Economic Crises: Evidence and Insights from East Asia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

James Duesenberry As a Practitioner of Behavioral Economics

Journal of Behavioral Economics for Policy, Vol. 2, No. 1, 13-18, 2018 James Duesenberry as a practitioner of behavioral economics Ken McCormick1* Abstract In 1949 James Duesenberry published Income, saving and the theory of consumer behavior. His objective was to solve a puzzle presented by the macroeconomic data on consumption. To do so, he created the Relative Income Hypothesis. Duesenberry explicitly challenged the neoclassical assumption of independent consumer preferences and made use of ideas that are now common in behavioral economics: loss aversion, status quo bias, spotlight effects, herd behavior, and interdependent preferences. He also raised policy questions about the effect of redistributive taxes on national saving. To answer the questions he raised, we need empirical research by behavioral economists. Finally, the issue arises as to why the Relative Income Hypothesis has virtually disappeared from economics even though it is superior to the Permanent Income Hypothesis that replaced it. JEL Classification: B31; E21; E71 Keywords Duesenberry — Relative Income Hypothesis — independent preferences — saving 1University of Northern Iowa *Corresponding author: [email protected] “State a moral question to a ploughman and a reasons for supposing that preferences are in fact interdepen- professor. The former will decide it as well and dent” (1949, 3). often better than the latter because he has not Duesenberry’s appeal to psychological and sociological been led astray by artificial rules”. evidence marks him as an early practitioner of behavioral economics. In his view, Homo Economicus leads economists THOMAS JEFFERSON (1787) astray. Economists need to work with a more realistic vi- sion of human behavior, one that will provide more accurate Introduction predictions. -

Economic Analysis by Nobel Laureate Joseph Stiglitz

BEFORE THE UNITED STATES DEPARTMENT OF JUSTICE UNITED STATES OF AMERICA, Plaintiff, v. Civil Action No. 98-1232 (CKK) MICROSOFT CORPORATION, Defendant. STATE OF NEW YORK ex rel. Attorney General Eliot Spitzer, et al., Plaintiffs, v. Civil Action No. 98-1233 (CKK) MICROSOFT CORPORATION, Defendant. DECLARATION OF JOSEPH E. STIGLITZ AND JASON FURMAN TABLE OF CONTENTS I. QUALIFICATIONS ........................................................................................................... 1 II. PURPOSE............................................................................................................................ 2 III. INTRODUCTION............................................................................................................... 2 IV. THE MODERN ECONOMIC THEORY OF COMPETITION AND MONOPOLY .6 A. Acquisition of a monopoly............................................................................................ 7 B. Potential for competition............................................................................................ 10 C. Consequences of monopoly ........................................................................................ 12 D. Monopolies and innovation ........................................................................................ 14 V. FACTS AND LEGAL CONCLUSIONS RELATING TO MICROSOFT.................. 16 A. Monopoly power.......................................................................................................... 16 B. Anticompetitive behavior .......................................................................................... -

The Relevance of Duesenberry's Relative Income Hypothesis In

Keeping up with the Joneses: the Relevance of Duesenberry’s Relative Income Hypothesis in Ethiopia Tazeb Bisset ( [email protected] ) Dire Dawa University Dagmawe Tenaw Dire Dawa University https://orcid.org/0000-0002-9768-0430 Research Article Keywords: Duesenberry’s demonstration and ratchet effects, relative income, APC, ARDL, Ethiopia Posted Date: October 7th, 2020 DOI: https://doi.org/10.21203/rs.3.rs-83692/v1 License: This work is licensed under a Creative Commons Attribution 4.0 International License. Read Full License Keeping up with the Joneses: the Relevance of Duesenberry’s Relative Income Hypothesis in Ethiopia Tazeb Bisset1 and Dagmawe Tenaw2 Department of Economics Dire Dawa University, Dire Dawa, Ethiopia 1Email: [email protected] 2Email: [email protected] Abstract Although it was mysteriously neglected and displaced by the mainstream consumption theories, the Duesenberry’s relative income hypothesis seems quite relevant to the modern societies where individuals are increasingly obsessed with their social status. Accordingly, this study aims to investigate the relevance of Duesenberry’s demonstration and ratchet effects in Ethiopia using a quarterly data from 1999/2000Q1-2018/19Q4. To this end, two specifications of relative income hypothesis are estimated using Autoregressive Distributed Lag (ARDL) regression model. The results confirm a backward-J shaped demonstration effect. This implies that an increase in relative income induces a steeper reduction in Average Propensity to consume (APC) at lower income groups (the demonstration effect is stronger for lower income households). The results also support the ratchet effect, indicating the importance of past consumption habits for current consumption decisions. In resolving the consumption puzzle, the presence of demonstration and ratchet effects reflects a stable APC in the long-run. -

Saving out of Different Types of Income

LESTER D. TAYLOR* Universityof Michigan Saving out of Diferent Types of Income IT HAS ALWAYSBEEN A SOURCEof professionalpride to me to be able to tell my undergraduatestudents in macro theory that economists know a lot about what makes consumers tick. However, in light of the experience of the past several years, I now state this proposition much more circumspectly, and perhaps should restrain myself altogether. For the fact is that in the last three or four years, the consumer has done few things predicted of him. To be sure, there have been some new elements in the picture: interest rates at the highest levels in a century; a "roaring" inflation, at least by contem- porary U.S. standards; and a temporary tax increase. But even so, the con- sumer seems to have injected his own element of eccentricity. Among other things, he was thrifty in 1967 and the first half of 1968 on a scale then un- precedented for the postwar period. And while he regained his taste for spending in the last half of 1968, it was rather short-lived. For in the third quarter of 1969, the personal saving rate again began to rise, and from the third quarter of 1970 through the second quarter of 1971, was in excess of the unheard-of level of 8 percent. * Computationsand researchassistance supported by the National Science Founda- tion. I am gratefulto membersof the Brookingspanel for commentsand criticisms,to Daniel Weiserbsand Angelo Mascarofor researchassistance, and to Joan Hinterbichler and PatriciaRamsey for secretarialassistance. I have also greatlybenefited from access to an unpublishedpaper of H. -

Politics Aside, a Common Bond for Two Economists by N

The New York Times, June 30, 2013 Politics Aside, a Common Bond for Two Economists By N. GREGORY MANKIW ONE of the cool things about hanging around a place like Harvard, where I have been a professor for almost 30 years, is that you get to meet some supertalented people long before the world recognizes their talents. I had a vivid reminder of this just a few days ago, when President Obama appointed Jason Furman as chairman of the Council of Economic Advisers, a position that I held under George W. Bush. Jason was once a student of mine at Harvard. As the president noted in announcing the appointment, I was chairman of Jason’s Ph.D. dissertation committee. He and I have remained friends ever since. In Washington these days, comity between Republicans and Democrats is rare. Yet my relationship with Jason has never been hampered by our differing political affiliations. During the campaign of 2004, I was part of the Bush administration and he was working for two Democratic candidates, first for Wesley K. Clark in the primary season and then for John Kerry during the general election. Yet the fact that our bosses were steeped in a political battle at the highest level did not stop us from enjoying regular dinners together. For me, and I suspect for Jason as well, friendship trumps politics. Our friendship is based in part on the common bond of all economists. The field of economics offers a lens through which to view the world. For those who buy into it and pursue it as a career, it provides a foundation of a personal and political philosophy. -

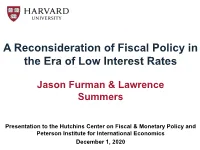

A Reconsideration of Fiscal Policy in the Era of Low Interest Rates

A Reconsideration of Fiscal Policy in the Era of Low Interest Rates Jason Furman & Lawrence Summers Presentation to the Hutchins Center on Fiscal & Monetary Policy and Peterson Institute for International Economics December 1, 2020 Interest rates are low despite debt being high Note: Debt-to-GDP forecast is the CBO 10-year ahead forecast (2030 from June 2019 Alternative Fiscal Scenario for 2020). Real interest rates are based on 10-year Treasury Inflation Protected Securities (TIPS) from January 2000 and February 2020. Source: Congressional Budget Office; U.S. Department of the Treasury; authors' calculations. Interest rates have fallen everywhere, starting before the financial crisis and continuing after it Real Ten-Year Benchmark Rate Percent 12 Canada France Germany Italy 10 United Kingdom Japan United States 8 6 4 2 0 -2 -4 1985 1990 1995 2000 2005 2010 2015 2020 Note: Inflation measured by one-year changes in the core consumer price index (core personal consumption expenditures for United States). Source: Bank of Canada; Statistics Canada; Eurostat; Japanese Statistics Bureau; U.S. Bureau of Economic Analysis; Macrobond; authors’ calculations. Interest rates are expected to stay low Ten-Year Treasury Rate Percent 16 2030:Q4 Market expectations: 14 72% probability FFR < 0.25 12 five years from now 10 Historical 1.4% FFR a decade from 8 now 6 -0.9% real FFR a decade from now 4 CBO 2 2% nominal 10-year rate a Market-implied decade from now 0 1964 1974 1984 1994 2004 2014 2024 Note: Dashed lines are projections. Market-implied rates as of November 27, 2020. -

American Economic Association

American Economic Association /LIH&\FOH,QGLYLGXDO7KULIWDQGWKH:HDOWKRI1DWLRQV $XWKRU V )UDQFR0RGLJOLDQL 6RXUFH7KH$PHULFDQ(FRQRPLF5HYLHZ9RO1R -XQ SS 3XEOLVKHGE\$PHULFDQ(FRQRPLF$VVRFLDWLRQ 6WDEOH85/http://www.jstor.org/stable/1813352 $FFHVVHG Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=aea. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. American Economic Association is collaborating with JSTOR to digitize, preserve and extend access to The American Economic Review. http://www.jstor.org Life Cycle, IndividualThrift, and the Wealth of Nations By FRANCO MODIGLIANI* This paper provides a review of the theory Yet, there was a brief but influential inter- of the determinants of individual and na- val in the course of which, under the impact tional thrift that has come to be known as of the Great Depression, and of the interpre- the Life Cycle Hypothesis (LCH) of saving. -

HAMILTON Achieving Progressive Tax Reform PROJECT in an Increasingly Global Economy Strategy Paper JUNE 2007 Jason Furman, Lawrence H

THE HAMILTON Achieving Progressive Tax Reform PROJECT in an Increasingly Global Economy STRATEGY PAPER JUNE 2007 Jason Furman, Lawrence H. Summers, and Jason Bordoff The Brookings Institution The Hamilton Project seeks to advance America’s promise of opportunity, prosperity, and growth. The Project’s economic strategy reflects a judgment that long-term prosperity is best achieved by making economic growth broad-based, by enhancing individual economic security, and by embracing a role for effective government in making needed public investments. Our strategy—strikingly different from the theories driving economic policy in recent years—calls for fiscal discipline and for increased public investment in key growth- enhancing areas. The Project will put forward innovative policy ideas from leading economic thinkers throughout the United States—ideas based on experience and evidence, not ideology and doctrine—to introduce new, sometimes controversial, policy options into the national debate with the goal of improving our country’s economic policy. The Project is named after Alexander Hamilton, the nation’s first treasury secretary, who laid the foundation for the modern American economy. Consistent with the guiding principles of the Project, Hamilton stood for sound fiscal policy, believed that broad-based opportunity for advancement would drive American economic growth, and recognized that “prudent aids and encouragements on the part of government” are necessary to enhance and guide market forces. THE Advancing Opportunity, HAMILTON Prosperity and Growth PROJECT Printed on recycled paper. THE HAMILTON PROJECT Achieving Progressive Tax Reform in an Increasingly Global Economy Jason Furman Lawrence H. Summers Jason Bordoff The Brookings Institution JUNE 2007 The views expressed in this strategy paper are those of the authors and are not necessarily those of The Hamilton Project Advisory Council or the trustees, officers, or staff members of the Brookings Institution. -

Uncorrected Transcript

1 CEA-2016/02/11 THE BROOKINGS INSTITUTION FALK AUDITORIUM THE COUNCIL OF ECONOMIC ADVISERS: 70 YEARS OF ADVISING THE PRESIDENT Washington, D.C. Thursday, February 11, 2016 PARTICIPANTS: Welcome: DAVID WESSEL Director, The Hutchins Center on Monetary and Fiscal Policy; Senior Fellow, Economic Studies The Brookings Institution JASON FURMAN Chairman The White House Council of Economic Advisers Opening Remarks: ROGER PORTER IBM Professor of Business and Government, Mossavar-Rahmani Center for Business and Government, The John F. Kennedy School of Government at Harvard University Panel 1: The CEA in Moments of Crisis: DAVID WESSEL, Moderator Director, The Hutchins Center on Monetary and Fiscal Policy; Senior Fellow, Economic Studies The Brookings Institution ALAN GREENSPAN President, Greenspan Associates, LLC, Former CEA Chairman (Ford: 1974-77) AUSTAN GOOLSBEE Robert P. Gwinn Professor of Economics, The Booth School of Business at the University of Chicago, Former CEA Chairman (Obama: 2010-11) PARTICIPANTS (CONT’D): GLENN HUBBARD Dean & Russell L. Carson Professor of Finance and Economics, Columbia Business School Former CEA Chairman (GWB: 2001-03) ALAN KRUEGER Bendheim Professor of Economics and Public Affairs, Princeton University, Former CEA Chairman (Obama: 2011-13) ANDERSON COURT REPORTING 706 Duke Street, Suite 100 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 2 CEA-2016/02/11 Panel 2: The CEA and Policymaking: RUTH MARCUS, Moderator Columnist, The Washington Post KATHARINE ABRAHAM Director, Maryland Center for Economics and Policy, Professor, Survey Methodology & Economics, The University of Maryland; Former CEA Member (Obama: 2011-13) MARTIN BAILY Senior Fellow and Bernard L. Schwartz Chair in Economic Policy Development, The Brookings Institution; Former CEA Chairman (Clinton: 1999-2001) MARTIN FELDSTEIN George F. -

Trend Inflation, Indexation, and Inflation Persistence in The

Trend Inflation, Indexation, and Inflation Persistence in the New Keynesian Phillips Curve∗ Timothy Cogley University of California, Davis Argia M. Sbordone Federal Reserve Bank of New York Abstract A number of empirical studies conclude that purely forward-looking versions of the New Keynesian Phillips curve (NKPC ) generate too little inflation per- sistence. Some authors add ad hoc backward-looking terms to address this shortcoming. In this paper, we hypothesize that inflation persistence results mainly from variation in the long-run trend component of inflation, attributable to shifts in monetary policy, and that the apparent need for lagged inflation in the NKPC comes from neglecting the interaction between drift in trend in- flation and non-linearities in a more exact version of the model. We derive a version of the NKPC as a log-linear approximation around a time-varying inflation trend and examine whether such a model explains the dynamics of in- flation around that trend. When drift in trend inflation is taken into account, there is no need for a backward-looking indexation component, and a purely forward-looking version of the model fits the data well. JEL Classification: E31. Keywords:Trendinflation; Inflation persistence; Phillips curve; time-varying VAR. ∗For comments and suggestions, we are grateful to two anonymous referees. We also wish to thank Jean Boivin, Mark Gertler, Peter Ireland, Sharon Kozicki, Jim Nason, Luca Sala, Dan Waggoner, Michael Woodford, Tao Zha and seminar participants at the Banque de France, the November 2005 NBER Monetary Economics meeting, the October 2005 Conference on Quantitative Models at the Federal Reserve Bank of Cleveland, the 2004 Society for Computational Economics Meeting in Amsterdam, the Federal Reserve Banks of New York, Richmond, and Kansas City, Duke University, and the Fall 2004 Macro System Committe Meeting in Baltimore. -

Maurice Obstfeld

February 1, 2019 CURRICULUM VITAE OF MAURICE OBSTFELD PERSONAL DATA Address: Department of Economics University of California, Berkeley 549 Evans Hall #3880 Berkeley, CA 94720-3880 Telephone: 510-643-9646 Fax: 510-642-6615 E-mail: [email protected] Homepage: http://elsa.berkeley.edu/~obstfeld EDUCATION 1975-79: Massachusetts Institute of Technology (Cambridge, MA) Ph.D., September 1979. Dissertation: Capital Mobility and Monetary Policy under Fixed and Flexible Exchange Rates. Adviser: Rudiger Dornbusch. 1973-75: King's College, Cambridge University (Cambridge, U.K.) M.A., June 1975 (Mathematical Tripos, Parts II and III). 1969-73: University of Pennsylvania (Philadelphia, PA) B.A., Summa Cum Laude with Distinction in Mathematics, May 1973. 1 PRINCIPAL EMPLOYMENT EXPERIENCE Class of 1958 Professor of Economics, University of California, Berkeley, from July 1, 1995. Chair, Department of Economics, University of California, Berkeley, July 1, 1998-June 30, 2001. Professor of Economics, University of California, Berkeley, July 1, 1989-June 30, 1995. Visiting Professor of Economics, Harvard University, July 1, 1989—January 31, 1991. Professor of Economics, University of Pennsylvania, July 1, 1986—June 30, 1989. Professor of Economics, Columbia University, July 1, 1985—June 30, 1986. Associate Professor of Economics, Columbia University, July 1, 1981—June 30, 1985. Assistant Professor of Economics, Columbia University, July 1, 1979—June 30, 1981. OTHER EXPERIENCE Senior Nonresident Fellow, Peterson Institute of International Economics, Washington, DC, from February 2019. Economic Counselor and Director of the Research Department, International Monetary Fund, September 2015-December 2018. Member, President’s Council of Economic Advisers, Washington, DC, July 2014 – August 2015. One-Week Training Course, Bank of Korea Academy, August 2011, August 2013. -

The Relative Income Theory of Consumption: a Synthetic Keynes-Duesenberry- Friedman Model

RESEARCH INSTITUTE POLITICAL ECONOMY The Relative Income Theory of Consumption: A Synthetic Keynes-Duesenberry-Friedman Model Thomas I. Palley April 2008 Gordon Hall 418 North Pleasant Street Amherst, MA 01002 Phone: 413.545.6355 Fax: 413.577.0261 [email protected] www.peri.umass.edu WORKINGPAPER SERIES Number 170 The Relative Income Theory of Consumption: A Synthetic Keynes-Duesenberry- Friedman Model Abstract This paper presents a theoretical model of consumption behavior that synthesizes the seminal contributions of Keynes (1936), Friedman (1956) and Duesenberry (1948). The model is labeled a “relative permanent income” theory of consumption. The key feature is that the share of permanent income devoted to consumption is a negative function of household relative permanent income. The model generates patterns of consumption spending consistent with both long-run time series data and modern empirical findings that high-income households have a higher propensity to save. It also explains why consumption inequality is less than income inequality. JEL ref.: E3 Keywords: Consumption, permanent income, relative income, Keynes, Duesenberry, Friedman. December 2007 1 I Introduction After World War II the theory of consumption became a central focus of research in macroeconomics. With consumption spending making up approximately two-thirds of peacetime GDP and with economists fearful that the economy would fall back into a condition of mass unemployment, this focus was natural. Initially, thinking was dominated by Keynes’ theory of the aggregate consumption function that he had developed in his General Theory (1936). According to Keynes’s theory, aggregate consumption was a positive but diminishing function of aggregate income. James Duesenberry’s 1949 book, Income, Saving and the Theory of Consumer Behavior, challenged Keynes’ construction of consumption behavior by introducing psychological factors associated with habit formation and social interdependencies based on relative income concerns.