Annual Monitoring Report 12, 2014-15 March 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inventory of the CE Patrick Collection

Inventory of the CE Patrick collection These pages were created by Tom Foster in 1965 / 1966 (Possibly transcribed by Derek Sutcliffe, who passed them to Steve Jarvis) co v.,ks j-, jo ^ wTia. of - a,. t .~ . p.aFk i 8K. 0 he eked and r ;or.h ! Ji Thru .1960,, PADKmT LKf-uh-K. v/ith r ....KCl, r T ■--d03. (i»ote : - . iV such le t - e r a . Vh e ..urkings and a straight line name Oa a pos- lo'./n w ill be found in that part of these notes). 1. Entire from d.n. --all at ro..illy, Ja uica, kited 5th July I t >•')&, to isa Florence halx., Oircua -root, Ju ••*2.aid Place, Lon on. Has been port© at a district post office in Jamaica and sent through the ini, nd post at the pro. aid inland rate of 7£d local curr cy, this fee cover!a • a sin le leti.er travelling up.to a distance o 100 miles (crossed out in tor ri ht corner). *‘o ti’ace of the office narking. deceived -in. a -o^ 1015 only 1808 it., ty, .. F I. Heed. London *’3 Augurt 1808 an charged 4/-, la t e r corrected to 2/- the correct rate for sin : le packet letters to London at this time. 2. .'.intire from Henry Swift at Port aria on 18th ay 1810 to his brother r. 'illiar. v.lft, .out ell, .ot:,i a< shire. A-osied in Kin, 3ton on 26th -ay 1810 v/ith type F2, as there is no truce of inle t poau. -

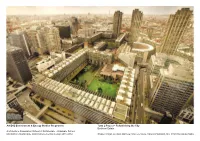

First Concept Designs Released for London Centre for Music Project As Next Steps Announced

PRESS RELEASE For immediate release: 21 January 2019 FIRST CONCEPT DESIGNS RELEASED FOR LONDON CENTRE FOR MUSIC PROJECT AS NEXT STEPS ANNOUNCED Images, animation and film available for download from: https://bit.ly/2QX8SVN The Barbican, London Symphony Orchestra and Guildhall School of Music & Drama have today released the first concept designs for their project to create a world class Centre for Music in London, as part of a progress update on their plans for the proposed new building. This update follows the recent news that the City of London Corporation has backed the next phase of work by providing £2.49 million for the three partners to undertake further design development, and to progress fundraising, business modelling and capital funding plans. The Centre for Music would be a world-class venue for performance and education across all musical genres, harnessing the power of three internationally recognised cultural organisations - the Barbican, LSO and Guildhall School - to inspire a new generation with a love of music. The Centre would include a world class concert hall and superb spaces for performance, education and rehearsal. It would, above all, be a place for people of all ages and backgrounds to experience the joy of making-music first hand. The concept designs, developed by lead architects Diller Scofidio + Renfro, demonstrate the potential to deliver this landmark new building on the current Museum of London site. Elizabeth Diller, Founding Partner, Diller Scofidio + Renfro, said: “We want to unlock the urban potential of the Centre for Music's site at the southern tip of the Barbican by reclaiming the roundabout for the public realm, where the car’s isolating effects are keenly felt today. -

Undertakings and Assurances

CROSSRAIL BILL REGISTER OF UNDERTAKINGS AND ASSURANCES To Whom (Petition No. Documentary/ No. Type Date Given Subject Action & Comment Text (where relevant) (where relevant)) Parliamentary Reference Section A: general or generic assurances that have been given in the various Crossrail Information Papers that have general application 1 Assurance General 20/11/2007 Business relocation Information Paper C1 - Therefore, once the Crossrail Bill has received Royal Assent, and the necessary funding Information for Property Owners - arrangements are in place, the Secretary of State or his nominated undertaker will make Version 2 - Paragraph 2.6 - arrangements to provide businesses with a longer period in which to relocate than the Second and Third Sentences three months specified in the Bill, where this is practicable. In such cases, the Secretary of State’s overall aim will be to provide as long a period as is practicable, commensurate with the co-ordinated progress of the Crossrail works. 2 Assurance General 20/11/2007 Establishment of an agency Information Paper C1 - With a view to assisting those existing businesses which do face the prospect of service to assist in business Information for Property Owners - displacement from their existing premises in relation to Crossrail in their search for suitable relocation Version 2 - Paragraph 2.3 - First alternative accommodation, the Secretary of State will establish an agency service at his and Second Sentences expense (or that of his nominated undertaker).The agency service will help firms ascertain -

Timeline Copy

POLITICS 1066 Norman invasion of England 1216 establishment of the Parliament of England 1888 creation of the London County Council 410 Londinium is abandoned following Roman decline the power of England is centralised: 1963 creation of the Greater London William the Conqueror recognises the autonomy 1500s economy in the City of London, Roman foundation of Londinium 1067 the Common Council of 43 of the City of London from the monarchy politics and religion in Westminster failed attempt to amalgamate the City with the rest of London 1376 the City is created 200 000 1894 2000 Ken Livingstone appointed Mayor of London establishment of the Corporation of London the Anglo-Saxons move inside the ~1150 ~890 Wall for defence purposes Amsterdam falls under the French ~1100 Westminster becomes the official seat of the King 1795 loosing its role as financial capital of Europe ~520 the Anglo-Saxons take over, and 2009 Labour proposes (in vain) to introduce settle outside the Roman town political control on the Corporation 1215 the King recognizes the Lord Mayor, directly elected by the City underground and rail lines in 1902 ECONOMICS beginning of insurance market the “Big Bang”: deregulation of financial 1688 in E. LLoyd’s coffehouse 1986 1300s incorporation of the Livery Companies markets and introduction of electronic trading in the City government 1571 Royal Exchange 1694 Bank of England 2007 start of the financial crisis 1665 the Great Plague 140 000 THE CITY OF LONDON 1350 the Black Death 1666 the Great Fire 1941 the Blitz: German bombings over London 1993 Bishopsgate bombing by IRA A BRIEF SPATIAL AND POLITICAL HISTORY 2002 renewed spatial planning policies 1200s First covered markets demolition of the Wall 1976 completion of the Barbican Estate completion of 30 St. -

Barbican Estate

Rapporteur InnovaImage not foundConcrete or type unknown 2019 Fundación DOCOMOMO Ibérico [email protected] Image not found or type unknown Barbican Estate United Kingdom Commission Silk Street 1955 London EC2Y 8DS London Completion 1975 Other denominations The Barbican Original use Current use Housing/housing ensemble Housing/housing ensemble Architects Chamberlin, Powell and Bon (Geoffry Powell, Peter "Joe" Chamberlin, Christoph Bon) Concrete by reinforcement Reinforced concrete Construction method Architectural concrete Cast-in-place concrete, in-situ concrete, Precast Exposed aggregate concrete concrete, precast element, Facade cladding Structural types One-dimensional/concrete frame Description In an area of central London devastated by bombings during World War II, the architects Chamberlin, Powell and Bon built a utopian urban vision in one of the most emblematic parts of the City of London, a paradigm of 1970s post-war urban planning. The heart of the complex is a large artistic and cultural center. The rest is occupied by residential buildings of different types, configurations and volumes; all this surrounds a large central void with carefully designed gardens and ponds, generating an exquisite spatial quality. The monumental scale of the building and public spaces combines perfectly with the domestic sphere, through elevated access walkways that are more like pedestrian streets than simple distribution corridors. The urban quality of the whole is remarkable and much appreciated by Londoners, contrasting sharply with other examples from the same period that have suffered a slow decline. The characteristic appearance of the concrete used for the Barbican is the result of a careful choice of sands and aggregates, and an extremely complex and precise final treatment, in which the craftsmen first exposed the aggregate and then manually brushed the surface to obtain the desired shine and color. -

BA Response to Barbican and Golden Lane Area Strategy

Response from Barbican Association to Barbican and Golden Lane Area Strategy SUMMARY We welcome the intention to improve the area around the Barbican and Golden Lane estates. We appreciate the emphasis on maintaining the tranquillity and residential amenity of the Barbican Estate. Residents accept that the area is likely to get busier. What we are keen to preserve is the tranquillity that respondents of all types recognise in the area. For residents what matters in particular (and which has existed since the estate was built) is quietness from the middle evening on into the night and during most of the weekend. We understand the desire of the cultural institutions for more visibility and accessibility and support that where it will not interfere with residential amenity. Our detailed responses to the many proposals in this strategy are outlined in this document. We highlight three in particular and make four further general points. 1 We strongly support the creation of a way finding and signage review and strategy and would give it the highest priority. Done well and sensitively, a way finding strategy that includes the wider area (including stations) and the cultural institutions themselves could go a considerable way to solving some of the other problems at considerably less cost. 2 We strongly oppose the insertion of an additional bridge across the lake. This would ruin one of the iconic vistas of the Barbican estate and would damage the tranquillity that is appreciated by residents and visitors alike. It would also radically change the nature of the estate, and not protect residential amenity. -

Term 2 Project

AA E+E Environment & Energy Studies Programme Term 2 Project - Refurbishing the City Barbican Estate Architecture Association School of Architecture - Graduate School Msc/MArch Sustainable and Environemental Design 2011-2012 Shaker Majali, Luciana Mathew, Marcelo Mello, Saachi Padubidri, Nor Izzati Mohamad Salim ARCHITECTURAL ASSOCIATION SCHOOL OF ARCHITECTURE GRADUATE SCHOOL PROGRAMMES COVERSHEET FOR SUBMISSION 2011-2012 PROGRAMME: Sustainable Environmental Design TERM: 2 Shaker Majali,Luciana Mathew,Marcelo Mello,Nor Izzati Mohamad STUDENT NAME(S): Salim,Saachi Padubidri SUBMISSION TITLE Barbican Estate Refurbishment:terraced apartment study NO. OF WORDS 10700 COURSE TITLE Refurbishing the city COURSE TUTOR Joana Carla Sares Goncalves COURSE TITLE Refurbishing the city SUBMISSION DATE: 30th March 2012 DECLARATION: “I certify that this piece of work is entirely my/our own and that any quotation or paraphrase from the published or unpublished work of others is duly acknowledged.” Signature of Student(s): Date: 29th March 2012 69 Acknowledgements Abstract We would like to thank Mrs. Sarah Guventa, Mr. David Hills and Mr. Robert This Term’s design project was a continuation of our Refurbishing the City the use of the existing district heating system by making changes only within Barker (the residents of the Barbican estate) for their time and patience to research agenda. Our case study was to analyze the Barbican Estate as the apartments from electric underfloor heating to hot water pipes. answer all our questions during the entire process of the term 2 building a refurbished project. Its purpose was to build on the findings of last years The third was to develop architecture of sustainable environmental design. -

(Public Pack)Agenda Document for Barbican Estate

Public Document Pack Barbican Estate Residents Consultation Committee Date: MONDAY, 22 MAY 2017 Time: 6.30 pm Venue: COMMITTEE ROOMS, 2ND FLOOR, WEST WING, GUILDHALL Members Graham Wallace - Chairman John Tomlinson - Cromwell Tower Vacancy x 2 - Deputy Chairman Mary Bonar - Wallside Richard Tomkins - Lauderdale Fred Rodgers - Breton House Mark Bostock - Frobisher David Graves - Seddon House Gordon Griffiths - Bunyan Court Richard Dykes - Gilbert House Fiona Lean - Ben Jonson House Ted Reilly - Shakespeare Tower Jane Smith - Barbican Association Christopher Makin - Speed House John Taysum - Bryer Court Nancy Chessum - Andrewes House Janet Wells - John Trundle House Jim Davies - Mountjoy House vacancy - Willoughby House Sandy Wilson - Shakespeare Tower Averil Baldwin - Thomas More House David Kirkby - Defoe House Enquiries: Julie Mayer tel.no.: 020 7332 1410 [email protected] John Barradell Town Clerk and Chief Executive AGENDA 1. APOLOGIES 2. DECLARATIONS BY MEMBERS UNDER THE CODE OF CONDUCT IN RESPECT OF ITEMS ON THE AGENDA 3. MINUTES To agree the minutes of the Barbican Residents’ Consultation Committee (RCC) held on 30 January 2017 and the meeting of the RCC’s AGM on 6 March 2017. For Decision (Pages 1 - 12) 4. 'YOU SAID: WE DID' : OUTSTANDING ACTIONS LIST Report of the Director of Community and Children’s Services. For Information (Pages 13 - 14) 5. ELECTION OF DEPUTY CHAIRMAN This item was deferred at the RCC’s AGM on 6 March 2017. For Decision 6. BARBICAN CHARGING POLICY FOR CAR PARKING Report of the Director of Community and Children’s Services. For Information (Pages 15 - 28) 7. REPAIRS AND MAINTENANCE TO ROOFS/BALCONIES FOLLOWING WATER PENETRATION Report of the Director of Community and Children’s Services. -

Blake Tower, Barbican EC2 Offers in Excess of £650,000

Blake Tower, Barbican EC2 Offers in excess of £650,000 Hamilton Brooks 73 Long Lane London EC1a 9ET T: 020 7606 8000 E: [email protected] Brand new contemporary twenty first century version of a Barbican Apartment. This bright and airy one Bed apartment. Gorgeous contemporary kitchen, double bedroom, stunning walk in shower room, wide spacious hallway & plenty of storage. Superb entrance lobby with concierge. The Barbican Fourth Tower. Superb conversion by Redrow Homes of this Grade II Listed Tower now offering 74 apartments in the Barbican’s 4th Tower block. Design and architecture studio Conran and Partners has reworked the interior of a 17-storey block that forms part of London's Brutalist Barbican Estate, Built in 1968 by architects Chamberlin, Powell and Bon, who also designed the Barbican Estate in the 1950s. Renamed Blake Tower after 18th-century English poet and artist William Blake, whose grave is located in nearby Bunhill Fields. This mews is in a primary location, just across the road from the new FARRINGDON CROSSRAIL (Elizabeth Line) station opening this year 2018, which will become the biggest transport hub in London with 140 trains an hour going East/West & North/South with underground stations within close proximity, Chancery Lane Station (0.1 miles - Central line), Farringdon Station (Thameslink, Crossrail, Circle, Hammersmith & City and Metropolitan lines), and Holborn Station (0.5 miles - Central and Piccadilly lines). Terms : Subject to contract Ground Rent: £10 Per Annum Tenure: 150 years Council Tax Band F £1348.26 For the period 1 April 2018 – 31 March Service Charge: Approx £5 per sq ft 2019 Local Authority: Corporation of London Important Notice In accordance with the Property Misdescriptions Act (1991) we have prepared these particulars these particulars as a general guide to give a broad descriptions of the property of the property . -

Call for Entries from Architects, Designers and Artists to Improve Culture Mile’S Pedestrian Experience Along Its North-South Route

Call for entries from architects, designers and artists to improve Culture Mile’s pedestrian experience along its North-South route The City of London Corporation is delighted to announce a call for entries to improve wayfinding, walkability and the pedestrian experience along Culture Mile’s ‘North-South route’ between the Millennium Bridge and Barbican. The City of London Corporation is seeking an innovative design concept and proposal for the ‘Culture Mile North-South Route’, between the Millennium Bridge, St Paul’s Cathedral, Aldersgate Street and St Martin’s-le-Grand, to be included as part of the Culture Mile 2019-2020 public programme. The City is looking for inspiring designs that will improve the wayfinding, walkability, appearance and vitality of this key thoroughfare, which links the Southbank to the Culture Mile area. This busy route incorporates entrances to several landmarks, such as St Paul’s Cathedral, the Museum of London and the Barbican estate. It includes the Barbican and St Paul’s underground stations, which collectively provide over 28 million passenger entrances/exits annually. We are inviting architects, designers and artists to submit a concept design that will elevate and enhance the look and feel of this area, providing visual cues, increased wayfinding and a deeper sense of connection between St Paul’s and Barbican underground stations. Following the shortlist of entries in July, the winning team will be revealed and commissioned to develop a fully costed, feasible design that can be installed in a section of the route, subject to planning permission and other relevant City authorisations. The design will remain in situ between Autumn 2019 and Spring 2020. -

Architecture & Finance

bulletin Architecture & Finance 2019/20 eabh (The European Association for Banking and Financial History e.V.) Image: Bank of Canada and Museum entrance. 29 Sept 2017. Photo: doublespace bulletin Architecture & Finance 2019/20 www.bankinghistory.org ISSN 2219-0643 bulletin | 2019/20 3 CONTENTS contents Athens to New York 6 The barriers of banking 24 Societe Generale’s architecture in Africa 32 Caixa Geral Depósitos in Brazil: Agência Financial in Rio de Janeiro 35 Bank of Canada: An architectural heritage 39 The Masonry of capitalism 45 L’Hôtel de la Monnaie de Paris: A royal architecture to the service of the monetary process 48 The house of Commerzbank at Pariser Platz in Berlin 56 Deutsche Bundesbank: Regional office in Hesse 60 KfW Group Westarkade: An energy efficient office building 65 Athenian neoclassical residence in the 19th century: A photography collection 68 Dutch functionalism in the tropics: The factory of the Netherlands Trading Society 73 BNP Paribas Asia Pacific campus 79 Headquarters of Banco Santander: The buildings of Buenos Aires, Santiago de Chile and São Paulo 87 Martins Bank head office: Liverpool 1927-32 92 Intended for magnificent business: The enduring legacy of New Court 102 Locations of the Royal Mint 107 Schroders plc 112 The New York Stock Exchange’s 11 Wall Street building 115 KEY TITLE EDITORS SUBMISSIONS bulletin (eabh - The European Carmen Hofmann, eabh All submissions by email Association for Banking and Gabriella Massaglia, eabh EMAIL Financial History) Hanauer Landstrasse 126-128, D-60314 [email protected] Frankfurt am Main, Germany DESIGN TEL Richard McBurney, Grand Creative, LANGUAGE EDITOR +49(0)69 36 50 84 650 www.grand-creative.com Jonathan Ercanbrack, SOAS University Chloe Colchester, Oxford University WEBSITE www.bankinghistory.org bulletin | 2019/20 5 ATHENS TO NEW YORK Athens to New York Carmen Hofmann his article provides the long view of financial architecture reaching from T antiquity to the present day, and focussing on the most important neo-classi- cal financial buildings in New York. -

Culture Mile Look and Feel Strategy

CULTURE MILE LOOK AND FEEL STRATEGY DETAILED DELIVERY PLAN 1 2 CONTENTS INTRODUCTION 05 • The team • Structure of this document • Public and Stakeholder engagement THE AIMS 01 - Form a Culture Spine 17 02 - Take the Inside Out 35 03 - Discover and Explore 51 04 - Be Recognisable and be Different 69 SUMMARY DELIVERY PLAN 81 APPENDIX 87 • Appendix 1 - Form a Culture Spine • Appendix 2 - Take the Inside Out • Appendix 3 - Discover and Explore • Appendix 4 - Be Recognisable and be Different 3 4 CULTURE MILE LOOK AND FEEL STRATEGY INTRODUCTION 5 THE TEAM FLUID As lead consultant we are responsible for the project management, leadership and vision development. Fluid led on the site analysis, research, engagement and development of the public realm strategy. LEAD CONSULTANT ALAN BAXTER VISION DEVELOPMENT Provided heritage expertise and input into the transport, PUBLIC REALM STRATEGY movement and access strategies. CONTEMPORARY ART SOCIETY (CAS) Developed the cultural strategies that aid place activation and advised on governance considerations. SEAM Looked at the opportunities for lighting to aid wayfinding, highlight landmarks and give expression to key spaces. ARUP DIGITAL PUBLIC INFORMATION HERITAGE Developed digital tools for interactive communications CULTURAL STRATEGY LIGHTING STRATEGY LANDSCAPE AND GREENING TRANSPORT AND MOVEMENT and public information. SECURITY ARUP LANDSCAPE Developed the landscape, green infrastructure and sustainability principles and advised on management. ARUP SECURITY Advised on security matters, providing guidance on protecting people and property in the public realm. 6 STRUCTURE OF THIS DOCUMENT LOOK AND FEEL STRATEGY This document is organised into four sections: 1. PUBLIC AND STAKEHOLDER ENGAGEMENT - Contains information on findings of engagement about Culture Mile and the Look and Feel Strategy.