Vectura Group Plc Annual Report and Accounts Particle Generation Technology Vectura Group Plc Annual Report and Accounts 2004/5 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Cboe UK Healthcare Sector Index BUKHLTH

Cboe UK Healthcare Sector Index BUKHLTH Page 1 August 2021 Cboe Exchange This sector represents products and services that are designed, developed, and utilized in the promotion of health and well-being, including medical services, health plans, medical devices, and biopharmaceuticals. The parent index is the Cboe UK All Companies (BUKAC). The index base level is 10,000 as of December 31st, 2010. This is a price return index. Objective The index is designed for use in the creation of index tracking funds, derivatives and as a performance benchmark. Investability Liquidity Transparency Availability Stocks are selected and Stocks are screened to Uses a transparent, rules-based Calculation is based on weighted to ensure that the ensure that the index is construction process. Index price and total return index is investable. tradable. Rules are freely available on the methodologies, both real cboe.com/europe/indices -time, intra-second and website. end of day. Statistics Index ISIN Ticker RIC Currency Cboe UK Healthcare Sector DE000SLA1DJ6 BUKHLTH .BUKHLTH GBP Cboe UK Healthcare Sector - net DE000SLA18F5 BUKHLTHN .BUKHLTHN GBP Volatility Volatility (1y) 0.1776 Returns(%) 1M 3M 6M YTD 1Y 3Y 5Y BUKHLTH 2.03 2.35 16.31 7.02 -2.85 13.78 17.14 BUKHLTHN 2.97 3.33 18.35 10.28 0.52 26.24 39.74 Top 5 Performers Country 1 month return % INDIVIOR PLC UNITED KINGDOM 17.70 MEDICLINIC INTERNATIONAL PLC UNITED KINGDOM 12.80 OXFORD BIOMEDICA PLC UNITED KINGDOM 11.38 PURETECH HEALTH PLC UNITED KINGDOM 8.77 VECTURA GROUP PLC UNITED KINGDOM 7.76 Historical Performance Chart 100% 80% 60% 40% 20% 0% 2011 2013 2014 2016 2017 2018 2020 2021 Cboe UK Healthcare Sector (GBP) Cboe UK All Companies (GBP) Cboe.com | ©Cboe | /CboeGlobalMarkets | /company/cboe © 2021 Cboe Exchange, Inc. -

Brown Capital Management International Small Company Fund Schedule of Investments As of December 31, 2020 (Unaudited)

7 Brown Capital Management International Small Company Fund Schedule of Investments As of December 31, 2020 (Unaudited) Shares Value (Note 1) COMMON STOCKS - 96.60% Australia - 6.06% 708,305 REA Group, Ltd. $ 81,287,705 1,464,269 WiseTech Global, Ltd. 34,713,030 116,000,735 Austria - 0.72% 364,651 Schoeller-Bleckmann Oilfield Equipment AG 13,854,217 Canada - 8.81% (a) 1,493,328 Descartes Systems Group, Inc. 87,342,501 (a) 574,515 Kinaxis, Inc. 81,395,267 168,737,768 Denmark - 8.36% 1,718,159 Ambu A/S - Class B 74,226,815 1,231,585 NNIT A/S 24,581,567 412,166 SimCorp A/S 61,259,325 160,067,707 France - 10.09% 1,499,660 Albioma SA 86,106,283 12,180 Esker SA 2,627,739 1,167,698 Interparfums SA 61,268,589 1,412,713 Lectra 43,145,760 193,148,371 Germany - 13.03% (a) 2,470,144 Evotec SE 91,373,934 1,216,343 Nexus AG 75,782,759 548,366 STRATEC SE 82,264,614 249,421,307 Hong Kong - 3.55% 16,666,000 Kingdee International Software Group Co., Ltd. 67,932,795 India - 1.37% 588,229 CRISIL, Ltd. 15,469,415 1,862,265 Emami, Ltd. 10,800,079 26,269,494 Ireland - 1.34% 125,371 Flutter Entertainment PLC 25,562,163 Israel - 3.46% (a) 410,426 CyberArk Software, Ltd. 66,320,737 Italy - 1.62% 1,424,162 Azimut Holding SpA 30,916,548 Japan - 12.95% 245,400 GMO Payment Gateway, Inc. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

Vectura Group Plc Annual Report and Accounts 2017 Annual Report and Accounts 2017 Accounts and Report Annual

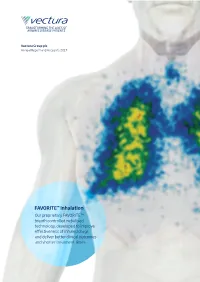

TRANSFORMING THE LIVES OF AIRWAYS DISEASE PATIENTS Vectura Group plc Vectura Group plc Annual Report and Accounts 2017 Annual Report and Accounts 2017 FAVORITE™ inhalation Our proprietary FAVORITE™ breath controlled nebulised technology, developed to improve effectiveness of inhaled drugs and deliver better clinical outcomes and shorter treatment times ASTHMA Asthma is one of the most common non-communicable diseases.1 Asthma is a chronic, reversible disease that inflames and narrows airways in the lungs, causing wheezing, chest tightness and coughing.2 Not all asthma is the same and severe asthma can have a number of underlying causes.3 Triggers4 Dust mites Pets Sulphites in Infections, such Physical activity, foods and drinks as colds including exercise Symptoms Prevalence • Recurring attacks of breathlessness and wheezing that • Asthma is a significant health burden of considerable vary in severity and frequency from person to person5 and growing significance with increasing urbanisation7 • Asthma attacks – a sudden worsening of symptoms, • Estimated 10m adults under the age of 45 affected in Europe9 can be unpredictable and 18.4m adults in the US9 • During an asthma attack, the lining of the bronchial • Prevalence continues to increase and it is estimated that tubes swell, causing the airways to narrow and by 2025 asthma will affect more than 400m people globally10 6 reducing the flow of air into and out of the lungs • Asthma affects people of all ages but most frequently begins in childhood11 14% of the world’s children experience asthma symptoms12 Impact 40–50% • Patients with uncontrolled asthma are significantly of patients are not well controlled14; poor more likely to suffer from poor outcomes and adherence to treatment and device user errors contribute to lack of control 15 medical emergencies • Asthma caused 383,000 deaths in 201513 By 2025 the total asthma market is expected to be worth over $17bn16 1 Latest WHO estimates, released in December 2016, 9 2014; 12; 24: 14009; Centers for Disease, Control and Prevention (CDC). -

Phoenix Unit Trust Managers Manager's Interim Report

PHOENIX UNIT TRUST MANAGERS MANAGER’S INTERIM REPORT For the half year: 2 May 2020 to 1 November 2020 (unaudited) PUTM UK STOCK MARKET FUND (SERIES 3) Contents Investment review 2-3 Portfolio of investments 4-10 Top ten purchases and sales 11 Statistical information 12-14 Statements of total return & change in unitholders’ funds 15 Balance sheet 16 Distribution table 17 Corporate information 18-19 1 Investment review Dear Investor Performance Review Welcome to the PUTM Stock Market Series 3 Unit Trust Over the review period, the accumulation units in the interim report for the six months to 1 November 2020. PUTM Stock Market Series 3 Unit Trust returned 3.35% (Source: SSGA/HSBC for six months to 1/11/20). Over the same period, the FTSE 250 (ex Investment Trusts) Index returned +3.32% (Source: FactSet, FTSE 250 (ex Investment Trusts) Index for six months to 1/11/20). In the table below, you can see how the Fund performed against its benchmark over the last five discrete one-year periods. Standardised Past Performance Nov 19-20 Nov 18-19 Nov 17-18 Nov 16-17 Nov 15-16 % growth % growth % growth % growth % growth PUTM UK Stock Market (Series 3) Unit Trust -16.97 8.69 -5.08 18.76 3.26 FTSE 250 (ex Invt Trust) Index -16.98 8.90 -5.05 19.01 3.55 Source: Fund performance: SSGA and HSBC to 1 November for each year. Benchmark index performance: FactSet, FTSE 250 (ex Invt Trust) Index Total Return, to 1 November for each year. -

Morningstar® Developed Markets Ex-North America Target Momentum Indexsm 18 June 2021

Morningstar Indexes | Reconstitution Report Page 1 of 8 Morningstar® Developed Markets ex-North America Target Momentum IndexSM 18 June 2021 The index consists of liquid equities that display above-average return on equity. The indexes also emphasize stocks with increasing fiscal For More Information: earnings estimates and technical price momentum indicators. http://indexes.morningstar.com US: +1 312 384-3735 Europe: +44 20 3194 1082 Reconstituted Holdings Name Ticker Country Sector Rank (WAFFR) Weight (%) KUEHNE & NAGEL INTL AG-REG KNIN Switzerland Industrials 1 0.50 PostNL NV PNL Netherlands Industrials 2 0.50 Uponor Corporation UPONOR Finland Industrials 3 0.51 Smart Metering Systems PLC SMS United Kingdom Industrials 4 0.50 QT GROUP OYJ QTCOM Finland Technology 5 0.50 ASML Holding NV ASML Netherlands Technology 6 0.51 Vectura Group PLC VEC United Kingdom Healthcare 7 0.50 Lasertec Corp 6920 Japan Technology 8 0.52 Troax Group AB Class A TROAX Sweden Industrials 9 0.48 BayCurrent Consulting Inc 6532 Japan Technology 10 0.50 Sagax AB B Shares SAGA B Sweden Real Estate 11 0.50 Bilia AB A BILIa Sweden Consumer Cyclical 12 0.51 Mycronic AB MYCR Sweden Technology 13 0.49 Protector Forsikring ASA PROTCT Norway Financial Services 14 0.49 AP Moller - Maersk AS B MAERSK B Denmark Industrials 15 0.50 Polar Capital Holdings PLC POLR United Kingdom Financial Services 16 0.51 Secunet Security Networks AG YSN Germany Technology 17 0.50 Hermes Intl RMS France Consumer Cyclical 18 0.50 Kety KTY Poland Basic Materials 19 0.51 ASM Intl ASMI Netherlands Technology 20 0.51 Nippon Yusen KK 9101 Japan Industrials 21 0.54 Dexerials Corp. -

Skyepharma PLC PLC Skyepharma Skyepharma

SkyePharma PLC SkyePharma PLC SkyePharma Making good drugs better Annual Report and Accounts 2009 Registered Head Office Annual Report and Accounts 2009 105 Piccadilly London W1J 7NJ Registered No: 107582 Telephone: +44 (0)207 491 1777 Fax: +44 (0)207 491 3338 Email: [email protected] Web: www.skyepharma.com www.skyepharma.com Making good drugs better Advisers Auditors Depositary Bankers Ernst & Young LLP Bank of New York Mellon HSBC Bank plc Apex Plaza 101 Barclay Street 70 Pall Mall Reading New York NY 10286 London RG1 1YE USA SW1 5EZ Solicitors Joint Corporate Brokers Registrars Fasken Martineau LLP & Financial Advisers Capita Registrars 17 Hanover Square Credit Suisse Northern House London 20 Columbus Courtyard Woodsome Park W1S 1HU London Fenay Bridge E14 4DA Huddersfield Clifford Chance LLP West Yorkshire Welcome to 10 Upper Bank Street Piper Jaffray Ltd HD8 0GA London One South Place E14 5JJ London SkyePharma PLC EC2M 2BR SkyePharma’s mission is to become one of the world’s leading speciality drug delivery companies, powered WARNING TO SHAREHOLDERS – BOILER ROOM SCAMS through excellence in its oral and inhalation technologies. Over the last year, many companies have become aware that their shareholders have received unsolicited phone calls or SkyePharma strives to deliver clinical benefits for patients correspondence concerning investment matters. These are typically from overseas based “brokers”who target UK shareholders, offering to sell them what often turn out to be worthless or high risk shares in US or UK investments. These operations are commonly known as by using its multiple delivery technologies to create “boiler rooms ”. These “brokers”can be very persistent and extremely persuasive, and a 2006 survey by the Financial Services Authority (FSA) has reported that the average amount lost by investors is around £20,000. -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Benchmark Holdings BMK Pharmaceuticals and Biotechnology — GBP 0.605 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 0.7 300 190 1D WTD MTD YTD 0.65 180 Absolute 0.8 1.7 -5.5 -4.7 Rel.Sector 0.2 0.6 -6.9 -9.5 250 170 0.6 Rel.Market -0.3 3.1 -6.1 -12.8 160 0.55 200 150 VALUATION 0.5 140 0.45 Trailing Relative Price Relative Relative Price Relative 150 130 0.4 PE -ve 120 Absolute Price (local (local currency) AbsolutePrice EV/EBITDA 22.3 0.35 100 110 PB 1.5 0.3 100 PCF -ve 0.25 50 90 Div Yield 0.0 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales 4.0 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.4 100 90 90 Div Payout 0.0 90 80 80 ROE -ve 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 The Company is an international animal health, 40 40 40 RSI RSI (Absolute) technical publishing and sustainability business. -

Direct Equity Investments 310315

Security Name ISIN ABERDEEN ASSET MANAGEMENT PLC COMMON STOCK GBP 10 GB0000031285 AMEC FOSTER WHEELER PLC COMMON STOCK GBP 50 GB0000282623 ANTOFAGASTA PLC COMMON STOCK GBP 5 GB0000456144 ASHTEAD GROUP PLC COMMON STOCK GBP 10 GB0000536739 BHP BILLITON PLC COMMON STOCK GBP 0.5 GB0000566504 ARM HOLDINGS PLC COMMON STOCK GBP 0.05 GB0000595859 WS ATKINS PLC COMMON STOCK GBP 0.5 GB0000608009 BARRATT DEVELOPMENTS PLC COMMON STOCK GBP 10 GB0000811801 BELLWAY GBP0.125 GB0000904986 BALFOUR BEATTY PLC COMMON STOCK GBP 50 GB0000961622 BTG ORD GBP0.10 GB0001001592 BIOSCIENCE INVESTMENT TRUST ORD GBP0.25 GB0001121879 BRITISH LAND CO PLC/THE REIT GBP 25 GB0001367019 SKY PLC COMMON STOCK GBP 50 GB0001411924 TULLOW OIL PLC COMMON STOCK GBP 10 GB0001500809 J D WETHERSPOON PLC COMMON STOCK GBP 2 GB0001638955 DIPLOMA ORD GBP0.05 GB0001826634 BOVIS HOMES GROUP GBP0.50 GB0001859296 AVIVA PLC COMMON STOCK GBP 25 GB0002162385 CRODA INTERNATIONAL PLC COMMON STOCK GBP 10 GB0002335270 DIAGEO PLC COMMON STOCK GBP 28.93518 GB0002374006 SCHRODERS VTG SHS GBP1 GB0002405495 ELEMENTIS PLC COMMON STOCK GBP 5 GB0002418548 DCC PLC COMMON STOCK GBP 0.25 IE0002424939 DAIRY CREST GROUP PLC COMMON STOCK GBP 25 GB0002502812 BAE SYSTEMS PLC COMMON STOCK GBP 2.5 GB0002634946 DERWENT LONDON PLC ORD GBP 0.05 GB0002652740 BRITISH AMERICAN TOBACCO PLC COMMON STOCK GBP 25 GB0002875804 ELECTROCOMPONENTS ORD GBP0.10 GB0003096442 SPECTRIS PLC COMMON STOCK GBP 5 GB0003308607 PREMIER FARNELL ORD GBP0.05 GB0003318416 FENNER PLC COMMON STOCK GBP 25 GB0003345054 FIRSTGROUP ORD GBP0.05 GB0003452173 -

Angle AGL Pharmaceuticals and Biotechnology — GBP 1.21 at Close 14 May 2021

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Angle AGL Pharmaceuticals and Biotechnology — GBP 1.21 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 1.3 250 160 1D WTD MTD YTD 1.2 150 Absolute 6.6 6.6 3.9 153.4 Rel.Sector 6.0 5.5 2.2 140.7 1.1 140 Rel.Market 5.4 8.0 3.1 132.0 200 130 1 120 0.9 VALUATION 110 0.8 150 100 Trailing Relative Price Relative 0.7 Price Relative 90 PE -ve 0.6 Absolute Price (local currency) (local Price Absolute 80 100 EV/EBITDA -ve 0.5 70 PB 8.3 0.4 60 PCF -ve 0.3 50 50 Div Yield 0.0 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales +ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.1 100 100 100 Div Payout 0.0 90 90 90 ROE -ve 80 80 80 70 Index) Share 70 Share Sector) Share - - 70 60 60 DESCRIPTION 60 50 50 50 The principal activity of the Company is 40 40 RSI RSI (Absolute) 40 commercialising a platform technology that can 30 30 capture cells circulating in blood which are related to 20 30 20 cancer diagnostics and foetal health. -

Zurich Artemis UK Smaller Companies ZP

We've written this fund factsheet assuming you have some experience of investing. This means that although we have tried to write as much as possible in plain language, we may have used certain words or phrases that might not be familiar to you, particularly if you are new to investing. Its purpose is to help you understand how the fund is invested and performing. You should not use it on its own for making investment decisions. It is not an offer to buy or sell any investments or shares. If there's something you don't understand, please contact your adviser. If you don't have an adviser, please call us, we can help you find one near you. Zurich Artemis UK Smaller Companies ZP September 2021 Fund objective Zurich fund information The Artemis UK Smaller Companies fund (the underlying 'Fund') aims to grow capital over a (as at 31/08/2021) 5 year period. It can also invest up to 20% in bonds, cash and near cash, other transferable securities, other funds (up to 10%) managed by Artemis and third party funds, money Launch date 15/08/2005 market instruments and derivatives. The Fund may use derivatives for efficient portfolio Single price 373.30p management purposes to reduce risk, manage the fund efficiently. The Fund invests in the Fund size (£m) 0.6 (as at 31/08/2021) United Kingdom, including companies in other countries that are headquartered or have a ABI Sector UK Smaller Companies significant part of their activities in the United Kingdom. Fund Charges* 0.76% SEDOL B0C3FW3 The manager adopts a long-term investment approach and seeks to mostly invest in SEDOL codes © London Stock Exchange, reproduced under license companies with predictable and/or growing cashflow streams which require little additional Mex ID ADUSM capital to sustain.