RESTRICTED WT/TPR/S/325 13 October 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Critical Conceptualisation of Leadership and Organisational

A Critical Conceptualisation of Leadership And Organisational Change: The Case of Royal Jordanian Airline By Basil Obeidat Director of Studies: Dr Tom Baum Supervisor: Dr Austin Chakaodza 2020 Dedication Dedication My wife and children are dear to me. They have supported my ambition to become a qualified researcher. I am grateful for all their love and support. i | Page Acknowledgements Acknowledgements This research work has been possible with the expert direction and support provided by my Director of Studies Professor Tom Baum. Dr Austin Chakaodza provided the know-how guidance necessary to undertake PhD level research. I am grateful to them both, thank you. I should mention Professor Don Harper and Sheku Fofanah and the PhD Administration team who guided me through all the paperwork. ii | Page Abstract Abstract This present thesis is based on the critical conceptualisation of the leadership and the organisational change. Leadership is an action of the leading group of the people and company. It is a practical skill and research area that encompassing the ability of a person or company to lead other people in, team and firm. The organisational change is about the procedure of changing processes, culture, strategies and technologies of the company. It is a process under which a company make changes in its working methods and aim effectively, investigating the leadership style of the top management executives, including the Chief Executive Officer of Royal Jordanian airline to understand the factors that influence organisational cultural change within the company. There have been few studies of the Middle-Eastern situation that treats organisational cultural change in the development of an organisation in terms of the values of the company. -

Urban Growth Scenario Modeling

ّ سيناريوهات النمو ال َح رضي المملكة اﻷردنية الهاشمية 2018 Korea WORLD BANK GROUP Green Growth Trust Fund Urban Growth Scenarios for The Hashemite Kingdom of Jordan This is a project developed in coordination with the Ministry of Planning and International Cooperation (MoPIC) and the Ministry of Municipal Affairs (MoMA) to outline sustainable development paths for five Jordanian cities: Amman, Irbid, Mafraq, Russeifa and Zarqa. Duration: April to December 2017. 2 Objective To compare the environmental, social and economic impacts of different urban growth paths for five Jordanian cities to guide the identification, preparation and implementation of sustainable urban investment projects. Through the completion of the project, governments are expected to: • Create consensus with stakeholders. • Request funding from cooperation agencies. • Disseminate the potential benefits of their projects. • Test rough ideas and present solid proposals. • Convince others by providing numerical data. Land GHG Infrastructure Municipal consumption Energy emissions costs services costs 2 JD / capita km kWh/capita/annum kgCO2eq/capita/annum Millions of JD BAU 2 km kWh/capita/annum kgCO2eq/capita/annum Millions of JD JD / capita MODERATE 2 kWh/capita/annum Millions of JD JD / capita km kgCO2eq/capita/annum GROWTH COMPACT 2 km kWh/capita/annum kgCO2eq/capita/annum Millions of JD JD / capita VISION 4 Three steps in our methodology Identify problems and solutions, estimate indicators and disseminate the results Decision makers explain the A multidisciplinary team models Decision makers use the outputs to: problems that their city is the possible outcomes from the * Create consensus facing and the solutions that implementation of such * Request funding they are currently exploring. -

Solid Waste Value Chain Analysis Irbid and Mafraq Jordan

SOLID WASTE VALUE CHAIN ANALYSIS IRBID AND MAFRAQ JORDAN Mitigating the Impact of the Syrian Refugee Crisis on Jordanian Vulnerable Host Communities for UNDP Jordan June 2015 Solid Waste Value Chain Analysis Final Report Irbid and Mafraq – Jordan June 2015 TABLE OF CONTENTS LIST OF TABLES ......................................................................................................................... III LIST OF FIGURES .......................................................................................................................IV LIST OF ANNEXES .......................................................................................................................V LIST OF ABBREVIATIONS ..........................................................................................................VI 1.0 EXECUTIVE SUMMARY ...................................................................................................... 1 1.1 Waste Generation and Management ......................................................................... 1 1.2 Solid Waste Actors ...................................................................................................... 1 1.3 Solid Waste Value Chains ............................................................................................ 2 1.4 Solid Waste Trends ...................................................................................................... 2 1.5 Solid Waste Intervention Recommendations ............................................................. 3 1.6 Conclusion -

Business Guide

TOURISM AGRIFOOD RENEWABLE TRANSPORT ENERGY AND LOGISTICS CULTURAL AND CREATIVE INDUSTRIES BUSINESS GROWTH OPPORTUNITIES IN THE MEDITERRANEAN GUIDE RENEWABLERENEWABLERENEWABLERENEWABLERENEWABLE CULTURALCULTURALCULTURALCULTURALCULTURAL TRANSPORTTRANSPORTTRANSPORTTRANSPORTTRANSPORT AGRIFOODAGRIFOODAGRIFOODAGRIFOODAGRIFOOD ANDANDAND ANDCREATIVE ANDCREATIVE CREATIVE CREATIVE CREATIVE ENERGYENERGYENERGYENERGYENERGY TOURISMTOURISMTOURISMTOURISMTOURISM ANDANDAND ANDLOGISTICS ANDLOGISTICS LOGISTICS LOGISTICS LOGISTICS INDUSTRIESINDUSTRIESINDUSTRIESINDUSTRIESINDUSTRIES GROWTH GROWTH GROWTH GROWTH GROWTH OPPORTUNITIES IN OPPORTUNITIES IN OPPORTUNITIES IN OPPORTUNITIES IN OPPORTUNITIES IN THE MEDITERRANEAN THE MEDITERRANEAN THE MEDITERRANEAN THE MEDITERRANEAN THE MEDITERRANEAN ALGERIA ALGERIA ALGERIA ALGERIA ALGERIA BUILDING AN INDUSTRY PREPARING FOR THE POST-OIL PROMOTING HERITAGE, EVERYTHING IS TO BE DONE! A MARKET OF 40 MILLION THAT MEETS THE NEEDS PERIOD KNOW-HOW… AND YOUTH! INHABITANTS TO BE OF THE COUNTRY! DEVELOPED! EGYPT EGYPT EGYPT REBUILD TRUST AND MOVE EGYPT SOLAR AND WIND ARE BETTING ON THE ARAB UPMARKET EGYPT PHARAONIC PROJECTS BOOMING WORLD’S CULTURAL THE GATEWAY TO AFRICA ON THE AGENDA CHAMPION AND THE MIDDLE EAST IN ISRAEL SEARCH FOR INVESTORS ISRAEL ACCELERATE THE EMERGENCE ISRAEL TAKE-OFF INITIATED! ISRAEL OF A CHEAPER HOLIDAY COLLABORATING WITH THE THE START-UP NATION AT THE OFFER ISRAEL WORLD CENTRE OF AGRITECH JORDAN FOREFRONT OF CREATIVITY LARGE PROJECTS… AND START-UPS! GREEN ELECTRICITY EXPORTS JORDAN JORDAN IN SIGHT JORDAN -

Records Fall at Farnborough As Sales Pass $135 Billion

ISSN 1718-7966 JULY 21, 2014 / VOL. 448 WEEKLY AVIATION HEADLINES Read by thousands of aviation professionals and technical decision-makers every week www.avitrader.com WORLD NEWS More Malaysia Airlines grief The Airbus A350 XWB The US stock market fell sharply was a guest on fears of renewed hostilities of honour at after the news that a Malaysian Farnborough Airlines flight was allegedly shot (left) last week down over eastern Ukraine, with as it nears its service all 298 people on board reported entry date dead. US vice president Joe Biden with Qatar said the plane was “blown out of Airways later the sky”, apparently by a surface- this year. to-air missile as the Boeing 777 Airbus jet cruised at 33,000 feet, some 1,000 feet above a closed section of airspace. Ukraine has accused Records fall at Farnborough as sales pass $135 billion pro-Russian “terrorists” of shoot- Airbus, CFM International beat forecasts with new highs at UK show ing the plane down with a Soviet- era SA-11 missile as it flew from The 2014 Farnborough Interna- Farnborough International Airshow: Major orders* tional Airshow closed its doors Amsterdam to Kuala Lumpur. Airframer Customer Order Value¹ last week safe in the knowledge Boeing 777 Qatar Airways 50 777-9X $19bn Record show for CFM Int’l that it had broken records on many fronts - not least on total Boeing 777, 737 Air Lease 6 777-300ER, 20 737 MAX $3.9bn CFM International, the 50/50 orders and commitments for Air- Airbus A320 family SMBC 110 A320neo, 5 A320 ceo $11.8bn joint company between Snec- bus and Boeing aircraft, which ma (Safran) and GE, celebrated Airbus A320 family Air Lease 60 A321neo $7.23bn hit a combined $115.5bn at list record sales worth some $21.4bn Embraer E-Jet Trans States 50 E175 E2 $2.4bn prices for 697 aircraft - over 60% at Farnborough. -

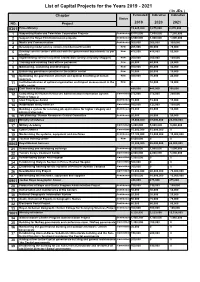

List of Capital Projects for the Years 2019 - 2021 ( in Jds ) Chapter Estimated Indicative Indicative Status NO

List of Capital Projects for the Years 2019 - 2021 ( In JDs ) Chapter Estimated Indicative Indicative Status NO. Project 2019 2020 2021 0301 Prime Ministry 13,625,000 9,875,000 8,870,000 1 Supporting Radio and Television Corporation Projects Continuous 8,515,000 7,650,000 7,250,000 2 Support the Royal Film Commission projects Continuous 3,500,000 1,000,000 1,000,000 3 Media and Communication Continuous 300,000 300,000 300,000 4 Developing model service centers (middle/nourth/south) New 205,000 90,000 70,000 5 Develop service centers affiliated with the government departments as per New 475,000 415,000 50,000 priorities 6 Implementing service recipients satisfaction surveys (mystery shopper) New 200,000 200,000 100,000 7 Training and enabling front offices personnel New 20,000 40,000 20,000 8 Maintaining, sustaining and developing New 100,000 80,000 40,000 9 Enhancing governance practice in the publuc sector New 10,000 20,000 10,000 10 Optimizing the government structure and optimal benefiting of human New 300,000 70,000 20,000 resources 11 Institutionalization of optimal organization and impact measurement in the New 0 10,000 10,000 public sector 0601 Civil Service Bureau 485,000 445,000 395,000 12 Completing the Human Resources Administration Information System Committed 275,000 275,000 250,000 Project/ Stage 2 13 Ideal Employee Award Continuous 15,000 15,000 15,000 14 Automation and E-services Committed 160,000 125,000 100,000 15 Building a system for receiving job applications for higher category and Continuous 15,000 10,000 10,000 administrative jobs. -

Entry Regulations to Jordan

Entry Regulations to Jordan Dear Trade Partners Greetings from Royal Jordanian Airlines. As received from Jordan Civil Aviation Regulatory Commission (JCARC), effective 09th of March 2021 and until 24th of March 2021 midnight, International scheduled flights are allowed to operate from/to Jordanian airports. Accordingly, the following to be applied on inbound flights: • Airlines are responsible to ensure that before boarding each passenger has negative PCR test conducted within 72 hours prior to the departure from the first embarkation airport, health insurance for Non-Jordanians, and install (AMAN Mobile App.). • Military passengers and their families are required to visit https://gateway2jordan.gov.jo to complete the required form and obtain the QR code which is mandatory for boarding • All QR code of passengers obtained before suspending valid • PCR test is required upon arrival, each passenger has to pay 28 JOD via electronic payment as follows: - Queen Alia International Airport – Amman (AMM): - https://registration.questlabjo.com/ - King Hussein International Airport – Aqaba (AQJ): - https://COVID19.biolab.jo - Amman Civil Airport – Marka (ADJ): - The amount will be collected directly in the Lab • Each passenger has to obtain a payment bill to show at check in counter before boarding, passenger who cannot pay through the links, the airline is responsible to collect the amount as EMD. • PCR test is not required for children below 5 years of age. • Diplomats and Employees of Regional and International Organizations (and their dependents -

Agent Name Mobile Address Mohd Hashim Saleh Parter Co 962791603734 Aqaba

Agent Name Mobile Address Mohd Hashim Saleh parter Co 962791603734 Aqaba - Aldofla St - Alalmyeh lumi market 962797620823 Tafileh - Rween lumi market 962797620823 Madaba - Jeser Madaba lumi market 962797620823 Amman - Marka lumi market 962797620823 Amman - Marka - Mkhabez Jwad lumi market 962797620823 Alghor - North Shoneh lumi market 962797620823 Irbid - Naaemh lumi market 962797620823 Tafeleh - Jaerf Aldrawesh lumi market 962797620823 Irbid - Main St lumi market 962797620823 Jarash - Bwabet Jarash lumi market 962797620823 Tafeleh - Uni St lumi market 962797620823 Karak - Thanieh lumi market 962797620823 Maan - Alsahrawi lumi market 962797620823 Ajloun - Aben lumi market 962797620823 Mafraq - Almadenh lumi market 962797620823 Deadsea - Aladsyeh lumi market 962797620823 Maan - Alshobak lumi market 962797620823 Amman - Almoqableen lumi market 962797620823 Amman - Twneb lumi market 962797620823 Amman - Jbeha lumi market 962797620823 Amman - Abdoun lumi market 962797620823 Salat - Alsaro 1 lumi market 962797620823 Salat - Alsaro 2 lumi market 962797620823 Amman - Jwydeh 1 lumi market 962797620823 Amman - Jwydeh 2 lumi market 962797620823 Amman - Shmesani lumi market 962797620823 Amman - Uni St lumi market 962797620823 Amman - Maca St lumi market 962797620823 Amman - Wadi Saqra lumi market 962797620823 Amman - Tabarbour lumi market 962797620823 Amman - Baqaa lumi market 962797620823 Amman - Sweleh lumi market 962797620823 Amman - Wadi Alseer lumi market 962797620823 Amman - Abdulah Ghosheh street lumi market 962797620823 Amman - alhezam St -

Twinning Fiche Project Title: Supporting Civil Aviation

Twinning Fiche Project title: Supporting Civil Aviation Regulatory Commission in the reinforcement of aviation security in Jordan Beneficiary administration: Civil Aviation Regulatory Commission (CARC), The Hashemite Kingdom of Jordan Twinning Reference: JO 17 ENI TR 04 20 Publication notice reference: EuropeAid/170904/ID/ACT/JO EU funded project TWINNING TOOL 1 Table of Contents Acronyms ................................................................................................................................................... 4 1. Basic Information .................................................................................................................................. 6 2. Objectives ............................................................................................................................................... 7 3. Description ......................................................................................................................................... 8 3.1 Background and justification ......................................................................................................... 8 3.2 Ongoing reforms .............................................................................................................................. 9 3.3 Linked activities ............................................................................................................................. 12 3.4 List of applicable Union acquis / Standards / Norms ................................................................. -

Academic Qualifications

Prof. Dr. Eng. Ali El-Naqa Curriclum Vitae Nationality Jordanian Date & Place of Birth Present 9/6/1965, Amman, Jordan Position & Profession Head of the Department of Water Management and Environment (1999- 2002), May 2004- 2005 Professor and Expert Engineer in Water Resources and Environment Address for Correspondence Work: Hashemite University, Jordan Dept. of Water Management & Environment Dept. of Earth & Environmental Sciences Tel. 962 5 3903333 (ext. 4231) Fax. 962 5 3826823 E-mail: [email protected] Home: Amman-Jordan Amman 11121, P.O.Box 8696 Tel. 00962-6-5512796, Mobile No . 00962-777439609 00962-799047033 Marital Status Married, one son and tw o daughter s Academic Qualifications 1994 Ph.D Groundwater Engineering, University of Ferrara, Italy. Fields : engineering geology and Hydrogeology Dissertation Title: Studio geologico-tecnico e geofisico della zona di imposta della diga e studio idrologico ed idrogeologico del suo bacino/ Giordania. "Geotechnical and geophysical study of Wadi Mujib Damsite and hydrological and hydrogeological study of its basin/Jordan". M.Sc. In Hydrogeology and Hydrochemistry, University of Jordan, Jordan. 1990 Fields : Hydrochemistry and Hydrogeology of Groundwaters. Dissertation Title : Hydrogeochemistry of groundwaters resources in the area between Wadi El-Yabis and Yarmouk River/ Jordan Valley area. B.Sc. Earth and Environmental Sciences, Yarmouk University, Jordan. 1987 Professional Experience 2010- Professor 2003-2005 Associate Professor Head of the Department of Water Management and Environmental Hashemite University – Jordan. Assistant Professor 1999-2002 Head of the Department Department of Water Management and Environmental, Institute of Lands, Water and Environment Hashemite University – Jordan. 1996-1998 Assistant Researcher Environment and Water Resources Research Unit Al al-Bayt University, Jordan 2/1996-8/1996 Geological Engineer Al -Remal Consulting Engineers, Amman, Jordan. -

Central Region Syrian Refugee Vulnerability

Central Region Syrian Refugee Vulnerability Basic Needs Vulnerability in Amman, Balqa, Madaba and Zarqa Basic Needs Vulnerability Rating (VAF) Ajloun Jarash Mafraq Average Scores Dair Alla Al-Ardha Hashemiyah Bierain Allan Dhlail Ain Albasha Zarqa Zarqa Salt Zarqa Salt Governorate EJC Al Jami'ah Balqa Russeifa Governorate Fuhais Low Moderate High Severe Amman Qasabah Marka Sahab Amman Yargha Azraq Wadi Essier Amman Quaismeh Governorate Azraq Azraq Shoonah Na'oor Dependancy Ratio Rating Coping Strategy Rating Janoobiyah Rajm al-Shami (Composite Indicator) (Composite Indicator) Average Scores Average Scores Muaqqar Hosba'n Um Elbasatien Jrainah Faisaliah Madaba Madaba Governorate m. Legend 85 K Madaba Camp/Refugee location Null B V Low a u Maeen s l n i c e N Moderate r a e b Low Moderate High Severe Low Moderate High Severe e i l d i High t s y Jizah Debt per capita Expenditure per capita Economic State Rating Severe Mlaih (Basic Indicator) (Basic Indicator) (Composite Indicator) 1 - 10 Average Scores Average Scores Average Scores 11 - 50 T o a t s a 51 - 100 s l e c s Areedh a s s 101 - 250 e e d s 251 - 500 501 - 750 Dieban > 750 Sub-district Um Al-Rasas Governorate Karak 0 2 4 8 Low Moderate High Severe Low Moderate High Severe Km. Low Moderate High Severe Production date: 14 May 2015 Feedback: please contact Koen Van Rossum on [email protected] produced by Central Region Syrian Refugee Vulnerability Education Vulnerability in Amman, Balqa, Madaba and Zarqa Ajloun Jarash Mafraq Dair Alla Al-Ardha Hashemiyah Bierain Allan Dhlail Ain -

JORDAN ECONOMIC GROWTH PLAN 2018 - 2022 the Economic Policy Council

JORDAN ECONOMIC GROWTH PLAN 2018 - 2022 The Economic Policy Council JORDAN ECONOMIC GROWTH PLAN 2018 - 2022 The Economic Policy Council EXECUTIVE SUMMARY Overview The JEGP is comprised of economic, fiscal and The Jordan sectoral strategies that outline the vision and Economic Growth policies pertaining to each sector. It further identifies the required policy interventions, Plan 2018 - 2022 public projects and private investments that must be undertaken to realize these sectoral (JEGP) is developed visions. A successful implementation of the IMF Extended Fund Facility Program (EFF) to recapture the along with the JEGP will put Jordan on a growth momentum sustainable growth trajectory and ensure its economic resilience in the face of regional and realize Jordan’s turmoil. development A successful implementation by the Government of Jordan of JEGP will double potential. the economic growth of Jordan over the coming five years, at the minimum, in spite of ongoing regional turbulence. 4 Jordan Economic Growth Plan 2018 - 2022 Executive Summary Jordan’s Economic Outlook Jordan has showcased its ability to remain Jordan’s GDP growth between 2000 and resilient, maintain internal cohesion, and 2009 averaged 6.5%, but from 2010 until reinvent itself in the face of adversity. The 2016, average growth was a mere 2.5%. combination of the global financial crisis Furthermore, Jordan’s total public debt has of 2009, Arab spring regional turbulence, increased at a rate exceeding economic energy crisis, closure of trade routes growth. This has resulted in a debt-to-GDP resulting in de facto economic siege (Exports ratio of 95% at the end of 2016, compared to Iraq amounted to 20% of Jordan’s total to approximately 61% in 2010.