Thanet Retail and Leisure Assessment – July 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Swale Borough Council

SWALE BOROUGH COUNCIL Project: RETAIL STUDY 2010: Bulky and DIY Goods Addendum Latest Revision: 20/05/2011 - DRAFT Study area population by zone Zone 2010 2015 2020 2025 1 39,501 40,410 41,418 42,595 2 12,888 13,185 13,514 13,897 3 46,052 47,112 48,287 49,659 4 11,242 11,501 11,788 12,123 5 19,162 19,603 20,092 20,663 6 5,340 5,463 5,599 5,758 TOTAL 134,185 137,274 140,698 144,695 Sources/notes for frontispiece 1. 2010 population for each zone from Pitney Bowes Business Insight Area Profile Report (6 July 2010) 2. Growth in population based on growth rates implied by scenarioKent County 3 of Council 6 scenarios population prepared forecasts by Research for Swale & Intelligence, Borough - South Kent CouEastntyPlan Council Strategy (16- Septemberbased Forecasts 2010). (September The KCC projections 2009) Total are Population based on SwaleForecasts. Borough Available: Counciil's 'Option 1' for newhttps://shareweb.kent.gov.uk/Documents/facts homes which assumes an additional 13,503-and dwellings-figures/sep between-forecasts 2006-sep-2031-09 -usingweb.pdf a phasing Access provideddate: 12 byOctober SBC 2010 OTHER COMPARISON GOODS Table 3.1 Expenditure per capita (£) Zone 2007 2010 2015 2020 2025 1 2,062 2,162 2,592 3,124 3,764 2 2,356 2,470 2,962 3,569 4,301 3 2,164 2,269 2,721 3,278 3,950 4 2,336 2,449 2,937 3,539 4,264 5 2,194 2,300 2,758 3,324 4,005 6 2,347 2,460 2,951 3,555 4,284 Sources/notes for Table 3.1 1. -

Regeneration and Economic Development Policy Overview and Scrutiny Committee

KENT COUNTY COUNCIL REGENERATION AND ECONOMIC DEVELOPMENT POLICY OVERVIEW AND SCRUTINY COMMITTEE MINUTES of a meeting of the Regeneration and Economic Development Policy Overview and Scrutiny Committee held in the Council Chamber, Sessions House, County Hall, Maidstone on Wednesday, 17 November 2010. PRESENT: Mr M C Dance (Chairman), Mr I S Chittenden (Vice-Chairman), Mr A R Chell, Mr K A Ferrin, MBE, Mr P J Homewood, Mrs J P Law, Mr K H Pugh, Mrs J A Rook, Mr K Smith, Mr M V Snelling and Mrs E M Tweed ALSO PRESENT: Mr K G Lynes, Mr M J Whiting and Mr M A Wickham IN ATTENDANCE: Mr D Cockburn (Executive Director, Strategy, Economic Development & ICT), Mr N Smith (Head of Development Investment), Mr M Bodkin (Head of Urban Regeneration), Mrs T Bruton (Head of Regeneration Projects) and Miss T Grayell (Democratic Services Officer) UNRESTRICTED ITEMS 45. Minutes of the meeting held on 23 September 2010 (Item A3) RESOLVED that the Minutes of the meeting held on 23 September 2010 are correctly recorded and that they be signed by the Chairman. 46. Update on District Visits (Item B1) Mr M J Whiting, Member for Swale Central, was present for this item and spoke on it with the permission of the Chairman. Mr M Bodkin, Head of Urban Regeneration, Mrs T Bruton, Head of Regeneration Projects, Mr P Campion, Development Contributions Manager, Mrs H Coleman, Economic Development Manager, Mr R Hancock, Regeneration and Projects Manager, Mr D Hughes, Regeneration and Projects Manager, Mr I Lewis, Growth Areas Manager, and Mr K Mackenney, Regeneration and Projects Manager, were in attendance for this item. -

Archaeological Evaluation Report Westwood Cross, Thanet Kent

Archaeology South-East ASE Archaeological Evaluation Report Westwood Cross, Thanet Kent NGR: TR 36455 67441 Planning Ref: F/TH/12/0781 ASE Project No: 6729 Site Code: TWE14 ASE Report No: 2014159 OASIS id: archaeol6-179227 Catherine Douglas Archaeological Evaluation Report Westwood Cross, Thanet Kent NGR: TR 36455 67441 Planning Ref: F/TH/12/0781 ASE Project No: 6729 Site Code: TWE14 ASE Report No: 2014159 OASIS id: archaeol6-179227 Catherine Douglas With contributions by Anna Doherty and Karine Le Hégarat Illustrations by Justin Russell May 2014 Archaeology South-East Units 1 & 2 2 Chapel Place Portslade East Sussex BN41 1DR Tel: 01273 426830 Fax: 01273 420866 Email: [email protected] Archaeology South-East Eval: Westwood Cross, Thanet, Kent ASE Report No: 2014159 Abstract Archaeology South-East was commissioned by CgMs Ltd, to undertake an archaeological evaluation by trial trenching on land at Westwood Cross, Thanet, Kent. Five trenches were excavated. A single undated post hole containing a piece of struck flint was identified in Trench 2, and a sherd of medieval pottery was retrieved from the topsoil in Trench 5. Some degree of modern truncation was identified in Trench 1, but the paucity of archaeology in the other trenches and the survival of an intact subsoil horizon suggest a lack of past activity on the site. © Archaeology South-East UCL i Archaeology South-East Eval: Westwood Cross, Thanet, Kent ASE Report No: 2014159 CONTENTS 1.0 Introduction 2.0 Archaeological Background 3.0 Archaeological Methodology 4.0 Results 5.0 The Finds -

Web List.Xlsx

WELSH STORE CLOSURES Store Address CLOSE DATE Aberdare The Works, 2 & 3 Commercial Street, Aberdare, CF44 7RW Closed from Sunday 20th December Abergavenny TheWorks.co.uk, Unit 3, Cibi Shopping Centre, Abergavenny, NP7 5AJ Closed from Sunday 20th December Aberystwyth The Works, 35 Terrace Road, Aberystwyth, SY23 2AE Closed from Sunday 20th December Bangor The Works, 241 High Street, Bangor, LL57 1PA Closed from Sunday 20th December Barry The Works, Unit 4, 110-118 Holton Road, Barry, CF63 4HH Closed from Sunday 20th December Brecon TheWorks.co.uk, Unit 14/15, Bethel Square Shopping Centre, Brecon, LD3 7JP Closed from Sunday 20th December Bridgend TheWorks.co.uk, 22 Adare Street, Bridgend, CF31 1EJ Closed from Sunday 20th December Bridgend Outlet TheWorks.co.uk, Unit 86a, Welsh Designer Village, Pen-Y-Cae, Bridgend, CF32 9SU Closed from Sunday 20th December Caernarfon The Works, 11 Pool Street, Caernarfon, LL55 2AD Closed from Sunday 20th December Caerphilly TheWorks.co.uk, Unit 8, Castle Court Shopping Centre, Caerphilly, CF83 1NU Closed from Sunday 20th December Cardiff Queens Street The Works, 16 Queens Street, Cardiff, CF10 2BU Closed from Sunday 20th December Cardigan The Works, 7 / 8 High Street, Cardigan, SA43 1HJ Closed from Sunday 20th December Carmarthen The Works, 11 Pool Street, Caernarfon, LL55 2AD Closed from Sunday 20th December Colwyn Bay The Works, 11 Bay View Centre, Sea View Road, Colwyn Bay, LL29 8DG Closed from Sunday 20th December Cwmbran TheWorks.co.uk, 2-4 The Parade, Cwmbran Shopping Centre, Cwmbran, NP44 1PT Closed -

34 Bus Time Schedule & Line Route

34 bus time schedule & line map 34 Birchington-On-Sea View In Website Mode The 34 bus line (Birchington-On-Sea) has 6 routes. For regular weekdays, their operation hours are: (1) Birchington-On-Sea: 8:20 PM - 9:20 PM (2) Margate: 5:18 AM - 2:03 PM (3) Margate: 6:57 AM (4) Minnis Bay: 6:30 AM - 5:48 PM (5) Ramsgate: 5:58 AM - 6:07 PM (6) Westwood: 6:51 PM Use the Moovit App to ƒnd the closest 34 bus station near you and ƒnd out when is the next 34 bus arriving. Direction: Birchington-On-Sea 34 bus Time Schedule 16 stops Birchington-On-Sea Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 8:20 PM - 9:20 PM Cecil Square, Margate Cecil Square, Margate Tuesday 8:20 PM - 9:20 PM Marine Terrace, Margate Wednesday 8:20 PM - 9:20 PM Hall by the Sea Road, Margate Thursday 8:20 PM - 9:20 PM Nayland Rock, Westbrook Friday 8:20 PM - 9:20 PM Albert Road, Margate Saturday 8:20 PM - 9:20 PM Royal Sea Bathing, Westbrook 77 Canterbury Road, Margate Waverley Road, Garlinge 34 bus Info The Hussar, Garlinge Direction: Birchington-On-Sea 221 Canterbury Road, Margate Stops: 16 Trip Duration: 14 min St James' Park Road, Garlinge Line Summary: Cecil Square, Margate, Marine 218 Canterbury Road, Margate Terrace, Margate, Nayland Rock, Westbrook, Royal Sea Bathing, Westbrook, Waverley Road, Garlinge, Walmer Castle, Westgate-On-Sea The Hussar, Garlinge, St James' Park Road, Garlinge, Canterbury Road, Margate Walmer Castle, Westgate-On-Sea, Library, Westgate- On-Sea, Domneva Road, Westgate-On-Sea, Hengist Library, Westgate-On-Sea Road, Birchington-On-Sea, -

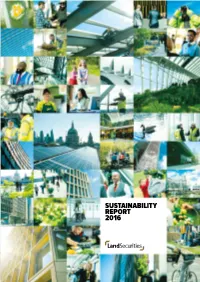

SUSTAINABILITY REPORT 2016 Progress Commitments

SUSTAINABILITY REPORT 2016 Progress Commitments Complete Existing commitment (retained) AT A GLANCE On track Existing commitment (extended) Not on track New commitment Our Commitments and Progress to date CREATING JOBS AND OPPORTUNITIES EFFICIENT USE OF NATURAL RESOURCES COMMUNITY RENEWABLE EMPLOYMENT FAIRNESS ELECTRICITY WASTE COMMITMENT COMMITMENT COMMITMENT COMMITMENT Help a total of 1,200 Ensure the working Continue to procure 100% Send zero waste to landfill with disadvantaged people secure environments we control are renewable electricity across at least 75% recycled across all jobs by 2020 fair and ensure that everyone our portfolio our operational and construction who is working on our behalf activities by 2020 PROGRESS – within an environment we PROGRESS control – is paid at least the PROGRESS Employment secured Living Wage by 2020 As of 1 April 2016, our for 779 people from group electricity contract is Diverting 98.6% from landfill and disadvantaged backgrounds PROGRESS 100% renewable recycling 72% All tenders and contractual clauses for new developments ENERGY now stipulate Living Wage CARBON requirements COMMITMENT COMMITMENT DIVERSITY HEALTH, SAFETY AND SECURITY Reduce carbon intensity Reduce energy intensity (kWh/ 2 2 (kgCO2/m ) by 40% by 2030 m ) by 40% by 2030 compared compared to a 2013/14 to a 2013/14 baseline, for COMMITMENT COMMITMENT baseline, for property under property under our management Make measurable Maintain an exceptional our management for at least for at least two years improvements to the profile standard -

Thanet District Transport Strategy Draft Infrastructure Plan

Potential Marine Terrace Public Thanet District Transport Strategy Realm Improvements Westwood Cross Relief Strategy Reroute Tourist Traffic Away From Seafront Draft Infrastructure Plan Star Lane Improvements Delivered 2015 Poorhole Lane Link Delivered 2015 Improve pedestrian facilities & provide bus priority through the centre of Westwood (As per Oxford Circus above). Open up future frontage devel- Star Lane Link opment opportunities Delivered 2012 Potential Potential Feature Description Funding Feature Description Funding Reconfigure roundabout at Queens Source Source Avenue/Tivoli Road/Grosvenor Gardens and introduce one-way Upgrade footpath TM31 to bridleway to link to bridleway flow on Queens Avenue Tesco Link Road Between Create New Road Link Between A28 Brooksend Hill On Site Delivery TBC Improve Capacity 13 TE12A & link to Shottendane Road improvements to S106 / 38 (Subject to Funding) 1-2 and Minnis Road. (S106) Two Lane Approach to provide shared use pedestrian cycle route. Westwood Cross Roundabout Between Road link between A28 Brooksend Hill and Acol Hill/ On Site Improvement of Bridleway TM22 surface to width of 3m 2-3 B2050. (S38)(S106) 14 S106 / 38 as part of Garlinge development. St Nicholas at Wade Extension to Millennium Way Between Widen B2050 Manston Road between junction with On Site Manston to Haine Road Link Upgrade Footpath TM14 on edge of development to Delivery TBC 3-4 Acol Hill and Shottendane Road. (S38)(S106) 15 S106 / 38 Bridleway. Widen / Improvements to Shottendane Road as far as New Cross Road Between the vicinity of Firbank Gardens, Margate and improve S106 Reintroduce Two-Way Traffic Flow on Delivered 2014 16 Provide improved surface and widen Bridleway TM11 S106 / 38 Tivoli Road—Junction Improvement 4-8 junctions with Park Road, Minster Road and High LGF Street Garlinge. -

Town Centre Retail, Leisure, Tourism and Culture Assessment

Town Centre Retail, Leisure, Tourism and Culture Assessment Appendices Thanet District Council December 2012 13115/PW/JeH/HFo This document is formatted for double sided printing. © Nathaniel Lichfield & Partners Ltd 2012. Trading as Nathaniel Lichfield & Partners. All Rights Reserved. Registered Office: 14 Regent's Wharf All Saints Street London N1 9RL All plans within this document produced by NLP are based upon Ordnance Survey mapping with the permission of Her Majesty’s Stationery Office. © Crown Copyright reserved. Licence number AL50684A Thanet District Council : Town Centre Retail, Leisure, Tourism and Culture Assessment Appendices1 Appendix 1 Study Area and Methodology Appendix 2 Existing Retail Facilities Appendix 3 Audit of Centres Appendix 4 Convenience Assessment Appendix 5 Comparison Assessment Appendix 6 Household Survey Results Appendix 7 In-Centre Survey Results 3392928v1 Thanet District Council : Town Centre Retail, Leisure, Tourism and Culture Assessment Appendix 1 Study Area and Methodology 3392928v1 Thanet District Council : Town Centre Retail, Leisure, Tourism and Culture Assessment Thanet Retail Study Area Zones Table 1.1 Thanet Retail Study Area Zones and Postcode Sectors Zone Area Postcode Sectors 1 Margate East CT9 2 CT9 3 2 Margate West CT9 1 CT9 4 CT9 5 3 Broadstairs/Westwood CT10 1 CT10 2 CT10 3 4 Ramsgate CT11 0 CT11 7 CT11 8 CT11 9 CT12 6 5 Westgate/Birchington CT7 9 CT8 8 6 Thanet Rural CT7 0 CT12 4 CT12 5 3392928v1 Thanet District Council : Town Centre Retail, Leisure, Tourism and Culture Assessment Plan 1: Study Area 3392928v1 Thanet District Council : Town Centre Retail, Leisure, Tourism and Culture Assessment Retail Capacity Assessment – Methodology and Data Price Base 1.1 All monetary values expressed in this study are at 2010 prices, consistent with Experian’s base year expenditure figures for 2010 (Retail Planner Briefing Note 9), which is the most up to date information available. -

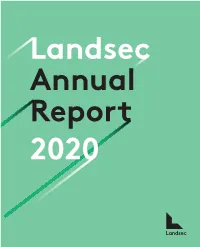

Annual Report 2020 Welcome to Landsec 2020 in Numbers Here Are Some of the Our Portfolio Important Financial and Non-Financial Performance Figures for Our Year

Annual Annual Report 2020 Landsec Annual Report 2020 Welcome to Landsec 2020 in numbers Here are some of the Our portfolio important financial and non-financial performance figures for our year. Some of these measures are impacted by Covid-19. 23.2p Dividend, down 49.1% 55.9p Adjusted diluted earnings per share (2019: 59.7p) Office Retail Specialist Our Office segment consists of Our Retail segment includes outlets, Our Specialist segment comprises high-quality, modern offices in great retail parks, large regionally dominant 17 standalone leisure parks, 23 hotels 1,192p locations in central London. Our offer shopping centres outside London and the iconic Piccadilly Lights in EPRA net tangible assets ranges from traditional long-term and shopping centres within London. central London. per share, down 11.6% leases through to shorter-term, flexible We also have great retail space within Pages 24-29 space. We also have significant our office buildings. development opportunities. Pages 24-29 Pages 24-29 -8.2% Total business return (2019: -1.1%) A £12.8bn portfolio Chart 1 10 1. West End office 26% 9 £11.7bn 2. City office 13% 8 1 Total contribution to 3. Mid-town office 11% the UK economy each 4. Southwark and other office 4% 7 year from people based 5. London retail 11% Combined at our assets 6. Regional retail 13% 7. Outlets 7% Portfolio 6 8. Retail parks 3% 2 9. Leisure and hotels 9% £(837)m 10. Other 3% 5 Loss before tax 3 4 (2019: £(123)m) Read more on pages 174-177 Comprising 24 million sq ft Chart 2 -4.5% Ungeared total property of space return (2019: 0.4%) 1 1. -

RC Car Racer WHS HS Sep20.Xls

RC CAR RACER - WHS HS STORE LIST SEPT 20 STORE_NUMBERSTORE_NAME ADDRESS_1 1016 ABERGAVENNY 1 CIBI WALK 1024 ABERYSTWYTH 36 TERRACE ROAD 1038 ABERDEEN ST NICHOLLS UNIT E5 1074 ALDERSHOT 12A WELLINGTON CENTRE 1106 ALFRETON UNIT B 1148 ARGYLE ST 53-55 ARGYLE STREET 1206 AYLESBURY 27/29 HIGH STREET 1316 BARNSTAPLE 76 HIGH STREET 1332 BARROW 38-42 PORTLAND WALK 1340 BASILDON 29 TOWN SQUARE 1356 BATH UNION STREET 6/7 UNION STREET 1414 BEDFORD 29/31 THE HARPUR CENTRE 1486 BEXLEYHEATH 89 THE BROADWAY 1532 BIRKENHEAD 37 BOROUGH PAVEMENT 1534 BIRMINGHAM UNION ST 29 UNION STREET 1538 BISHOPS STORTFORD 1 SOUTH STREET 1646 BOLTON 5-7 VICTORIA SQUARE 1704 BOURNEMOUTH CASTLE POINT UNIT P 1708 BOURNEMOUTH 9 - 13 OLD CHRISTCHURCH ROAD 1724 BRACKNELL 10 PRINCESS SQUARE 1750 BRAINTREE 19 GEORGE YARD 1802 BRIDGNORTH 40/41 HIGH STREET 1854 BRISTOL GALLERIES THE GALLERIES 1892 BROUGHTON PARC BROUGHTON PARK 1980 BURTON ON TRENT 13/17 UNDERHILL WALK 1998 BURY ST EDMUNDS 15 CORNHILL 2014 BUXTON UNIT 1 THE SPRINGS SHOPPING CENTRE 2088 CANTERBURY 19 ST GEORGE STREET 2106 CARDIFF 83/85 QUEEN STREET 2122 CARLISLE 51/53 ENGLISH STREET 2250 CHELMSFORD 73/75 HIGH STREET 2258 CHELTENHAM HIGH ST 192/194 HIGH STREET 2272 CHESTERFIELD 4 MIDDLE PAVEMENT 2292 CHESTER 5/7 FOREGATE STREET 2302 CHICHESTER 16 NORTH STREET 2318 CHIPPENHAM 2 THE HIGH STREET 2336 CHRISTCHURCH SAXON SQUARE SHOPPING CENTRE 2360 CIRENCESTER 19/21 CASTLE STREET 2456 COLCHESTER 19 CULVER WALK 2490 COVENTRY WEST ORCHARD SHOPPING CENTRE 2514 CRIBBS CAUSEWAY UNIT LR 1 & 2 2520 CREWE 13 VICTORIA CENTRE 2566 -

Download Where Retail Happens 2016 Issue 3

150.5mm 10mm 150.5mm 2016 2016 Issue 3/Autumn 2016 happens retail Where Where retailWhere happens At Hammerson, we create destinations that excite shoppers, attract and support retailers, reward investors and serve communities; destinations where more happens. hammerson.com [email protected] 210mm London Kings Place, 90 York Way, London N1 9GE +44 (0) 20 7887 1000 Paris 48 rue Cambon 75001 Paris +33 (0)1 56 69 30 00 Dublin Harcourt Centre, Harcourt Street, Dublin 2 +353 86 248 9065 BACK COVER SPINE OUTER FACE / FRONT COVER 150.5mm 10mm 150.5mm Aberdeen Belfast Birmingham Bristol Didcot Dublin Falkirk Glasgow Gloucester Kirkcaldy Where fashion happens Leeds Where fun happens Leicester Where footfall happens London Where retail happens Luton Where retail happens We are Hammerson. As a leading Middlesbrough owner-manager and developer of retail Paisley destinations, we are proud to be behind Reading some of the greatest retail experiences 210mm Rugby in Europe. Our £10 billion real estate Southampton portfolio comprises 22 prime regional Swansea shopping centres, 19 convenient retail Thanet parks and investments in 15 premium designer outlet villages which draw Our portfolio and excite shoppers and attract and Aulnay-sous-Bois support retailers. Our success is the result of putting more time, more care, more Beauvais knowledge and more imagination into Cergy-Pontoise our projects. By doing this, we create Marseille destinations where more happens. Nancy Nice Paris Saint-Quentin-en-Yvelines Strasbourg SPINE DIRECTORY BOOK INSERT FIXED HERE WELCOMING OVER 2 8 0 MILLION CUSTOMERS TO Where 02 retail 03 – happens 02 OUR DESTINATIONS EACH Our Product Experience Framework is embedded across everything we do, YEAR providing a unique point of differentiation to our operational model. -

Thanet District Transport Strategy 2015-2031

Thanet District Transport Strategy 2015-2031 Draft Version 2 July 2018 Thanet District Transport Strategy 2015-2031 (Draft) Contents Foreword Introduction Executive Summary 1 Introduction 1 1.1 Role and Purpose of the Transport Strategy 1 1.2 Policy Context 1 1.3 Roles and Responsibilities 3 2 Geographical Context 4 2.1 Local Geography 4 3 Spatial Characteristics 5 3.1 Social, Economic and Environmental Character 5 3.2 Settlements 6 3.3 Margate 6 3.4 Broadstairs 7 3.5 Ramsgate 7 3.6 Westwood 8 4 Existing Transport Network 9 4.1 Road 9 4.2 Rail 9 4.3 Bus 11 4.4 Community Transport 13 4.5 Sea 14 4.6 Walking 15 4.7 Cycling 15 5 Key Transport Challenges and Options 17 5.2 Existing Travel Patterns 17 5.3 Supporting Expansion at the Port of Ramsgate 19 5.4 Economic Situation 18 5.5 Car Parking Strategy 19 5.6 Quality of Life 23 5.7 Thanet Parkway Rail Station 24 6 Traffic Challenges 26 6.2 M2 / A2 / A299 - Brenley Corner 26 6.3 B2050 / B2190 - Spitfire Junction 27 6.4 A28 / B2055 / B2051 Marine Terrace / Marine Parade 27 6.5 A256 / A255 - Dane Court Roundabout 28 6.6 B2052 - Coffin House Corner 28 6.7 Westwood Cross 29 6.8 A254 / B2052 Victoria Traffic Signal Junction 29 6.9 A28 / Birchington Square 30 6.10 A255 St Lawrence Junctions 31 6.11 A256 Haine Road / Westwood Road Corridor 31 7 Air Quality 32 Thanet District Transport Strategy 2015-2031 (Draft) 8 Planned Development 34 8.2 Key Development Sites 34 9 The Action Plan 37 9.1 Addressing Challenges 37 9.2 Improving The Local Highway Network 37 9.3 The Inner Circuit Route Improvement Strategy