A Business History of the Swatch Group (1983-2010)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Business Networking in the Swatch Group

SPECIAL SECTION: ELECTRONIC COMMERCE AND LOGISTICS , g A b s t r a c t n i Business Networking in the Swatch k r o As part of ’The Swatch Group’ ETA SA w t supplies watch movements and spare Group e n n g s parts to all Swatch brands and other i s s e e n customers such as retailers and watch- d i s e ¨ r RAINER ALT, HUBERT OSTERLE, CHRISTIAN REICHMAYR AND u makers. To improve the quality and the l b e , RUDOLF ZURMU¨ HLEN n t efficiency of the customer relationships n n a e h ETA started a Business Networking pro- m c e g n ject in cooperation with the University a o i n t a of St Gallen. This project focused on u b m i r the complementary application of two n t i s i a Business Networking strategies that are d h c , l e usually treated separately: supply chain y l d p o p management and electronic commerce m u s e (e-commerce). Both concepts allow for , c e n c e r establishing direct relationships to the r e e f m customers. Supply chain management e r m o s enables direct deliveries to the custo- c n o c i i mers at lower costs and improved t n a r o r reliability. E-commerce provides centra- e t p c o e lized catalogues and order entry proce- l n e i : a dures with significant advantages in s ESSENCE AND RELEVANCE OF Networking. -

Contents Contents 2 4 5 6 Message from Operational Organization Organization & Distribution Organs of the Group the Chairman

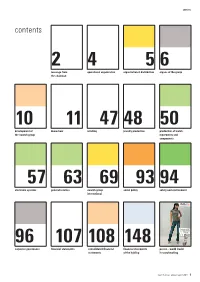

contents contents 2 4 5 6 message from operational organization organization & distribution organs of the group the chairman 10 11 47 48 50 development of know-how retailing jewelry production production of watch, the swatch group movements and components 57 63 69 93 94 electronic systems general services swatch group social policy safety and environment international 96 107 108 148 corporate governance financial statements consolidated financial financial statements poster – world leader statements of the holding in watchmaking swatch group annual report 2004 1 message from the chairman message from the chairman Ladies and Gentlemen, Shareholders, Another year has come to an end. 2004 was in fact a very good year for the Swatch Group despite some major obstacles, the first of which was – and I’m sorry to have to mention it yet again – the problem of the Swiss franc, which con- tinues to rise at a staggering rate compared with all other currencies except the euro and the pound sterling. This is causing serious problems for all of Switzer- land apart from some sections of the financial community. Some of the air of stagnation and resignation, which we see in many of our political leaders, is beginning to spread right across the country. The collapse of Swissair-Swiss then Swiss-Lufthansa is one upsetting and depressing example of this. In fact, I am outraged that in Switzerland, the land of some great business founders of the past, we are no longer able to find enough entrepreneurs capable of preserving and developing the heritage that has been handed down to us, and of which we are the guardians. -

When Corporatism Leads to Corporate Governance Failure

When corporatism leads to corporate governance failure The case of the Swiss watch industry Isabelle Schluep Campo & Philipp Aerni When corporatism leads to corporate governance failure The case of the Swiss watch industry Isabelle Schluep Campo & Philipp Aerni When corporatism leads to corporate governance failure The case of the Swiss watch industry Dr Isabelle Schluep Campo, Head of Sustainable Impact, Center for Corporate Responsibility and Sustainability (CCRS) at the University of Zurich, Zähringerstrasse 24, 8001 Zurich, Switzerland; tel. +41 44 634 40 20; email [email protected] Dr Philipp Aerni, Director of the Center for Corporate Responsibility and Sustainability (CCRS) at the University of Zurich, Zähringerstrasse 24, 8001 Zurich, Switzerland; tel. +41 44 634 40 60; email [email protected] © Isabelle Schluep Campo and Philipp Aerni 2016 ISBN: 978-0-9932932-6-9 Citation: Schluep Campo, I. and Aerni, P. 2016. When corporatism leads to corporate governance failure: the case of the Swiss watch industry. Banson, Cambridge, UK. Available online: www.ourplanet.com Published by Banson, Cambridge, UK. Printed in the UK by Cambridge Printers Contents Summary 6 Acknowledgements 8 Acronyms and abbreviations 9 1 Introduction 11 2. Historical background 15 2.1 The Foundation of ASUAG 16 2.2 The 1951 “Watch Statute” 18 2.3 Post World War II economic expansion and the 1961 Watch Statute 19 3. Corporatism in Switzerland 21 3.1 Corporatism embodied in the “Swiss made” label for watches 23 4. The crisis of the Swiss watch industry in the 1970s 27 4.1 Swiss technology commercialized elsewhere 28 4.2 The role of the Swiss banks 29 4.2.1 SSIH before the merger 29 4.2.2 ASUAG before the merger 31 5. -

Swatch Group Annual Report 2013

SWATCH GROUP ANNUAL REPORT 2013 SWATCH GROUP | ANNUAL REPORT 2013 1 Contents Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Big Brands 11 Watches and Jewelry 12–76 Retailing and Presence 77–82 Production 83 Electronic Systems 93 Corporate, Belenos 99 Swatch Group in the World 107 Governance 133 Environmental Policy 134 Social Policy 136 Corporate Governance 138 Financial Statements 2013 151 Consolidated Financial Statements 152 Financial Statements of the Holding 206 Swatch Group’s Annual Report is published in French, German and English. The text on pages 1 to 137 is originally published in French and the text on pages 138 to 216 in German. These original versions are binding. © The Swatch Group Ltd, 2014 2 SWATCH GROUP | ANNUAL REPORT 2013 | MESSAGE FROM THE CHAIR Message from the Chair Dear Madam, Dear Sir, automation, robotics and design. The Swatch SISTEM51 that we Dear Fellow Shareholders, launched in Switzerland in December 2013 is an emblematic example of this philosophy. Swatch Group is the name of the multi-faceted company that we all jointly own. The fact that it was Swatch that gave its name to This change did not only make it possible to create an incredible our company is no coincidence. Thirty-one years ago, the launch number of jobs, thus consolidating the position as a hub of of Swatch saved the Swiss watchmaking industry. On the occa- Swiss industry; it did not only save professions – which today sion of its 30th birthday, which we celebrated with a number of are undoubtedly different but are nonetheless secured; it did events in 2013, Swatch finally reached adulthood. -

The Comeback of the Swiss Watch Industry on the World Market: a Business History of the Swatch Group (1983-2010)

Munich Personal RePEc Archive The comeback of the Swiss watch industry on the world market: a business history of the Swatch Group (1983-2010) Donzé, Pierre-Yves Osaka University, Graduate School of Economics April 2011 Online at https://mpra.ub.uni-muenchen.de/30736/ MPRA Paper No. 30736, posted 06 May 2011 02:26 UTC Discussion Papers In Economics And Business The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010) Pierre-Yves DONZÉ Discussion Paper 11-14 Graduate School of Economics and Osaka School of International Public Policy (OSIPP) Osaka University, Toyonaka, Osaka 560-0043, JAPAN The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010) Pierre-Yves DONZÉ Discussion Paper 11-14 April 2011 Graduate School of Economics and Osaka School of International Public Policy (OSIPP) Osaka University, Toyonaka, Osaka 560-0043, JAPAN The Comeback of the Swiss Watch Industry on the World Market: A Business History of the Swatch Group (1983-2010)* † Pierre-Yves DONZÉ Abstract The objective of this paper is to contribute to a better understanding of the comeback of the Swiss watch industry on the world market since the end of the 1980s. It focuses on the Swatch Group (SG), currently the world’s biggest watch company. In 1983, the merger of the largest watch group (SSIH) and of the trust controlling the production of parts and movements of watches (ASUAG) into SG was the main measure taken to overcome the Japanese competition. Managed since 1986 by Nicolas G. -

Swatch Group Annual Report 2014

SWATCH GROUP ANNUAL REPORT 2014 SWATCH GROUP 1 ANNUAL REPORT 2014 CONTENTS Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Art & Philanthropy 11 Big Brands 15 Watches and Jewelry 16–80 Retailing and Presence 81–86 Production 87 Electronic Systems 97 Corporate, Belenos 103 Swatch Group in the World 111 Governance 137 Environmental Policy 138 Social Policy 140 Corporate Governance 142 Financial Statements 2014 155 Consolidated Financial Statements 156 Financial Statements of the Holding 206 Compensation Report 2014 219 Swatch Group’s Annual Report and Compensation Report are published in French, German and English. Pages 1 to 141 are originally published in French and pages 142 to 218, as well as the Compensation Report, in German. These original versions are binding. © The Swatch Group Ltd, 2015 2 SWATCH GROUP MESSAGE ANNUAL REPORT FROM 2014 THE CHAIR MESSAGE FROM THE CHAIR Dear Madam, Dear Sir, materials; we examine, we explore, we review… and, of course, Dear Fellow Shareholders, we also invent. In 2014, we registered a new patent on average every two days. “Construction site”… a term often used to identify an area where Speaking of the latest skills, we have also always invested in there are still problems to solve. I would like to use it in the way training. Swatch Group employees have bright prospects here: Swatch Group sees it: building, creating something new, devel we train several hundred apprentices and then offer them stable oping, improving, taking the bull by the horns. -

Annual Report 2018 2

www.fhs.swiss Annual Report 2018 1 Annual Report 2018 2 ISSN 1421-7384 The annual report is also available in French and German in paper or electronic format, upon request. © Fédération de l’industrie horlogère suisse FH, 2019 3 Table of contents The word of the President 4 Highlights of 2018 6 Swiss made – The revised Ordinance 8 WebIntelligence 2 – Fight against counterfeiting on the Internet 9 Training the authorities - Significant progress in Mexico 11 Access to markets – Mercosur and the United Kingdom 13 Data protection – New regulation 15 Panorama of the 2018 activities 16 Improvement of framework conditions 18 Information and public relations 22 The fight against counterfeiting 26 Standardisation 32 Legal, economic and commercial services 33 Relations with the authorities and economic circles 34 FH centres abroad 37 The Swiss watch industry in 2018 38 Watch industry statistics 40 Structure of the FH in 2018 44 The FH in 2018 46 The General Meeting 47 The Board 48 The Bureau and the Commissions 49 The Divisions and the Departments 50 The network of partners 51 The word of 5 the President Export results reported by developed entirely in-house. The FH now has the benefi t of the Swiss watch industry a high-performance, comprehensive tool to continue to fi ght in 2018 were in line with effectively against counterfeiting. forecasts. Their total value reached CHF 21.1 billion, Even though counterfeiting has shifted largely onto the internet, an increase of 6.3% com- in reality, unlawful copies of watches are still in circulation pared with 2017. -

Annual Report / 2017 1 Contents

ANNUAL 2017 REPORT THE EARTH, THE SUN, A YEAR The Earth needs about 365.25 days to complete its gravity-assisted elliptical orbit of the sun. Of course, we generally round this number down and take care of that extra quarter day every four years. Typically, a day consists of 24 hours but we often record its two 12-hour halves. The 8760 hours in Swatch Group’s 2017 were significant. This is their story. SWATCH GROUP / ANNUAL REPORT / 2017 1 CONTENTS MESSAGE FROM THE CHAIR 2 OPERATIONAL ORGANIZATION 4 ORGANIZATION AND DISTRIBUTION IN THE WORLD 5 ORGANS OF SWATCH GROUP 6 BOARD OF DIRECTORS 6 EXECUTIVE GROUP MANAGEMENT BOARD 8 EXTENDED GROUP MANAGEMENT BOARD 9 DEVELOPMENT OF SWATCH GROUP 10 ART & PHILANTHROPY 11 BIG BRANDS 19 WATCHES AND JEWELRY 20 – 84 RETAILING AND PRESENCE 85 – 90 PRODUCTION 91 ELECTRONIC SYSTEMS 101 CORPORATE, BELENOS 107 SWATCH GROUP IN THE WORLD 115 GOVERNANCE 141 ENVIRONMENTAL POLICY 142 SOCIAL POLICY 149 CORPORATE GOVERNANCE 152 FINANCIAL STATEMENTS 2017 165 CONSOLIDATED FINANCIAL STATEMENTS 166 FINANCIAL STATEMENTS OF THE SWATCH GROUP LTD 216 COMPENSATION REPORT 2017 231 PLEIADES Swatch Group’s Annual Report and The Pleiades are an open star cluster in the Compensation Report are published in constellation Taurus. They are part of the French, German and English. Milky Way and can be seen from Earth with Pages 1 to 151 are originally published in the naked eye. Its name connects it not only French and pages 152 to 230, as well as the to the nymphs in Greek mythology, but also Compensation Report, in German. -

Annual Report 2020 24 25

ANNUAL REPORT 2020 24 25 GOVERNANCE CORPORATE RESPONSIBILITY SOCIAL POLICY CORPORATE GOVERNANCE Nathan Wyburn (United Kingdom) THANK YOU Pictures of National Health Service (NHS) workers collected on social media and put together to create an image of a nurse wearing a protective mask, with the words “thank you”. To show respect to the true NHS heroes. SWATCH GROUP / ANNUAL REPORT / 2020 ART IN LOCKDOWN SWATCH GROUP / ANNUAL REPORT / 2020 GOVERNANCE 26 27 www.swatchgroup.com Legal & Functional Requirements Training Standards CORPORATE RESPONSIBILITY Product improvement Materials Homologation Laboratories OUR APPROACH TO SUSTAINABILITY GOVERNANCE compliance with regulatory requirements by all Group companies. Our high standards of quality, safety and sustainability are also CORPORATE RESPONSIBILITY This includes regular courses and training for our employees. Our required of our partners and suppliers. This includes, in particular, The Executive Group Management Board is responsible for en- Group companies are currently subject to various directives and responsible sourcing, i.e. full compliance with our Code of Conduct, Taking responsibility for the protection of life, quality of life, safe- suring compliance with our high standards in the area of sustain- technical specifications, e.g., substances that we exclude from our the principles of our business practices and zero-tolerance policy ty and health, and the protection of our environment are funda- ability. It anchors our ESG principles in our corporate strategy watch components and packaging materials, marketing and label- to human rights violations. As a company with a special responsi- mental concerns of Swatch Group. We endeavor to do the best we and defines concrete targets and measures to achieve them. -

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT of NEW YORK MONTRES BREGUET SA, BLANCPAIN SA, GLASHÜTTER UHRENBETRIEB Gmbh

Case 1:19-cv-01708-PAE Document 1 Filed 02/22/19 Page 1 of 67 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK MONTRES BREGUET S.A., BLANCPAIN S.A., GLASHÜTTER UHRENBETRIEB GmbH, Civil Action No. 1:19-cv-1708 MONTRES JAQUET DROZ S.A., OMEGA S.A., COMPAGNIE DES MONTRES LONGINES, FRANCILLON S.A., TISSOT S.A., MIDO S.A., HAMILTON INTERNATIONAL S.A. and COMPLAINT FOR FEDERAL SWATCH S.A., AND STATE TRADEMARK INFRINGEMENT, FEDERAL Plaintiffs, AND STATE UNFAIR COMPETITION, AND STATE vs. UNFAIR BUSINESS PRACTICES SAMSUNG ELECTRONICS CO. LTD., and SAMSUNG ELECTRONICS AMERICA, INC., Demand for Jury Trial Defendants. Plaintiffs Montres Breguet S.A., Blancpain S.A., Glashütter Uhrenbetrieb GmbH, Montres Jaquet Droz S.A., Omega S.A., Compagnie des Montres Longines, Francillon S.A., Tissot S.A., Mido S.A., Hamilton International S.A. and Swatch S.A. (collectively, the “Swatch Group Companies”), by their undersigned attorneys, allege as follows: NATURE OF THE ACTION 1. This action arises from Defendants’ continuing violation of the Swatch Group Companies’ invaluable federally-registered trademarks relating to high-quality, Swiss-made watches that the Swatch Group Companies sell to consumers in the United States and worldwide. 2. For decades, the Swatch Group Companies have invested many millions of dollars to design, develop, manufacture and promote their unique and exclusive watches in the United States and around the world. Those watches are sold under exclusive and famous brand Case 1:19-cv-01708-PAE Document 1 Filed 02/22/19 Page 2 of 67 names, including Blancpain, Breguet, Glashütte, Hamilton, Jaquet Droz, Longines, Mido, Omega, Swatch, and Tissot. -

Swatch Group Annual Report 2012 2012 Annual Reportannual

Swatch Group Annual Report 2012 2012 Annual ReportAnnual Swatch Group Swatch Swatch Group Annual Report 2012 The Swatch Group Ltd P.O. Box, Seevorstadt 6, CH-2501 Biel / Bienne, Switzerland Phone: +41 32 343 68 11, Fax: +41 32 343 69 11 E-mail: www.swatchgroup.com/contactus Internet: www.swatchgroup.com 2003 1991 SO FRESH 700 YEAR SET 1ST EDITION Swatch Group – Annual report 2012 1 Contents Message from the Chair 2 Operational Organization 4 Organization and Distribution in the World 5 Organs of Swatch Group 6 Board of Directors 6 Executive Group Management Board 8 Extended Group Management Board 9 Development of Swatch Group 10 Big Brands 11 Watches and Jewelry 12–72 Retailing and Presence 73–78 Production 79 Watches, Jewelry 80–88 Electronic Systems 89 Corporate, Belenos 95 Swatch Group in the World 103 Governance 127 Environmental Policy 128 Social Policy 129 Corporate Governance 131 Financial Statements 2012 143 Consolidated Financial Statements 144 Financial Statements of the Holding 206 Swatch Group’s Annual Report is published in French, Swiss-German and English. The text on pages 1 to 130 is originally published in French, the text on pages 131 to 142 in German and the text on pages 143 to 216 in English. These original versions are binding. © The Swatch Group Ltd, 2013 2 Swatch Group – Annual report 2012 – Message from the Chair Message from the Chair Dear Madam, Dear Sir, unsellable item might be sold to pick up a little spare change. Dear Fellow Shareholders, Today, can you imagine a Swatch that was not from Swatch Group? We must bear in mind that the income recorded in 1982 You may be surprised to see that the 2012 Annual Report is by the company that was, after many years and a lot of hard strongly associated with Swatch’s thirtieth birthday. -

Annual Report 2009 “WE CHOOSE to GO to the MOON.” - John F

AnnuAl RepoRt 2009 “WE CHOOSE TO GO TO THE MOON.” - John F. Kennedy Learn more by visiting the John F. Kennedy Presidential Library & Museum at www.jfklibrary.org MW18_C179_A4.indd 1 1.3.2010 9:50:22 Uhr Swatch Group – annual report 2009 1 contents contents Message from the chairman 2 operational organization 6 organization and Distribution 7 organs of the Group 8 Board of Directors 8 Executive Group Management Board and Extended Group Management Board 10 Development of the Group 12 Big Brands 13 Watches and Jewelry 14 Retailing and Landmarks 78 Production 81 Jewelry 82 Watches 84 electronic systems 93 corporate, Belenos 99 swatch Group in the World 107 Governance 129 Environmental Policy 130 Social Policy 131 Corporate Governance 132 Financial statements 2009 143 Consolidated Financial Statements 144 Financial Statements of the Holding 206 The text on pages 1 to 131 is originally published in French, the text on pages 132 to 142 in German and the text on pages 143 to 216 in English. These original versions are binding. Cover by Ted Scapa © The Swatch Group Ltd, 2010 2 Swatch Group – annual report 2009 message from the chairman MESSAGE FROM THE CHAIRMAN DEAR CO-SHAREHOLDERS LADIES AND GENTLEMEN When Swatch Group published its sales results for 2009 on Präzisionstechnik undertaken in 2008) in decline by –8.1%, 20th January this year, they were met with congratulations including losses incurred by exchange rates of CHF 105 million and enthusiastic headlines by financial analysts and journalists. (–6.3% without these losses). • Watch segment sales with a decrease of –7.7% largely Thus, for example, on 21st January 2010, a respected and outperform Federation of the Swiss Watch Industry (FH) important Swiss economic and financial newspaper headlined export sales (–22.3% in 2009), gaining market shares for the its front page with “Insolent rise in turnover – Swatch Group Group in practically all price segments and markets.