Definitive Information Statement 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

Download File

C O V E R S H E E T for AUDITED FINANCIAL STATEMENTS SEC Registration Number 2 9 3 1 6 C O M P A N Y N A M E R O B I N S ON S BANK CORPORATI ON AND SUBSI D I ARY PRINCIPAL OFFICE ( No. / Street / Barangay / City / Town / Province ) 1 7 t h Fl o o r , G a l l e r i a Co r p o r a t e Ce n t e r , EDSA c o r n e r O r t i g a s A v e n u e , Qu e z o n Ci t y Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A C O M P A N Y I N F O R M A T I O N Company’s Email Address Company’s Telephone Number Mobile Number www.robinsonsbank.com.ph 702-9500 N/A No. of Stockholders Annual Meeting (Month / Day) Fiscal Year (Month / Day) 15 Last week of April December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Ms. Irma D. Velasco [email protected] 702-9515 09988403139 CONTACT PERSON’s ADDRESS 17th Floor, Galleria Corporate Center, EDSA corner Ortigas Avenue, Quezon City NOTE 1 : In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Participating Robinsons Supermarket Branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST

Participating Robinsons Supermarket branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST. NOAH'S ARC BLDG. BF HOMES PARANAQUE CITY ROBINSONS EASYMART ALIMA BAY ALIMA BAY RESIDENCES AND COMMERCIAL COMPLEX IN GEN. EVANGELISTA ST. BRGY. ALIMA BACOOR CAVITE ROBINSONS EASYMART ANTIPOLO ROBINSONS EASYMART ANTIPOLO RODRIGUEZ ROAD BARANGAY SITIO PARUGAN SAN JOSE ANTIPOLO CITY ROBINSONS EASYMART ARNAIZ ARNAIZ AVENUE, LIBERTAD PASAY CITY PASAY 1300 ROBINSONS EASYMART E RODRIGUEZ SR 340 E. RODRIGUEZ SR. AVE COR. CORDILLERA ST. BRGY. DON MANUEL, QC ROBINSONS EASYMART FILINVEST BATASAN FILINVEST II GATE B SAN MATEO ROAD-BATASAN HILLS QUEZON HILLS CITY ROBINSONS EASYMART GREENGATE IMUS PHASE 3 GREEN GATE SUBDV. MALAGASANG 2A IMUS CAVITE ROBINSONS EASYMART KAMUNING #89 K1ST BARANGAY KAMUNING QUEZON CITY ROBINSONS EASYMART LAGRO SUNBEST BLDG. ASCENSION AVENUE BRGY. GREATER LAGRO, QUEZON CITY ROBINSONS EASYMART LOYOLA HEIGHTS #88 ROSA ALVERO ST. LOYOLA HEIGHTS QUEZON CITY ROBINSONS EASYMART MARILAO GROUND FLOOR OF CINDY SQUARE IN MC ARTHUR HIGHWAY, ABANGAN,NORTE,MARILAO BULACAN ROBINSONS EASYMART MARIPOSA ARCADE G/F MARIPOSA ARCADE A. MABINI ST. KAPASIGAN PASIG CITY ROBINSONS EASYMART MOONWALK LP G/F SAVER'S BUILDUING ALABANG ZAPOTE ROAD TALON 1 MOONWALK LAS PINAS CITY ROBINSONS EASYMART PILILIA RIZAL J.P. RIZAL STREET, BRGY. IMATONG, PILILLA, RIZAL ROBINSONS EASYMART POBLACION 888 SAN IGNACIO ST., BRGY. POBLACION I, SAN JOSE DEL MONTE BULACAN 3023 PHILIPPINES ROBINSONS EASYMART PROJECT 6 #54 EMERALD COURT BLDG. ROAD 8, PROJECT 6, QUEZON CITY ROBINSONS EASYMART SAN AGUSTIN-TANZA SAN AGUSTIN COR SAN FRANCISCO ST POBLACION 2 TANZA CAVITE 4108 PHILIPPINES ROBINSONS EASYMART SAN MATEO KAMBAL ROAD BRGY.GITNANG BAYAN 1 SAN MATEO, RIZAL ROBINSONS EASYMART SAVERS ROOSEVELT 192 SAVERS APPLIANCE DEPOT ROOSEVELT AVE. -

FOI Manuals/Receiving Officers Database

National Government Agencies (NGAs) Name of FOI Receiving Officer and Acronym Agency Office/Unit/Department Address Telephone nos. Email Address FOI Manuals Link Designation G/F DA Bldg. Agriculture and Fisheries 9204080 [email protected] Central Office Information Division (AFID), Elliptical Cheryl C. Suarez (632) 9288756 to 65 loc. 2158 [email protected] Road, Diliman, Quezon City [email protected] CAR BPI Complex, Guisad, Baguio City Robert L. Domoguen (074) 422-5795 [email protected] [email protected] (072) 242-1045 888-0341 [email protected] Regional Field Unit I San Fernando City, La Union Gloria C. Parong (632) 9288756 to 65 loc. 4111 [email protected] (078) 304-0562 [email protected] Regional Field Unit II Tuguegarao City, Cagayan Hector U. Tabbun (632) 9288756 to 65 loc. 4209 [email protected] [email protected] Berzon Bldg., San Fernando City, (045) 961-1209 961-3472 Regional Field Unit III Felicito B. Espiritu Jr. [email protected] Pampanga (632) 9288756 to 65 loc. 4309 [email protected] BPI Compound, Visayas Ave., Diliman, (632) 928-6485 [email protected] Regional Field Unit IVA Patria T. Bulanhagui Quezon City (632) 9288756 to 65 loc. 4429 [email protected] Agricultural Training Institute (ATI) Bldg., (632) 920-2044 Regional Field Unit MIMAROPA Clariza M. San Felipe [email protected] Diliman, Quezon City (632) 9288756 to 65 loc. 4408 (054) 475-5113 [email protected] Regional Field Unit V San Agustin, Pili, Camarines Sur Emily B. Bordado (632) 9288756 to 65 loc. 4505 [email protected] (033) 337-9092 [email protected] Regional Field Unit VI Port San Pedro, Iloilo City Juvy S. -

Memorandum of Agreement

LIST OF POWER MAC CENTER PARTICIPATING REDEMPTION OUTLETS BRANCH (METRO MANILA) ADDRESS 1 Ayala Malls Cloverleaf 2/L Ayala Malls Cloverleaf, A. Bonifacio Ave., Brgy. Balingasa, Quezon City 2 Circuit Lane G/L Ayala Malls Circuit Lane, Hippodromo, Makati City 3 Festival Supermall UGF Expansion Area, Festival Supermall, Filinvest City, Alabang, Muntinlupa City 4 Glorietta 5 3/L Glorietta 5, Ayala Center, Makati City 5 Greenbelt 3 2/L Greenbelt 3, Ayala Center, Makati City 6 Power Plant Mall 2/L Power Plant Mall, Rockwell Center, Poblacion, Makati City 7 SM Aura Premier 3/L SM Aura Premier, 26th St. Corner McKinley Parkway, Bonifacio Global City, Taguig City 8 SM City Bacoor 4/L Cyberzone, SM City Bacoor Gen. Aguinaldo Cor. Tirona Bacoor, Cavite 9 SM City BF Parañaque 3/L Cyberzone, SM City BF Paranaque, Dr. A. SantoS Ave., Brgy. BF HomeS, Paranaque City 10 SM City Dasmariñas 2/L Cyberzone, SM City DaSmarinaS Brgy. Sampaloc 1, DaSmarinaS City, Cavite 11 SM City Fairview 3/L Cyberzone, SM Fairview, Brgy. Greater Lagro, Quezon City 12 SM City Marikina G/L SM City Marikina, Marcos Highway, Marikina City 13 SM Mall of Asia 2/L SM Mall of Asia, Central Business Park Bay Blvd., Pasay City 14 SM Megamall 4/L Cyberzone, SM Megamall Bldg. B, EDSA, Mandaluyong City 15 SM South Mall 3/L Cyberzone, SM Southmall, Alabang Zapote Road, LaS PinaS City 16 The Annex at SM City North EDSA 4/L Cyberzone, Annex Bldg at SM City North EDSA, Quezon City 17 The Podium 3/L The Podium, 18 ADB Avenue, Ortigas Center, Mandaluyong City 18 TriNoma 3/L Mindanao Wing, TriNoma, Quezon City BRANCH (PROVINCIAL) ADDRESS 1 Abreeza Mall 2/L Abreeza Ayala Mall, J.P. -

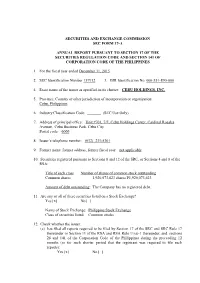

SEC 17-A 2015 Annual Report -CHI Pdf

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2015 2. SEC Identification Number 157912 3. BIR Identification No. 000-551-890-000 4. Exact name of the issuer as specified in its charter: CEBU HOLDINGS, INC. 5. Province, Country or other jurisdiction of incorporation or organization: Cebu, Philippines 6. Industry Classification Code: _______ (SEC Use Only) 7. Address of principal office: Unit #701, 7/F, Cebu Holdings Center, Cardinal Rosales Avenue, Cebu Business Park, Cebu City Postal code: 6000 8. Issuer’s telephone number: (032) 231-5301 9. Former name, former address, former fiscal year: not applicable 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sections 4 and 8 of the RSA: Title of each class Number of shares of common stock outstanding Common shares 1,920,073,623 shares P1,920,073,623 Amount of debt outstanding : The Company has no registered debt. 11. Are any or all of these securities listed on a Stock Exchange? Yes [x] No [ ] Name of Stock Exchange: Philippine Stock Exchange Class of securities listed: Common stocks 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and sections 26 and 141 of the Corporation Code of the Philippines during the preceeding 12 months (or for such shorter period that the registrant was required to file such reports): Yes [x] No [ ] (b) has been subject to such filing requirements for the past 90 days: Yes [x] No [ ] 13. -

Landbank of the Philippines Post-Contract Award Disclosure As of March 15, 2021

Landbank of the Philippines Post-Contract Award Disclosure As of March 15, 2021 APPROVED AMOUNT OF NAME OF WINNING OFFICIAL BUSINESS ADDRESS CONTRACT DATE OF DATE OF IMPLEMENTING OFFICE/UNIT OF PROJECT NAME BUDGET FOR THE CONTRACT BIDDER OF THE WINNING BIDDER PERIOD AWARD ACCEPTANCE THE BANK CONTRACT AWARDED TWO (2) YEARS SUBSCRIPTION TO 816,000.00 816,000.00 CONVERGE INFORMATION Reliance Center Annex 1, 99 E. Rodriguez Jr. 10CD/NTP 05-Jan-21 05-Jan-21 NETWORK OPERATIONS DEPARTMENT (NOD) TWO (2) UNITS CONVERGE IBIZ AND COMMUNICATIONS Ave., Ugong, Pasig City (BROADBAND) INTERNET FOR TECHNOLOGY SOLUTIONS, T - 8667-0888 LANDBANK DIOSDADO MACAPAGAL INC. F - 8667-0895 HALL AND ADJACENT ROOMS E - [email protected] MS. PAMELA C. DEL ROSARIO AIRCONDITIONINIG UNITS 555,600.00 522,410.59 MARCO, INC. 12 Matatag Street, Diliman, Quezon City 30CD/NTP AND 05-Jan-21 05-Jan-21 C/O PROJECT MANAGEMENT & ENGINEERING T - 8929-3767 ADVICE FROM DEPARTMENT (PMED) F - 8920-4598 PMED - HIMAMAYLAN BR. E - [email protected] MR. OLIVERT Y. DUYA ONE (1) YEAR HARDWARE 47,000,000.00 47,000,000.00 IBM PHILIPPINES, INC. 28/F One World Place, 32nd Street, ONE (1) YEAR 05-Jan-21 05-Jan-21 DATA CENTER MANAGEMENT DEPARTMENT MAINTENANCE SERVICES FOR IBM Bonifacio Global City, Taguig City BEGINNING ON (DCMD) MACHINES T - 8995-2426 THE RECEIPT OF CP - 0917-6344723 NTP E - [email protected] MR. RAMIL D. CABODIL VARIOUS VAULTS AND SAFES 627,710.00 341,500.00 MOSLER PHILIPPINES, INC. 8011 Elisco Road, Ibayo, Tipas, Taguiig City 30CD/NTP AND 06-Jan-21 06-Jan-21 C/O PROJECT MANAGEMENT & ENGINEERING T - 8641-4054 ADVICE FROM DEPARTMENT (PMED) E - [email protected] PMED - BALINGASAG BRANCH MR. -

Jcb Unique Dining Experience Merchants

JCB UNIQUE DINING EXPERIENCE MERCHANTS 7107 Culture + Cuisine Restaurant • G/F, Treston Bldg., BGC Alba Restaurante Espaǹol • Bel-Air, Makati City • Tomas Morato Quezon City • Westgate Center,Muntinlupa City • Prism Plaza, TwoEcom Center Building Mall of Asia Complex, Pasay City • Estancia Mall Capitol Commons, Pasig City Alchemy - Bistro • 4893 Durban St. Poblacion Makati Bari Uma Ramen • Ground Floor Serendra, Bonifacio High Street, BGC • Ayala Center Cebu Burgoo • The Block, North Edsa • SM City Marikina • The District Imus • Solenad 3, Nuvali • Robinsons Galleria • SM Mall of Asia • Gateway Mall • SM Southmall • Fairview Terraces • Vista Mall, Taguig Butamaru • West Gate Center, Alabang, Muntinlupa City • Technopoint Bldg, Pasig Chairman Wang's • Molito Lifestyle Bldg, Alabang Chotto Matte • Net Park, 5th Avenue, Bonifacio Global City, Taguig City Gumbo • SM Mall of Asia • Mega Atrium, Megamall • Robinsons Magnolia Hatsu Hana Tei • Herald Suites, Don Chino Roces Avenue, Makati City Ikomai & Tochi • ACI Group Building Makati City Izakaya Sensu • Net Park Building Bonifacio, Global City Kichitora • Bonifacio Highstreet Central, Bonifacio Global City • SM Megamall La Cabrera • Ayala Business Center, 6750 Ayala Avenue Mireio • 1 Raffles Drive Makati Avenue, Makati City Motto Motto • Ground Floor, Serendra, Bonifacio Global City, Taguig City Txanton • Alegria Alta Building,Makati City Wooden Horse Steakhouse • Molito Complex Alabang Yanagi • Midas Hotel Roxas Blvd, Pasay Yoshinoya • Glorietta Mall • SMCity Cebu North • Robinsons, Cybergate -

AFE-ADB News No 43.Indd

No. 43 | September 2013 The Newsletter of the Association of Former Employees of the Asian Development Bank Delhi Annual General Meeting People, Places and Passages Chapter News IN THIS ISSUE Our Cover No. 43 | September 2013 SEPTEMBER 2013 The Newsletter of the Association of Former Employees of the Asian Development Bank 3 AFE–ADB Updates 3 From the AFE President Delhi Annual General Meeting 3 Chapter Coordinators 4 What’s New at HQ?: Professor Yasutomo on ADB’s Beginnings People, Places and Passages Chapter News 6 Delhi 2013 6 Chapter Coordinators’ Meeting 9 AFE–ADB 27th Annual General Meeting 12 Cocktails 15 Participants Top right: ADB President Takehiko Nakao, 16 Around Delhi former ADB President (and new AFE member) Haruhiko Kuroda, and AFE Chair 19 Chapter News Bong-Suh Lee at the AFE Cocktail Left: “See Through” by Bill Staub 19 Indonesia Below: At the New Zealand Chapter gathering 20 New Zealand: Art Deco, Wine, and More 21 Washington DC 22 People, Places, and Passages AFE–ADB News 22 Connections: Bill Staub’s Art 25 Standing on Their Own (Jaipur) Feet Publisher: Hans-Juergen Springer 27 News Briefs 28 A Letter from the Governor Publications Committee: Jill Gale de Villa (head), 30 North to Anvaya Cove Gam de Armas, Wickie Mercado, Stephen 31 Fifty Years and Still Counting Banta, David Parker, Hans-Juergen Springer 32 Travel and Writing 33 A Walk in the Wilds Graphic Assistance: Jo Jacinto-Aquino 35 Friendship, Food, and Fun at CalloSpa Photographs: ADB Photobank, ADB Security Unit, 36 Humanitarian Ethel Raquel Cabiles, Adrian Davis, Daisy de Chavez, 37 AFE Finland Gathering Graham James Dwyer, Estrellita Gamboa, Ian 37 AFE–ADB Committees Gill, Midi Diel Kawashima, V.R. -

Where Is My New Servicing Branch Located and How Can I Contact The

Where is my HSBC Ortigas Branch currently located at GF/29F Discovery Suites, ADB Avenue, new servicing Ortigas Center, San Antonio, Pasig City will be relocated to the Lower Ground Level, branch located Shangri-La Plaza East Wing, EDSA corner Shaw Boulevard, Mandaluyong City on and how can I January 4, 2021. You may call HSBC Ortigas Branch phone numbers (+632) 8581- contact the 7903 or (+632) 8581-7435 for any questions. branch? HSBC Quezon City Branch will be permanently closed on December 29, 2020 and client accounts will be transferred to the new location of HSBC Ortigas Branch. You may call HSBC Quezon City Branch phone numbers (+632) 8581-7928 or (+632) 8581-7822 until December 29. 2020. Starting January 4, 2021, you may call HSBC Ortigas Branch through phone numbers mentioned above. HSBC Binondo Branch will be permanently closed on February 16, 2021 and accounts will be transferred to HSBC Makati Branch located at GF, Tower 1, The Enterprise Center, Ayala Avenue corner Paseo de Roxas, Makati City. You may call HSBC Binondo Branch phone numbers (+632) 8581-7249 or (+632) 8581-8198 until February 16, 2021. Starting February 17, 2021, you may call HSBC Makati Branch through phone numbers (+632) 8581-7787 or (+632) 8581-8097. How does this Your account will be automatically transferred into the branches specified above. affect us There will be no impact on how you transact your account which you can do in any of (customers)? our 5 HSBC branches: Makati, BGC, Ortigas, Cebu, and Davao. Do I need to do However, if you have a Safe Deposit Box in Ortigas Branch, Quezon City Branch or anything? Binondo Branch, please refer to the instructions on retrieval of your Safe Deposit Box (SDB) contents. -

MAXICARE PRIMA Outpatient Unbundled Product That Has No Age

MAXICARE PRIMA Outpatient unbundled product that has no age eligibility and application form requirement. The product offers unlimited outpatient consultation and laboratory procedures with additional emergency coverage of up to P20,000. Access will be through Maxicare’s Primary Care Center and MyHealth Clinics nationwide. Prima Gold VARIANTS Php 12, 999 SRP *Prices may be changed at any time without further notice Maximum Benefit Limit N/A Age Qualification 60 years old and above Benefit Description - Unlimited outpatient consultations with Maxicare Primary Care Center Physicians. - Pre- existing conditions are covered. - Coverage for outpatient laboratory and diagnostic procedure requested by Maxicare Primary Care Center physicians e.g. Laboratories (CBC, Urinalysis, Lipid Studies, Glucose, etc.) X-ray tests (Chest, Scoliotic, etc) or see last pages for the complete List of Laboratory & Diagnostic Procedures Additional Benefits -Up to P20,000 annual emergency room coverage for PRIMA GOLD, can be availed at any Maxicare affiliated hospital nationwide. -Avail of the following services for free once within one year in METRODENTAL CLINICS nationwide: o Mild Oral Prophylaxis (Cleaning) o Panoramic X-Ray (Full Mouth) o Dental Consult o Emergency relief of dental pain through medication o Cosmetic/Oral Rehab treatment planning o Dental nutrition and counselling o Dental Health Education o Preparation of dental certificates o Safekeeping of dental records as required by law and/or client 1 Enrollment Eligibility Maximum of One (1) card per member per year. Activation You can use the voucher or electronic card for consultation and laboratory within 24 hours from the registration period. For the emergency coverage of Prima Gold, activation is after 7 days from the date of registration. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1.