2. Premium Airline Model – Status Quo and Characteristics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

No. Title First Name Last Name Organisation Job Title 1 Mr. Ramah Ettir Afriqiyah Airways CEO Organizations and International Relations 2 Mr

AFRAA MEMBERS No. Title First Name Last Name Organisation Job Title 1 Mr. Ramah Ettir Afriqiyah Airways CEO Organizations and International Relations 2 Mr. Mohamed Elmeshkhi Afriqiyah Airways Manager 3 Mr. Tamzali Hassen AIR ALGERIE Directeur des Accords 4 Mr. Djeraba Ali AIR ALGERIE Cadre Dirigeant BRIGARDIER ALBERTUS 5 Mr. THOMAS SCHEFFERS AIR BOTSWANA BOARD MEMBER 6 Mr. SERGIO ROSA AIR BURKINA CEO 7 Mr. Mohamed Ghelala Air Burkina consultant 8 Mr. MAMADY SANOH AIR BURKINA CHAIRMAN 9 Mr. HUGUES RATSIFERANA AIR MADAGASCAR CHIEF EXECUTIVE MANAGER 10 Mrs. DOMINIQUE ANDRIANTSOA AIR MADAGASCAR ALLIANCES / PLANNING DIRECTOR 11 Mr. Abderahmane BERTHE AIR MALI Chief Executive Officer 12 Mr. LASSANA TRAORE AIR MALI CHAIRMAN 13 Mr. El Moctac KONE AIR MALI Communication and Marketing Manager 14 Mr. Praveslall (Pravesh) Tarachand Air Mauritius Ltd Manager Corporate Development-Office CEO 15 Ms. Theopoltina Namases Air Namibia Acting Managing Director 16 Mr. KINFE KAHSSAYE FEKADU AIRNIGERIA CEO 17 Mr. Innocent Mavhunga Air Zimbabwe Acting Group Cheif Executive Officer 18 Mr. BUSERA AWEL BAGI ASKY AIRLINES CHIEF EXECUTIVE OFFICER 19 Mr. KOFFI GERVAIS GBONDJIDE DJONDO ASKY AIRLINES PRESIDENT DU CONSEIL D'ADMINISTRATION 20 Mr Kawashi Kpornu Mawuli Fly Asky 21 Mr. Santiago NSOBEYA EFUMAN NCHAMA CEIBA INTERCONTINENTAL Chief Executive Officer 22 Miss Stella Marie AHO CEIBA INTERCONTINENTAL International Affairs Manager 23 Mr. Hussein Massoud EgyptAir Chairman & CEO 24 Mr. Mohamed Soliman EgyptAir V.P. Alliances & Int\'l Relations 25 Mrs. Nervin Magdi EgyptAir Regional Associations Affairs manager 26 Mr. Tewolde GebreMariam Ethiopian Airlines CEO 27 Mr. Henok Teferra Shawl Ethiopian Airlines Director Corporate Strategy & Government Affairs 28 Mr. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Airline Business & Law: Aircraft Acquisition, Finance & Leasing

Airline Business & Law: Aircraft Acquisition, Finance & Leasing Airline Business & Law (ASPL 614) McGill Institute of Air & Space Law Mark Lessard Pillsbury Winthrop Shaw Pittman LLP Table of Contents 1. Introduction: Aircraft as Investments 2. The Principal Players a. Aircraft Operators b. The Metal-Heads c. Sources of Finance 3. Aircraft Acquisition Process a. Selecting Equipment b. OEM Aircraft Purchase Agreements c. Pre-Delivery Payments and Financing d. Secondary Market 4. The Aircraft Leasing Industry a. Operating Leasing vs. Finance Leasing b. Asset Risk Arbitrage vs. Credit Arbitrage c. Depreciation Table of Contents 5. Aircraft Financing Methods a. Airline Credit vs. Asset Values b. Commercial Bank Lending c. Export Credit Agencies d. Capital Markets 6. Legal and Contractual Protections a. Perfecting Security in Aircraft b. Operation, Maintenance and Return Conditions c. Insurance 7. Default and Remedies a. Lease and Loan Defaults b. Airline Bankruptcies c. Foreclosure and Repossession d. Transition and Deficiency 8. Conclusion: Risk and Reward Introduction: Aircraft as Investments Q: What is the surest way to become a millionaire? A: Become a billionaire and start an airline… - Richard Branson Introduction: 10 Reasons for Investor Caution 1. Danger and liability = highly regulated industry (SAFETY!) 2. Variable operating costs, mainly driven by fuel and personnel 3. Highly mobile, crossing national borders and subject to expropriation 4. Expensive to maintain even when not in use 5. Value dependent on maintenance status, variant, upgrades, engine type, operating conditions, line number etc… 6. Highl y cycli cal i nd ust ry (GDP growth necessary b u t not suffi c ien t) 7. Long-dated asset (30 + years) 8. -

An Introduction to DOT Form 41 Web Resources for Airline Financial Analysis

An Introduction to DOT Form 41 Web Resources for Airline Financial Analysis Joan Combs Durso, Ph.D. Assistant Professor of Finance Rubel School of Business Bellarmine University 2001 Newburg Road Louisville, KY 40205 Phone: 502-452-8471 Fax: 502-452-8013 Email: [email protected] Up to date as of: December 30, 2007 1 INTRODUCTION .......................................................................................................................... 3 FORM 41 DATA USE IN FINANCE............................................................................................ 4 GETTING STARTED WITH TRANSTATS................................................................................. 5 Preliminary Advice ................................................................................................................. 5 Aviation Support Tables .........................................................................................................6 Aircraft Types ......................................................................................................................... 7 Carrier Decode Table.............................................................................................................. 8 Master Coordinate Table....................................................................................................... 10 FORM 41 FINANCIAL REPORTS ............................................................................................. 10 FORM 41 TRAFFIC STATISTICS ............................................................................................ -

Dubai Airshow Aspires to Be the Biggest International Event

11-15th Nov. 2007, Airport Expo. Dubai United Arab Emirates The SHOW DAILY is Published by SAP MEDIA WORLDWIDE LTD. DAY ONE SUNDAY, 11th NOV. 2007 FROM THE PUBLISHERS OF INTERNATIONAL AEROSPACE TODAy’s pro- GRAMME Dubai Airshow Aspires To Be Sunday, 11th November 2007 The Biggest International Event Room A 09.00am Dubai 2007 official opening he 10th edition of the at Royal Pavilion Dubai Airshow, is com- 10.00am Press conference Lockheed Tpletely sold out, and has Martin at Press Conf. Room broken all the international Mezzanine Floor East Hall event’s previous records of 11.00am Press conference DAE Press size, exhibitor and aircraft Conf. Room at Mezzanine numbers and aircraft displayed Floor East Hall as it readies for its final show- 12.00nn Press conference BOEING ing at the Airport Expo Dubai. at Press Conf. Room Mez The largest ever Dubai Airshow zanine Floor East Hall is a barometer for huge Middle 01.00pm Press conference Lockheed East Aviation growth, says HH Martin at Press Conf. Room Sheikh Ahmed. The growth is in Mezzanine Floor East Hall tandem with its 2009 move to 02.00pm Press conference BOEING a new, purpose-built facility at at Press Conf. Room Mez Dubai World Central, the huge His Highness Sheikh Ahmed Bin Saeed Al Maktoum, President, Dubai Civil Aviation zanine Floor East Hall urban aviation community being Authority (DCAA), and Chairman of Dubai Airports at the press conference. 03.00pm Press conference Airbus at built in Jebel Ali, 30 kilometres Press Conf. Room Mezzanine north of Dubai city centre. -

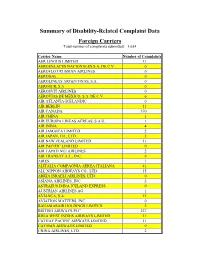

Summary of Disability-Related Complaint Data Foreign Carriers

Summary of Disability-Related Complaint Data Foreign Carriers Total number of complaints submitted: 1,654 Carrier Name Number of Complaints AER LINGUS LIMITED 11 AEROENLACES NACIONALES S.A. DE C.V. 0 AEROFLOT RUSSIAN AIRLINES 0 AEROGAL 0 AEROLINEAS ARGENTINAS, S.A. 0 AEROSUR, S.A. 0 AEROSVIT AIRLINES 0 AEROVIAS DE MEXICO, S.A. DE C.V. 6 AIR ATLANTA-ICELANDIC 0 AIR BERLIN 11 AIR CANADA 370 AIR CHINA 1 AIR EUROPA LINEAS AEREAS, S.A.U. 1 AIR INDIA 4 AIR JAMAICA LIMITED 2 AIR JAPAN, CO., LTD. 5 AIR NEW ZEALAND LIMITED 11 AIR PACIFIC LIMITED 0 AIR TAHITI NUI AIRLINES 2 AIR TRANSAT A.T., INC. 6 AIRES 1 ALITALIA COMPAGNIA AEREA ITALIANA 41 ALL NIPPON AIRWAYS CO., LTD. 15 ARKIA ISRAELI AIRLINES, LTD. 0 ASIANA AIRLINES, INC. 2 ASTRAEUS D/B/A ICELAND EXPRESS 0 AUSTRIAN AIRLINES AG 1 AVIANCA, S.A. 15 AVIATION MATTERS, INC. 0 BAHAMASAIR HOLDINGS LIMITED 2 BRITISH AIRWAYS PLC 237 BWIA WEST INDIES AIRWAYS LIMITED 11 CATHAY PACIFIC AIRWAYS LIMITED 11 CAYMAN AIRWAYS LIMITED 0 CHINA AIRLINES, LTD. 2 CHINA EASTERN AIRLINES CORPORATION 0 COMLUX AVIATION AG 0 COMLUX MALTA LTD. 0 COMPANIA MEXICANA DE AVIACION, S.A. 1 COMPANIA PANAMENA DE AVIACION, S.A. 10 CONDOR FLUGDIENST GMBH 2 CORSAIR 0 CZECH AIRLINES 1 DC AVIATION GMBH 0 DEUTSCHE LUFTHANSA AG 151 EGYPTAIR 1 EL AL ISRAEL AIRLINES LTD. 23 EMIRATES 24 ETHIOPIAN AIRLINES ENTERPRISE 0 ETIHAD AIRWAYS P.J.S.C. 6 EUROATLANTIC AIRWAYS TRANSPORTES AE 0 EVA AIRWAYS CORPORATION 6 FINNAIR OY D/B/A FINNAIR OYJ 1 FIRST AIR 0 GLOBAL JET LUXEMBOURG S.A. -

Change 3, FAA Order 7340.2A Contractions

U.S. DEPARTMENT OF TRANSPORTATION CHANGE FEDERAL AVIATION ADMINISTRATION 7340.2A CHG 3 SUBJ: CONTRACTIONS 1. PURPOSE. This change transmits revised pages to Order JO 7340.2A, Contractions. 2. DISTRIBUTION. This change is distributed to select offices in Washington and regional headquarters, the William J. Hughes Technical Center, and the Mike Monroney Aeronautical Center; to all air traffic field offices and field facilities; to all airway facilities field offices; to all international aviation field offices, airport district offices, and flight standards district offices; and to the interested aviation public. 3. EFFECTIVE DATE. July 29, 2010. 4. EXPLANATION OF CHANGES. Changes, additions, and modifications (CAM) are listed in the CAM section of this change. Changes within sections are indicated by a vertical bar. 5. DISPOSITION OF TRANSMITTAL. Retain this transmittal until superseded by a new basic order. 6. PAGE CONTROL CHART. See the page control chart attachment. Y[fa\.Uj-Koef p^/2, Nancy B. Kalinowski Vice President, System Operations Services Air Traffic Organization Date: k/^///V/<+///0 Distribution: ZAT-734, ZAT-464 Initiated by: AJR-0 Vice President, System Operations Services 7/29/10 JO 7340.2A CHG 3 PAGE CONTROL CHART REMOVE PAGES DATED INSERT PAGES DATED CAM−1−1 through CAM−1−2 . 4/8/10 CAM−1−1 through CAM−1−2 . 7/29/10 1−1−1 . 8/27/09 1−1−1 . 7/29/10 2−1−23 through 2−1−27 . 4/8/10 2−1−23 through 2−1−27 . 7/29/10 2−2−28 . 4/8/10 2−2−28 . 4/8/10 2−2−23 . -

World Air Transport Statistics, Media Kit Edition 2021

Since 1949 + WATSWorld Air Transport Statistics 2021 NOTICE DISCLAIMER. The information contained in this publication is subject to constant review in the light of changing government requirements and regulations. No subscriber or other reader should act on the basis of any such information without referring to applicable laws and regulations and/ or without taking appropriate professional advice. Although every effort has been made to ensure accuracy, the International Air Transport Associ- ation shall not be held responsible for any loss or damage caused by errors, omissions, misprints or misinterpretation of the contents hereof. Fur- thermore, the International Air Transport Asso- ciation expressly disclaims any and all liability to any person or entity, whether a purchaser of this publication or not, in respect of anything done or omitted, and the consequences of anything done or omitted, by any such person or entity in reliance on the contents of this publication. Opinions expressed in advertisements ap- pearing in this publication are the advertiser’s opinions and do not necessarily reflect those of IATA. The mention of specific companies or products in advertisement does not im- ply that they are endorsed or recommended by IATA in preference to others of a similar na- ture which are not mentioned or advertised. © International Air Transport Association. All Rights Reserved. No part of this publication may be reproduced, recast, reformatted or trans- mitted in any form by any means, electronic or mechanical, including photocopying, recording or any information storage and retrieval sys- tem, without the prior written permission from: Deputy Director General International Air Transport Association 33, Route de l’Aéroport 1215 Geneva 15 Airport Switzerland World Air Transport Statistics, Plus Edition 2021 ISBN 978-92-9264-350-8 © 2021 International Air Transport Association. -

Star Alliance Takes Best Alliance Title at Skytrax

STAR ALLIANCE TAKES BEST ALLIANCE TITLE AT SKYTRAX WORLD AIRLINE AWARDS Star Alliance Los Angeles Lounge Best Airline Alliance Lounge Four Star Alliance Airlines ranked among the Top 10 13 Member Carriers Claim a Total of 26 Awards Experience Star Alliance carriers by winning a million miles* PARIS, FRANCE – June 20th, 2017 – In its 20th Anniversary year, Star Alliance has claimed the Best Airline Alliance title at the Skytrax World Airline Awards for the second year running. The Alliance’s prestigious Los Angeles Lounge also received the Best Airline Alliance Lounge Award for the third year in row. Accepting the award at the Paris – Le Bourget Air Show, Jeffrey Goh, CEO Star Alliance said: “This is an important accolade to receive in our 20th Anniversary year. It once again shows that our investment into a modern IT infrastructure is paying off, enabling the more than 440,000 member airline employees to provide customers with an even better Alliance travel experience. Our IT hubs are the foundation which will allow us to use digital technology to offer a more individual and a better Alliance travel experience going forward.” Star Alliance was the first airline alliance to receive the Best Alliance Award from Skytrax when the category was first introduced in 2005 and has since held the award eight times. The World Airline Awards are managed by international air transport rating organisation, Skytrax Research of London, UK. The latest survey was conducted between August 2016 and May 2017, attracting 19.87 million eligible entries with participants from 105 nationalities. The survey covered over 325 airlines, from largest international airlines to smaller domestic carriers, measuring quality standards for 41 Key Performance Indicators across front-line product and service factors in the airport and on-board environments. -

AIRLINE MARKETING and MANAGEMENT.Pdf

AIRLINE MARKETING AND MANAGEMENT This page intentionally left blank Airline Marketing and Management Sixth Edition STEPHEN SHAW © Stephen Shaw 2007 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without the prior permission of the publisher. Stephen Shaw has asserted his right under the Copyright, Designs and Patents Act, 1988, to be identified as the author of this work. Published by Ashgate Publishing Limited Ashgate Publishing Company Gower House Suite 420 Croft Road 101 Cherry Street Aldershot Burlington, VT 05401-4405 Hampshire GU11 3HR USA England Ashgate website: http://www.ashgate.com British Library Cataloguing in Publication Data Shaw, Stephen, 1950- Airline marketing and management. - 6th ed. 1. Airlines - Management 2. Airlines - Marketing I. Title 387.7'4'0688 Library of Congress Cataloging-in-Publication Data Shaw, Stephen, 1950- Airline marketing and management / by Stephen Shaw. p. cm. Includes index. ISBN: 978-0-7546-4819-2 (Hbk) ISBN: 978-0-7546-4820-8 (Pbk) 1. Aeronautics, Commercial--Marketing. 2. Airlines--Marketing. I. Title. HE9781.S35 2007 387.7'40688--dc22 2007002941 ISBN: 978-0-7546-4819-2 (Hbk) ISBN: 978-0-7546-4820-8 (Pbk) Printed and bound in Great Britain by MPG Books Ltd, Bodmin, Cornwall. Contents Introduction xii 1 The Fundamentals 1 1:1 What is Marketing? 1 1:1:1 Definition 1 1:1:2 The “Marketing Mix” 2 1:1:3 Stages in the Application of Marketing Principles -

An Empirical Study of Domestic Airline Industry in India Abstract

DIMENSIONS OF CUSTOMER SERVICE QUALITY - AN EMPIRICAL STUDY OF DOMESTIC AIRLINE INDUSTRY IN INDIA ABSTRACT OF THE THESIS SUBMITTED FOR THE AWARD OF THE DEGREE OF Ph. D. (BUSINESS ADMINISTRATION) BY . VIPPAN RAJ DUTTT Under the Supervision of Dr. Mohammed Naved Khan' ; Dr. S C Bansal Senior Lecturer ' , » Associate Professor Department of Business Administration Indian Institute of Management Faculty of Mgt. Studies & Research Lucknow Aligarh Muslim University, Allgarh (India) (India) (Internal Advisor) (External Advisor) DEPARTMENT OF BUSINESS ADMINISTRATION FACULTY OF MANAGEMENT STUDIES & RESEARCH ALIGARH MUSLIM UNIVERSITY ALIGARH (INDIA) 2008 ABSTRACT Introduction Civil Aviation represents one of the biggest industries worldwide with global airline revenues exceeding US$ 485 billion in 2007 (lATA, 2008b). The industry has moved towards liberalisation in the ownership of national carriers, capacity sharing, price controls and market access, leading to greater competition among airlines. In the de-regulated environment, the customer has many choices, if the first airline does not measure up-to the desired standards of service. Focus on service quality is the need of the hour if the airlines aspire to improve market share and further enhance financial perforniance in domestic and international markets. The airline industry has been a pioneer in the innovative use of Information Technology (IT) (Ghobrial & Trusilov, 2005). E-commerce and IT are changing the nature of the airline business. The dramatic growth of web and self-service technologies facilitate simplified passenger travel involving e-ticketing, automated check-in, common-user self-service kiosks and other passenger, services (Shon, Chen & Chang, 2003). Growth in the air traffic in recent years is due to the spread of low cost service.