Comptroller and Auditor-General's (Duties, Powers and Conditions of Service) Act, 1971

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Internal Audit Committee FAQ1

Internal Audit Committee FAQ1 What is an audit committee? What are the roles and Members that provide oversight of auditing and responsibilities of the audit internal control for the agency and help support independence of the internal audit function. committee? • Oversight of the Internal Audit Function Why do agencies that have an internal audit • Governance • Ethics (including tone at the top) function need an audit committee? • Risk Management Oregon Administrative Rule (OAR) 125-700-0125 (5) • Internal Control and Compliance states that “each agency having an internal audit • Operational Effectiveness and Efficiency function shall establish and maintain an audit committee.” The OAR also provides the framework for audit committees as: • The role and function of the audit committee shall What should the audit committee review? be stated in a formal, written charter that • Audit Committee Charter describes the authority, responsibilities, and • Internal Audit Charter structure of the audit committee. The charter • Annual Risk Assessment must be approved and periodically reviewed by • Audit Plan the audit committee and governing board (or • Audit Reports (both internal and external) agency head in the absence of a governing board). • Follow-up on prior audit recommendations • The primary purpose of the audit committee is to • Annual Report to DAS enhance the quality and independence of the • Performance Metrics audit function, thereby helping ensure the • External Quality Assurance Reviews (peer integrity of the internal audit process. -

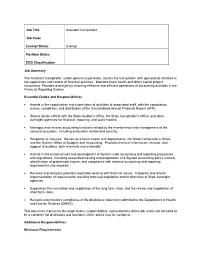

Job Title Assistant Comptroller Job Code Exempt Status Exempt

Job Title Assistant Comptroller Job Code Exempt Status Exempt Position Status EEO Classification Job Summary The Assistant Comptroller, under general supervision, assists the Comptroller with operational activities in the supervision and control of financial activities. Monitors fiscal health and direct capital project accounting. Provides oversight by ensuring effective and efficient operations of accounting activities in the Financial Reporting System. Essential Duties and Responsibilities • Assists in the coordination and supervision of activities of associated staff, with the compilation, review, completion, and distribution of the Consolidated Annual Financial Report (AFR). • Directs liaison efforts with the State Auditor’s Office, the State Comptroller’s Office, and other oversight agencies for financial, reporting, and audit matters. • Manages and reviews accounting functions related to the maintenance and management of the accounting system, including production control and security. • Responds to inquiries. Serves as a fiscal liaison with departments, the State Comptroller’s Office, and the System Office of Budgets and Accounting. Provides financial information, records, and support to auditors, both internally and externally. • Assists in the enhancement and development of System-wide accounting and reporting procedures and regulations, including associated training and preparation of a System accounting policy manual, identification of problematic issues, and compliance with external accounting and reporting requirements and requests. • Reviews and analyzes potential legislation dealing with financial issues. Interprets and directs implementation of requirements resulting from new legislation and/or directives of State oversight agencies. • Supervises the calculation and negotiation of the long form rates, and the review and negotiation of short form rates. • Reviews and monitors compliance of the disclosure statement submitted to the Department of Health and Human Services (DHHS). -

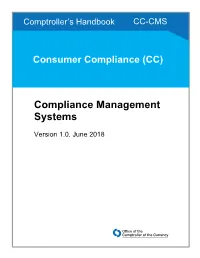

Compliance Management Systems, Comptroller's Handbook

Comptroller’s Handbook CC-CMS Consumer Compliance (CC) Compliance Management Systems Version 1.0, June 2018 Version 1.0 Contents Introduction .............................................................................................................................1 Compliance Management Systems Defined ................................................................. 1 Use of this Booklet........................................................................................................ 1 CMS Examinations ....................................................................................................... 2 Community Reinvestment Act Considerations .................................................... 3 Heightened Standards ................................................................................................... 3 Risks Associated With CMS ......................................................................................... 4 Compliance Risk .................................................................................................. 4 Operational Risk .................................................................................................. 4 Strategic Risk ....................................................................................................... 5 Reputation Risk .................................................................................................... 5 CMS Components ....................................................................................................................6 -

Comptroller of the Treasury COMPTROLLER of the TREASURY State Capitol Nashville, TN 37243-0260 (615) 741–2501

JOHN G. MORGAN Comptroller of the Treasury COMPTROLLER OF THE TREASURY State Capitol Nashville, TN 37243-0260 (615) 741–2501 www.comptroller.state.tn.us The comptroller of the treasury is a constitutional officer elected by the General Assembly for a term of two years. State statutes prescribe his duties, the most important of which relate to audit of state and local government entities, and participation in the general financial and administrative management of state government. The comptroller is a member of the State Building Commission, State Capitol Commission, Board of Claims, Board of Equalization, State Funding Board, Tennessee State School Bond Authority, Tennessee Local Development Author- ity, Tennessee Housing Development Agency, Board of Standards, Tennessee Consolidated Retirement System Board of Trustees, Tennessee Health Services and Development Agency, Tennessee Student Assistance Corporation, Publica- tions Committee, Public Records Commission, State Insurance Committee, Local Education Insurance Committee, Local Government Insurance Committee, State Library and Archives Management Board, Tennessee Advisory Commission on Intergovernmental Relations, Information Systems Council, Tennessee Competi- tive Export Corporation, State Trust of Tennessee Board of Directors, Child Care Facilities Corporation, Governor’s Council on Health and Physical Fitness, Sports Festivals Incorporated, Utility Management Review Board, Tennessee Commod- ity Producers Indemnity Corporation, Water and Wastewater Financing Board, Council on Pensions -

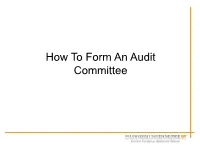

How to Form an Audit Committee Contents

How To Form An Audit Committee Contents • Background Info • Purpose of the Audit Committee • The Audit Committee – Establishment • ThreeStar Applicant/Grantee Requirements – Membership • ThreeStar Applicant/Grantee Requirements – Duties • ThreeStar Applicant/Grantee Requirements – Meetings • ThreeStar Applicant/Grantee Requirements – Sample Resolution – Sample Checklist – ThreeStar Program Adjustments March, 12 2013 Background • The Local Government Modernization Act of 2005 encourages counties to form an audit committee. • The Local Government Modernization Act of 2005 is codified in TCA §9-3-405. Background Cont. • The comptroller of the treasury may require the formation of an audit committee if: – a local government is not in compliance with Government Accounting and Standards Board (GASB) standards by June 30, 2008, – or has recurring findings of material weakness in internal control for three or more consecutive years. Background Cont. • ThreeStar Program Adjustments as of March 12, 2013 for the ThreeStar Grant Applicant/Grantee • The TN Department of Economic and Community Development will follow an audit committee process (after consultation with the TN Comptrollers Office) for the ThreeStar Grant Applicants/Grantee Purpose of the Audit Committee • The audit committee is established to provide independent review and oversight of: – the government’s financial reporting processes, – the government’s internal controls, – a review of the external auditor’s report and following up on corrective action, – and compliance with laws, regulations, and ethics. The Audit Committee • Establishment – ThreeStar applicant requirement • Membership – ThreeStar applicant requirement • Duties • Meetings – ThreeStar applicant requirement • Sample Resolution • Sample Checklist Audit Committee Establishment • This committee is created by the county legislative body (established by resolution or charter), which selects the members. -

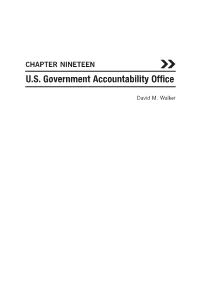

Chapter Nineteen U.S

CHAPTER NINETEEN U.S. Government Accountability Office David M. Walker 126 U.S. GOVERNMENT ACCOUNTABILITY OFFICE By David M. Walker There is one very important and nonpartisan federal agency with a major government-wide impact that will not be directly affected by the transition to a new presidential administration in 2017: the U.S. Government Account- ability Office (GAO). The head of the GAO is the Comptroller General of the United States. You may have some initial apprehension regarding GAO. After all, GAO is the “Watchdog for Congress.” As such, GAO has a critically important role in helping Congress oversee the executive branch. In addition to GAO’s well- known oversight work, the agency is also in the insight and foresight business. Specifically, GAO has insights on what federal government programs, policies, functions, and activities work and which ones don’t. GAO is exposed to “best practices” and “lessons learned” across the federal government and from its counterpart audit organizations around the world. GAO also employs foresight by identifying key trends and challenges that affect the United States and its position in the world. These can help government address current and emerging challenges before they reach crisis proportions, while also capital- izing on related opportunities. Furthermore, in an effort to lead by example, GAO engaged in a widely acclaimed transformation starting in the late 1990s. GAO’s transformation offers valuable information and insights to other agency leaders who want to achieve major transformational change in their own agencies. Given these facts, GAO can be a valuable source of professional and objective information for new administration officials. -

GOVERNMENT ACCOUNTABILITY OFFICE 441 G Street NW., Washington, DC 20548 Phone, 202–512–3000

LEGISLATIVE BRANCH 47 GOVERNMENT ACCOUNTABILITY OFFICE 441 G Street NW., Washington, DC 20548 Phone, 202–512–3000. Internet, www.gao.gov. Comptroller General of the United States DAVID M. WALKER Chief Operating Officer GENE L. DODARO Chief Administrative Officer SALLYANNE HARPER Associate Chief Administrative Officer CHERYL WHITAKER General Counsel GARY L. KEPPLINGER Teams: Managing Director, Acquisition and KATHERINE SCHINASI Sourcing Management Managing Director, Applied Research and NANCY KINGSBURY Methods Directors THOMAS J. MCCOOL, SIDNEY SCHWARTZ Chief Accountant ROBERT DACEY Chief Economist SUSAN OFFUTT Chief Statistician RONALD FECSO Chief Technologist NABAJYOTI BARKAKATI, Acting Chief Actuary JOSEPH APPLEBAUM Managing Director, Defense Capabilities and JANET ST. LAURENT Management Managing Director, Education, Workforce, CYNTHIA M. FAGNONI and Income Security Managing Director, Financial Management MCCOY WILLIAMS and Assurance Managing Director, Forensic Audits and GREGORY D. KUTZ Special Investigations Managing Director, Financial Markets and RICHARD J. HILLMAN Community Investments Managing Director, Health Care MARJORIE KANOFF Managing Director, International Affairs and JACQUELYN WILLIAMS-BRIDGERS Trade Managing Director, Information Technology JOEL WILLEMSSEN Managing Director, Natural Resources and ROBERT A. ROBINSON Environment Managing Director, Physical Infrastructure PATRICIA A. DALTON Managing Director, Strategic Issues J. CHRISTOPHER MIHM Managing Director, Homeland Security and NORMAN J. RABKIN Justice Support Functions: -

Constitutional Provisions Chapter - V

CONSTITUTIONAL PROVISIONS CHAPTER - V COMPTROLLER AND AUDITOR GENERAL OF INDIA 148. Comptroller and Auditor General of India (1) There shall be a Comptroller and Auditor General of India who shall be appointed by the President by warrant under his hand and seal and shall only be removed from office in like manner and on like grounds as a Judge of the Supreme Court. (2) Every person appointed to be the Comptroller and Auditor General of India shall, before he enters office, make and subscribe before the President or some person appointed in that behalf by him, an oath or affirmation according to the form set out for the purpose in the Third Schedule. (3) The salary and other conditions of service of the Comptroller and Auditor General shall be such as may be determined by Parliament by law and, until they are so determined, shall be as specified in the Second Schedule: Provided that neither the salary of the Comptroller and Auditor General nor his rights in respect of leave of absence, pension or age of retirement shall be varied to his disadvantage after his appointment. (4) The Comptroller and Auditor General shall not be eligible for further office either under the Government of India or under the Government of any State after he has ceased to hold office. (5) Subject to the provisions of this Constitution and of any law made by Parliament, the conditions of service of persons serving in the Indian Audit and Accounts Department and the administrative powers of the Comptroller and Auditor General shall be such as may be prescribed by rules made by the President after consultation with the Comptroller and Auditor General. -

Audit Committees – Form and Functions

AUDIT COMMITTEES – FORM AND FUNCTIONS THE TENNESSEE COMPTROLLER OF THE TREASURY, TGFOA AND CTAS CPE OCTOBER 8, 2020 2 LEARNING OBJECTIVES 1. Audit Committee Objectives 2. Creation of an Audit Committee 3. Audit Committee Functions 4. Internal Controls 5. Annual External Audit and Other Types of Audits 3 SECTION 1 – AUDIT COMMITTEE OBJECTIVES 4 COMPTROLLER - AUDIT COMMITTEE OBJECTIVES From the perspective of the Division of Local Government Audit (LGA), the main objectives of a formal audit committee are to: Carefully review, upon completion of the local government’s annual audit, all audit findings in audit report and consult with the external auditors regarding any irregularities and deficiencies disclosed in the annual audit. The audit committee is empowered to meet with management to discuss audit findings and/or disagreements with the external auditors. The audit committee should satisfy itself that appropriate and timely corrective action has been taken by management to remedy any identified weaknesses. The audit committee should determine what corrective action, if any, should be recommended to the governing body. 5 COMPTROLLER - AUDIT COMMITTEE OBJECTIVES (CONT.) To consider the effectiveness of the internal control system, including information technology security and control, review the effectiveness of the system for monitoring compliance with laws and regulations, and review the process for communicating the government’s ethics policies to its employees and monitoring compliance therewith. To establish a process by which employees, taxpayers, or other citizens may confidentially report suspected illegal, improper, wasteful or fraudulent activity under provisions of T.C.A. § 9-3-406. To annually present a written committee report detailing how it discharged its duties and any committee recommendations to the full governing body. -

NYS Accounting and Reporting Manual

TABLE OF CONTENTS PART I - Accounting and Reporting Chapter 1 - Introduction.................................................................................................................... 3 Chapter 2 - Basic Governmental Accounting Principles ............................................................. 6 Chapter 3 - Measurement Focus and Basis of Accounting .......................................................12 Chapter 4 - Funds and Supplemental Schedules .........................................................................16 Chapter 5 - Classification and Coding Structure ........................................................................19 Chapter 6 - Budgeting ......................................................................................................................24 Chapter 7 - Defining the Financial Reporting Entity .................................................................29 Chapter 8 - Financial Reporting .....................................................................................................37 Chapter 9 - GASB Statement No. 34............................................................................................39 Chapter 10 - Sample Journal Entries.............................................................................................43 Budget Entries ...........................................................................................44 Real Property Tax Entries ........................................................................47 Revenue Entries.........................................................................................65 -

Gene L. Dodaro, Comptroller General, U.S. Government Accountability Office

Gene L. Dodaro, Comptroller General, U.S. Government Accountability Office Gene L. Dodaro became the eighth Comptroller General of the United States and head of the U.S. Government Accountability Office (GAO) on December 22, 2010, when he was confirmed by the United States Senate. He was nominated by President Obama in September of 2010 from a list of candidates selected by a bipartisan, bicameral congressional commission. He had been serving as Acting Comptroller General since March of 2008. Mr. Dodaro has testified before Congress dozens of times on important national issues, including the nation's long term fiscal outlook, efforts to reduce and eliminate overlap and duplication across the federal government and GAO's "High Risk List" that focuses on specific challenges—from reducing improper payments under Medicare and Medicaid to improving the Pentagon's business practices. In addition Mr. Dodaro has led efforts to fulfill GAO's new audit responsibilities under the Dodd-Frank Wall Street Reform and Consumer Protection Act. As Comptroller General, Mr. Dodaro helps oversee the development and issuance of hundreds of reports and testimonies each year to various committees and individual Members of Congress. These and other GAO products have led to hearings and legislation, billions of dollars in taxpayer savings, and improvements to a wide range of government programs and services. In a GAO career dating back more than 40 years, Mr. Dodaro has held a number of key executive posts. For 9 years, Mr. Dodaro served as the Chief Operating Officer, the number two leadership position at the agency, assisting the Comptroller General in providing direction and vision for GAO's diverse, multidisciplinary workforce. -

Accounting and Reporting Manual for School Districts

Office of the NEW YORK STATE COMPTROLLER School Districts Accounting and Reporting Manual New York State Comptroller THOMAS P. DiNAPOLI AUGUST 2021 Updated August 2021 to reflect: Accounting Bulletin (revised November 2020) – Accounting and Financial Reporting for Fiduciary Activities as Required by GASB Statement 84 – Deleted the agency fund, updated the private- purpose trust fund, and added the custodial fund in chapters 2 and 4. Updated journal entry 31 to demonstrate how to account for payroll withholdings in the general fund and deleted journal entry 31b as agency funds are no longer active. Deleted all agency fund codes and added custodial fund codes and miscellaneous general fund codes in the account code appendix. Accounting Bulletin (July 2020) – Coronavirus Aid, Relief and Economic Security (CARES) Act Information – Added account code 4286 – Federal Aid, CARES Act Education Stabilization Fund in the account code appendix. Table of Contents PART I - Accounting and Reporting 1 Chapter 1 - Introduction 1 Chapter 2 - Basic Governmental Accounting Principles 3 Chapter 3 - Measurement Focus and Basis of Accounting 9 Chapter 4 - Funds and Supplemental Schedules 13 Chapter 5 - Classification and Coding Structure 17 Chapter 6 - Budgeting 23 Chapter 7 - Financial Reporting 28 Chapter 8 - Sample Journal Entries 30 PART II – APPENDIX 105 School District Account Codes 106 Contacts 158 Part I - Accounting and Reporting Chapter 1 - Introduction The Office of the State Comptroller (OSC) has compiled this manual as a comprehensive accounting guide for school district officials and others interested in accounting by school districts in New York State. It provides an overview of generally accepted governmental accounting and financial reporting principles, and OSC’s interpretations of such principles, where pronouncements are silent or do not address problems common among school districts within New York State.