The Good Guide to Pensions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

UK DB Bulk Pensions Insurance 3Rd Edition

MARKET REVIEW 2017 HEALTH WEALTH CAREER UK DB BULK PENSIONS INSURANCE MARKET REVIEW THIRD EDITION, JUNE 2017 1 UK DB BULK PENSIONS INSURANCE 2 MARKET REVIEW 2017 CONTENTS 01 02 03 FOREWORD INTRODUCTION 2016 WAS A RECORD YEAR,AS £21 BILLION OF BULK ANNUITY TRANSFERS TOOK PLACE 04 05 06 LONGEVITY SWAPS — TAKING ACTION GETTING MORE OUT INCREASING RANGE OF AND FOCUSING ON OF YOUR BUY-IN OPTIONS FOR EFFICIENT THE END GAME LONGEVITY RISK TRANSFER 07 08 09 MERCER PENSION RISK ACHIEVING ACCOUNTING INVESTMENT EXCHANGE® — CREATING A SETTLEMENT OF BILLIONS CONSIDERATIONS CLEAR LINE OF SIGHT TO A OF POUNDS OF PENSION WHEN TRANSACTING POTENTIAL ‘END GAME’ LIABILITY, RAPIDLY A BULK ANNUITY AND AFFORDABLY 10 11 12 SCENARIOS OF FUTURE MEDICAL UNDERWRITING — MEDICAL UNDERWRITING MORTALITY NOT JUST BULK ANNUITIES — A KEY TO UNLOCKING BUT ALSO VALUATIONS OPPORTUNITIES OR THE KEY TO PANDORA’S BOX? 13 LIST OF BULK ANNUITY AND LONGEVITY SWA P TRANSACTIONS 1 UK DB BULK PENSIONS INSURANCE 01. FOREWORD WELCOME TO THE THIRD EDITION OF UK DB BULK PENSIONS INSURANCE — MARKET REVIEW. In our fast-moving, volatile economic and political world, it is now even easier than it was to miss the right deal or the right opportunity to transfer pension risk, whether that’s a buy-in, buyout or a longevity swap. Keeping in touch with the latest developments in the UK DB risk transfer market is important for all stakeholders, so we have sought Andrew Ward Mercer UK Leader to bring you more of the latest information in this Risk Transfer l Strategic Solutions Group market review, including all the latest deal statistics covering 2016 — articles 3, 4 and 13 and our view on where the market is headed in 2017 and beyond. -

Scottish Widows Retirement Saver

SCOTTISH WIDOWS RETIREMENT SAVER TERMS AND CONDITIONS Important information about Zurich pension funds Terms and conditions PAGE 18 PAGE 3 14. CHARGES AN INTRODUCTION TO THE RETIREMENT SAVER PAGE 20 WHAT IS THE RETIREMENT SAVER? 15. DISINVESTMENT STRATEGY THE PURPOSE OF THE PLAN PAGE 21 AUTO ENROLMENT 16. TAKING BENEFITS FROM YOUR PLAN SERVICES PROVIDED PAGE 25 17. WHAT HAPPENS IF YOU DIE BEFORE TAKING BENEFITS PAGE 4 WHO PROVIDES THE RETIREMENT SAVER? PAGE 26 18. LEAVING YOUR EMPLOYER WHAT INVESTMENTS ARE AVAILABLE UNDER THE RETIREMENT SAVER? 19. TRANSFERRING TO ANOTHER PENSION SCHEME EMPLOYER SELECTED THIRD PARTY SERVICE PROVIDER 20. ENDING YOUR PLAN PAGE 5 21. CHANGES WE CAN MAKE TO THE TERMS AND CONDITIONS TERMS AND CONDITIONS PAGE 27 1. YOUR CONTRACT WITH US 22. CORPORATE ACTIONS PAGE 6 PAGE 29 2. WHAT WE ASK YOU TO DO 23. GENERAL TERMS AND CONDITIONS PAGE 7 PAGE 30 3. OUR RESPONSIBILITIES 24. LAW PAGE 8 PAGE 31 4. WHO CAN HAVE A PLAN? 25. COMPENSATION 5. YOUR RIGHT TO CANCEL OR OPT OUT 26. HOW TO COMPLAIN PAGE 9 PAGE 32 6. MANAGING YOUR PLAN 27. DATA PRIVACY 7. PAYMENTS INTO YOUR PLAN 28. OUR REGULATOR PAGE 11 29. ANTI-MONEY LAUNDERING AND FRAUD 8. INVESTMENT OPTIONS 30. SANCTIONS PAGE 13 31. HMRC PRACTICE 9. CASH DEPOSITS 32. HOW TO CONTACT US PAGE 14 10. BUYING AND SELLING ZURICH PENSION FUNDS PAGE 33 PAGE 15 APPENDIX 1 – DATA PRIVACY NOTICE 11. BUYING AND SELLING WIDER MARKET INVESTMENTS PAGE 35 PAGE 16 APPENDIX 2 – OUR ORDER EXECUTION POLICY 12. SWITCHING AND REDIRECTION PAGE 38 PAGE 17 13. -

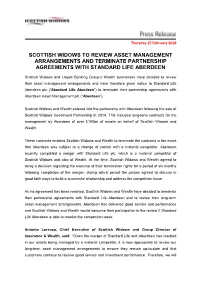

Scottish Widows to Review Asset Management Arrangements and Terminate Partnership Agreements with Standard Life Aberdeen

Thursday 15 February 2018 SCOTTISH WIDOWS TO REVIEW ASSET MANAGEMENT ARRANGEMENTS AND TERMINATE PARTNERSHIP AGREEMENTS WITH STANDARD LIFE ABERDEEN Scottish Widows and Lloyds Banking Group’s Wealth businesses have decided to review their asset management arrangements and have therefore given notice to Standard Life Aberdeen plc (“Standard Life Aberdeen”) to terminate their partnership agreements with Aberdeen Asset Management plc (“Aberdeen”). Scottish Widows and Wealth entered into the partnership with Aberdeen following the sale of Scottish Widows Investment Partnership in 2014. This included long-term contracts for the management by Aberdeen of over £100bn of assets on behalf of Scottish Widows and Wealth. These contracts enabled Scottish Widows and Wealth to terminate the contracts in the event that Aberdeen was subject to a change of control with a material competitor. Aberdeen recently completed a merger with Standard Life plc, which is a material competitor of Scottish Widows and also of Wealth. At the time, Scottish Widows and Wealth agreed to delay a decision regarding the exercise of their termination rights for a period of six months following completion of the merger, during which period the parties agreed to discuss in good faith ways to build a successful relationship and address the competition issue. As no agreement has been reached, Scottish Widows and Wealth have decided to terminate their partnership agreements with Standard Life Aberdeen and to review their long-term asset management arrangements. Aberdeen has delivered good service and performance and Scottish Widows and Wealth would welcome their participation in the review if Standard Life Aberdeen is able to resolve the competition issue. -

Our Investments

Wood Pension Plan Investment Policy Implementation Document – May 2021 (replaces March 2021) 1. Introduction The Statement of Investment Principles (“SIP”) of the Wood Pension Plan (the “Plan”) sets out the guiding principles upon which the Plan’s investments are based. The purpose of this Investment Policy Implementation Document (“IPID”) is to provide details of the specific investments in place alongside other information relevant to the management of the investments. Investment policy can be considered in two parts; the strategic management, the setting of which is one of the fundamental responsibilities of the Trustee, and the day-to-day management of the assets, which is delegated to professional investment managers. The Plan provides two types of benefit; one linked to final salary (Defined Benefit Section) and the other of a money purchase type (Defined Contribution Section). 2. Strategic Management - Defined Benefit Section The benchmark allocation of the Plan’s assets between the major asset classes is detailed in the table overleaf. The benchmark allocation will be reviewed by the Trustee on an ongoing basis in line with any changes to the Plan’s investment strategy. Page 2 Benchmark Asset Class Allocation (%) Benchmark Return-Seeking Assets 15.0 Global Listed Equities 15.0 MSCI AC World (NDR) Index 1 Private Equity - 2 n/a Mid-Risk / Cashflow Matching 30.0 Assets Property - 3 n/a Corporate Bonds – UK Buy & 10.0 iBoxx Sterling Non-Gilts Index Maintain – RLAM4 Corporate Bonds – Global Buy & 10.0 Barclays Global Aggregate Corporate Maintain - PGIM4 (GBP Hedged) Index Corporate Bonds – Global Buy & 10.0 ICE BofA Merrill Lynch Sterling Non Gilts Maintain - AXA4 Index Liability Matching Assets 55.0 Liability-Driven Investment 55.0 n/a Total 100.0 1 Global equity benchmark at total Plan level. -

Scottish Widows Limited Annual Report

Scottish Widows Limited Annual Report and Accounts 2020 Member of Lloyds Banking Group SCOTTISH WIDOWS LIMITED (03196171) CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS CONTENTS PAGE(S) Company Information 3 Group Strategic Report 4-15 Directors’ Report 16-20 Independent Auditors’ Report to the Member of Scottish Widows Limited 21-30 Consolidated Statement of Comprehensive Income for the year ended 31 December 2020 31 Balance Sheets as at 31 December 2020 32 Statements of Cash Flows for the year ended 31 December 2020 33 Statements of Changes in Equity for the year ended 31 December 2020 34 Notes to the Financial Statements for the year ended 31 December 2020 35-118 2 SCOTTISH WIDOWS LIMITED (03196171) CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS COMPANY INFORMATION Board of Directors N E T Prettejohn (Chair) J R A Bond W L D Chalmers K Cheetham J E M Curtis J C S Hillman* J F Hylands A Lorenzo* C J G Moulder S J O’Connor G E Schumacher * denotes Executive Director Company Secretary J M Jolly Independent Auditors PricewaterhouseCoopers LLP Chartered Accountants and Statutory Auditors 2 Glass Wharf Temple Quay Bristol BS2 0FR Registered Office 25 Gresham Street London EC2V 7HN Company Registration Number 03196171 3 SCOTTISH WIDOWS LIMITED (03196171) CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS GROUP STRATEGIC REPORT The Directors present their strategic report on Scottish Widows Limited ('the Company') and its subsidiary undertakings (together referred to as 'the Group') for the year ended 31 December 2020. The Company is limited by share capital. The Group contributes to the results of the Insurance and Wealth Division of Lloyds Banking Group. -

Living in a 1% World

LivingLiving inin aa 1%1% WorldWorld FredFred GoodwinGoodwin GroupGroup ChiefChief ExecutiveExecutive Slide 2 Living in a 1% World 1% World Stakeholder pensions Sandler regulated products Slide 3 Living in a 1% World Implications for RBS Lower margins on long term savings Less than 1% of RBS income from long term savings Higher volumes of distribution of long term savings Simpler products, processes better for bank distribution Slide 4 Living in a 1% World What are the required characteristics for growth? Slide 5 Required Characteristics for Growth Organic growth – Large distribution capacity – Multiple brands – Low market shares – Effective sales processes – Able to grow new businesses – Diversity of income Acquisitions – Able to make good acquisitions – Good at integration of acquisitions Efficiency – Able to improve efficiency Slide 6 Large Distribution Capacity Distribution Channels UK Ranking Branches #1 Supermarkets #1 Telephone #1 = Internet #? (large) ATMs #1 Relationship Managers #1 Source: Company Accounts, CACI and Link Slide 7 Multiple Brands Multi-Brand, Multiple Channel Strategy Slide 8 Multiple Brands Multi-Brand, Multiple Channel Strategy Appeals to different customer groups Allows different product variants, pricing Gives flexibility for future Allows management autonomy Slide 9 Low Market Shares UK Market Shares Total RBS Current accounts 21% Savings accounts 8% Personal loans 10% Mortgages 5% Credit cards 17% Life insurance 2% Motor insurance 16%* Home insurance 13%* Small business relationships 30% -

How to Analyse Workplace Pension Default Funds

How to analyse workplace pension default funds April 2020 Sponsors Accredited by Contents Introduction 3 Who should read this guide? 4 Part 1 – Key factors to consider when 5 reviewing default funds Key factors to consider when reviewing a default fund 8 Part 2 – Comparison of default funds 21 Summary 31 Conclusion 33 Test yourself for CPD 35 Appendix A 37 2 Introduction Welcome to the Defaqto annual guide to reviewing workplace pension default funds. Taking our standard impartial position, we explain the key factors to consider when reviewing default funds and then take a deep-dive into the most commonly used schemes. Last year, 2019, was interesting. The higher 8% contribution rate came into force and a new tough authorisation standard was introduced by The Pensions Regulator (TPR) for master trusts. The higher contribution rate didn’t create the mass increase in opt-outs that some pundits had predicted and so, positively, record numbers of employees continue to save for their retirement. The new authorisation process had a much bigger impact, with over half of master trusts closing in 2019. In addition, those that remain now need to maintain standards in order to retain their authorisations. The 2020/21 year will also be an interesting one after the FCA introduced minimum standards for publishing and disclosing costs and charges to workplace pension members. When it comes to choice, we still have a healthy and diverse array of scheme types and investment strategies to choose from. However, we can see a void growing between the well-managed and performing default funds and those where improvements are needed. -

Judgment (PDF)

Trinity Term [2011] UKSC 32 On appeal from: [2010] CSIH 47; [2008] UKSPC 664 JUDGMENT Scottish Widows plc (Appellant) v Commissioners for Her Majesty's Revenue and Customs (Respondent) (Scotland) Scottish Widows plc No 2 (Appellant) v Commissioners for Her Majesty's Revenue and Customs (Respondent) (Scotland) Scottish Widows plc (Respondent) v Commissioners for Her Majesty's Revenue and Customs (Appellant) (Scotland) before Lord Hope, Deputy President Lord Walker Lady Hale Lord Neuberger Lord Clarke JUDGMENT GIVEN ON 6 July 2011 Heard on 16 and 17 May 2011 Appellant Respondent John Gardiner QC Andrew Young QC David Johnston QC Kenneth Campbell Philip Walford (Instructed by Maclay (Instructed by Office of Murray & Spens LLP) the Solicitor to the Advocate General for Scotland) Cross Appellant Cross Respondent Andrew Young QC John Gardiner QC Kenneth Campbell David Johnston QC Philip Walford (Instructed by Office of (Instructed by Maclay the Solicitor to the Murray & Spens LLP) Advocate General for Scotland) LORD HOPE 1. This is an appeal from an interlocutor of the First Division of the Inner House of the Court of Session (the Lord President (Hamilton), Lord Reed and Lord Emslie) in a joint referral to the Special Commissioners by Scottish Widows Plc (“the Company”) and Her Majesty’s Revenue and Customs (“HMRC”) under para 31 of Schedule 18 to the Finance Act 1998: [2010] CSIH 47, 2010 SLT 885, 2010 STC 2133. The question that was referred to the Special Commissioners for their determination was in these terms: “Whether in computing the -

Uk Db Bulk Pensions Insurance

MARKET REVIEW 2016 HEALTH WEALTH CAREER UK DB BULK PENSIONS INSURANCE MARKET REVIEW SECOND EDITION, JULY 2016 1 UK DB BULK PENSIONS INSURANCE 2 MARKET REVIEW 2016 CONTENTS 01 02 03 FOREWORD - A BUMPY START - £12 MEDICAL UNDERWRITING WELCOME TO THE BILLION OF BULK ANNUITY – A KEY TO UNLOCKING SECOND EDITION TRANSFERS TOOK PLACE IN OPPORTUNITIES OR THE THE FIRST HALF OF 2016 KEY TO PANDORA’S BOX? 04 05 06 LONGEVITY SWAPS – THE ART OF ASSESSING MERCER PENSION RISK INCREASING RANGE OF YOUR SCHEME’S LONGEVITY EXCHANGE® - CREATING A OPTIONS FOR EFFICIENT RISK AND DECIDING CLEAR LINE OF SIGHT TO A LONGEVITY RISK TRANSFER WHETHER TO BUY POTENTIAL “END GAME” PROTECTION 07 08 09 A REVOLUTION IN THE ALIGNING INVESTMENTS AS WHY ARE INCREASING SETTLEMENT OF LARGE PART OF A BULK ANNUITY NUMBERS OF SCHEMES PENSION LIABILITIES TRANSACTION C A R R Y I N G O U T A PENSIONER BUY-IN? 10 LIST OF BULK ANNUITY AND LONGEVITY SWAP TRANSACTIONS 1 UK DB BULK PENSIONS INSURANCE 01. FOREWORD WELCOME TO THE SECOND EDITION OF UK DB BULK PENSIONS INSURANCE — MARKET REVIEW. In our fast moving and volatile “post Brexit” world, it is now even easier than it was to miss the right deal or the right opportunity. Bulk pensions insurance policies are irreversible and decisions made, or not made, have long-lasting outcomes. Keeping in touch with the latest developments in the UK DB bulk pensions insurance market is David Ellis Mercer UK Leader, important for all stakeholders, so we have sought Bulk Pensions Insurance Advisory to bring you the latest information in this market review, including all the latest deal statistics – articles 02, 04 and 10, and how to get actual insurer prices every month – article 06. -

Aon's UK Risk Settlement Market Review 2020

Aon’s UK Risk Settlement Market Review 2020 Helping you navigate through the bulk annuity, longevity swap and consolidation options Welcome What a year 2019 was for the UK risk settlement market! Bulk annuities Market Insights The volumes of bulk annuity transactions exceeded £43bn in 2019, Our 2019 transactions were characterised by both collaboration and which is well in excess of historic totals (the previous high being innovation. We are excited to share market insights from a selection c£24bn, in 2018). Activity during 2019 led to at least six of the eight of the Aon-led transactions with you throughout this risk settlement insurers writing their highest volume of business in their history, and market review report: four of the eight insurers writing the largest UK bulk annuity transac- • Asda Group Pension Scheme - why was demand from large tion in their history. Completing this volume of transactions required schemes so high in 2019? the market to find new solutions to both old and new issues, paving Martin Bird the way for more schemes to de-risk through bulk annuities in the • HSBC Bank (UK) Pension Scheme - the sign of more Senior Partner and Head to come? future. of Risk Settlement We are incredibly proud to say that Aon has been at the • telent GEC 1972 Plan – successfully transitioning a complex [email protected] forefront of this, having been the lead adviser on bulk annuity £4.7bn asset portfolio transactions totalling over £20bn of liabilities in 2019, and • National Grid UK Pension Scheme - when you can’t secure enhancing security for over 100,000 scheme members during the full scheme, how do you choose which members to insure? the year. -

Life Fund Scottish Widows Cautious Growth Life

Cautious 31 August 2021 Life Fund Scottish Widows Cautious Growth Life Asset Allocation (as at 30/06/2021) This document is provided for the purpose of UK Fixed Interest 31.3% information only. This factsheet is intended for individuals who are familiar with investment Global Fixed Interest 25.8% terminology. Please contact your financial UK Equities 9.4% adviser if you need an explanation of the terms used. This material should not be relied upon Global Equities 7.8% as sufficient information to support an Property Shares 6.9% investment decision. The portfolio data on this Money Market 6.3% factsheet is updated on a quarterly basis. Futures 3.5% North American Equities 3.3% Fund Aim Global Emerging Market Equities 3.0% The Fund aims to provide exposure primarily to bonds (this may include UK Government Other 2.8% bonds, index- linked securities, other UK fixed interest securities, overseas bonds and high Asset Allocation Relative to Strategic Asset Allocation yield bonds) and property (which can be both in the UK and overseas). The Fund may also (as at 30/06/2021) provide exposure to equities (which may include UK, overseas and emerging markets), commodities and other alternative assets such as derivatives. In addition the Fund has the power to invest in other asset classes permitted by FCA rules. Basic Fund Information Fund Launch Date 28/06/2010 Fund Size £379.1m ISIN - MEX ID - SEDOL - Manager Mark Henzell, Matthew Names Davies Manager Since 28/06/2010, 01/07/2013 The composition of asset mix and asset allocation may change at any