2020 Annual Report (Pdf)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Memorandum of Agreement

LIST OF POWER MAC CENTER PARTICIPATING REDEMPTION OUTLETS BRANCH (METRO MANILA) ADDRESS 1 Ayala Malls Cloverleaf 2/L Ayala Malls Cloverleaf, A. Bonifacio Ave., Brgy. Balingasa, Quezon City 2 Circuit Lane G/L Ayala Malls Circuit Lane, Hippodromo, Makati City 3 Festival Supermall UGF Expansion Area, Festival Supermall, Filinvest City, Alabang, Muntinlupa City 4 Glorietta 5 3/L Glorietta 5, Ayala Center, Makati City 5 Greenbelt 3 2/L Greenbelt 3, Ayala Center, Makati City 6 Power Plant Mall 2/L Power Plant Mall, Rockwell Center, Poblacion, Makati City 7 SM Aura Premier 3/L SM Aura Premier, 26th St. Corner McKinley Parkway, Bonifacio Global City, Taguig City 8 SM City Bacoor 4/L Cyberzone, SM City Bacoor Gen. Aguinaldo Cor. Tirona Bacoor, Cavite 9 SM City BF Parañaque 3/L Cyberzone, SM City BF Paranaque, Dr. A. SantoS Ave., Brgy. BF HomeS, Paranaque City 10 SM City Dasmariñas 2/L Cyberzone, SM City DaSmarinaS Brgy. Sampaloc 1, DaSmarinaS City, Cavite 11 SM City Fairview 3/L Cyberzone, SM Fairview, Brgy. Greater Lagro, Quezon City 12 SM City Marikina G/L SM City Marikina, Marcos Highway, Marikina City 13 SM Mall of Asia 2/L SM Mall of Asia, Central Business Park Bay Blvd., Pasay City 14 SM Megamall 4/L Cyberzone, SM Megamall Bldg. B, EDSA, Mandaluyong City 15 SM South Mall 3/L Cyberzone, SM Southmall, Alabang Zapote Road, LaS PinaS City 16 The Annex at SM City North EDSA 4/L Cyberzone, Annex Bldg at SM City North EDSA, Quezon City 17 The Podium 3/L The Podium, 18 ADB Avenue, Ortigas Center, Mandaluyong City 18 TriNoma 3/L Mindanao Wing, TriNoma, Quezon City BRANCH (PROVINCIAL) ADDRESS 1 Abreeza Mall 2/L Abreeza Ayala Mall, J.P. -

SEC 17-A 2015 Annual Report -CHI Pdf

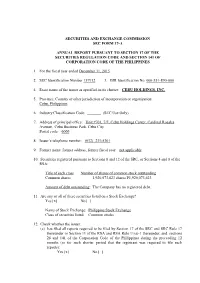

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2015 2. SEC Identification Number 157912 3. BIR Identification No. 000-551-890-000 4. Exact name of the issuer as specified in its charter: CEBU HOLDINGS, INC. 5. Province, Country or other jurisdiction of incorporation or organization: Cebu, Philippines 6. Industry Classification Code: _______ (SEC Use Only) 7. Address of principal office: Unit #701, 7/F, Cebu Holdings Center, Cardinal Rosales Avenue, Cebu Business Park, Cebu City Postal code: 6000 8. Issuer’s telephone number: (032) 231-5301 9. Former name, former address, former fiscal year: not applicable 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sections 4 and 8 of the RSA: Title of each class Number of shares of common stock outstanding Common shares 1,920,073,623 shares P1,920,073,623 Amount of debt outstanding : The Company has no registered debt. 11. Are any or all of these securities listed on a Stock Exchange? Yes [x] No [ ] Name of Stock Exchange: Philippine Stock Exchange Class of securities listed: Common stocks 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and sections 26 and 141 of the Corporation Code of the Philippines during the preceeding 12 months (or for such shorter period that the registrant was required to file such reports): Yes [x] No [ ] (b) has been subject to such filing requirements for the past 90 days: Yes [x] No [ ] 13. -

Standards Monitoring and Enforcement Division List Of

DEPARTMENT OF TOURISM OFFICE OF TOURISM STANDARDS AND REGULATION - STANDARDS MONITORING AND ENFORCEMENT DIVISION LIST OF OPERATIONAL HOTELS AS OF MARCH 26, 2020, 09:00 AM NATIONAL CAPITAL REGION COUNT NAME OF ESTABLISHMENT ADDRESS 1 Ascott Bonifacio Global City 5th ave. Corner 28th Street, BGC, Taguig 2 Ascott Makati Glorietta Ayala Center, San Lorenzo Village, Makati City 3 Cirque Serviced Residences Bagumbayan, Quezon City 4 Citadines Bay City Manila Diosdado Macapagal Blvd. cor. Coral Way, Pasay City 5 Citadines Millenium Ortigas 11 ORTIGAS AVE. ORTIGAS CENTER, PASIG CITY 6 Citadines Salcedo Makati 148 Valero St. Salcedo Village, Makati city Asean Avenue corner Roxas Boulevard, Entertainment City, 7 City of Dreams Manila Paranaque #61 Scout Tobias cor Scout Rallos sts., Brgy. Laging Handa, Quezon 8 Cocoon Boutique Hotel City 9 Connector Hostel 8459 Kalayaan Ave. cor. Don Pedro St., POblacion, Makati 10 Conrad Manila Seaside Boulevard cor. Coral Way MOA complex, Pasay City 11 Cross Roads Hostel Manila 76 Mariveles Hills, Mandaluyong City Corner Asian Development Bank, Ortigas Avenue, Ortigas Center, 12 Crowne Plaza Manila Galleria Quezon City 13 Discovery Primea 6749 Ayala Avenue, Makati City 14 Domestic Guest House Salem Complex Domestic Road, Pasay City 15 Dusit Thani Manila 1223 Epifanio de los Santos Ave, Makati City 16 Eastwood Richmonde Hotel 17 Orchard Road, Eastwood City, Quezon City 17 EDSA Shangri-La 1 Garden Way, Ortigas Center, Mandaluyong City 18 Go Hotels Mandaluyong Robinsons Cybergate Plaza, Pioneer St., Mandaluyong 19 Go Hotels Ortigas Robinsons Cyberspace Alpha, Garnet Road., San Antonio, Pasig City 20 Gran Prix Manila Hotel 1325 A Mabini St., Ermita, Manila 21 Herald Suites 2168 Chino Roces Ave. -

Urgent! Brand Philippines

INSIDER 7107THE PHILIPPINE GUIDE FOR HOTEL, PROPERTY, AND TOURISM DEVELOPMENTS ISSUE 2 2011 Watch list on tourism and property markets Urgent! Brand Philippines Low cost Tune Hotels and Go Hotels are pioneering s the world markets buckle due to looming threat of another recession, the ‘no frills’ concept and expanding Athe country’s flag carrier Philippine Airlines (PAL) is paralyzed by extensively in mainstream and emerging a wildcat strike that grounded both domestic and international flights, cities. Both companies are related to low cost carriers AirAsia and Cebu Pacific, affecting thousands of its passengers. Though operations are going back respectively. LCC passengers will have to normal, PAL’s brand as the national carrier is seriously damaged. a similar experience on these low cost hotels with cheap rates on early bookings and ‘pay as you need’ amenities. The Philippines market emerges as Asia’s largest low-cost carrier battleground, with further growth in 2011 and beyond. Philippine carriers Century Properties hires style icon transported 16.6 million domestic passengers in 2010 and double-digit Paris Hilton to design for Azure traffic growth is expected with the entrance of leading Asian low-cost Beachclub, then signs a partnership with Donald Trump to build Trump Tower airlines AirAsia and Tiger. Domestic market is predominantly strong with a Manila. The skyscraper will comprise over ‘go-go’ attitude among the locals while foreign arrivals have also increased 220 residential units located at the flagship to 12%, compared to same period of Jan-August last year. This has boost mixed-use development of Century City in Makati (formerly International School). -

CEBU | OFFICE 1Q 2018 9 March 2018

Colliers Bi-Annual CEBU | OFFICE 1Q 2018 9 March 2018 Offshore Forecast at a glance Demand Total office transactions reached nearly gambling rises 107,000 sq m (1.2 million sq ft) in 2017. Offshore gambling is an emerging office Joey Roi Bondoc Research Manager segment and we see greater absorption from this sector over the next two to three years. The continued demand from Offshore gambling is emerging as a critical segment BPO and KPO firms should support at of the Cebu office market as it accounted for almost least a 10% annual growth in 25% of recorded transactions in 2017. Business transactions until 2020. Process Outsourcing(BPO)-Voice companies continue to dominate covering more than a half of Supply transactions while the Knowledge Process We see Cebu's office stock breaching Outsourcing (KPO) firms that provide higher value the 1 million sq m (10.8 million sq ft) services also sustained demand, taking 20% of the mark this year. Between 2018 and 2020, total office leases. Colliers sees the current we expect the completion of close to administration's infrastructure implementation and 400,000 sq m (4.3 million sq ft) of new office space. A combined 60% of the decentralization thrust benefiting Cebu as it is the new supply will be in Cebu Business largest business destination outside Metro Manila. Park (CBP) and Cebu IT Park (CITP). This should entice more offshore gambling, BPO, KPO and traditional firms to set up shop or expand Vacancy rate operations. We encourage both landlords and Overall vacancy in Cebu stood at 9.7% tenants to as of end-2017.This is lower than the 12% recorded at end-2016. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

Professional Regulation Commission Cebu Medical Technologist January 21 - 22, 2021

PROFESSIONAL REGULATION COMMISSION CEBU MEDICAL TECHNOLOGIST JANUARY 21 - 22, 2021 School : BENEDICTO COLLEGE - CEBU CITY CAMPUS Address : DON BERNARDO BENEDICTO ST. RECLAMATION CEBU CITY, CEBU (BESIDE ROBINSONS GALLERIA CEBU) Building : Floor : 4TH Room/Grp No. : 401 Seat Last Name First Name Middle Name School Attended No. 1 ABA ALVIN SY SOUTHWESTERN UNIVERSITY 2 ACEDO JESSA MARIA CALAMBA HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 3 ACIDO FRANCIS XAVIER TAMAYO VELEZ COLLEGE 4 ADIONG CHRISTINE ORAIZ SOUTHWESTERN UNIVERSITY 5 AGERO MARIAN OLGA COLUMNAS SOUTHWESTERN UNIVERSITY 6 ALBUERA SHEENA ROSS AWIT VELEZ COLLEGE 7 ALIVIO FE ANIANNE JAGUROS VELEZ COLLEGE 8 ALVEZ RULE PERNITO SOUTHWESTERN UNIVERSITY 9 AMORGANDA LLOYD CABIARA VELEZ COLLEGE REMINDER: USE SAME NAME IN ALL EXAMINATION FORMS. IF THERE IS AN ERROR IN SPELLING AND OTHER DATA KINDLY REQUEST YOUR ROOM WATCHERS TO CORRECT IT ON THE FIRST DAY OF EXAMINATION. REPORT TO YOUR ROOM ON OR BEFORE 6:30 A.M. LATE EXAMINEES WILL NOT BE ADMITTED. PROFESSIONAL REGULATION COMMISSION CEBU MEDICAL TECHNOLOGIST JANUARY 21 - 22, 2021 School : BENEDICTO COLLEGE - CEBU CITY CAMPUS Address : DON BERNARDO BENEDICTO ST. RECLAMATION CEBU CITY, CEBU (BESIDE ROBINSONS GALLERIA CEBU) Building : Floor : 4TH Room/Grp No. : 402 Seat Last Name First Name Middle Name School Attended No. 1 ANDIT FEGEE ANN GOLOAN SOUTHWESTERN UNIVERSITY 2 ANDO QUENCY GIGANTO SOUTHWESTERN UNIVERSITY 3 ANDOY JOMELLE ANGELLA POYAOAN HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 4 ANGANA CATHARD GRACE ESCRIBANO VELEZ COLLEGE 5 ANNUAL RADZMALYN AJIJUL MINDANAO MEDICAL FOUNDATION COLLEGE 6 APOSTOL PATRICIA RALDINE SERAFIN OUR LADY OF FATIMA UNIVERSITY-VALENZUELA 7 ARANAS TRIXIA CASTINO HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 8 ARASAN CYRIL ABEJARON HOLY NAME UNIVERSITY (for.DIVINE WORD- TAGBILARAN) 9 ARELLANO MARK OMBOY SOUTHWESTERN UNIVERSITY REMINDER: USE SAME NAME IN ALL EXAMINATION FORMS. -

Where to Buy Yazz

WHERE TO BUY YAZZ YAZZ STORE PARTNERS Bahayang Pag-Asa Market Ground Floor Bahayang Pag-asa Market, Imus, Cavite Autohide Autoload Panganiban Drive, Naga CIty Emall – Cloudfone Kiosk GF Emall Elias Angeles St. Penafrancia Ave. Naga City Kooky N Luscious G/F MCC Building Ayala Ave Makati CIty Pacific Mall Lucena Viewerss Mobile 2f (M.L Tagarao St.), Lucena City Viewers Mobile Gadgets Quezon Ave. Lucena City CD-R KING BRANCHES BRANCH NAME ADDRESS Alabang Town Center-under 3/f alabang town center brgy. ayala alabang renovation until May 31 muntinlupa city Upper Ground Floor Alimall, Araneta Center Alimall Cubao, Brgy. Socorro, Quezon City Anonas LRT City Center, Aurora Blvd., Brgy. Anonas LRT Bagumbuhay, Quezon City 3rd Floor Stall 312 , Ayala Center Cebu, Bus. Park, Ayala Cebu Cebu City (Capital), Cebu, 6000, Central Visayas Unit S10-12 Bluewave Strip Mall, marikina, Bluewave Strip Mall Sumulong Highway, Marikina City 2nd Floor Cash & Carry Mall, South Super Cash and Carry Highway cor. Filmore St. Palanan Makati City. 3rd Floor Centrio Mall CM Recto Avenue, Cagayan De Oro City (Capital), Misamis Centrio Mall CDO Oriental, 9000, Northern Mindanao Dela Rosa Carpark 1, Delarosa Street, Legaspi Dela Rosa Carpark 1 – Makati Village, Makati City 2/F EDSA Central Pavillion, Edsa cor Shaw Blvd. Edsa Central Brgy. Highway Hills,Mandaluyong City 3rd Floor Elizabeth Mall Corner N. Bacalso Leon Kilat Street, Cebu City (Capital), Cebu, 6000, E-mall Cebu Central Visayas Unit L2-212 Nagaland Elizabeth-Mall, Elias Angeles Street San Francisco, Naga City, E-Mall Nagaland Camarines Sur, 4400, Bicol Region SF 16 &17, 2nd Floor Centris Station, Quezon E-ton Centris-under renovation Ave.,Pinyahan Quezon City 2/F Ever Gotesco Commonwealth, Ever Commonwealth Commonwealth Ave., Batasan Hills, Quezon City Fairview Terraces Level 3 Fairview Terraces Quirino Highway Pasong Putik Novaliches Quezon City Ground Floor New Farmers Plaza, Araneta Farmers Center Cubao, Brgy. -

As of 21 December 2020 FACILITIES SUITABLE for STRINGENT QUARANTINE (TI=I989 Fasilili98 Af9-A189 8Wil951 Fqr MJ!.NQA:Rory

• FAC!! 'TIES AS OF Bece,""er J.;ink: https"/IglJarantjne dob 9Q'a'.j3R}facililies-i. ispected-as-of deeefTlger 21 aQ2fJe. As of 21 December 2020 FACILITIES SUITABLE FOR STRINGENT QUARANTINE (TI=I989 fasilili98 aF9-a189 8wil951 fQr MJ!.NQA:rORY 1. Manila Hotel 33. Conrad Hotel 2. Manila Prince Hotel 34. Networld Hotel 3. Go Hotel Ermita 35. Hotel Jen 4. Manila Grand Opera Hotel 36. The Courtyard Hotel Pasay 5. Red Planet Mabini 37. Seda BGC 6. Rizal Park Hotel 38. Go Hotels Timog 7. Go Hotel, Otis 39. Go Hotels North, Edsa 8. Eurotel, Pedro Gil 40. Park Inn by Radisson North 9. Amelie Hotel Manila Edsa 10. Hotel Kimberly Manila 41. Sequioa Hotel Manila Bay 11. Ramada Manila Central 42. Sequioa Hotel QC 12. Best Western Hotel La 43. Hotel Rembrandt QC Corona 44. Summit Hotel, QC 13. Aloha Hotel 45. Hive Hotel, QC 14. The Bayleaf, Intramuros 46. Cocoon Hotel QC 15. Bayview Park Hotel Manila 47. Privata Hotel, QC 16. 1898 Hotel Colonia - Makati 48. Novotel Cubao 17. The Sphere Residences- 49. Wow Hotel Aurora Cubao Makati 50. F1 Hotel BGC 18. The Charter House -Makati 51. Somerset Olympia Makati 19. Royal Bellagio Hotel - 52. Cabin by Eco Hotels Makati 53. Container by Eco Hotels 20. Nest Nano Suites - Makati 54. Diamond Hotel Manila 21. Ritz Astor Hotel - Makati 55. Oyo Nano Suites Fort 55 22. Crown Regency Hotel 56. Asiatel Makati 57. Elan Hotel Annapolis 23. Privata Hotel, Makati 58. E-Hotel Makati 24. Hotel Celeste, Makati 59. Pearl Blossom, Manila 25. -

Power Mac Center Protect Plus Claim Form

Power Mac Center Protect Plus Program Claim Form Policy and Claimant Details Name of Insured Address (Unit No., Street, Brgy/Town, City and Postcode) Name of Claimant Address (Unit No., Street, Brgy/Town, City and Postcode) Date of Birth (mm/dd/yy) Occupation Mobile No. ( ) Tel. No.(Home) ( ) Tel. No.(Business) ( ) Email Address Equipment Details Brand and Model Date of Purchase Store of Purchase Serial No. Important Information 1. In order to submit your claim, please complete the relevant sections. • This first page must be completed for all claims. • The privacy consent must be completed for all claims. 2. The supporting documentation required for your claim is detailed in each section. 3. The issuance and acceptance of this form does not constitute an admission of liability by Chubb or a waiver of its rights. 4. A Participation Fee equivalent to 20% of the equipment retail price cost should be settled prior to repair of the equipment. 5. Chubb shall not be liable in respect of Equipment that have undergone unauthorized modification. 6. Fraud Warning: Section 251 of the lnsurance Code, as amended, imposes a fine not exceeding twice the amount claimed and/or imprisonment of two (2) years, or both, at the discretion of the court, to any person who presents or causes to be presented any fraudulent claim for the payment of a loss under a contract of insurance, and who fraudulently prepares, makes or subscribes any writing with intent to present or use the same, or to allow it to be presented in support of any claim. Chubb Power Mac Center Protect Plus Program Care Claim Form. -

The French Touch

HOTELS EN JVD CATALOGUE • 2020 THE FRENCH TOUCH Asia-Pacific/Middle-east JVD HOTELS P1 THE HOSPITALITY EXPERIENCE In JVDs Hotels universe, accessories make each room unique and transform a hotel stay into a delightful experience in itself. Every day, we innovate to provide hotel guests with accessories that combine functionality, safety and ergonomics. JVD’s Hotels accessories have become a delight for hotels and travellers around the world. Visit our website for more information General Disclaimer Reasonable efforts are used to include accurate and up-to date information in this catalogue. They may contain technical inaccuracies or typographical errors. We do reserve the rights to change the information without prior notification or any obligation. In no event will JVD or its As part of our environment friendly approach, JVD would like to invite all subsidiaries be liable to any part for any damages whether direct or indirect, consequential, our partners and customers to ensure we have their e-mail address to send punitive or others for use of its contents. this directly in electronic format. P2 JVD HOTELS INNOVATION IN THE SERVICE OF WELL-BEING The strength of JVD resides in our provision of accessories adorning hotel rooms around the world for more than 30 years. JVD accessories help to personalize hotel rooms, giving them the final touch to ensure guests’ well-being. Accessories are what truly At JVD, there is no room for boredom. make a difference. We are proud to present our catalogue of 2020 collections to you, just brimming with new items: JVD does not believe in simply copying and pasting! Our team have been working tirelessly in Nantes, Singapore, Alicante and Mexico City to offer you and your customers enhanced well-being. -

A Time to Build, a Time to Rehabilitate

INSIDER THE PHILIPPINE GUIDE ISSUE NO.5 | 2018 FOR HOTEL, PROPERTY, AND TOURISM DEVELOPMENT CAt’s A WAtcH LIST EYE A Time To Build, ON TOURISM AND PROPERTY A Time To Rehabilitate MARKET omposed of 7,641 islands (the official count was updated from 7,107*), the Philippines has More, more, more hotels rooms. Over 18,000 Cmuch to offer in terms of natural attractions and destinations. Yet, the country is still lagging hotel rooms (50% in Metro Manila alone) are behind neighboring countries such as Thailand, Malaysia and Indonesia when it comes to tourist expected to open in the Philippines over the next arrivals. The biggest obstacles in attracting foreign tourists to the country are poor infrastructure four years. Currently, more than 70 hotel projects and inadequate access—making it expensive and difficult to travel to and within the country— are in the pipeline in anticipation of the estimated which President Duterte is addressing aggressively through his proposed Build! Build! Build! arrival of 10 million foreign tourists by 2020, as program. well as an increase in domestic tourists. This ambitious agenda will see $160B to $180B go into implementing 75 flagship projects, More international hotel groups are opening including six airports, nine railways, three bus rapid transits, 32 roads and bridges, and four in the Philippines. Grand Hyatt, Mandarin seaports. If successful, Build!Build!Build! will generate more jobs, encourage countryside Oriental, Sheraton, Westin and Hilton are just investments, and make the movement of goods and people more efficient, possibly ushering some of the global brands opening in the next two in a “golden era” of economic development.