2005-024 Syllabus: 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CPY Document

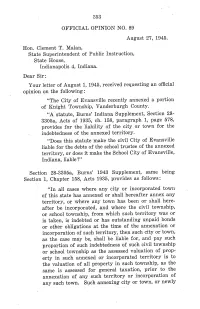

353 OFFICIAL OPINION NO. 89 August 27, 1945. Hon. Clement T. Malan, State Superintendent of Public Instruction, State House, Indianapolis 4, Indiana. Dear Sir: Your letter of August 1, 1945, received requesting an offcial opinion on the following: "The City of Evansvile recently annexed a portion of Knight Township, Vanderburgh County. "A statute, Burns' Indiana Supplement, Section 28- 3305a, Acts of 1935, ch. 158, paragraph 1, page 578, provides for the liabilty of the city or town for the indebtedness of the annexed territory. "Does this statute make the civil City of Evansvile liable for the debts of the school trustee of the annexed territory, or does it make the School City of Evansvile, Indiana, liable?" Section 28-3305a, Burns' 1943 Supplement, saine being Section 1, Chapter 158, Acts 1935, provides as follows: "In all cases where any city or incorporated town of this state has annexed or shall hereafter annex any territory, or where any town has been or shall here- after be incorporated, and where the civil township, or school township, from which such territory was or is taken, is indebted or has outstanding unpaid bonds or other obligations at the time of the annexation or incorporation of such territory, then such city or town, as the case mày be, shall be liable for, and pay such proportion of such indebtedness of such civil township or school township as the assessed valuation of prop- erty in such annexed or incorporated territory is to the valuation of all property in such township, as the same is assessed for general taxation, prior to the annexation of any such territory or incorporation of any such town. -

Volume 2 Appendix S Detailed Map Book Part 7 Central Section

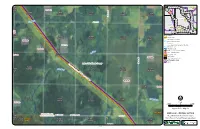

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! 33 34 35 36 37 International ! 38 "11 T 158N 57 39 Falls R32W ! Red Lake 58 40 ! 59 41 S23 83 T 158N T 158N T 158N T 158N 60 42 80 81 82 ! T 158N 84 R32W S24 R31W S19 R31W S20 61 R31W S21 R31W S22 43 85 217" ! 44 " 17th Ave SW 62 86 ! 63 Koochiching 45 46 87 ! (! 64 County Big "65 "72 65 88" r " Falls 47 Riv!e 89 Rapid 67th St SW 66 48 ! (! 67 49 (! Beltrami (! 68 50 ! County 69 51 ! 70 71 "6 Kelliher Mizpah 72 " 90 73 52 ! 53 91 Northome 74 "1 75 76 54 Red ! 92 93 94 95 96 97 77 Funkley 98 55 Lake ! 78 79 56 T 158N ! Proposed Routes R32W S26 T 158N T 158N T 158N ! T 158N R32W S25 T 158N Orange Route R31W S30 R31W S29 (! ! R31W S28 ! (!( R31W S27 Anticipated Route Width Red Lake (! ! Anticipated Right-of-Way ! (! Residences ! Red Lake (! Commercial or Non-Residential Structure ! NHD Watercourse Red Lake ! PWI Watercourse ! Wildlife Management Area (WMA) reek yC ! o Indian Reservation Land T 158N Tr Snowmobile Trail Red Lake R31W! S31 ! Civil Township Red Lake ! Public Land Survey Section ! Existing Transmission Lines ! ! ! ! 500 kV 13th Ave SW Proposed! Orange Route Lake of the Woods County ! T 158N ! T 158N T 158N T 158N R32W S36 a ! T 158N Ch se Brook R31W S32 R32W ! R31W S33 R31W S34 S35 Xcel! Energy, Inc. 500kV ! ! ! ! ! ! Red Lake ! ! ! T 157N Red Lake ! R31W S3 -

The Trajectory of Indian Country in California: Rancherias, Villages, Pueblos, Missions, Ranchos, Reservations, Colonies, and Rancherias

Tulsa Law Review Volume 44 Issue 2 60 Years after the Enactment of the Indian Country Statute - What Was, What Is, and What Should Be Winter 2008 The Trajectory of Indian Country in California: Rancherias, Villages, Pueblos, Missions, Ranchos, Reservations, Colonies, and Rancherias William Wood Follow this and additional works at: https://digitalcommons.law.utulsa.edu/tlr Part of the Law Commons Recommended Citation William Wood, The Trajectory of Indian Country in California: Rancherias, Villages, Pueblos, Missions, Ranchos, Reservations, Colonies, and Rancherias, 44 Tulsa L. Rev. 317 (2013). Available at: https://digitalcommons.law.utulsa.edu/tlr/vol44/iss2/1 This Native American Symposia Articles is brought to you for free and open access by TU Law Digital Commons. It has been accepted for inclusion in Tulsa Law Review by an authorized editor of TU Law Digital Commons. For more information, please contact [email protected]. Wood: The Trajectory of Indian Country in California: Rancherias, Villa THE TRAJECTORY OF INDIAN COUNTRY IN CALIFORNIA: RANCHERIAS, VILLAGES, PUEBLOS, MISSIONS, RANCHOS, RESERVATIONS, COLONIES, AND RANCHERIAS William Wood* 1. INTRODUCTION This article examines the path, or trajectory,1 of Indian country in California. More precisely, it explores the origin and historical development over the last three centuries of a legal principle and practice under which a particular, protected status has been extended to land areas belonging to and occupied by indigenous peoples in what is now California. The examination shows that ever since the Spanish first established a continuing presence in California in 1769, the governing colonial regime has accorded Indian lands such status. -

Hydro-Social Permutations of Water Commodification in Blantyre City, Malawi

Hydro-Social Permutations of Water Commodification in Blantyre City, Malawi A thesis submitted to the University of Manchester for the degree of Doctor of Philosophy in the Faculty of Humanities 2014 Isaac M.K. Tchuwa School of Environment Education and Development Table of Contents Table of Contents ............................................................................................................ 2 List of Figures ................................................................................................................. 6 List of Tables ................................................................................................................... 7 List of Graphs ................................................................................................................. 7 List of Photos .................................................................................................................. 8 List of Maps .................................................................................................................... 9 Abstract ......................................................................................................................... 10 Declaration .................................................................................................................... 11 Copyright Statement .................................................................................................... 12 Acknowledgements .................................................................................................... -

The Concepts of Enclave and Exclave and Their Use

www.ssoar.info The concepts of enclave and exclave and their use in the political and geographical characteristic of the Kaliningrad region Rozhkov-Yuryevsky, Yuri Veröffentlichungsversion / Published Version Zeitschriftenartikel / journal article Empfohlene Zitierung / Suggested Citation: Rozhkov-Yuryevsky, Y. (2013). The concepts of enclave and exclave and their use in the political and geographical characteristic of the Kaliningrad region. Baltic Region, 2, 113-123. https://doi.org/10.5922/2079-8555-2013-2-11 Nutzungsbedingungen: Terms of use: Dieser Text wird unter einer Free Digital Peer Publishing Licence This document is made available under a Free Digital Peer zur Verfügung gestellt. Nähere Auskünfte zu den DiPP-Lizenzen Publishing Licence. For more Information see: finden Sie hier: http://www.dipp.nrw.de/lizenzen/dppl/service/dppl/ http://www.dipp.nrw.de/lizenzen/dppl/service/dppl/ Diese Version ist zitierbar unter / This version is citable under: https://nbn-resolving.org/urn:nbn:de:0168-ssoar-351079 RESEARCH REPORTS This article focuses on the genesis of THE CONCEPTS and correlation between the related con- OF ENCLAVE cepts of enclave and exclave and the scope of their use in different sciences, fields of AND EXCLAVE knowledge, and everyday speech. The au- thor examines the circumstances of their AND THEIR USE emergence in the reference and professional IN THE POLITICAL literature in the Russian language. Special attention is paid to the typology of the AND GEOGRAPHICAL world’s enclave territories as objects of po- CHARACTERISTIC litical geography; at the same time, their new categories and divisions (international OF THE KALININGRAD enclave, overseas exclaves, internal en- claves of different levels) are extended and REGION introduced. -

Land Tenure Issues in Southern Sudan: Key Findings and Recommendations for Southern Sudan Land Policy

LAND TENURE ISSUES IN SOUTHERN SUDAN: KEY FINDINGS AND RECOMMENDATIONS FOR SOUTHERN SUDAN LAND POLICY DECEMBER 2010 This publication was produced for review by the United States Agency for International Development. It was prepared by Tetra Tech ARD. LAND TENURE ISSUES IN SOUTHERN SUDAN: KEY FINDINGS AND RECOMMENDATIONS FOR SOUTHERN SUDAN LAND POLICY THE RESULTS OF A RESEARCH COLLABORATION BETWEEN THE SUDAN PROPERTY RIGHTS PROGRAM AND THE NILE INSTITUTE OF STRATEGIC POLICY AND DEVELOPMENT STUDIES DECEMBER 2010 DISCLAIMER The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government. CONTENTS Acknowledgements Page i Scoping Paper Section A Sibrino Barnaba Forojalla and Kennedy Crispo Galla Jurisdiction of GOSS, State, County, and Customary Authorities over Land Section B Administration, Planning, and Allocation: Juba County, Central Equatoria State Lomoro Robert Bullen Land Tenure and Property Rights in Southern Sudan: A Case Study of Section C Informal Settlements in Juba Gabriella McMichael Customary Authority and Traditional Authority in Southern Sudan: A Case Study Section D of Juba County Wani Mathias Jumi Conflict Over Resources Among Rural Communities in Southern Sudan Section E Andrew Athiba Synthesis Paper Section F Sibrino Barnaba Forojalla and Kennedy Crispo Galla ACKNOWLEDGEMENTS The USAID Sudan Property Rights Program has supported the Southern Sudan Land Commission in its efforts to undertake consultation and research on land tenure and property rights issues; the findings of these initiatives were used to draft a land policy that is meant to be both legitimate and relevant to the needs of Southern Sudanese citizens and legal rights-holders. -

Extracting Semantic Relations from Wikipedia Using Spark

BACHELORTHESIS Extracting Semantic Relations from Wikipedia using Spark vorgelegt von Hans Ole Hatzel MIN-Fakult¨at Fachbereich Informatik Wissenschaftliches Rechnen Studiengang: Informatik Matrikelnummer: 6416555 Betreuer: Dr. Julian Kunkel Erstgutachter: Dr. Julian Kunkel Zweitgutachter: Prof. Dr. Thomas Ludwig CONTENTS CONTENTS Contents 1 Introduction 3 1.1 Motivation . .3 1.2 Goals of this Thesis . .3 1.3 Outline . .4 2 Background 5 2.1 Wikipedia . .5 2.2 Spark . .5 2.2.1 PySpark . .7 2.3 Linguistics . .7 2.3.1 Proper Nouns & Common Nouns . .8 2.3.2 Compound Words . .8 2.4 CRA . .8 2.5 Part-of-Speech Tagging . .8 2.6 Data Mining . .8 2.6.1 K-Means Clustering . .8 2.7 TF-IDF . .9 3 Related Work 10 3.1 Explicit Semantic Analysis . 10 3.2 Word2Vec . 10 4 Design 12 4.1 Preparing Raw Data . 12 4.2 Pipeline for Finding Compound Words . 12 4.2.1 Identifying Nouns . 13 4.2.2 Counting Words . 14 4.2.3 Forming Pairs of Words . 15 4.2.4 Alternative for Forming Pairs . 16 4.2.5 Grouping . 16 4.2.6 Sorting . 16 4.3 Generating CRA Tasks . 17 4.3.1 Psychological considerations . 17 4.3.2 Extracting CRA Tasks . 17 4.3.3 Pruning of results . 19 4.3.4 An Alternative Approach . 19 4.4 Finding solutions for CRA Tasks . 20 4.4.1 Generated Tasks . 20 4.4.2 Real World Tasks . 20 4.5 Finding Semantic Groups in List of Words . 21 4.5.1 Filtering to Improve Word Vectors . -

Conflict & Communication Online 15,2

conflict & communication online, Vol. 15, No. 2, 2016 www.cco.regener-online.de ISSN 1618-0747 Editorial Friedensjournalismus Peace Journalism Saumava Mitra Sichtbarmachen durch photojournalistische Hervorhebung als Selbstreflexivität des Photojournalismus: Zwei Fallstudien über akzidentiellen Friedensjournalismus Display-through-foregrounding by photojournalists as self-reflexivity in photojournalism: Two case studies of accidental peace photojournalism Marta Natalia Lukacovic Friedensjournalismus und radikale Medienethik Peace journalism and radical media ethics Essays Wilhelm Kempf Gefahren des Friedensjournalismus Dangers of peace journalism Freie Beiträge Non-thematic contributions Patrick Osei-Kufuor, Stephen B Kendie & Kwaku Adutwum Boakye Konflikt, Frieden und Entwicklung: Eine räumlich-thematische Analyse gewaltförmiger Konflikte im Norden Ghanas zwischen 2007 und 2013 Conflict, peace and development: A spatio-thematic analysis of violent conflicts in Northern Ghana between 2007 and 2013 Dokumentation Documentation „Kindness builds the world" Willkommenflyer der jüdisch-österreichischen Freiwilligengruppe Shalom Alaikum / Jewish Aid for Refugees Vienna Welcome flyer of the Jewish-Austrian volunteer group Shalom Alaikum / Jewish Aid for Refugees Vienna "Freundschaft gegen Hass" Link zu einem Aufsatz von Alexia Weiss in der Wiener Zeitung vom 23.6.2016 "MuslimInnen und Islam in Österreich" Link zu einem Katalog von Fragen und Antworten der österreichischen Menschenrechtsorganisation SOS Mitmensch „Kasseler Schulderklärung“ Dokumentation -

""6 ""11 ""217 ""65 ""72

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! T 159N R33W S5 T 159N R33W S4 T 159N ! T 159N T 159N T 159N 33 34 35 36 37 38 International R33W S3 ! "11 R33W S2 R33W S1 39 " Falls R32W S6 57 40 ! 58 59 41 Red Lake ! 80 81 82 83 60 42 84 ! 61 43 85 217" ! 44 " 62 86 ! 63 Koochiching 45 46 87 ! 64 County Big "65 "72 65 88" " Falls 47 ! 66 4889 T 159N ! T 159N T 159N 67 49 R33W S8 ! T 159N Beltrami R33W S9 R33W S10 T 159N 68 50 ! T 159N County R33W S11 69 51 R33W S12 R32W S7 Kelliher 70 71 "6 ! 90 Mizpah 72 52 73 53 ! 91 Northome 74 54 "1 75 76 ! 92 93 94 95 96 97 77 Funkley 98 55 79 ! 78 56 ! Xcel Energy, Inc. 500kV Proposed Routes ! Red Lake Orange Route ! Alternatives ! Route Variation ! Anticipated Route Width ! Anticipated Right-of-Way ! Proposed Orange Route USFWS Interest Lands ! Indian Reservation Land ! Public Land Survey Section ! Existing Transmission Lines T 159N T 159N ! T 159N ! ! 500 kV R33W S17 T 159N ! R33W S16 R33W S15 T 159N R33W S14 T 159N ! R33W S13 R32W S18 ! ! Lake of the Woods County ! ! Red Lake ! ! ! ! ! ! ! ! ! Beltrami South Variation ! T 159N T 159N ! T 159N R33W S20 T 159N R33W S21 T 159N ! R33W S22 R33W S23 T 159N R33W S24 !R32W S19 ! ! ! ! S ! a n t a ! A n I a ! F Red Lake o Feet r ! e s 2,000 0 2,000 -

Final Report

Final Report Township of Springwater Economic Development Strategy June 2010 EXECUTIVE SUMMARY Strategic planning is one of the most important tools that a community or economic development organization can use for effective development. It is a means for establishing strategic initiatives and maintaining effective programming based on economic opportunities, constraints and the needs of a community. In the case of the Township of Springwater, its advantageous location within the County of Simcoe, one of the fastest growing regions in the Province, and puts Springwater on the doorstep of one of the busiest four season recreation areas with access to Highways 400, 26 and 93, providing a strong competitive advantage for business and investment attraction to the community. In light of these considerations, the Mayor and Council recognized the need for the community’s first Economic Development Strategy that is premised on building on the Township’s existing strengths and translating this into new opportunities for economic growth. An integral aspect in developing an economic development strategy for the Township of Springwater is to understand its current competitive advantages and disadvantages, its business base, its investment readiness, and the quality of place and experience that it offers both residents and visitors. These factors coupled with the Township’s potential to attract new investment, the presence of entrepreneurs and the capacity for growth in its existing business and industries will help to ensure the Township’s future economic success. Key Objectives Millier Dickinson Blais was contracted by the Township of Springwater to prepare a strategy that will assist and inform the economic development programming efforts of the Township. -

«@563 Case No

04>/5 /4411 IN THE SUPREME CGOURT OF OHIO ~«@563 CASE NO. STATE EX REL BOARD OF TRUSTEES OF ST. CLAIR TOWNSHIP, BUTLER COUNTY, OHIO and TOM BARNES TRUSTEE and GARY R. COUCH TRUSTEE and JUDY VALERIO TRUSTEE Relators, v. CITY OF HAMILTON, OHIO and JOSHUA SMITH L _;, CITY MANAGER OF HAMILTO 3‘? 1 APT? ~. = and CLERK OF COURT SUPREME COURT OF OHIO THOMAS VANDERHORST FINANCE DIRECTOR OF HAMILTON Respondents, Original Action in Mandamus RELATORS’ MOTION AND SUPPORTING MEMORANDUM FOR A PEREMPTORY WRIT OF MANDAMUS COUNSEL FOR RELA TORS COUNSEL FOR RESPONDENTS Gary L. Sheets (0019384) Heather Sanderson Lewis (0069212) Attorney At Law Director of Law 1731 Cleveland Avenue City of Hamilton, Ohio Hamilton, Ohio 45013 345 High Street glsheetsgii/1'use.net Hamilton, Ohio 45011 Office: 513-520-5517 Office: 513-785-7180 lewis@mfitt0n.eom Catherine A. Cunningham (0015730) Richard C. Brahm (0009481) Kegler, Brown, Hill & Ritter 65 East State Street, Suite 1800 Columbus, Ohio 43215 (614) 462-5486 Fax: (614) 228-1472 ccuninghamflkeglerbrownxom [email protected] IN THE SUPREME COURT OF OHIO STATE EX REL BOARD OF TRUSTEES OF ST. CLAIR TOWNSHIP, BUTLER COUNTY et al. Relators, V. Case No. CITY OF HAMILTON, OHIO et al \a~a~a\/sax/sasasysa Respondents, RELATORS' MOTION AND SUPPORTING MEMORANDUM FOR A PEREMPTORY WRIT OF MANDAMUS Relators St. Clair Township and its Trustees move this Court to issue a peremptory writ of mandamus in this case directed to the Respondents City of Hamilton, Ohio, its City Manager Joshua Smith, and its Finance Director Tom Vanderhorst. As grounds for the granting of such a peremptory writ, Relators say the relevant facts in this case are uncontroverted and it appears beyond doubt that St. -

IC 36-1-2 Chapter 2. Definitions of General Applicability

IC 36-1-2 Chapter 2. Definitions of General Applicability IC 36-1-2-1 Application to title Sec. 1. The definitions in this chapter apply throughout this title. As added by Acts 1980, P.L.211, SEC.1. IC 36-1-2-1.7 "Assessed value" Sec. 1.7. "Assessed value" has the meaning set forth in IC 6-1.1-1-3. As added by P.L.6-1997, SEC.202. IC 36-1-2-2 "Bonds" Sec. 2. "Bonds" means any evidences of indebtedness, whether payable from property taxes, revenues, or any other source, but does not include notes or warrants representing temporary loans that are payable out of taxes levied and in the course of collection. As added by Acts 1980, P.L.211, SEC.1. IC 36-1-2-3 "City" Sec. 3. "City" refers to a consolidated city or other incorporated city of any class, unless the reference is to a school city. As added by Acts 1980, P.L.211, SEC.1. IC 36-1-2-4 "Clerk" Sec. 4. "Clerk" means: (1) clerk of the circuit court, for a county; (2) county auditor, for a board of county commissioners or county council; (3) clerk of the city-county council, for a consolidated city; (4) city clerk, for a second class city; (5) clerk-treasurer, for a third class city; (6) clerk-treasurer, for a town; or (7) chief executive officer of a political subdivision not described in subdivisions (1) through (6). As added by Acts 1980, P.L.211, SEC.1. Amended by Acts 1981, P.L.44, SEC.35; P.L.186-2006, SEC.1.