1 Some Issues in Accounting for Disasters Charles Steindel New

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Story of New Jersey

THE STORY OF NEW JERSEY HAGAMAN THE UNIVERSITY PUBLISHING COMPANY Examination Copy THE STORY OF NEW JERSEY (1948) A NEW HISTORY OF THE MIDDLE ATLANTIC STATES THE STORY OF NEW JERSEY is for use in the intermediate grades. A thorough story of the Middle Atlantic States is presented; the context is enriohed with illustrations and maps. THE STORY OF NEW JERSEY begins with early Indian Life and continues to present day with glimpses of future growth. Every aspect from mineral resources to vac-| tioning areas are discussed. 160 pages. Vooabulary for 4-5 Grades. List priceJ $1.28 Net price* $ .96 (Single Copy) (5 or more, f.o.b. i ^y., point of shipment) i^c' *"*. ' THE UNIVERSITY PUBLISHING COMPANY Linooln, Nebraska ..T" 3 6047 09044948 8 lererse The Story of New Jersey BY ADALINE P. HAGAMAN Illustrated by MARY ROYT and GEORGE BUCTEL The University Publishing Company LINCOLN NEW YORK DALLAS KANSAS CITY RINGWOOD PUBLIC LIBRARY 145 Skylands Road Ringwood, New Jersey 07456 TABLE OF CONTENTS NEW.JERSEY IN THE EARLY DAYS Before White Men Came ... 5 Indian Furniture and Utensils 19 Indian Tribes in New Jersey 7 Indian Food 20 What the Indians Looked Like 11 Indian Money 24 Indian Clothing 13 What an Indian Boy Did... 26 Indian Homes 16 What Indian Girls Could Do 32 THE WHITE MAN COMES TO NEW JERSEY The Voyage of Henry Hudson 35 The English Take New Dutch Trading Posts 37 Amsterdam 44 The Colony of New The English Settle in New Amsterdam 39 Jersey 47 The Swedes Come to New New Jersey Has New Jersey 42 Owners 50 PIONEER DAYS IN NEW JERSEY Making a New Home 52 Clothing of the Pioneers .. -

NEW JERSEY LAW REVISION COMMISSION Tentative Report Addressing the Use of the Term “Inhabitant” in the New Jersey Law Again

NEW JERSEY LAW REVISION COMMISSION Tentative Report Addressing the Use of the Term “Inhabitant” in the New Jersey Law Against Discrimination. June 17, 2021 The New Jersey Law Revision Commission is required to “[c]onduct a continuous examination of the general and permanent statutory law of this State and the judicial decisions construing it” and to propose to the Legislature revisions to the statutes to “remedy defects, reconcile conflicting provisions, clarify confusing language and eliminate redundant provisions.” N.J.S. 1:12A-8. This Report is distributed to advise interested persons of the Commission's tentative recommendations and to notify them of the opportunity to submit comments. Comments should be received by the Commission no later than August 16, 2021. The Commission will consider these comments before making its final recommendations to the Legislature. The Commission often substantially revises tentative recommendations as a result of the comments it receives. If you approve of the Report, please inform the Commission so that your approval can be considered along with other comments. Please send comments concerning this Report or direct any related inquiries, to: Samuel M. Silver, Deputy Director New Jersey Law Revision Commission 153 Halsey Street, 7th Fl., Box 47016 Newark, New Jersey 07102 973-648-4575 (Fax) 973-648-3123 Email: [email protected] Web site: http://www.njlrc.org Project Summary1 The practices of discrimination against members of protected classes are matters of concern to the government of New Jersey. 2 To protect the “inhabitants” of the State from such discrimination, the Legislature enacted the “Law Against Discrimination.”3 The term “inhabitants,” as used in the preamble of the New Jersey Law Against Discrimination (NJLAD), is not defined in the Act.4 Moreover, the use of the term is inconsistent with the language used in other provisions of the statute, namely N.J.S. -

The Government of the United States

NEW LeadershipTM New Jersey The Government of the United States The Executive Branch At a time when all the major European states had hereditary monarchs, the idea of a president with a limited term of office was itself revolutionary. But the Constitution adopted in 1787 vested executive power in a president, and that remains the case today. The Constitution also provides for the election of a vice president, who succeeds to the presidency in case of the death, resignation, or incapacitation of the president. While the Constitution spells out in some detail the duties and powers of the president, it does not delegate any specific executive powers to the vice president, to the presidential cabinet (made up of the heads of the federal departments), or to other federal officials. The office of president of the United States is one of the most powerful in the world. The president, the Constitution says, must "take care that the laws be faithfully executed." To carry out this responsibility, he presides over the executive branch of the federal government — a vast organization numbering in the millions. In addition, the president has important legislative and judicial powers. Within the executive branch itself, the president has broad powers to manage national affairs and the workings of the federal government. The president can issue rules, regulations, and instructions called executive orders, which have the binding force of law upon federal agencies but do not require congressional approval. As commander-in-chief of the armed forces of the United States, the president may also call into federal service the state units of the National Guard. -

New Jersey Society About the Middle of the Eighteenth Century

I 4 f ^'^ '^^ " - -'^.^ . t UNIVERSITY OF ILLINOIS LIBRARY Nt Class Book Volume ^'4 MrlO-20M :,;>#:^; . ^ l|^ ^ ,f._ 4^ 4^ - . ,/., 4 The person charging this material is re- sponsible for its return to the library from which it was withdrawn on or before the Latest Date stamped below. Theft, mutilation, ond underlining of books are reasons for disciplinary action and may result in dismissal from the University. To renew call Telephone Center, 333-8400 UNIVERSI TY or- I Ll l NO IS- MiHABY l l gRAtjA-CHAMPAIGN r «tlURr^ (U IHESElS COLLECTKDN BUiLOiNG USE OfJlY u4 4- L161—O-1096 t- -f- * 4 •^ '•"--4- ^4- -I- 4 - ^ -I f , f- ^ f 4 -f' if i'- -f- ^- Digitized by the Internet Archive in 2013 http://archive.org/details/newjerseysocietyOOmoor NEW JERSEY SOCIETY ABOUT THE MIDDLE OF THE EIGHTEENTH CENTURY BY ELLSWORTH MOORE THESIS FOR THE DEGREE OF BACHELOR OF ARTS IN HISTORY IN THE COLLEGE OF LITERATURE AND ARTS OF THE UNIVERSITY OF ILLINOIS PRESENTED JUNE, 1910 ... Nil UNIVERSITY OF ILLINOIS THIS IS TO CERTIFY THAT THE THESIS PREPARED UNDER MY SUPERVISION BY Mdx.^ M<H^ ENTITLED IS APPROVED BY ME AS FULFILLING THIS PART OF THE REQUIREMENTS FOR THE DEGREE OF- Instructor in Charge APPROVED: HEAD OF DEPARTMENT OF 167828 UlUC \ J. A/ 4y 01 UNIVERSITY of ILLINOW PREFACE In the preparation of this essay it has been the constant aim the to treat only those things which have influenced most directly lives of the people and helped to mold their plastic institutions and ideas. The home, the church, the school, and the econoraio conditions, all receive attention. -

Hearing Unit Cover and Text

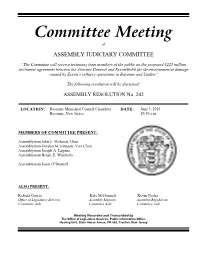

Committee Meeting of ASSEMBLY JUDICIARY COMMITTEE “The Committee will receive testimony from members of the public on the proposed $225 million settlement agreement between the Attorney General and ExxonMobil for the environmental damage caused by Exxon’s refinery operations in Bayonne and Linden” The following resolution will be discussed: ASSEMBLY RESOLUTION No. 242 LOCATION: Bayonne Municipal Council Chambers DATE: June 3, 2015 Bayonne, New Jersey 10:30 a.m. MEMBERS OF COMMITTEE PRESENT: Assemblyman John F. McKeon, Chair Assemblyman Gordon M. Johnson, Vice Chair Assemblyman Joseph A. Lagana Assemblyman Benjie E. Wimberly Assemblyman Jason O’Donnell ALSO PRESENT: Rafaela Garcia Kate McDonnell Kevin Nedza Office of Legislative Services Assembly Majority Assembly Republican Committee Aide Committee Aide Committee Aide Meeting Recorded and Transcribed by The Office of Legislative Services, Public Information Office, Hearing Unit, State House Annex, PO 068, Trenton, New Jersey TABLE OF CONTENTS Page James M. Davis Mayor City of Bayonne 2 Senator Raymond J. Lesniak District 20 4 Jeff Tittel Executive Director New Jersey Chapter Sierra Club 15 Peggy Wong Member Hudson County Waterfront Conservancy of New Jersey, Inc. 25 Ed Potosnak Executive Director New Jersey League of Conservation Voters 29 Marion R. Cooney Private Citizen 32 Michael Ruscigno Founder Bayonne Nature Club 35 Tim Dillingham Executive Director American Littoral Society 39 Matthew Zwerling Private Citizen 42 Nicole Dallara Coordinator Outreach and Communications Clean Ocean Action 44 TABLE OF CONTENTS (continued) Page Andrew Willner Founder New York/New Jersey Baykeeper, and Representing Sustainability Solutions 45 Evelyn Sabol Private Citizen 47 Joseph DiGiorgio Private Citizen 49 APPENDIX: Remedial Priority System score sheets submitted by Jeff Tittel 1x Testimony, and Hudson River Waterfront Walkway Map submitted by Peggy Wong 15x The Historical Heritage of Modern Bayonne by Dr. -

The New Jersey Pension Crisis Flailing in Deep Waters

The New Jersey Pension Crisis Flailing in Deep Waters Scott Andrew Shepard MERCATUS WORKING PAPER All studies in the Mercatus Working Paper series have followed a rigorous process of academic evaluation, including (except where otherwise noted) at least one double-blind peer review. Working Papers present an author’s provisional findings, which, upon further consideration and revision, are likely to be republished in an academic journal. The opinions expressed in Mercatus Working Papers are the authors’ and do not represent official positions of the Mercatus Center or George Mason University. 575-75125_coversheet.indd 1 08/05/18 4:02 PM Scott Andrew Shepard. “The New Jersey Pension Crisis: Flailing in Deep Waters.” Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2018. Abstract New Jersey has a deep pension-funding crisis. It has made excessively generous pension promises without funding them; simultaneously, it has run up some of the highest debts, lowest credit ratings, highest tax rates, lowest citizen satisfaction rates, and highest out-migration rates of any state. Its responses have proven futile or counterproductive. While the pension crisis has arisen largely from a lack of citizen oversight, the state has recently increased government- worker control. While it has failed to fund its pensions, it has recently made a cosmetic dedication of lottery revenues that will only serve to hide—not correct—underfunding. And while the state already shows signs of tax-base flight, it contemplates enormous tax increases. New Jersey’s future likely requires its officials to reduce pension promises for work not yet performed and to trim some already-granted pensions that run in excess of earnings during working years and reasonable New Jersey compensation levels. -

Geography and History of New Jersey

GEOGRAPHY AND HISTORY OF NEW JERSEY BY ALBERT B. MEREDITH AND VIVIAN p. HOOD GINN AND COMPANY BOSTON • NEW YORK CHICAGO - LONDON ATLANTA • DALLAS • COLUMBUS • SAN FRANCISCO FTst COPYRIGHT, 1921, BY GINN AND COMPANY ALL RIGHTS RESERVED &2I.8 SEP 28 i ^^. gCbe gltfttneeum jpregg l.INN AM) (OMI'ANV • I'KO- I'KIhTDKi • UUSTUN • U.S.A. 0)C!.A624539 PREFACE The geography and history of any state are closely inter- woven; New Jersey is no exception. Its coast position between two great cities, the long sandy stretches in the east, and the foothills toward the west and north have all combined to make of the history of this state not only an interesting story which every New Jersey school child should know but also one in which he should take great pride. It is the geographic conditions with which a people have to contend that determine to a great extent what that people shall accomplish. The authors of the present book have en- deavored to show clearly and definitely the character of the land which we call New Jersey : how it has fostered farming, fishing, and manufacturing ; how it has steadily made for progress ; and how it has brought wealth to the inhabitants. New Jersey has been greatly favored and her people have accomplished much. The history of New Jersey began almost with the history of our country, and from the time when the first settlers reached her coast and laid out their small farms and towns there have been no movements in our national history in which the men and women of New Jersey have not done their part. -

New Jersey News Facts a Absecon Allentown Andover Asbury

New Jersey News Facts A Absecon Allentown Andover Asbury Park Atlantic City Atlantic Highlands Avalon Av enel -------------------------------------------------------------------------------- B Barnegat Basking Ridge Bayonne Bayville Beach Haven Bedminster Belle Mead Bellev ille Bellmawr Belmar Belvidere Bergenfield Berkeley Heights Berlin Bernardsville Blackwood Blairstown Bloomfield Boonton Bordentown Bound Brook Branchville Bric k Bridgeton Bridgewater Brigantine Budd Lake Burlington Butler -------------------------------------------------------------------------------- C Caldwell Califon Camden Cape May Cape May Court House Carlstadt Carteret Cedar G rove Chatham Cherry Hill Chester Clark Clementon Cliffside Park Clifton Clinton Closter Collingswood Colonia Colts Neck Cranbury Cranford -------------------------------------------------------------------------------- D Deal Denville Dover Dumont Dunellen -------------------------------------------------------------------------------- E East Brunswick East Hanover East Orange East Rutherford Eatontown Edgewater Edis on Egg Harbor City Egg Harbor Township Elizabeth Elmer Elmwood Park Emerson Engl ewood Englewood Cliffs Englishtown -------------------------------------------------------------------------------- F Fair Lawn Fairfield Fairview Fanwood Farmingdale Flanders Flemington Florham Par k Forked River Fort Lee Franklin Franklin Lakes Franklin Park Franklinville Free hold Frenchtown -------------------------------------------------------------------------------- G Garfield Glassboro -

Download This PDF File

THE JOURNAL OF THE RUTGERS UNIVERSITY LIBRARIES 29 VOTE NO: ARCHBISHOP WALSH, THE CATHOLIC CHURCH AND THE 1944 NEW JERSEY CONSTITUTION BY NICHOLAS TURSE Nicholas Turse is an Archival Processor/Researcher at the New Jersey Department of State, Division of Archives and Records Management In 1947, the state of New Jersey cast out its 1844 Constitution that had become an antiquated, patchwork liability, and adopted a modern document that became a model for excellence. When this 1947 Constitution was in development, the powers backing it made conscious and conspicuous effort to rally support behind the new document. After a plethora of failed attempts at revision, nothing was left to chance. Foremost among groups courted for support of the constitution was the Roman Catholic Church. To comprehend and appreciate the need for and eventual gain of Catholic support of the “new” 1947 Constitution, one must fully examine the issues and innerworkings of the Church’s previous opposition. By doing so one can see a political shift not only in the Church, but also in power and policy in New Jersey as a whole. Constitutional Reform and the Battle Among Politicians Beginning in the winter of 1940-1941, New Jersey began a drive for a new constitution. After numerous proposals and abortive attempts at calling a constitutional convention, constitutional reform had become an issue during the 1940 gubernatorial campaign, which pitted Franklin D. Roosevelt’s Secretary of the Navy (and Thomas Edison’s son), Democrat Charles A. Edison, against the Republican New Jersey Senator Robert C. Hendrickson (Fig. 5). Hendrickson ran his campaign by attacking Edison as a “puppet of state Democratic boss Frank Hague,” and pushing for election and court reforms via amending the 1844 Constitution.1 Edison, for his part, ran on the theme of being “Independent.” Far from being a “puppet,” Edison was actually sent by FDR to “wrest control of the pro-Roosevelt forces in the Journal of the Rutgers University Libraries, Vol. -

Of New Jersey

···- ·---··--·--·--· -····- Speeches on the Constitution oF New Jersey by Governor Charles Edison N.J. STATE LIBRARY P.O. BOX 520 TRENTON,NJ08625-0520 I 9 4 3 ·~ . ..•' .( r ,• Speeches on the Constitution of New Jersey by Governor Charles Edison FROM THE SECOND ANNUAL MESSAGE TO THE LEGISLATURE January 12, 1943 The most important problem before the State of New Jersey is an old one. It is a problem that almost every governor since the Civil War has recognized. As the years have passed, the problem has grown steadily worse, and new aspects of it have cropped up to plague each succeeding generation of citizens. The problem is how to obtain modern, effective, responsible, and economical state government under the constitution of 1844. That constitution was perhaps satisfactory for a rural, thinly settled state, such as New Jersey was a hundred years ago. There is absolutely no question that the constitution is unequal to the tasks of our present com plex, urban, industrial society. Both political parties 'in New Jersey have recognized the necessity for constitutional reform. In the last gubernatorial election, both candidates favored a constitutional convention. I urged a convention in my inaugural address: The Legislature, however, set up a Commission on the Revision of the New Jersey Constitution. That commission did an excellent job, and its unanimous report is the high point in the history of the long struggle for constitutional reform in New Jersey. Some citizens thought the proposed constitution did not go far enough. Others objected to this provision or to that omission. But the prevailing judgment of all fair-minded students was that the proposed constitution would have gone a long way tow"ard providing a more workable arid less expensive state government. -

State Government 2017 Workforce Profile

201 7 W o rk f 2 o 0 1 r 5 c e P State Government r o f i l e g n i 2017 Workforce Profile n i a Chris Christie Robert M. Czech r T Governor Chair/CEO f o Kim Guadagno e c Lt. Governori f f O with select local data Table of Contents STATE OF NEW JERSEY State Government Workforce Profile 2017 TABLE OF CONTENTS State Government Workforce Profile: Introduction ............................................................................................................................................ Page 1 State Government Workforce At-a-Glance ................................................................................................................................................. Page 3 Statistics by Agency .......................................................................................................................................................................................... Page 4 State Government Employee Work Schedules by Department ................................................................................................................. Page 6 State Government Employees in Pay Status by Work Schedule ............................................................................................................... Page 7 Distribution of State Government Employees Titles by Service Division ................................................................................................... Page 8 Age, Salary and Length of Service by State Agency ................................................................................................................................ -

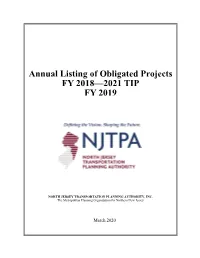

Annual Listing of Obligated Projects FY 2018—2021 TIP FY 2019

Annual Listing of Obligated Projects FY 2018—2021 TIP FY 2019 NORTH JERSEY TRANSPORTATION PLANNING AUTHORITY, INC. The Metropolitan Planning Organization for Northern New Jersey March 2020 FY 2019 Annual Listing of Obligated Projects FY 2018 – 2021 TIP North Jersey Transportation Planning Authority, Inc. The purpose of this report is to show which projects in the FY 2018-FY 2021 Transportation Improvement Program (TIP) for FY 2019 have received federal and state commitments for funding.1 A federal obligation is the result of a formal agreement, an authorization to proceed, between the NJTPA Subregions, NJDOT, NJ TRANSIT, PANYNJ and the USDOT. This agreement contractually commits the USDOT and the State of New Jersey to fund a specific phase of a project. The FY 2018 TIP included project funding for four years (FYs 2018, 2019, 2020, and 2021). This report focuses on the FY 2019 element of the FY 2018-FY 2021 TIP. State funds are obligated through a similar process within the government of New Jersey but unlike federal funds, state funds retain their obligation authority in future state fiscal years if not obligated. For the purposes of this report, non-federal funds include both State and “other funds” which are funding sources including potential local match or other partnership resources, including those of the Port Authority of New York and New Jersey and the New Jersey Turnpike Authority. Non-federal as well as federal funds are shown in this report to give a complete picture of funding as shown in the TIP. Non-federal and federal funds are mixed in some projects.