SEC 17-A 2016 Annual Report -CHI Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Memorandum of Agreement

LIST OF POWER MAC CENTER PARTICIPATING REDEMPTION OUTLETS BRANCH (METRO MANILA) ADDRESS 1 Ayala Malls Cloverleaf 2/L Ayala Malls Cloverleaf, A. Bonifacio Ave., Brgy. Balingasa, Quezon City 2 Circuit Lane G/L Ayala Malls Circuit Lane, Hippodromo, Makati City 3 Festival Supermall UGF Expansion Area, Festival Supermall, Filinvest City, Alabang, Muntinlupa City 4 Glorietta 5 3/L Glorietta 5, Ayala Center, Makati City 5 Greenbelt 3 2/L Greenbelt 3, Ayala Center, Makati City 6 Power Plant Mall 2/L Power Plant Mall, Rockwell Center, Poblacion, Makati City 7 SM Aura Premier 3/L SM Aura Premier, 26th St. Corner McKinley Parkway, Bonifacio Global City, Taguig City 8 SM City Bacoor 4/L Cyberzone, SM City Bacoor Gen. Aguinaldo Cor. Tirona Bacoor, Cavite 9 SM City BF Parañaque 3/L Cyberzone, SM City BF Paranaque, Dr. A. SantoS Ave., Brgy. BF HomeS, Paranaque City 10 SM City Dasmariñas 2/L Cyberzone, SM City DaSmarinaS Brgy. Sampaloc 1, DaSmarinaS City, Cavite 11 SM City Fairview 3/L Cyberzone, SM Fairview, Brgy. Greater Lagro, Quezon City 12 SM City Marikina G/L SM City Marikina, Marcos Highway, Marikina City 13 SM Mall of Asia 2/L SM Mall of Asia, Central Business Park Bay Blvd., Pasay City 14 SM Megamall 4/L Cyberzone, SM Megamall Bldg. B, EDSA, Mandaluyong City 15 SM South Mall 3/L Cyberzone, SM Southmall, Alabang Zapote Road, LaS PinaS City 16 The Annex at SM City North EDSA 4/L Cyberzone, Annex Bldg at SM City North EDSA, Quezon City 17 The Podium 3/L The Podium, 18 ADB Avenue, Ortigas Center, Mandaluyong City 18 TriNoma 3/L Mindanao Wing, TriNoma, Quezon City BRANCH (PROVINCIAL) ADDRESS 1 Abreeza Mall 2/L Abreeza Ayala Mall, J.P. -

SEC 17-A 2015 Annual Report -CHI Pdf

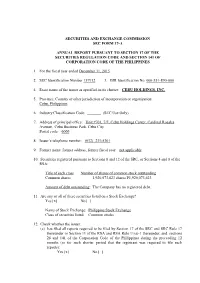

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2015 2. SEC Identification Number 157912 3. BIR Identification No. 000-551-890-000 4. Exact name of the issuer as specified in its charter: CEBU HOLDINGS, INC. 5. Province, Country or other jurisdiction of incorporation or organization: Cebu, Philippines 6. Industry Classification Code: _______ (SEC Use Only) 7. Address of principal office: Unit #701, 7/F, Cebu Holdings Center, Cardinal Rosales Avenue, Cebu Business Park, Cebu City Postal code: 6000 8. Issuer’s telephone number: (032) 231-5301 9. Former name, former address, former fiscal year: not applicable 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sections 4 and 8 of the RSA: Title of each class Number of shares of common stock outstanding Common shares 1,920,073,623 shares P1,920,073,623 Amount of debt outstanding : The Company has no registered debt. 11. Are any or all of these securities listed on a Stock Exchange? Yes [x] No [ ] Name of Stock Exchange: Philippine Stock Exchange Class of securities listed: Common stocks 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and sections 26 and 141 of the Corporation Code of the Philippines during the preceeding 12 months (or for such shorter period that the registrant was required to file such reports): Yes [x] No [ ] (b) has been subject to such filing requirements for the past 90 days: Yes [x] No [ ] 13. -

2020 Annual Report (Pdf)

ANNUAL REPORT 2020 Contents COMPANY PROFILE 3 Financial Highlights 4 Project Location Map 5 Directory 6 MESSAGE TO SHAREHOLDERS OUR BUSINESS UNITS 11 Commercial Centers Division 13 Residential Division 16 Office Buildings Division 18 Hotels & Resorts Division 20 Industrial & Integrated Developments Division 21 Chengdu Ban Bian Jie CORPORATE SOCIAL RESPONSIBILITY 23 RLove Program 25 Environment & Sustainability 27 Robinsons Mall Gift of Change CORPORATE GOVERNANCE 30 Our Commitment to Good Governance 33 The Board of Directors - Responsibilities and Composition 37 Enterprise Risk Management, Accountability, and Audit 40 Other Matters 42 BOARD OF DIRECTORS 43 AUDITED FINANCIAL STATEMENTS Financial Highlights For the Years ended December 31 2014 2015 2016 2017 2018 2019 2020 (in million pesos) Gross Revenues 17,460.22 20,306.91 22,809.05 22,516.82 29,545.31 30,583.84 25,404.83 Net Income 4,773.87 5,952.94 5,755.32 5,884.44 8,223.96 8,692.61 5,259.36 Total Assets 88,421.50 111,711.51 124,432.16 148,126.55 174,158.16 189,651.21 215,200.73 Stockholders' Equity 53,968.36 58,444.74 62,855.31 67,372.62 93,919.72 100,077.67 102,718.03 GROSS REVENUES TOTAL ASSETS (in billion pesos) (in billion pesos) 40 250 215.20 29.56 30.58 189.65 25.40 200 174.16 30 22.81 22.52 148.13 150 124.43 20 100 10 50 - - 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 NET INCOME STOCKHOLDERS' EQUITY (in billion pesos) (in billion pesos) 8.69 10 8.22 150 8 102.72 100.08 5.76 5.88 100 93.92 6 5.26 67.37 62.86 4 50 2 - - 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 -

CEBU | OFFICE 1Q 2018 9 March 2018

Colliers Bi-Annual CEBU | OFFICE 1Q 2018 9 March 2018 Offshore Forecast at a glance Demand Total office transactions reached nearly gambling rises 107,000 sq m (1.2 million sq ft) in 2017. Offshore gambling is an emerging office Joey Roi Bondoc Research Manager segment and we see greater absorption from this sector over the next two to three years. The continued demand from Offshore gambling is emerging as a critical segment BPO and KPO firms should support at of the Cebu office market as it accounted for almost least a 10% annual growth in 25% of recorded transactions in 2017. Business transactions until 2020. Process Outsourcing(BPO)-Voice companies continue to dominate covering more than a half of Supply transactions while the Knowledge Process We see Cebu's office stock breaching Outsourcing (KPO) firms that provide higher value the 1 million sq m (10.8 million sq ft) services also sustained demand, taking 20% of the mark this year. Between 2018 and 2020, total office leases. Colliers sees the current we expect the completion of close to administration's infrastructure implementation and 400,000 sq m (4.3 million sq ft) of new office space. A combined 60% of the decentralization thrust benefiting Cebu as it is the new supply will be in Cebu Business largest business destination outside Metro Manila. Park (CBP) and Cebu IT Park (CITP). This should entice more offshore gambling, BPO, KPO and traditional firms to set up shop or expand Vacancy rate operations. We encourage both landlords and Overall vacancy in Cebu stood at 9.7% tenants to as of end-2017.This is lower than the 12% recorded at end-2016. -

Professional Regulation Commission Cebu Medical Technologist January 21 - 22, 2021

PROFESSIONAL REGULATION COMMISSION CEBU MEDICAL TECHNOLOGIST JANUARY 21 - 22, 2021 School : BENEDICTO COLLEGE - CEBU CITY CAMPUS Address : DON BERNARDO BENEDICTO ST. RECLAMATION CEBU CITY, CEBU (BESIDE ROBINSONS GALLERIA CEBU) Building : Floor : 4TH Room/Grp No. : 401 Seat Last Name First Name Middle Name School Attended No. 1 ABA ALVIN SY SOUTHWESTERN UNIVERSITY 2 ACEDO JESSA MARIA CALAMBA HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 3 ACIDO FRANCIS XAVIER TAMAYO VELEZ COLLEGE 4 ADIONG CHRISTINE ORAIZ SOUTHWESTERN UNIVERSITY 5 AGERO MARIAN OLGA COLUMNAS SOUTHWESTERN UNIVERSITY 6 ALBUERA SHEENA ROSS AWIT VELEZ COLLEGE 7 ALIVIO FE ANIANNE JAGUROS VELEZ COLLEGE 8 ALVEZ RULE PERNITO SOUTHWESTERN UNIVERSITY 9 AMORGANDA LLOYD CABIARA VELEZ COLLEGE REMINDER: USE SAME NAME IN ALL EXAMINATION FORMS. IF THERE IS AN ERROR IN SPELLING AND OTHER DATA KINDLY REQUEST YOUR ROOM WATCHERS TO CORRECT IT ON THE FIRST DAY OF EXAMINATION. REPORT TO YOUR ROOM ON OR BEFORE 6:30 A.M. LATE EXAMINEES WILL NOT BE ADMITTED. PROFESSIONAL REGULATION COMMISSION CEBU MEDICAL TECHNOLOGIST JANUARY 21 - 22, 2021 School : BENEDICTO COLLEGE - CEBU CITY CAMPUS Address : DON BERNARDO BENEDICTO ST. RECLAMATION CEBU CITY, CEBU (BESIDE ROBINSONS GALLERIA CEBU) Building : Floor : 4TH Room/Grp No. : 402 Seat Last Name First Name Middle Name School Attended No. 1 ANDIT FEGEE ANN GOLOAN SOUTHWESTERN UNIVERSITY 2 ANDO QUENCY GIGANTO SOUTHWESTERN UNIVERSITY 3 ANDOY JOMELLE ANGELLA POYAOAN HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 4 ANGANA CATHARD GRACE ESCRIBANO VELEZ COLLEGE 5 ANNUAL RADZMALYN AJIJUL MINDANAO MEDICAL FOUNDATION COLLEGE 6 APOSTOL PATRICIA RALDINE SERAFIN OUR LADY OF FATIMA UNIVERSITY-VALENZUELA 7 ARANAS TRIXIA CASTINO HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 8 ARASAN CYRIL ABEJARON HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 9 ARELLANO MARK OMBOY SOUTHWESTERN UNIVERSITY REMINDER: USE SAME NAME IN ALL EXAMINATION FORMS. -

Where to Buy Yazz

WHERE TO BUY YAZZ YAZZ STORE PARTNERS Bahayang Pag-Asa Market Ground Floor Bahayang Pag-asa Market, Imus, Cavite Autohide Autoload Panganiban Drive, Naga CIty Emall – Cloudfone Kiosk GF Emall Elias Angeles St. Penafrancia Ave. Naga City Kooky N Luscious G/F MCC Building Ayala Ave Makati CIty Pacific Mall Lucena Viewerss Mobile 2f (M.L Tagarao St.), Lucena City Viewers Mobile Gadgets Quezon Ave. Lucena City CD-R KING BRANCHES BRANCH NAME ADDRESS Alabang Town Center-under 3/f alabang town center brgy. ayala alabang renovation until May 31 muntinlupa city Upper Ground Floor Alimall, Araneta Center Alimall Cubao, Brgy. Socorro, Quezon City Anonas LRT City Center, Aurora Blvd., Brgy. Anonas LRT Bagumbuhay, Quezon City 3rd Floor Stall 312 , Ayala Center Cebu, Bus. Park, Ayala Cebu Cebu City (Capital), Cebu, 6000, Central Visayas Unit S10-12 Bluewave Strip Mall, marikina, Bluewave Strip Mall Sumulong Highway, Marikina City 2nd Floor Cash & Carry Mall, South Super Cash and Carry Highway cor. Filmore St. Palanan Makati City. 3rd Floor Centrio Mall CM Recto Avenue, Cagayan De Oro City (Capital), Misamis Centrio Mall CDO Oriental, 9000, Northern Mindanao Dela Rosa Carpark 1, Delarosa Street, Legaspi Dela Rosa Carpark 1 – Makati Village, Makati City 2/F EDSA Central Pavillion, Edsa cor Shaw Blvd. Edsa Central Brgy. Highway Hills,Mandaluyong City 3rd Floor Elizabeth Mall Corner N. Bacalso Leon Kilat Street, Cebu City (Capital), Cebu, 6000, E-mall Cebu Central Visayas Unit L2-212 Nagaland Elizabeth-Mall, Elias Angeles Street San Francisco, Naga City, E-Mall Nagaland Camarines Sur, 4400, Bicol Region SF 16 &17, 2nd Floor Centris Station, Quezon E-ton Centris-under renovation Ave.,Pinyahan Quezon City 2/F Ever Gotesco Commonwealth, Ever Commonwealth Commonwealth Ave., Batasan Hills, Quezon City Fairview Terraces Level 3 Fairview Terraces Quirino Highway Pasong Putik Novaliches Quezon City Ground Floor New Farmers Plaza, Araneta Farmers Center Cubao, Brgy. -

Metro Cebu Market Update 2H 2018

RESEARCH METRO CEBU MARKET UPDATE 2H 2018 METRO CEBU REAL ESTATE SECTOR REVIEW CEBU REGAINS ATTRACTIVENESS AS A GO-TO SPOT FOR BUSINESS AND LEISURE ACTIVITIES COVER | Investments and Tourism further drive Metro Cebu’s growth in the second half of 2018 Heavy business and construction investments is noted in the fringes Exciting investment prospects activities in Metro Cebu are and surrounding cities. A great deal abound Metro Cebu, backed by the primarily observed in three of the of business and investments continuously growing local and area’s major cities, Cebu City, activities have been detected in regional economy, newly opened Mandaue City and Lapu-Lapu City. Mandaue City in particular. The Mactan-Cebu International Airport Cebu City has consistently been property sectors in Mandaue were (MCIA) and other proposed one of the preferred outsourcing perceived to be growing at a government infrastructure destinations in the world. Coming remarkable rate, following the low developments. Bridges designed to from the 12th spot in 2017, Cebu vacancies and almost full saturation connect Cebu to the other nearby City rose a level up to the 11th spot of Cebu City. islands, such as Bohol and Negros, of the latest Top 100 Super Cities are expected to further enhance the list released by Tholons, a Aside from boasting of a good ease of doing business between renowned international strategic business environment, Cebu Metro Cebu and adjacent areas. In advisory firm. The competitive talent continues to attract local and addition, road networks in the pool and cheap labor cost remain foreign tourists with the various pipeline will facilitate a smoother as major considerations in choosing leisure activities that could be done travel experience from Danao City in Cebu City over other locations. -

CIS BAYAD CENTER, INC. List of Partners As of February 2020*

CIS BAYAD CENTER, INC. List of partners as of February 2020* NO. BRANCH NAME ADDRESS BCO 1 BAYAD CENTER - BACOLOD COKIN BLDG. LOPEZ JAENA ST.,BACOLOD CITY, NEGROS OCCIDENTAL 2 BAYAD CENTER - BACOOR BACOOR BOULEVARD, BRGY. BAYANAN, BACOOR CITY HALL, CAVITE 3 BAYAD CENTER - CABANATUAN 720 MARILYN BLDG., SANGITAN ESTE, CABANATUAN CITY, NUEVA ECIJA 4 BAYAD CENTER - CEBU CAPITOL 2nd FLR., AVON PLAZA BUILDING, OSMENA BOULEVARD CAPITOL. CEBU CITY, CEBU BAYAD CENTER - DAVAO CENTER POINT 5 PLAZA ATRIUM CENTERPOINT PLAZA, MATINA CROSSING, DAVAO DEL SUR 6 BAYAD CENTER - EVER COMMONWEALTH 2ndFLR., EVER GOTESCO MALL, COMMONWEALTH AVE., QUEZON CITY 7 BAYAD CENTER - GATE2 EAST GATE 2, MERALCO COMPLEX, ORTIGAS, PASIG CITY 8 BAYAD CENTER - GMA CAVITE 2ND FLR. GGHHNC 1 BLDG., GOVERNORS DRVE, BRGY SAN GABRIEL, GMA, CAVITE 9 BAYAD CENTER - GULOD 873 QUIRINO HWAY,GULOD,NOVALICHES, QUEZON CITY 10 BAYAD CENTER - KASIGLAHAN MWCI.SAT.OFFICE, KASIGLAHAN VIL.,BRGY.SAN JOSE,RODRIGUEZ, RIZAL SPACE R-O5 GROUND FLR. REMBRANDT BLDG. LAKEFRONT BOARDWALK, PRESIDIO 11 BAYAD CENTER - LAKEFRONT LAKEFRONT, SUCAT, MUNTINLUPA CITY 12 BAYAD CENTER - LCC LEGAZPI 4TH FLR. LCC MALL, BRGY.DINAGAAN, LEGASPI CITY, ALBAY 13 BAYAD CENTER - LIGAO GROUND FLR. MA-VIC BLDG, SAN ROQUE ST., BRGY. DUNAO, LIGAO CITY, ALBAY MAYNILAD LAS PIÑAS BUSINESS CENTER, MARCOS ALVAREZ AVE. TALON UNO, LAS PIÑAS 14 BAYAD CENTER - M. ALVAREZ CITY 15 BAYAD CENTER - MAYNILAD ALABANG 201 UNIVERSITY AVE., AYALA ALABANG VILLAGE, BRGY. AYALA ALABANG, MUNTINLUPA CITY 16 BAYAD CENTER - MAYSILO 479-F MAYSILO CIRCLE, BRGY. PLAINVIEW, MANDALUYONG CITY LOWER GROUND FLR., METRO GAISANO SUPERMARKET, ALABANG TOWN CENTER, ALABANG- 17 BAYAD CENTER METRO - ALABANG ZAPOTE ROAD, ALABANG, MUNTINLUPA CITY GROUND FLOOR,MARQUEE MALL BLDG, DON BONIFACIO ST., PULUNG MARAGUL, ANGELES 18 BAYAD CENTER METRO - ANGELES CITY 19 BAYAD CENTER METRO - AYALA AYALA CENTER, CEBU ARCHBISHOP REYES AVE., CEBU BUSINESS PARK, CEBU CITY 20 BAYAD CENTER METRO - AYALA FELIZ MARCOS HI-WAY, LIGAYA, CORNER JP RIZAL, PASIG CITY 21 BAYAD CENTER METRO - BANILAD A.S FORTUNA CORNER H. -

Securities and Exchange Commission Sec Form 17-C

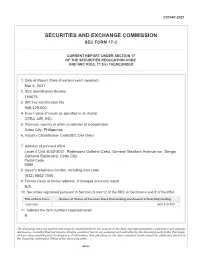

C01447-2021 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2(c) THEREUNDER 1. Date of Report (Date of earliest event reported) Mar 5, 2021 2. SEC Identification Number 154675 3. BIR Tax Identification No. 948-229-000 4. Exact name of issuer as specified in its charter CEBU AIR, INC. 5. Province, country or other jurisdiction of incorporation Cebu City, Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office Level 4 Unit 4030-4031, Robinsons Galleria Cebu, General Maxilom Avenue cor. Sergio Osmena Boulevard, Cebu City Postal Code 6000 8. Issuer's telephone number, including area code (632) 8802-7000 9. Former name or former address, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 600,316,700 11. Indicate the item numbers reported herein 9 The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Cebu Air, Inc. CEB PSE Disclosure Form 4-30 - Material Information/Transactions References: SRC Rule 17 (SEC Form 17-C) and Sections 4.1 and 4.4 of the Revised Disclosure Rules Subject of the Disclosure Cebu Air, Inc. -

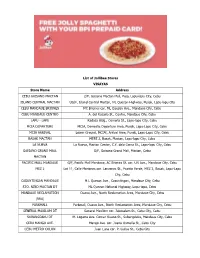

List of Jollibee Stores VISAYAS Store Name Address CEBU GAISANO

List of Jollibee Stores VISAYAS Store Name Address CEBU GAISANO MACTAN 2/F, Gaisano Mactan Mall, Pajo, Lapu-lapu City, Cebu ISLAND CENTRAL MACTAN UG/F, Island Central Mactan, ML Quezon Highway, Pusok, Lapu-lapu City CEBU MANDAUE BRIONES MC Briones cor. ML Quezon Ave., Mandaue City, Cebu CEBU MANDAUE CENTRO A. del Rosario St., Centro, Mandaue City, Cebu LAPU - LAPU Radaza Bldg., Osmeña St., Lapu-lapu City, Cebu MCIA DEPARTURE MCIA, Domestic Departure Area, Pusok, Lapu-Lapu City, Cebu MCIA ARRIVAL Lower Ground, MCIAt, Arrival Area, Pusok, Lapu-Lapu City, Cebu BASAK MACTAN MEPZ 2, Basak, Mactan, Lapu-lapu City, Cebu LA NUEVA La Nueva, Mactan Center, C.Y. dela Cerna St., Lapu-lapu City, Cebu GAISANO GRAND MALL G/F, Gaisano Grand Mall, Mactan, Cebu MACTAN PACIFIC MALL MANDAUE G/F, Pacific Mall Mandaue, AC Briones St. cor. UN Ave., Mandaue City, Cebu MEZ 2 Lot 11, Calle Moriones cor. Lanzones St., Pueblo Verde, MEZ 2, Basak, Lapu-Lapu City, Cebu CASUNTINGAN MANDAUE M.L Quezon Ave., Casuntingan, Mandaue City, Cebu STO. NIÑO MACTAN DT ML Quezon National Highway, Lapu-lapu, Cebu MANDAUE RECLAMATION Ouano Ave., North Reclamation Area, Mandaue City, Cebu (NRA) PARKMALL Parkmall, Ouano Ave., North Reclamation Area, Mandaue City, Cebu GENERAL MAXILOM DT General Maxilom cor. Jakosalem St., Cebu City, Cebu SUBANGDAKU DT M. Logarta Ave. Corner Ouano St., Subangdaku, Mandaue City, Cebu CEBU MANGO AVE. Mango Ave. cor. Juana Osmeña St., Cebu City CEBU METRO COLON Juan Luna cor. P. Gullas St., Cebu City ROBINSONS GALLERIA Level 3, Robinsons Galleria Cebu, 13th Ave. Cor. -

Definitive Information Statement 2021

COVER SHEET 9 3 2 6 9 - A SEC Registration Number R O B I N S O N S L A N D C O R P O R A T I O N (Company’s Full Name) L E V E L 2 , G A L L E R I A C O R P O R A T E C E N T E R E D S A C O R N E R O R T I G A S A V E N U E , Q U E Z O N C I T Y , M E T R O M A N I L A (Business Address: No. Street City/Town/Province) Atty. Elaine G. Miranda-Araneta 8397-1888 Corporate Secretary (Contact Person) (Company Telephone Number) 1 2 3 1 2 0 - I S Last Wednesday of May Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) Definitive Information Statement Issuer of Securities under SEC-BED Order No.125,Series of 1989; SEC-BED Order No.435, Series of 1989; SEC-BED Order No.523,Series of 1993; SEC-BED Order No.524 Series of 1993;SEC-BED Order No. 572, Series of 1995; SEC-BED Order No. 057, Series of 1997; SEC-CFD Order No. 128, Series of 2006; SEC-MSRD Order No 71, Series of 2015 (Secondary License Type, If Applicable) Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. -

2019 Annual Report Contents

2019 ANNUAL REPORT CONTENTS COMPANY PROFILE Financial Highlights . 3 Project Location (Map) . 4 Directory . 5 MESSAGE TO STAKEHOLDERS . 6 A TRIBUTE TO JOHN L. GOKONGWEI, JR. 10 OUR BUSINESS UNITS Commercial Centers . 13 Residential . 15 Office Buildings . 18 Hotels & Resorts . 20 Industrial & Integrated Developments . 22 Chengdu Ban Bian Jie . 23 CORPORATE SOCIAL RESPONSIBILITY RLove Program . 25 Robinsons Mall Gift of Change . 28 Environment & Sustainability . 30 CORPORATE GOVERNANCE Our Commitment to Good Governance . 33 The Board of Directors - Responsibilities and Composition . 37 Enterprise Risk Management, Accountability, and Audit . 42 Other Matters . 45 BOARD OF DIRECTORS . 47 AUDITED FINANCIAL STATEMENTS . 49 Financial Highlights For the Years ended December 31 2019 2018 2017 2016 2015 2014 2013 (in million pesos) Gross Revenues 30,583.84 29,558.48 22,516.82 22,809.05 20,306.91 17,460.22 16,552.44 Net Income 8,692.61 8,223.96 5,884.44 5,755.32 5,952.94 4,773.87 4,318.49 Total Assets 189,651.21 174,158.16 148,126.55 124,432.16 111,711.51 88,421.50 76,808.45 Stockholders' Equity 100,077.67 93,919.72 67,372.62 62,855.31 58,444.74 53,968.36 50,425.83 8.69 8.22 29.56 30.58 5.95 5.88 22.81 5.76 20.31 22.52 2015 2016 2017 2018 2019 2015 2016 2017 2018 2019 Gross Revenues Net Income (in billion pesos) (in billion pesos) 100.08 189.65 93.92 174.16 148.13 67.37 62.86 124.43 58.44 111.71 2015 2016 2017 2018 2019 2015 2016 2017 2018 2019 Total Assets Stockholders' Equity (in billion pesos) (in billion pesos) 3 ROBINSONS LAND CORPORATION