE CRUZ JR AGRICOLA LOS GIRASOLES SANTIAGO CHILE ALISON BOSSIO AGRILYST BROOKLYN NY CHRISTINA COLLINS AGRILYST BROOKLYN NY MICHAEL DAFLOS AGRILYST BROOKLYN NY ALLISON KOPF AGRILYST BROOKLYN NY JIM MOYER AGRILYST BROOKLYN NY JON SCHMITZ AGRILYST BROOKLYN NY KEVIN FRYE AGROFRESH PHILADELPHIA PA BILL LUCAS AGROFRESH PHILADELPHIA PA NARCISO VIVOT AGROFRESH PHILADELPHIA PA AMBER FOSTER AGROFRESH COLLEGEVILLE PA JUAN DUQUE AGROPECUARIA DUQUE BOTERO MEDELLIN COLOMBIA GUILLERMO DUQUE AGROPECUARIA DUQUE BOTERO MEDELLIN COLOMBIA DJIMY ANTOINE AGRO-VISION PORT-AU-PRINCE HAITI JEAN A THIERRY BOZILE AGRO-VISION PORT-AU-PRINCE HAITI CLARENS TRIBIE AGRO-VISION PORT-AU-PRINCE HAITI RANDY -

United Fresh Names 25 Retail Produce Manager Award Honorees

- Advertisement - United Fresh names 25 Retail Produce Manager Award honorees March 21, 2019 Marking 15 years of recognizing exceptional retail produce managers, United Fresh Produce Association announced the honorees of its 2019 Retail Produce Manager Awards program. The group of 25 produce managers represents supermarket banners, commissaries and independent retail stores from 16 different states and two Canadian provinces. The winners will be honored guests at the United Fresh 2019 convention, June 10-12 in Chicago. Sponsored by Dole Food Co., the program pays special recognition to produce managers working every day on the front line to increase sales and consumption of fresh fruits and vegetables. Since 1 / 3 the program’s inception in 2005, over 325 retail produce managers, representing more than 110 different retail banners, have been honored for their contributions to the industry. “Produce managers are the face of our industry to the consumer. Their creative merchandising and positive approach to customer service directly correlates to the growth of sales and ultimately consumption of fresh fruits and vegetables,” said Tom Stenzel, United Fresh president and chief executive officer. “We are grateful to Dole for once again sponsoring this program and for their partnership in recognizing these 25 deserving honorees. I look forward to celebrating our winners this June in Chicago” The 2019 Retail Produce Manager Award Winners are: Vincente Aguirre, Fort Bliss Commissary, El Paso, TX Gregory Barnufsky Jr., Yokes Fresh Markets, Spokane, WA Mike Burdi, Metro Ontario Inc., Toronto Jerry Clark II, The Fresh Market, Roanoke, VA Cassandra Crone, North State Grocery Inc., Auburn, CA Bobby David, Audubon Market, St. -

How Retailers Promote Pet Food & Pet Care

The Changing Landscape of Retail & Consumer Promotions Tom Pirovano March 15, 2011 1 Welcome! 2 Topics Covered • What’s What – The State of Retail Promotions Today • What’s New and What’s Next – Game-Changing Trends & Technology – Future Retailing & Promotion Opportunities 3 The State of Retail Promotions Today 4 Major Supermarkets Running More Ad Circulars in 2010 2009 2010 Count Retailer Circulars Circulars Change Safeway (Multiple Banners) 59 87 +28 Carr’s, Dominick’s, Genuardi’s, Randall’s, Tom Thumb, Vons, Pavilions Jewel-Osco 87 102 +15 King Soopers / City Market 52 64 +12 Publix 51 58 +7 Quality Food Centers 48 54 +6 Fresh & Easy 45 51 +6 Save-A-Lot 20 26 +6 Source: ECRM-MarketGate Ad Comparisons, Calendar 2010 5 Other Major Retailers Running Outside the Traditional More Ad Circulars in 2010 Grocery Channel 2009 2010 Count Retailer Circulars Circulars Change JC Penney 54 82 +28 Sears 47 70 +23 Family Dollar 25 44 +19 Home Depot 42 59 +17 Dollar General 18 30 +12 OfficeMax 34 39 +5 Walgreens 57 60 +3 Walmart-US 38 41 +3 Toys - R - Us 39 42 +3 Target Stores 52 54 +2 Source: ECRM-MarketGate Ad Comparisons, Calendar 2010 6 Very Few CPG Retailers Are Running Fewer Ad Circulars 2009 2010 Chg In Retailer Circulars Circulars Circulars Sentry Foods 52 49 -3 Kmart 66 64 -2 Copps 52 50 -2 Farm Fresh 52 50 -2 Big Lots 33 31 -2 Source: ECRM-MarketGate Ad Comparisons, Calendar 2010 7 Squeezing More Ads into Fewer Circulars 2010 Chg In Chg In Retailer Circulars Circulars Ad Blocks Sentry Foods 49 -3 +4,845 Kmart 64 -2 -567 Copps 50 -2 +3,217 Farm Fresh 50 -2 +2,896 Big Lots 31 -2 +253 Source: ECRM-MarketGate Ad Comparisons, Calendar 2010 8 Most leading retailers ran more ad blocks in 2010 than in 2009 Increased 2010 Ad Blocks Vs. -

Feature Advertising by U.S. Supermarkets Meat and Poultry

United States Department of Agriculture Agricultural Feature Advertising by U.S. Supermarkets Marketing Service Meat and Poultry Livestock, Poultry and Seed Program Independence Day 2017 Agricultural Analytics Division Advertised Prices effective through July 04, 2017 Feature Advertising by U.S. Supermarkets During Key Seasonal Marketing Events This report provides a detailed breakdown of supermarket featuring of popular meat and poultry products for the Independence Day marketing period. The Independence Day weekend marks the high watershed of the summer outdoor cooking season and is a significant demand period for a variety of meat cuts for outdoor grilling and entertaining. Advertised sale prices are shown by region, state, and supermarket banner and include brand names, prices, and any special conditions. Contents: Chicken - Regular and value packs of boneless/skinless (b/s) breasts; b/s thighs; split, bone-in breasts; wings; bone-in thighs and drumsticks; tray and bagged leg quarters; IQF breast and tenders; 8-piece fried chicken. Northeast .................................................................................................................................................................. 03 Southeast ................................................................................................................................................................. 21 Midwest ................................................................................................................................................................... -

1 Appleton/Fox Cities Area Collection Sites: A

“Help for the Homeless” Collection Sites 2019: In alphabetical order, by community. 83 crisis agencies in 15 communities receivedBadger Sportsdonations Park of new personal hygiene and cleaning items. Thanks to all of the following businesses, churches, and schools for placing (NOTE: Participating schools collection boxes in high traffic areas and promoting the drive! are encouraged to keep donations for their own “Care Closets” for students in need.) Baker Tilly Virchow Krause, LLP Appleton/Fox Cities Area Collection Sites: Bank of Kaukauna (the) A to Z Machine Co Bemis Appleton AASD (Appleton Area School District) : Appleton East Bemis Graphics HS Key Club BNA (Curwood) AASD: Appleton Area School Dist Community Early Boldt Company (The) Learning Cntr Calvary Bible Church AASD: Appleton North High School Key club PEERS Calvary Chapel of Appleton AASD: Appleton West HS - Key Club Catalpa – 2 locations AASD: Classical Charter School of Appleton Century 21 Affiliated First Realty AASD: Columbus Elementary School Christ the King AASD: Foster Charter Elementary School Christ the Rock AASD: Highlands Elementary School Christus Lutheran AASD: Horizons Elementary School Church of Christ AASD: Huntley Elementary CLA AASD: Janet Berry Elementary Clearwater Paper AASD: Johnston Elementary School CMD Corporation AASD: Lincoln Elementary School Community Church of Appleton AASD: Morgan Building Culver’s Darboy AASD: Wilson/Magellan Middle school Culver’s Little Chute Acre Realty Culver's Neenah Alliance Industries Cypress Benefits – 2 locations Alta Resources Fulfillment Center DoubleTree by Hilton Neenah Alta Resources Main Office East Wisconsin Savings Bank Amaze and Grace Emmanuel Lutheran Church Ansay and Associates Empower Yoga Apostolic Truth Church Essity Apple Valley Church Evergreen Credit Union Appleton Airport Faith Christian Church Appleton Alliance Church Faith Church Appleton Boys and Girls Club admin offices Faith Community Church UMC Greenville Appleton Community Evangelical Free Church Faith Lutheran – 2 locations Appleton Downtown Inc. -

Grocery Stores

GROCERY STORES Beloit Location Website/App Assistance Misc. Website: aldi.us App: ALDI & InstaCart Electric Scooters: N/A Aldi Order on app: Yes In-store shopping Wheelchairs: N/A 2780 Milwaukee Rd. Order online: Yes assistance: N/A Payments accepted: (855) 955-2534 Phone order: N/A Home delivery: Yes Debit, Credit, EBT, Hours: 9am-8pm Fee: First three orders Drive-up service: Yes Apple Pay, Google Pay over $35 are free Tipping Minimum purchase: N/A Recommended: No Website: Kauffman’s kauffmansstore.com Electric Scooters: N/A Country Store App: N/A In-store shopping Wheelchairs: N/A 9550 WI-81 Order on app: N/A assistance: Yes Payments accepted: (608) 362-1750 Order online: N/A Home delivery Debit, Credit, Checks Hours: 8:30am- Phone order: Yes available: N/A Tipping 5:30pm, Closed Fee: N/A Drive-up service: N/A Recommended: No Sundays Minimum purchase: N/A Website: Electric Scooters: N/A shopthepig.com Wheelchairs: N/A Piggly Wiggly App: N/A In-store shopping Payments accepted: 1827 Prairie Ave. Order on app: N/A assistance: N/A Debit, Credit, EBT (608) 362-1950 Order online: N/A Home delivery Tipping Hours: 7am-9pm Phone order: N/A available: N/A Recommended: No Fee: N/A Drive-up service: N/A Minimum purchase: N/A Website: walmart.com Electric Scooters: Yes In-store shopping App: Walmart Wheelchairs: Yes Walmart assistance: Yes Order on app: Yes Payments accepted: 2785 Milwaukee Rd. Home delivery Order online: Yes Debit, Credit, EBT (608) 362-0057 available: Yes, min. Phone order: Yes Tipping Hours: 24 Hours $40 Fee: N/A Recommended: No Drive-up service: N/A Minimum purchase: $40 Website: woodmans- Electric Scooters: Yes food.com In-store shopping Wheelchairs: Yes Woodman’s App: Shop Woodman’s assistance: Yes Payments accepted: 1877 S. -

Hartford Plaza News

Green Bay Wisconsin TUESDAY December 10, 2019 Packers keep National $1 finding ways Guard leader to win 1B resigns 5A DAILY NEWS A Trusted News Source Since 1855 One person dead, four hurt in I-41 crash Police Department news release, lanes and several vehicles had The news release said evidence around 10:22 p.m., the department crashed. and witness reports stated that a Incident occurred Sunday night received several calls reporting a When first responders arrived, Subaru SUV had been driven on GERMANTOWN — An 18-year- ing a wrong-way driver on Inter- crash on northbound I-41 south, of they found a three-vehicle crash the wrong side of the divided old female died and four others state 41 just south of Holy Hill Holy Hill Road. Callers told with one vehicle burning. Several highway by a 20-year-old man from were seriously hurt in a three- Road. authorities that a vehicle was trav- passing motorists stopped and vehicle crash Sunday night involv- According to a Germantown eling south in the northbound helped put out the fire. See CRASH, PAGE 8A RAISING THE ROOF TRUSS WEST BEND SCHOOL DISTRICT Board far from deciding about consolidating high schools Is ‘still very much in the information-gathering stage,’ says Fischer By Brianna Vogel [email protected] 262-306-5046 WEST BEND — While the Board of Education has mentioned the future possibility of consolidat- ing the district’s high schools, any determination is far in the future. They are, however, discussing changing the current policy as it pertains to merg- ing the two and some much-needed work in the 50- year-old buildings. -

Retail Consignees for Fsis Recall 094-2019

USDA United States Department of iiiiiiii Ag riculture Food Safety and Inspection Service RETAIL CONSIGNEES FOR FSIS RECALL 094-2019 FSIS has reason to believe that the following retail location(s) received ready-to-eat (RTE) poultry products that have been recalled by Tip Top Poultry, Inc, a Rockmart, Ga., establishment. This list may not include all retail locations that have received the recalled product or may include retail locations that did not actually receive the recalled product. Therefore, it is important that you use the product-specific identification information, available at https://www.fsis.usda.gov/wps/portal/fsis/topics/recalls-and-public-health-alerts/recall-case-archive/archive/2019/recall- 094-2019-release in addition to this list of retail stores, to check meat or poultry products in your possession to see if they have been recalled. Store list begins on next page. United States Food Safety D ep art:m ent of And Inspection ::a.. Ag1:i cul nu· e Service Retail List for Recall Number: 094-2019 RTE Chicken Products List Current As Of: 10-Dec-19 Nationwide, State-Wide, or Area-Wide Distribution Retailer Name Location All locatons in AZ, CA, CO, IL, ME, OR, PA, TX, UT, 1 Albertsons WA All locations in IL, PA, NJ, DE, TX, OK, IA, ND, MN, WI, SD, VA,WV, MD, IN, KY, FL, OH, GA, SC, AL, TN, 2 ALDI MS,MO, NE, AR, KS, NC, NY, VT, MA, RI, CT, NH, MI, CA, 3 AM/PM All locations in NV 4 Applegreen's Midwest All locations in WI, MN 5 Aramark All locations in VA,NC,GA,CA 6 Baker's All locations in NE 7 Big Lots All locations in AL, -

WGA Honorees List 2019

Excellence in Operations PAST RECIPIENTS 2019 Jeff McClure, UNFI (retired); Francis Kranz, Zinke’s Village Market, Wisconsin Dells; Doug Rinehart, Dick’s Fresh Market; Jason Nilssen, Nilssen’s Supervalu, Baldwin; Jason Stingl, Festival Foods; Mike Ptacek, Ptacek’s IGA, Prescott; Dave Tadych, Tadych’s Econofoods; Steve “Red” Salfai, Red’s Piggly Wiggly, Omro Don Theisen, Trig’s 2010 Bonnell Family, Dave’s County Market, Merrill; 2018 Greg, Kari & Nick Hansen , Hansen’s IGA; Steve Heise, T.A. Solberg, Rhinelander; Paul Godin , Godin’s Piggly Wiggly; Doug Niemuth, Thorp Supervalu; Tim Plevak , Trig’s, Wausau Lee Mylener, Lee’s Family Foods, Peshtigo 2017 Candie Baker, Webster's Marketplace; 2009 Alan Alden Steve Burkhardt, Skogen’s Festival Foods; , T.A. Solberg, Wausau; Brian Conrad Jason Nilssen, Nilssen’s Foods; , Lake Mills Sentry Foods, Jason Fritsche Brett & JoDee Rechek, Rechek’s Food Pride , Quality Foods, Wausau; Frank & Stephanie Lueptow, Frank’s Piggly Wiggly, Elkhorn; 2016 Michelle Harrington & Kerry Jeanpierre, Albrecht’s Delafield Randy Munns, Festival Foods, Green Bay; Market; Pat Barnes, Fox Brothers Piggly Wiggly Alex Zamarripa, Burnstad’s, Tomah 2015 Ann Garthwait, Lake Mills Sentry; Sue and Steve Jungwirth, Red's Piggly Wiggly; 2008 Karen & Dennis Wautlet, Denny’s SuperValu, Algoma; Carl Miller, Miller & Sons; Glenn Palmquist, Richter’s Markets, Twin Lakes; Jerry and Pat Mountin, Mountin’s Piggly Wiggly Nate Pederson, Sun Prairie Sentry, Sun Prairie; Mike Geidel, Geidel’s Piggly Wiggly, Kewaskum 2014 Bob Fleming, Meadow-brook/Fox Run Sentry; Bud & Frances Miller, Miller’s General Store, Lyndon Station; 2007 Ken Riley, Daniels Sentry Food Store, Janesville; Jeff & David Schafer, Gordy’s County Market, Chippewa Falls; Mark Stellpflug, Stell’s Piggly Wiggly, New Holstein; David Spiegelhoff, Gooseberries Fresh Food Market, Burlington; Dick & Ted Stodola, Stodola’s IGA, Luxemburg; Jeff Tate, Watertown Piggly Wiggly Mary & Bruce Weber, St. -

United Fresh Names 25 Retail Produce Manager Award Honorees 2019 Marks 15 Years of Honoring Outstanding Retail Produce Managers

NEWS RELEASE For Immediate Release, March 18, 2019 Contact: Mary Coppola [email protected] 202-303-3425 United Fresh Names 25 Retail Produce Manager Award Honorees 2019 Marks 15 Years of Honoring Outstanding Retail Produce Managers WASHINGTON, D.C. (March 18, 2019) – Marking 15 years of recognizing exceptional retail produce managers, United Fresh Produce Association announced the honorees of its 2019 Retail Produce Manager Awards Program. The group of 25 produce managers represents supermarket banners, commissaries and independent retail stores from 16 different states and two Canadian provinces. The winners will be honored guests at the United Fresh 2019 convention, June 10-12 in Chicago. Sponsored by Dole Food Company, the program pays special recognition to produce managers working every day on the front line to increase sales and consumption of fresh fruits and vegetables. Since the program’s inception in 2005, over 325 retail produce managers, representing more than 110 different retail banners, have been honored for their contributions to the industry. “Produce managers are the face of our industry to the consumer. Their creative merchandising and positive approach to customer service directly correlates to the growth of sales and ultimately consumption of fresh fruits and vegetables,” said United Fresh President & CEO Tom Stenzel. “We are grateful to Dole for once again sponsoring this program and for their partnership in recognizing these 25 deserving honorees. I look forward to celebrating our winners this June in Chicago” The 2019 Retail Produce Manager Award Winners are: • Vincente Aguirre, Fort Bliss Commissary, El Paso, TX • Gregory Barnufsky Jr., Yokes Fresh Markets, Spokane, WA • MiKe Burdi, Metro Ontario Inc., Toronto, ON, Canada • Jerry Clark II, The Fresh Market, Roanoke, VA • Cassandra Crone, North State Grocery, Inc., Auburn, CA • Bobby David, Audubon Market, St. -

Retail Consignees for Fsis Recall 077-2017

RETAIL CONSIGNEES FOR FSIS RECALL 077-2017 FSIS has reason to believe that the following retail location(s) received breaded chicken products that have been recalled by Maxi Canada, Inc. This list may not include all retail locations that have received the recalled product or may include retail locations that did not actually receive the recalled product. Therefore, it is important that you use the product-specific identification information, available at http://www.fsis.usda.gov/wps/portal/fsis/topics/recalls-and-public-health-alerts/recall-case-archive/archive/2017/recall-077-2017-release in addition to this list of retail stores, to check meat or poultry products in your possession to see if they have been recalled. Store list begins on next page. Retail List for Recall Number: 077-2017 (Breaded Chicken Products) List Current As Of: 13-Jul-17 Nationwide, State-Wide, or Area-Wide Distribution Retailer Name Location 1 ACME Locations in DE, NJ, NY and PA 2 Big Y Locations in CT and MA Locations in FL, MA, NC, NJ, NY, OH, PA, RI, SC 3 BJ's Wholesale and VA 4 Brookshire Brothers Locations in TX 5 Cashwise Locations in MN and ND 6 City Market Locations in CO 7 Coborn's Locations in MN and SD 8 C-Town Locations in NY 9 Cub Meat Locations in MN 10 D&W Fresh Market Locations in MI 11 Dave's Marketplace Locations in RI 12 Family Fare Locations in MI 13 Festival Foods Locations in WI 14 Fine Fare Locations in NY 15 Food Bazaar Locations in CT, NJ, and NY 16 Food City Locations in TN and VA 17 Food4Less Locations in CA 18 Foodsco Locations in