New Challenges and the Future of Italian Superyacht Yards

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mediterranean Magic with Summer in the Mediterranean Fast Approaching, Unique Luxury Reveals the Luxury Sailing Mecca’S New Elite Hot Spots

Mediterranean Magic With summer in the Mediterranean fast approaching, Unique Luxury reveals the luxury sailing mecca’s new elite hot spots. By Bronwen Gora Porto de Soller, Mallorca 182 www.uniqueestates.com.au UniqueUnique Luxury Luxury 183 183 Reid from The Moorings. Such outfits offer the kind of super yachts Spa treatments excel at Monte Carlo’s Les Thermes Marin where used by celebrities and high net worth individuals who frequent the a day pass is available to a gym, pool and terrace, and ESPA in the Mediterranean. Ocean Alliance, for instance, has access to more than Metropole Hotel. Major Monaco attractions to include are the Princes 1,400 of the globe’s best, most opulent and modern vessels and motor Palace, the private residence of the ruling Prince, open to public this yachts available for charter. The Moorings also offers a full range of season from April 2nd to October 31st, and Saint Nicholas (or Monaco) craft, ranging from Beneteau to Leopard catamarans, all specifically Cathedral, where many of the Grimaldi’s, including Grace Kelly and built for charter and with so many mod cons they become a “home Rainier III, are buried. Away from the indoors, a must are Monaco’s away from home” says Mr Reid. Vessels can be provided with the magical gardens. services of a captain and as many staff as you choose, as well as The 7000 square metre Japanese gardens emulate a larger landscape gourmet chefs. with a hill, mountain, waterfall, beach and brook while the Jardin Elegantly appointed interiors, full facilities from simple DVD players to Exotique is on the side of a cliff and home to more than 1,000 cacti theatrettes, and of course the obligatory sundecks create the air of a species, a collection started at the turn of the 20th century. -

Amsterdam Your Superyacht Destination DISCLOSURE: All Rights Reserved

Amsterdam Your Superyacht Destination DISCLOSURE: All rights reserved. No part of the publication may be reproduced, stored in a retrieval system, or transmitted, in any form, by any means, mechanical photocopying, recording or otherwise, without the prior permission of the publisher. All information is provided in good faith. Port of Amsterdam and HISWA Holland Yachting Group take no legal responsibility for the accuracy, truthfulness or reliability of the information provided. 2 Introduction Dear reader, The appeal of Amsterdam as a destination for superyachts – both in its own right and as a port of call enroute to Scandinavia and beyond – is increasingly on the radar of superyacht owners and captains. Port of Amsterdam and HISWA Holland Yachting Group are working closely together with other parties turning Amsterdam into the superyacht hub of Northern Europe and beyond. Amsterdam’s prime geographical location and friendly regulatory environment for large yachts is backed up by superb mooring spots in the heart of the city and the rich diversity of leisure opportunities on offer. The city is ideally situated as a start or ending point for the Northern European Route. Moreover, the options for refits are growing fast and there is a dense web of superyacht building yards, designers and suppliers in close proximity of the city. Amsterdam is a city of great traditions and has a rich history. One of the traditions we embrace is the hand-over of the plaque and key of the city to ships during their first call. We continue this tradition for visiting superyachts. Captains and owners are pleased to receive this warm welcome and at the same time it gives us the opportunity to explain more about Amsterdam and the Northern European Route. -

Infrastructure Shipping and Navigation

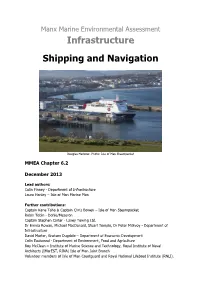

Manx Marine Environmental Assessment Infrastructure Shipping and Navigation Douglas Harbour. Photo: Isle of Man Steampacket MMEA Chapter 6.2 December 2013 Lead authors: Colin Finney - Department of Infrastructure Laura Hanley – Isle of Man Marine Plan Further contributions: Captain Kane Taha & Captain Chris Bowen – Isle of Man Steampacket Robin Tobin - Dohle/Mezeron Captain Stephen Carter - Laxey Towing Ltd. Dr Emma Rowan, Michael MacDonald, Stuart Temple, Dr Peter McEvoy - Department of Infrastructure David Morter, Graham Dugdale – Department of Economic Development Colin Eastwood - Department of Environment, Food and Agriculture Roy McClean – Institute of Marine Science and Technology, Royal Institute of Naval Architects (IMarEST, RINA) Isle of Man Joint Branch Volunteer members of Isle of Man Coastguard and Royal National Lifeboat Institute (RNLI). MMEA Chapter 6.2 – Infrastructure Manx Marine Environmental Assessment Version: December 2013 © Isle of Man Government, all rights reserved This document was produced as part of the Isle of Man Marine Plan Project, a cross Government Department project funded and facilitated by the Department of Infrastructure, Department of Economic Development and Department of Environment, Food and Agriculture. This document is downloadable from the Department of Infrastructure website at: http://www.gov.im/categories/planning-and-building-control/marine-planning/manx-marine- environmental-assessment/ For information about the Isle of Man Marine Plan Project please see: http://www.gov.im/categories/planning-and-building-control/marine-planning/ Contact: Manx Marine Environmental Assessment Isle of Man Marine Plan Project Planning & Building Control Division Department of Infrastructure Murray House, Mount Havelock Douglas, IM1 2SF Suggested Citations Chapter Finney, C., Hanley, L., Taha, K., Bowen, C., Tobin, R., Carter, S., Rowan, E., MacDonald, M., Temple, S., McEvoy, P., Morter, D., Dugdale, G., Eastwood, C., McClean, R. -

A Guide to Yacht Finance

A GUIDE TO YACHT FINANCE Those seeking to purchase a yacht or superyacht may often need to borrow the funds in order to buy it. But there are a number of other financially sound reasons to pursue this route, even if you have already amassed enough wealth to buy the asset in the first place. These include both practical and legal arguments ranging from running-cost benefits to tax advantages. In this article, Jonathan Hadley-Piggin provides a definitive guide to yacht finance. Jonathan Hadley-Piggin 020 3319 3700 [email protected] www.keystonelaw.co.uk REGISTRATION AND FLAG PREFERENCE A flag state is the country under whose laws a yacht is registered. This might be the country in which the owner lives or a ship registry in a country more synonymous with the complexities that surround charters and yacht ownership. Registration also grants the privilege and protection of flying the flag of that particular country. Every maritime nation, and even some land-locked countries such as Switzerland, has a system of ship registration that permits the registration of mortgages and other security interests. In 1993, a centralised UK registry replaced the system of individual registries in each major port. The centralised registry is divided into four separate parts, of which two are relevant to yachts: PART I PART III This is the main register consisting of merchant ships This is for small ships of under twenty-four metres and yachts alike. It is a full title register and has the in length. Known as the Small Ships Registry (abbr. -

MONACO YACHT SHOW 2019 Intelligence Report by Superyacht

Visit us at stand QH12 MONACO YACHT SHOW 2019 Intelligence Report by SuperYacht Times Yachts At The Monaco Evolution Of Yachts At Yacht Show 2019 The Monaco Yacht Show: Bigger And Better SuperYacht Times is proud to be the official intelligence partner of the Monaco Yacht Show. As such, we also like to dig into the data of the superyacht fleet on display at the show. This year’s Monaco Yacht Show will see over 125 yachts on display. At the time of writing, the display of at At SuperYacht Times, we have compiled lists of yachts present at the Monaco Yacht Show on our least 108 superyachts over 30 metres in length had been confirmed. Expect more superyachts website for each edition of the show since 2015. As the composition of the 2019 fleet is not yet final, to be confirmed as we get closer to the show’s start as there are usually around 109 superyachts we cannot yet compare it to earlier shows. However, we have compiled statistics over the previous over 30 metres on display at the show. four years (2015-2018). What do they tell us? PRELIMINARY STATISTICS 30M+ FLEET ON DISPLAY AT MONACO YACHT SHOW 2019 WHAT IS THE SHARE OF SAILING YACHTS? While the total size of the fleet over 30 metres present at the show is always roughly the same due 4 YEARS 8 YEARS €37.8 MILLION 500 DAYS to the size limitations of the port (around 109 superyachts), the mix of yachts varies quite a bit. The share of sailing yachts in the fleet on display has gone up and down significantly over the past Average age Average age Average asking price Yachts for sale on display at four years, from a high of 17 yachts, or 16% of the fleet, in 2016, to a low of nine yachts, or 8% of of motor of sailing of yachts available for the Monaco Yacht Show 2019 yachts yachts sale at Monaco Yacht have been on the market for an the fleet, in 2017. -

World Commerce Review Monaco Yacht Show Review

Monaco Yacht Show WORLD COMMERCE2018 Preview REVIEW THE ISLE OF MAN, THE WHAT CAN YOU EXPECT THE POOL OF TALENTED PLACE FOR MARITIME FROM MYS2018? SEAFARERS IS DRYING UP BUSINESS THE GLOBAL TRADE PLATFORM “Aviation Malta - Open for Business” The Malta Business Aviation Association (MBAA) aims to promote excellence and professionalism amongst our Members to enable them to deliver best-in-class safety and operational efficiency, whilst representing their interests at all levels in Malta and consequently Europe. The MBAA will strive to ensure recognition of business aviation as a vital part of the aviation infrastructure and the Maltese economy. MBAAMALTA BUSINESS AVIATION ASSOCIATION a: 57, Massimiliano Debono Street, Lija, LJA 1930, Malta t: +356 21 470 829 | f: +356 21 422 365 | w: www.mbaa.org.mt | e: [email protected] Foreword elcome to the WCR Monaco Yacht Show 2018 ePub. www.worldcommercereview.com WAnother year and another MYS, and as always World Commerce Review is covering the event in-depth with comment and reviews, so welcome to you all. Once again the MYS brings together the best of the yachting and aviation industry and their clients. This is a great opportunity for all those involved in the sector to network and discuss ongoing opportunities. You will note that we have a wide range of editorial contributions from some of the most innovative and leading companies in the industry. We hope that you will find this stimulating and informative.■ www.worldcommercereview.com CONTENTS A luxury guide to MYS 2018 What can you expect -

MSN 054 Isle of Man LY3 National Annex Issued: Jan 2019

Isle of Man Ship Registry Manx Shipping Notice Red Ensign Group Yacht Code & Ref. MSN 054 Isle of Man LY3 National Annex Issued: Jan 2019 1. Introduction This MSN advises of the new Red Ensign Group Yacht Code and also includes the National Annex for yachts constructed to LY1, LY2 or LY3. 2. Red Ensign Group (REG) Yacht Code The Red Ensign Group Yacht Code was launched on 13th November 2017 at the Global Superyacht Forum in Amsterdam. The Isle of Man (IoM) Ship Registry’s Regulations to apply the REG Yacht Code Part A and the Common Annexes entered into force on 01st January 2019. A link to the REG Yacht Code is available on the Red Ensign Group’s website. The REG Yacht Code Part A applies in its entirety to all commercial yachts of 24 metres in load line length or over, constructed on or after 01 January 2019 which are permitted to carry a maximum of 12 passengers. There are also additional requirements stated in Chapter 1.6 of the REG Yacht Code Part A, which existing commercial yachts must comply with prior to their first annual survey after 1st January 2019. However these yachts may continue to be surveyed in accordance with the Code they were constructed under (LY1, LY2 or LY3). The REG Yacht Code includes a set of Common Annexes which include many of the technical requirements for commercial yachts, for example battery systems, over-side working and helicopter landing areas. The REG Yacht Code Part B is the Passenger Yacht Code, up to 36 passengers. -

Tenders & Toys Guide

OCTOBER 2016 TRUTH • OPINION KNOWLEDGE • IDEAS & SUPERYACHT OWNER INSIGHT KORMARAN Luxury transformed – a class of its own SPECIFICATIONS e essence of the Kormaran is to transform, to convert itself. To perfectly adjust to every situation. e KORMARAN K7 First Edition combines optimum comfort with safety, power LOA: 7,1M and elegance. Whether gliding, driving or ying the K7 FE, unique experiences and driving BEAM: 1,7M - 3,7M sensations can be expected. DRAUGHT: 0,4M e transformation system is a groundbreaking innovation, allowing the Kormaran to change TOP SPEED: 70KMH / 38KNOTS the distance between the hulls and the height of the central passenger cabin. In this way it RANGE: 200KM / 108NM allows the variability and the multifunctionality of the vessel. WEIGHT: 1,5T / 2,0T While conventional boats cannot change their characteristics, the Kormaran can transform ENGINES: 2 / 3 X 300HP even while in motion, elegantly combining the agility of a monohull for quick manoevres with ROTAX JET PROPULSION the stability of a catamaran or trimaran. In addition, the K7 FE can gracefully transform into a DELIVERY TIME: 12 MONTHS large sunbathing island, without compromising transport or storage space. Wilhelm-Spazier Str. 2a, A-5020 Salzburg, Austria T: +43 662 828886 500 E: [email protected] W: www.kormaran.com TENDERS & TOYS GUIDE All your tenders, all your toys Tenders Toys and much more... BUILD | DELIVERY | AFTER-SALES | BROKERAGE | SLIDES | JET SKIS | SEABOBS | FLYBOARDS | & LOTS MORE Contact | UK: +44 2380 01 63 63 | FR: +33 489 733 347 -

Global Superyacht Transport

Contact info: Exceeding Expectations UK (Head Offi ce) in Superyacht transport +44 (0) 2380 480 480 [email protected] www.petersandmay.com Our global offi ces include: UK (Head Offi ce) | USA | France | Spain | Italy | Germany | Netherlands | Dubai | Hong Kong | Singapore SM7013 superyacht Brochure.indd 1-2 08/01/2019 16:16 Superyacht Shipping is an essential part of Peters & May’s global business The shipment of yachts and motor boats of this Exceeding expectations size and weight requires additional handling from the outset. Peters & May uses specifi c in commercial transport lifting equipment suitable for heavy lifting, the best cradling systems and the fi nest people in With Peters & May’s long history, we can be the industry to oversee all procedures from trusted to deliver and exceed the expectations start to fi nish. Peters & May understands the of clients by providing a level of service that importance of having specially trained staff to warrants the reputation of our brand. Peters & oversee every part of the shipping process, May continues to be the world’s most especially the loading and unloading of these respected marine shipping consultant and unique yachts. logistics provider. Being completely Head offi ce personnel are committed to independent of any carrier association, we are supplying not just a quotation but a proposal best placed to provide clients with shipping to demonstrate how the equipment is used opportunities that meet both their budgetary and an outline of the operations procedures. requirements and date expectations. This proposal will always include references to past work carried out by Peters & May. -

The Ultimate Guide for First-Time Charterers

THE ULTIMATE GUIDE FOR FIRST-TIME CHARTERERS THE CHARTER EXPERTS OF NORTHROP & JOHNSON THE AUTHORITY ON YACHTING FIRST-TIME CHARTER GUIDE 02 SINCE 1949 NORTHROP & JOHNSON THE ULTIMATE GUIDE FOR FIRST-TIME CHARTERERS As more and more travelers seek out luxury vacation options that ensure exclusivity, security and peace of mind, many are opting for a luxury yacht charter. With its ultra-hygienic and self-sustaining environment, a luxury yacht charter is a safe sanctuary and affords guests a worry-free vacation. As such, Northrop & Johnson has seen an influx of inquiries from first-time charterers looking for new and cautious ways to travel. Our charter brokers have a wealth of expertise and wide variety of skills to assist first-time charterers every step of the way. Knowing that first-timers will have many questions, Northrop & Johnson’s charter brokers have compiled a guide to help you gain a better understanding of the yacht charter process. Please peruse our guide, which covers some of the most important things you need to know about yacht charter, as you prepare for a conversation with your charter broker. Wishing you a very memorable trip and smooth sailing! Cheers, DANIEL ZIRIAKUS President & COO, Northrop & Johnson YACHT CHARTER 101 THE AUTHORITY ON YACHTING FIRST-TIME CHARTER GUIDE 04 SINCE 1949 NORTHROP & JOHNSON What is yacht charter? —— Whether you are looking for a family vacation in the Caribbean, an island-hopping adventure, or a safe and secure environment to celebrate with friends, a superyacht charter means doing things your way – your own timetable, bespoke itinerary, and favorite past-times in absolute luxury. -

Background to the Large Yacht Code

Background to the Large Yacht Code The UK’s Maritime and Coastguard Agency’s “Code of Practice for the Safety of Large Commercial Sailing and Motor Vessels”, or LY1, and sometimes known as “The Megayacht Code”, was introduced in 1998. The Code applied to vessels in commercial use for sport or pleasure, which are 24 metres in “load line” length and over. Or, if they were built before July 1968, are 150 gross tons (GT) and over, according to the tonnage measurement regulations at that date. Such vessels are not permitted to carry cargo, or more than 12 passengers. The code sets standards of safety and pollution prevention, which are appropriate to the size and operation of the vessel. For vessels of this size, standards are normally set by the relevant international conventions. The Code provides equivalent standards, as permitted by these conventions where it is not reasonable or practical to comply with the prescriptive requirements of the international convention. It was recognised that LY1 would have to be revised to take account of advances in technology and changes of practice. This revision took place in consultation with the Large Yacht Industry. All comments from that consultation were considered by working groups comprising experts from the international large yacht industry. LY2 The new Code, now known as “The Large Commercial Yacht Code”, or LY2, came into effect on 24th September 2004. The Code recognises that vessels in commercial use for sport or pleasure do not fall naturally into a single classification and prescribed merchant ship safety standards may be incompatible with the safety needs particular to such vessels. -

The Global Order Book (GOB) Is the Superyacht

Business 2019 Data and research – Raphael Montigneaux & Marilyn Mower; ofInfographics – Valerioy Pellegrini;achtin Photography - Silvano Pupella g The Global Order Book (GOB) is the superyacht industry’s trusted annual health check; a deep-dive examination of global boatbuilding that logs the number of yachts over 24 metres either on order or in build anywhere around the world. This year, Boat International has introduced a new standard of data verification in compiling an even more accurate GOB than usual. We have logged more than 20,000 kilometres visiting shipyards, meeting contractors and checking the status of announced projects – and deleting many “on-hold” ones. Read on for an unparalleled snapshot of what’s happening in the world of boatbuilding in 2018 – and what to expect in the years to come. www.boatinternational.com | January 2019 <#x#> <#y#> GLOBAL ORDER BOOK 2019 2019 GLOBAL ORDER BOOK 12 FRANCE 06 3 UK 2 NETHERLANDS 9 NORWAY 19 SWEDEN Total length: 198m Total length: 3,126m Total length: 4,667m Total length: 353m Total length: 109m Number of projects: 5 Number of projects: 109 Number of projects: 75 Number of projects: 3 Number of projects: 3 Average length: 40m Average length: 29m Average length: 62m Average length: 118m Average length: 36m 14 FINLAND The top 20 builder nations and what they have in store... Total length: 176m Number of projects: 5 The big picture Average length: 35m 20 POLAND Total length: 70m 4 TURKEY 15 AUSTRALIA Number of projects: 2 Total length: 3,000m Total length: 170m Average length: 35m Number